Battery Metals: The Strategic Investment Case for 2026

Battery metals face supply chain concentration risk. Nickel and graphite investments offer asymmetric returns as EV demand surges and Western policy supports new supply.

- Most mineral and metal prices are forecast to edge higher in 2026 driven by stabilizing global growth, reduced trade tensions, and sustained net-zero sector demand, with base and battery metals expected to outperform.

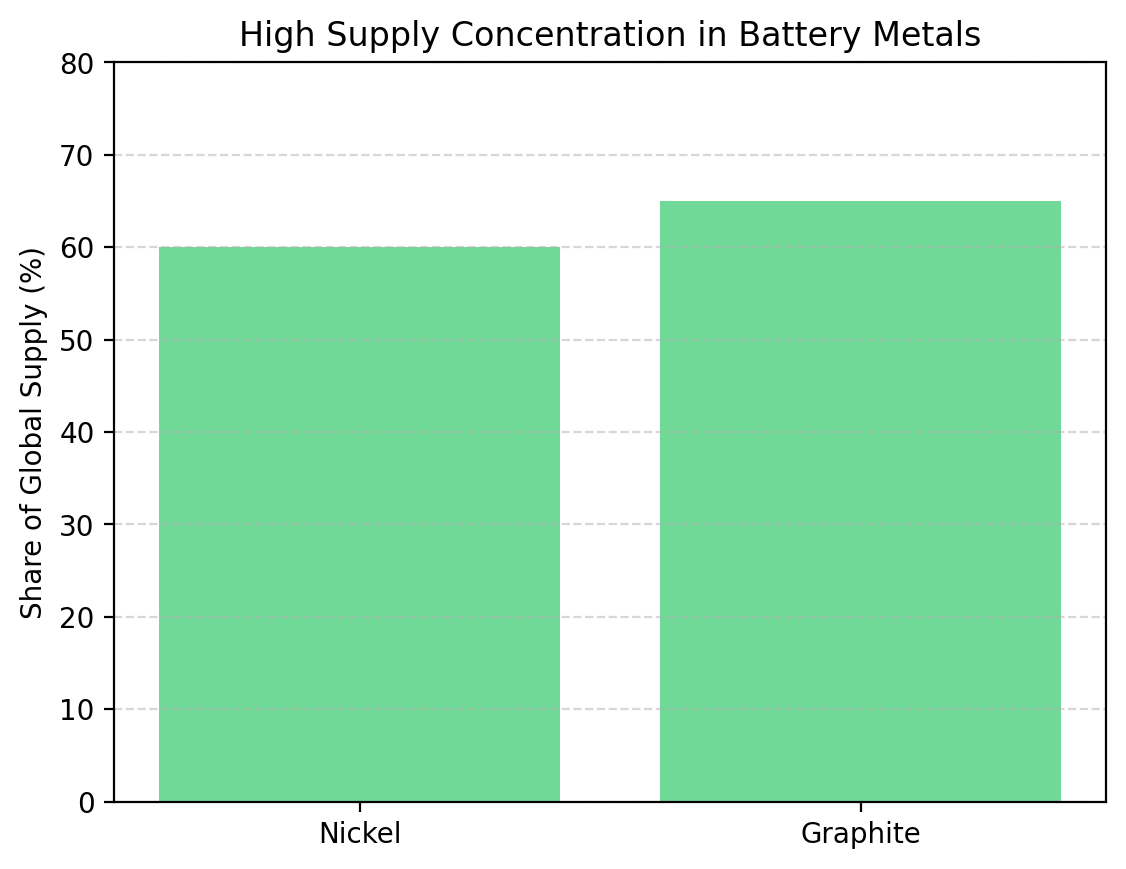

- Indonesia controls over 60% of global nickel supply while China dominates graphite production and processing, creating OPEC-style concentration risk that drives Western government support for alternative supply sources.

