Big Tech Demands More Uranium from Suppliers: Where is it Coming From?

Nuclear investment and uranium supply crisis create compelling multi-decade investment opportunity as tech demand meets structural shortfalls

- The uranium sector has reached a critical inflection point where supply fundamentals are tightening while demand surges from artificial intelligence energy requirements, climate commitments, and energy security concerns, shifting market focus from demand uncertainty to acute supply shortage recognition.

- Technology giants are entering nuclear markets seeking reliable, carbon-free baseload power for energy-intensive operations, bringing unprecedented institutional demand and substantial capital resources that traditional utility customers typically lack.

- Persistent supply-side challenges throughout 2025 have resulted in multiple producers issuing downward guidance revisions across various jurisdictions, while global uranium production remains below consumption levels and development timelines spanning 10-20 years limit supply response capabilities.

- Sophisticated institutional investors managing billions in assets are entering uranium markets through favorable financing structures, validating the sector's structural transformation while providing capital for strategic growth initiatives at terms previously unavailable to uranium companies.

- Geopolitical considerations and resource nationalism are creating strategic advantages for suppliers in stable, allied jurisdictions, while operational excellence has emerged as the primary value differentiator between successful producers and development-stage projects facing technical uncertainties.

The uranium sector stands at a critical inflection point where supply fundamentals are tightening while demand surges from an unexpected quarter. The convergence of artificial intelligence energy requirements, climate commitments, and energy security concerns is creating a compelling investment landscape for uranium exposure. Multiple indicators suggest the market has shifted from questioning demand fundamentals to recognizing acute supply shortages, positioning well-managed uranium companies for significant value creation.

Technology Sector Drives Unprecedented Demand Growth

The most significant development transforming uranium markets is the entry of technology giants seeking reliable, carbon-free baseload power for energy-intensive operations. Microsoft's recent investment in restarting Three Mile Island Unit 2 and its membership in the World Nuclear Association represents an interesting involvement in an undersupplied market.

"Big tech is just so important and it's so good to see them starting to get involved at the industry level. These tech companies, they just absolutely want to deliver their products in the most green emission-free way and they see nuclear as a solution for safe green power at a large scale with incredible uptime." - Premier American Uranium's CEO Colin Healey

Interview with Colin Healey, CEO of Premier American Uranium

The scale of this technological demand shift cannot be overstated. As observed at the 2025 World Nuclear Association Symposium, the presence of Microsoft at the nuclear industry gathering demonstrates how buoyant, festive energy has replaced previous years' cautious optimism.

Additionally, IsoEnergy's Philip Williams explained that while downstream sectors see investment and expansion,

"You can have all the conversion capacity in the world, all the enrichment capacity in the world, all the nuclear plants being coming online or being planned to be built, but if you don't have the fuel at the beginning, then it's all irrelevant." - IsoEnergy Director & CEO Philip Williams

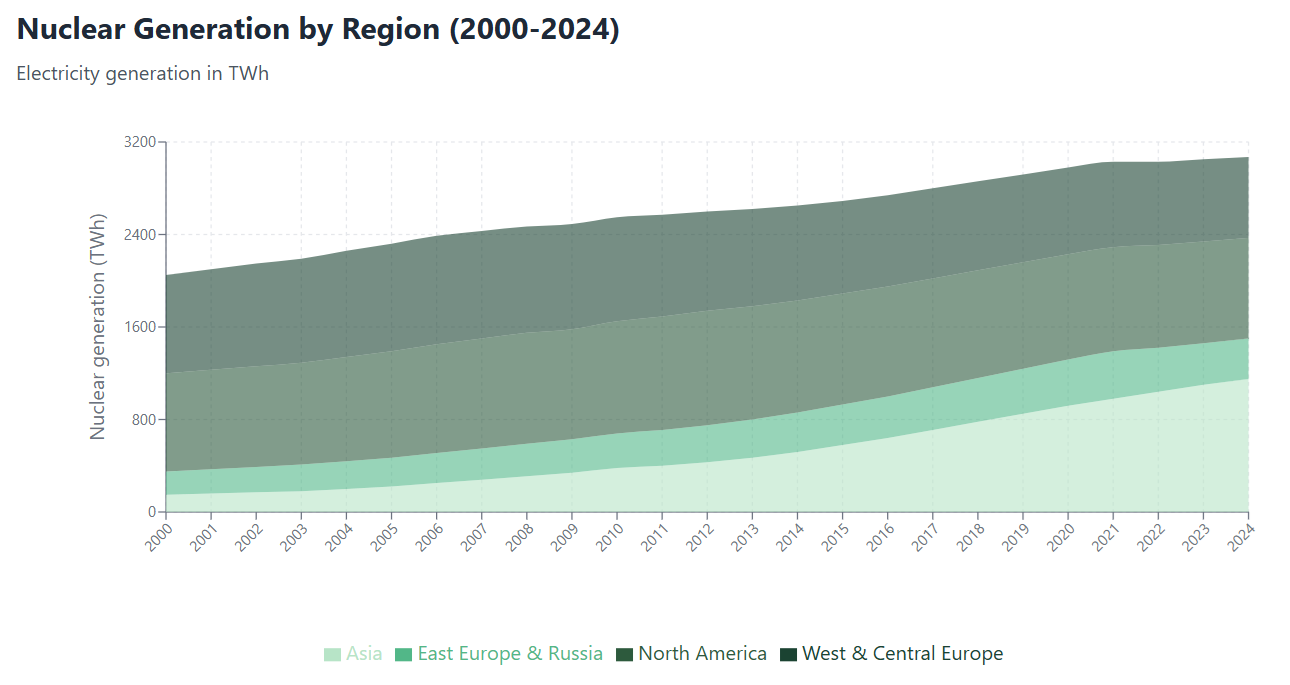

The timing of this institutional embrace coincides with years of uranium underinvestment following the Fukushima incident. Global uranium production remains below consumption levels, while utility inventory drawdowns have masked the supply deficit. As artificial intelligence and data center expansion accelerate, power consumption requirements are growing exponentially, making nuclear energy's 24/7 reliability increasingly valuable compared to intermittent renewables.

The Supply Chain Investment Thesis

The uranium industry has experienced persistent supply-side challenges throughout 2025, with multiple producers issuing downward guidance revisions across various jurisdictions. When producers operate below nameplate capacity, their fixed costs spread across fewer pounds, creating higher per-unit costs that the market has yet to fully recognize.

These operational challenges extend beyond simple production metrics to fundamental supply-demand mathematics. As Munro noted from the WNA conference, the analysis revealed an absolute undeniable conclusion showing insufficient uranium availability even under conservative demand scenarios.

“The reason why I’m being very blunt about this supply-demand deficit… is that it is an absolute undeniable conclusion that’s coming out of this conference. We anticipate that these conditions will provoke a contracting cycle… certain utilities will realise the best way they can mitigate shortage scenarios into the 2030s is to start restocking and getting back to more comfortable levels.” - Bannerman Energy's Executive Chairman Brandon Munro

The supply constraints compound through multiple vectors. Kazakhstan's Kazatomprom has confirmed reduced production targets, eliminating speculation about returning to full capacity levels. Several junior mining companies experienced operational setbacks, while major producers faced various constraints limiting output expansion.

Energy Fuels' recent results illustrate both the challenges and opportunities within this constrained environment. The company's exceptional performance at the Pinyon Plain mine, producing uranium at grades of 2.23% U3O8, demonstrates the value premium commanded by successful operations.

"The exceptional production at this mine is a 'once in a lifetime event' and has come at the perfect time as it places us in the enviable position of increasing production while lowering costs." - Energy Fuels' CEO Mark Chalmers

Geopolitical Advantages Create Strategic Premiums

Russia and USA will maintain significant uranium inventory impact over the next few 15 years. Other countries like UK despite having stocks but with marginal quantities and lack of clear options to utilize their material. Resource nationalism and supply chain security considerations increasingly influence uranium purchasing decisions, creating strategic advantages for suppliers in stable, allied jurisdictions.

Geopolitical factors particularly benefit non-aligned countries like Namibia, which gain flexibility unavailable to restricted suppliers. As Munro observed, unlike Canadian producers restricted from selling to certain markets, suppliers from countries like Namibia can serve all markets globally. US domestic production remains insufficient for growing demand, necessitating imports from allied jurisdictions. Canada represents the preferred supplier, but Canadian production faces domestic demand growth from SMR deployment plans.