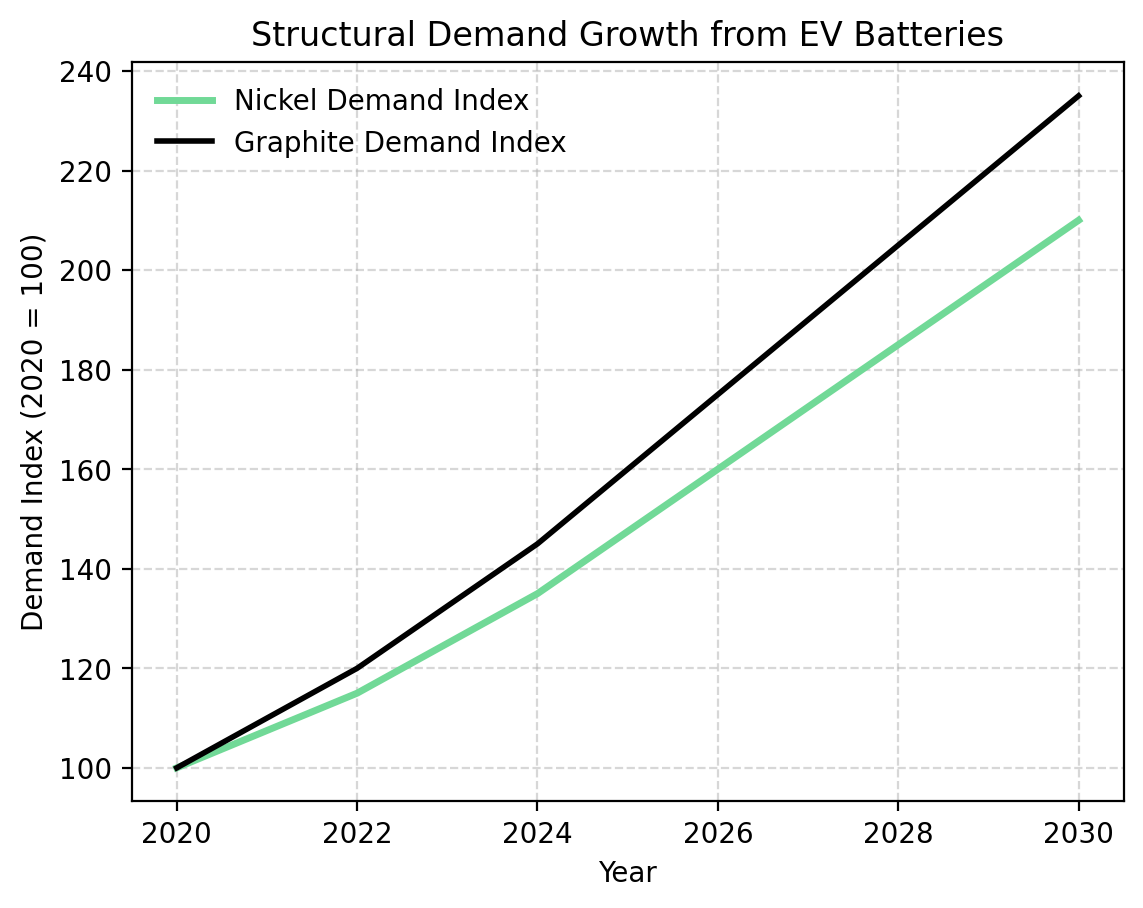

- Nickel demand is forecast to grow at over 7% annually and double to 5-6+ million tonnes by 2030, while new supply development outside Indonesia and China remains constrained by financing difficulties and long permitting timelines.

- Western projects must demonstrate first-quartile costs to secure financing, with Canada Nickel (US$0.39/lb), Lifezone Metals (US$3.36/lb), and Sovereign Metals' by-product model offering structural advantages.

- Government investment tax credits, national priority designations, and carbon sequestration capabilities provide economic support and premium valuations for projects demonstrating net-zero production profiles.

The Energy Transition Imperative Is Still Relative

The global energy transition is no longer a future aspiration but a present economic reality, and battery metals sit at the heart of this transformation. As governments worldwide commit to net-zero emissions targets and automotive manufacturers accelerate electric vehicle production, the demand for critical minerals has shifted from cyclical commodity exposure to structural growth story. Nickel and graphite, two essential components of lithium-ion batteries, represent compelling investment opportunities for 2026 and beyond.