Interview with Market Expert & Chairman of Bannerman Energy, Brandon Munro

This geographic positioning provides both broader customer bases and pricing premiums from supply-constrained regions. The bifurcated market structure creates multiple opportunities for strategically positioned suppliers, with U.S. market access commanding premiums due to security considerations while other markets provide volume opportunities.

Lotus Resources' operations in Malawi and planned development in Botswana illustrate these advantages. Lotus Resources has demonstrated operational competency by successfully restarting uranium production at the Kayelekera mine, a previously producing asset that operated until 2014. The company invested approximately $50 million in restart capital to bring the operation back online to steady-state production of 2.4 million pounds annually by 2026.

Niger's new mineral code, affecting Global Atomic's Dasa project has dropped the royalties while maintaining other favorable terms:

"They've dropped the royalties from 12% to 7%. The corporate tax is still the same at 30%. When you take the whole project into account, the Niger people get a fair share." - Global Atomic President & CEO Stephen G. Roman

This regulatory stability, combined with strong community relations and government support, creates sustainable operating environments that command valuation premiums.

The convergence of technological demand, supply constraints, and geopolitical considerations creates a multi-decade growth framework for uranium investments. As Roman notes about development timelines taking 10-20 years from development to production, suggesting sustained supply constraints supporting uranium prices and valuations for producing assets.

Interview with Stephen Roman, CEO & President of Global Atomic

Current market dynamics favor companies with operational excellence, financial flexibility, and strategic positioning in stable jurisdictions. IsoEnergy's diversified portfolio approach, spanning Canada, the United States, and Australia, provides what CEO Williams describes as multiple value propositions:

"Do you want near-term cash flow? We have it. Do you want high value exploration in the best place in the world, the Athabasca Basin? Do you want call optionality with large or high-grade projects? We've got that." - IsoEnergy Director & CEO Philip Williams

The sector's asymmetric risk-reward profile attracts institutional capital seeking exposure to supply-demand imbalances. Unlike previous commodity cycles driven primarily by demand growth, current uranium fundamentals reflect supply insufficiency regardless of demand scenarios, providing downside protection while maintaining substantial upside potential.

Interview with Philip Williams, CEO of IsoEnergy

Sophisticated Capital Allocation Attracts Institutional Investment

- Energy Fuels maintains a robust balance sheet with over $250 million of liquidity including $71.49 million of cash and cash equivalents, $126.41 million of marketable securities, and no debt. The company holds substantial uranium inventory of 1,875,000 pounds of U3O8, positioning the company to capitalize on anticipated higher uranium prices rather than immediate sales.

- enCore Energy successfully secured $115 million through convertible notes at a 5.5% coupon rate, which Executive Chairman William Sheriff describes as financing not seen before in the uranium sector.

- Global Atomic has secured term sheets from both the US Development Finance Corporation and an Eastern joint venture partner for project financing. The company has already invested approximately $250 million in the Dasa project, meeting the DFC's 40% capital contribution requirement for their financing structure.

- IsoEnergy maintains $85 million in cash and strategic backing from NextGen Energy, which owns 31% of the company and contributed $12 million to a recent $50 million financing. The company's New York Stock Exchange listing has opened access to U.S. institutional investors while Canadian flow-through share structures facilitate exploration funding.

- Premier American Uranium's increasing scale through the Nuclear Fuels acquisition provides enhanced financial flexibility for additional strategic opportunities while maintaining disciplined capital allocation. CEO Colin Healey notes that each transaction becomes less dilutive, allowing the company to pursue more advanced or expensive acquisitions.