The investment thesis for battery metals extends beyond simple demand growth. It encompasses supply chain security, geopolitical risk management, technological advancement, and the intersection of climate policy with industrial strategy. Unlike previous commodity cycles driven primarily by Chinese infrastructure spending or Western housing booms, the current battery metals cycle is characterized by multi-decade secular demand growth, government intervention to secure strategic supply chains, and a fundamental restructuring of global energy systems.

This article examines the investment case for battery metals, with particular focus on nickel and graphite markets, company case studies from Canada Nickel Company, Lifezone Metals, and Sovereign Metals, and actionable investment implications for portfolio managers and individual investors navigating this complex sector.

Global Market Dynamics: A Favorable Setup for 2026

The broader commodity price environment provides a supportive backdrop for battery metals investment in 2026. According to forecasts from BMI, most mineral and metal prices are expected to average higher in 2026 compared with 2025. This outlook is underpinned by several key factors: stabilizing global economic growth following the volatility of recent years, declining trade frictions as tariff uncertainties that peaked in 2025 continue to ease, and robust demand from net-zero related sectors that is projected to offset structural weaknesses in traditional industrial demand.

Within this broader commodity context, base and battery metals are positioned to outperform. Copper, aluminum, lithium, nickel, and other critical metals are expected to see supportive demand from electrification and clean energy projects, even as traditional demand drivers like Chinese property development remain subdued. Precious metals including gold and silver are forecast to average higher early in the year, though upside may be capped later in 2026 as monetary easing loses momentum and the U.S. Federal Reserve pauses its rate-cutting cycle.

The policy dimension of commodity markets has become increasingly important. Trade policy and tariff actions, including possible U.S. measures on refined metals, remain risks that could affect prices and global flows. However, the general direction of policy in Western economies is toward securing strategic mineral supply chains rather than restricting them, creating a fundamentally supportive environment for non-Chinese production.

Nickel Market Analysis: Supply Concentration Meets Surging Demand

The nickel market presents one of the most compelling supply-demand imbalances in the battery metals complex. Nickel demand has been growing at over 7% annually in the early part of this decade, with forecasts projecting that global nickel demand will double to between 5 and 6 million tonnes per annum by 2030. This growth is driven overwhelmingly by electric vehicle battery production, where nickel serves as a key component in nickel-manganese-cobalt (NMC) and nickel-cobalt-aluminum (NCA) battery chemistries that offer high energy density.

The supply side of the nickel market is characterized by extreme geographic concentration that creates both risks and opportunities. Indonesia has emerged as the dominant global nickel supplier, controlling over 60% of worldwide production. However, this concentration has created what industry observers have termed an "ONEC" situation, analogous to OPEC's historical influence over oil markets. The Indonesian government has implemented shorter mining licenses, tightened environmental regulations, and introduced export management policies that can influence global supply availability.

China's role adds another layer of complexity. While China is not a major nickel ore producer, Chinese companies control much of Indonesia's processing capacity and dominate the refining of nickel into battery-grade materials. Against this backdrop, Western nickel projects face both opportunity and challenge. The opportunity lies in serving customers who are willing to pay a premium for supply chain security and who benefit from government incentives designed to onshore critical mineral processing.

Graphite Market Analysis: Natural Graphite's Essential Battery Role

Natural graphite occupies a unique position in the battery supply chain. While it receives less attention than lithium or nickel, graphite is actually the largest component by weight in lithium-ion batteries, comprising the anode material that stores lithium ions during charging. The battery industry currently relies on a mix of natural graphite (sourced from mining) and synthetic graphite (produced from petroleum coke), with natural graphite generally preferred for its lower cost and reduced carbon footprint when sourced responsibly.

China's dominance in the graphite supply chain is even more complete than in nickel. China produces approximately 65% of the world's natural flake graphite and controls nearly 100% of the processing and purification capacity required to convert flake graphite concentrate into battery-grade spherical graphite. The challenge for non-Chinese graphite developers has traditionally been twofold: competing on cost with Chinese production and building downstream processing capacity that requires hundreds of millions of dollars in capital investment and technical know-how that has been closely held within China.