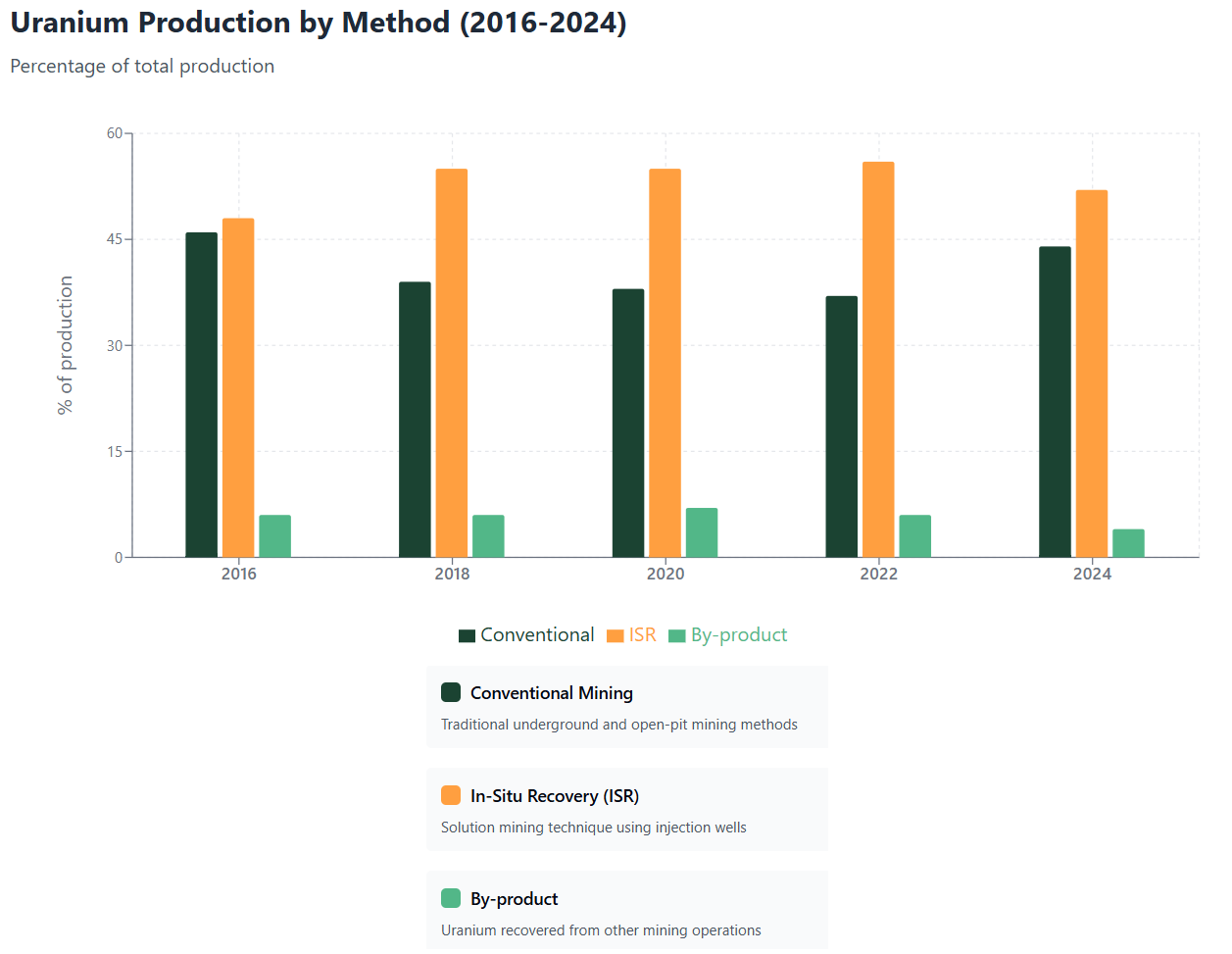

Production Method Evolution

In-Situ Recovery Mining

In-situ leaching, also known as solution mining, or in situ recovery (ISR), involves leaving the ore as it is in the ground, and recovering the minerals from it by dissolving them and pumping the pregnant solution to the surface where the minerals can be recovered. Since 2018, above 50% of world uranium mined was from by in situ leach.

enCore Energy's transformation demonstrates the operational leverage available to successful ISR operators when properly managed. The company reduced average well completion times from over seven days to just 1.3 days, a metric Sheriff considers rather profound because it directly correlates to production capacity. enCore Energy's combined with expansion from 12-14 rigs to 29 currently operating, these improvements resulted in production increases of 200% to up 300% on a daily basis.

"In order to up your production, you've got to get more wells in the ground. More wells, more fluid flow, more uranium going through the plant, higher recovery, higher daily production rate."

Interview with William Sheriff, Chairman of enCore Energy

Denison Mines' Wheeler River-Phoenix in-situ recovery (ISR) mine represents what President & CEO David Cates describes as the first new large-scale mine in the Athabasca basin in decades, targeting mid-2028 production of up to 9 million pounds annually. The structure's effectiveness becomes apparent in stress-testing scenarios. Beyond dilution protection, the financing provides cost advantages, Cates notes:

"We estimate this structure saves us over a hundred million less on interest cost compared to the best conventional project-secured project finance that we could have gotten as an alternate."

The rapid recovery characteristics of ISR operations accelerate cash flow but require constant drilling ahead of production to maintain output levels.

Interview with David Cates, President & CEO of Denison Mines

Hard Rock Mining Renaissance

While in-situ recovery (ISR) operations have historically dominated uranium production discussions, recent technical difficulties across multiple ISR projects are creating renewed appreciation for proven hard rock mining approaches. In 2024, uranium coming from conventional mining method has increased and reaching more than 40% of the global supply.

Lotus Resources' successful restart of the Kayelekera mine in Malawi exemplifies this trend, with Managing Director Greg Bittar explaining:

"We are hard rock small open pit mining operation. This plant performed before. So in production through to 2014, we spent a lot of time reviewing the records, but also with a number of people that we brought back in from the previous operations."

This operational approach provides several advantages, including proven metallurgy, established processing parameters, and reduced technical risk compared to newer extraction methods that have experienced industry-wide technical challenges. The company has built significant contingencies into its production schedule, acknowledging that restart operations require careful risk management while providing superior predictability compared to ISR operations facing unexpected technical difficulties.

Interview with Greg Bittar, MD of Lotus Resources

The contrasting experiences highlight how operational excellence, rather than extraction method alone, determines investment success. Companies demonstrating consistent production capabilities command significant premiums over development-stage projects facing technical uncertainties, regardless of whether they employ ISR or conventional mining approaches.

The Investment Thesis for Uranium

- Strategic Market Position: Uranium markets have shifted from demand uncertainty to supply shortage recognition, creating asymmetric investment opportunities where downside protection exists regardless of demand scenarios while maintaining substantial upside potential from technological adoption and supply constraints.

- Institutional Validation: Sophisticated institutional investors managing $10-30 billion are entering uranium markets, validating the sector's structural transformation while providing capital for strategic growth initiatives at favorable terms previously unavailable to uranium companies.

- Technology Sector Catalyst: Microsoft's nuclear investments and World Nuclear Association membership signal unprecedented demand from technology companies requiring reliable baseload power for AI and data centers, bringing substantial capital resources and urgency that traditional utility customers lack.

- Operational Differentiation: Companies demonstrating consistent production capabilities command significant premiums over development-stage projects, with operational excellence becoming the primary value differentiator as supply constraints intensify across both ISR and conventional mining approaches.

- Geopolitical Premium: Suppliers in stable, allied jurisdictions gain strategic advantages through geographic positioning, regulatory stability, and supply chain security considerations, with non-aligned producers capturing pricing premiums from supply-constrained regions.

- Supply Scarcity Value: Global uranium production remains below consumption levels with multiple producers facing operational challenges, creating scarcity value for successful operators while development timelines of 10-20 years limit supply response to current market signals.

- Portfolio Diversification: Uranium exposure provides portfolio diversification benefits through exposure to nuclear power's essential role in clean energy transitions, energy security objectives, and emerging technological infrastructure requirements.

- Actionable Investment Strategy: Focus on established producers with proven operational track records, companies in stable jurisdictions with government support, and developers with strategic utility relationships positioned to benefit from accelerated contracting cycles expected as supply constraints intensify.

The uranium sector's transformation from speculative investment theme to strategic necessity reflects fundamental shifts in energy infrastructure requirements and supply chain security priorities. The convergence of artificial intelligence energy demands, climate commitments, and geopolitical considerations creates compelling investment opportunities for companies positioned to capitalize on structural supply-demand imbalances. Technology sector adoption, exemplified by Microsoft's nuclear investments, provides unprecedented demand growth while supply constraints create scarcity value for successful operators. Institutional capital recognition of these dynamics, combined with operational differentiation and geopolitical advantages, positions well-managed uranium companies for sustained value creation across multiple market cycles.

Analyst's Notes

Subscribe to Our Channel

Stay Informed