However, the strategic calculus is changing rapidly. Western governments have recognized graphite as a critical mineral and are implementing policies to encourage domestic production and processing. Battery manufacturers are increasingly willing to enter long-term offtake agreements for non-Chinese graphite supply, even at premium prices, to satisfy customer requirements for supply chain transparency and to qualify for government incentives that often exclude Chinese content.

Company Case Studies

Canada Nickel's Company Building a Nickel District

Canada Nickel Company is developing what may become the Western world's most significant new nickel supply source. The company's flagship Crawford Nickel Sulphide Project in Timmins, Ontario has been recognized as a Canadian federal Major Project and designated a National Priority. According to Wood Mackenzie, Crawford hosts the world's second-largest nickel reserve and resource, and when in production, it is expected to be the third-largest nickel sulphide operation globally with a 41-year mine life.

Mark Selby, Chief Executive Officer of Canada Nickel Company, emphasized the project's competitive positioning:

"Crawford's life-of-mine Net C1 cash cost is projected at approximately US$0.39 per pound of nickel, positioning it in the first quartile of the global cost curve. This cost advantage is critical in an environment where Indonesian production has reset global cost expectations."

The company's most innovative strategy is its focus on carbon sequestration and "NetZero Nickel" production. Canada Nickel is pursuing three parallel carbon storage pathways: in-process tailings carbonation using proprietary IPT technology, NetCarb Alliance partnerships, and a carbon injection pilot with the University of Texas and the U.S. Department of Energy's ARPA-E program. If successful, these initiatives could enable Crawford to achieve a net-negative carbon footprint, providing meaningful competitive advantage as automotive manufacturers increasingly focus on Scope 3 emissions reduction.

Lifezone Metals: World-Class Economics & Advanced Timeline

Lifezone Metals combines a world-class nickel asset with proprietary hydrometallurgical processing technology. The company's Kabanga Nickel Project in Tanzania demonstrates exceptional economics, with the July 2025 Feasibility Study reporting an after-tax net present value of US$1.58 billion, an internal rate of return of 23.3%, and all-in sustaining costs of US$3.36 per pound of payable nickel. Lifezone holds 84% ownership with full operational control, while the Government of Tanzania holds the remaining 16%.

Chris Showalter, Chief Executive Officer of Lifezone Metals, has positioned Kabanga as strategically critical to Western supply chains:

"Nickel is critical to U.S. industries including batteries for AI and data infrastructure, aerospace, defense and nuclear applications. Indonesia dominates production and China-backed investment controls refining, creating rare earth-like dependency risk that Kabanga directly addresses."

Lifezone has made substantial execution progress, raising US$75 million in H2 2025 to fully fund pre-Final Investment Decision activities. The company reported zero health, safety, environment, or security incidents during the period while expanding camp capacity to 300 personnel and advancing geotechnical drilling programs. The timeline is clearly articulated: Q1 2026 for procurement strategy finalization and tender issuance, mid-2026 for Final Investment Decision and financial close, positioning Kabanga for first production in 2028-2029.

Sovereign Metals: Redefining Graphite Development Economics

Sovereign Metals has taken a different approach by developing Kasiya in Malawi primarily as a rutile project with graphite as a significant by-product. This strategy addresses the fundamental challenge of graphite development: competing on cost with Chinese producers without building expensive downstream processing facilities. The asset hosts the world's largest known rutile resource and second-largest known flake graphite resource, with Rio Tinto as a strategic investor providing validation and technical expertise.

Dr. Julian Stephens, Managing Director of Sovereign Metals, articulated the differentiation strategy:

"Kasiya's weathered saprolite mineralization offers significant processing advantages over hard-rock deposits. We're a mining company, not a chemistry company. Our by-product cost position allows us to compete even in current market conditions without requiring downstream integration."

The Optimized Pre-Feasibility Study emphasizes the incremental graphite cost of production concept, representing additional operating cost beyond the rutile circuit. This positions graphite revenue as highly margin-accretive to project economics. The low-sulphur content of Kasiya graphite is particularly valuable for battery applications, while the favorable flake size distribution commands premium pricing. The Q4 2025 Definitive Feasibility Study completion represents the next major milestone.

The Investment Thesis for Battery Metals

- Allocate 40-50% of battery metals portfolio to large-cap producers for stable commodity exposure, strong balance sheets, and dividend yield while accepting lower growth potential.

- Allocate 30-40% to companies like Canada Nickel, Lifezone Metals, and similar developers with projects approaching construction decisions within 24-36 months, completed feasibility studies, strategic partnerships, and government support.

- Limit graphite investment to 10-15% of portfolio, prioritizing by-product business models like Sovereign Metals that compete on cost without expensive downstream processing requirements.

- Use significant nickel price declines as accumulation opportunities, increasing allocation to high-quality developers by 20-30% while focusing on companies with strong balance sheets and first-quartile cost structures.

- Track investment tax credits, national priority designations, and government funding commitments as signals of which projects will successfully navigate financing and permitting challenges.

- Construct portfolios with exposure across multiple development stages, jurisdictions, and commodities, limiting single company exposure to 5-10% of battery metals allocation.

The investment case for battery metals in 2026 rests on multiple mutually reinforcing trends: structural demand growth driven by the energy transition, supply chain concentration that creates strategic vulnerability and pricing power for new entrants, cost curve dynamics that favor low-cost projects with competitive advantages, and policy support from Western governments seeking to secure critical mineral supply chains. The broader commodity price outlook with most mineral and metal prices expected to edge higher provides a supportive macro backdrop.

Company selection is critical for success. Canada Nickel Company, Lifezone Metals, and Sovereign Metals represent well-conceived approaches to battery metals development, each with completed feasibility studies, strategic partnerships with major players, and management teams capable of executing complex projects. However, all three require successful financing, permitting, and construction execution to realize their potential, making ongoing monitoring of development milestones essential.

For investors, the key takeaway is that battery metals warrant meaningful portfolio allocation as a structural growth theme with multiple drivers beyond simple commodity price appreciation. Success requires selectivity, patience, and ongoing monitoring of project development milestones, financing progress, and commodity price trends. The energy transition is a multi-decade process that will create sustained demand for battery metals, and investors positioned in high-quality projects with competitive cost structures, strong management teams, and supportive government environments are well-placed to benefit from this transformation.

TL;DR

Battery metals investment offers compelling risk-reward as the energy transition accelerates. Most mineral prices are forecast to rise in 2026 according to BMI and Fitch Solutions, with battery metals benefiting from structural EV demand growth. Nickel demand is expected to double by 2030, but Indonesian supply concentration creates strategic vulnerability and opportunities for Western projects. Canada Nickel Company's Crawford project offers world-class scale, first-quartile costs, and carbon sequestration innovation. Graphite faces Chinese dominance, but Sovereign Metals' by-product model and cost advantages provide competitive differentiation. Investors should combine large-cap producer exposure with selective development-stage positions in projects with government support, strategic partnerships, and proven management teams. Policy support and supply chain security concerns will drive capital allocation toward non-Chinese battery metals sources throughout 2026.

FAQs (AI-Generated)

Nickel is a key component in battery chemistries offering high energy density critical for electric vehicle range, while graphite serves as the anode material and is actually the largest component by weight in lithium-ion batteries.

Primary risks include commodity price volatility, development-stage execution challenges, financing difficulties following sector valuation resets, potential battery chemistry changes, and Chinese supply expansion that could pressure prices.

Canada Nickel focuses on large-scale nickel with carbon sequestration in tier-one Canadian jurisdiction, Lifezone offers superior economics and advanced timeline in Tanzania with proprietary processing technology, while Sovereign pursues graphite as by-product to rutile in Malawi with strategic investor backing.

Government policy has become increasingly determinative through investment tax credits, national priority designations, and strategic minerals programs that influence project economics, financing availability, and customer willingness to enter long-term offtake agreements.

Canada Nickel targets construction decision by year-end 2026 with first production targeted for year-end 2028, Lifezone targets mid-2026 Final Investment Decision with production in 2028-2029, while Sovereign targets Q4 2025 Definitive Feasibility Study completion with production likely 2028-2029.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

.jpg)

Stay Informed