Technology Sector's WNA Commitment Signals Uranium's Strategic Value as Energy Security Priority

AI drives uranium demand while supply struggles. Advanced developers in stable jurisdictions with strong balance sheets positioned for significant gains.

- The uranium sector is experiencing unprecedented demand from major technology companies investing billions in nuclear energy infrastructure to power artificial intelligence data centers, representing a fundamental shift from traditional utility-driven demand cycles to sustained corporate infrastructure investments.

- Global uranium supply faces persistent constraints as established producers consistently fail to meet production guidance due to operational complexities, while new project development requires 15-20 year timelines that cannot address current supply shortfalls.

- The United States confronts a critical strategic deficit, consuming 50 million pounds of uranium annually while producing only 4-5 million pounds domestically, creating dependence on foreign suppliers during heightened geopolitical tensions.

- Government policy support has intensified with uranium designated as a critical mineral, Development Finance Corporation backing for domestic projects, and strategic reserve programs that provide additional demand beyond utility requirements.

- Institutional price targets project uranium above $100 compared to current $70 spot prices, while sophisticated financing structures address traditional mining dilution concerns and companies with advanced projects in established jurisdictions position for production timing advantages.

The uranium sector stands at a critical inflection point where fundamental supply-demand dynamics are creating what industry veterans describe as the most favorable market conditions in over a decade. The convergence of artificial intelligence-driven energy demand, persistent supply constraints, and government policy support for domestic production creates a multi-faceted investment thesis that extends beyond traditional commodity cycles.

Technology Sector Catalyses Nuclear Renaissance

The most significant development reshaping uranium demand comes from an unexpected source: the technology sector's embrace of nuclear energy to power artificial intelligence infrastructure. Microsoft's decision to join the World Nuclear Association represents more than symbolic support. Dev Randhawa, CEO of F3 Uranium, explains the strategic imperative:

"Whoever wins the race to have more scalable green energy has a better chance of winning the AI wars."

The scale of corporate commitment validates this strategic shift. Amazon has donated $500 million to small modular reactor development while signing comprehensive nuclear supply agreements. Meta has similarly positioned itself in the nuclear space. These companies collectively possess market capitalisations exceeding entire stock exchanges, creating unprecedented capital flows into nuclear infrastructure.

The energy requirements are substantial and sustained. According to Randhawa, one SMR can run 700,000 homes or a data center. Nuclear energy represents the only baseload, scalable, and carbon-free power source capable of meeting AI data centers' consistent electricity demands. Unlike renewable sources that require backup power or storage solutions, nuclear provides the reliable, 24/7 energy density that artificial intelligence applications require.

This demand evolution differs fundamentally from previous uranium cycles driven primarily by utility procurement or financial speculation. Technology companies are making long-term infrastructure investments that create sustained consumption rather than cyclical purchasing patterns. The resulting demand profile provides greater visibility and durability than traditional utility contracting cycles.

Structural Supply Constraints Create Investment Opportunity

While demand accelerates from new sources, the supply response has proven consistently disappointing across established producers. David Cates, CEO of Denison Mines, offers a candid assessment:

"We've got Kazatomprom, it's had multiple years now of struggles achieving production guidance. Cameco recently announcing that they'll fall short this year as well."

The restart challenges facing established producers highlight the complexity of uranium production. Cates uses an automotive analogy:

"It's a bit like taking a used car out of storage, right? Like a new car, usually reliable. That's why you want one, has a warranty with that kind of stuff. The used car - and then putting it in storage - and then trying to bring it back to life, it's not that easy. And then when you do get it back to life, it's still a car that's been driven for whatever kilometers it was."

In-situ recovery operations face particular technical challenges across multiple jurisdictions. As Kazakhstan struggles with sulfuric acid cost inflation, Paladin encounters algae issues in Namibia. These difficulties span globally, suggesting systemic rather than isolated operational challenges. The supply picture becomes more concerning when considering the limited pipeline of new projects. Philip Williams, CEO of IsoEnergy, notes:

"It takes 10 years minimum by the time you explore and develop a project, and probably more like 15 or 20 years"

This extended development horizon means current supply constraints will persist even with immediate investment in new projects.

The challenges extend beyond simple operational difficulties to fundamental cost misunderstanding. Williams argues that the actual real price of getting that marginal pound of production out of the ground is much higher. When producers operate below nameplate capacity, fixed costs spread across fewer pounds create higher per-unit costs that current market pricing fails to reflect.

"Every day that goes by, we think it increases in value in both because the urgency for it to come online will only increase, but also we're obviously bullish on the market," Williams adds.

America's Strategic Uranium Deficit

The United States faces a particularly acute uranium supply challenge that creates strategic vulnerabilities and investment opportunities. Stephen Roman, CEO of Global Atomic, quantifies the deficit:

"US utilities are burning 50 million pounds a year while domestic production capacity reaches only 4-5 million pounds a year when fully ramped."

This 45-50 million pound annual deficit occurs at precisely the moment when geopolitical tensions heighten concerns about supply chain security. The Trump administration's response includes designating uranium as a critical mineral and implementing Defense Production Act provisions favoring domestic development. Roman reports that since the Trump administration has come in, there's been a complete change of attitude in the United States. Secretary of State Marco Rubio's leadership of the Development Finance Corporation signals high-level government commitment to uranium supply security. Roman notes,

"The administration right up to Secretary of State Marco Rubio knows about our project. This has been basically blessed by the White House, the State Department and various others in the administration."

The government policy support extends beyond strategic declarations to concrete financial backing. The Development Finance Corporation provides project funding for uranium developments that align with national security objectives, while strategic reserve programs create additional demand sources beyond utility requirements.

Investment success in uranium requires careful attention to asset quality and jurisdictional advantages. The most compelling opportunities exist in established uranium-producing regions with proven geology and existing infrastructure.

Bruce Lane, CEO of American Uranium, emphasizes geological continuity:

"When it comes down to geological discontinuity and depositional challenges, the projects in Wyoming around us - it's produced more pounds than any other project in Wyoming, and we're in that geology."

However, even aggressive domestic production scenarios cannot eliminate import dependence. This structural deficit ensures continued dependence on allied suppliers, particularly Canada's Athabasca Basin, creating investment opportunities for companies with advanced projects in stable jurisdictions.

Superior Asset Quality in the Established Athabasca Basin

Technical advantages extend beyond geology to operational expertise. Teams with decades of experience in specific jurisdictions possess knowledge that reduces execution risk compared to companies operating in unfamiliar territories. This expertise becomes particularly valuable as the industry faces widespread operational challenges.

- F3 Uranium exemplifies the discovery potential within the established Athabasca Basin. The company has achieved its fourth discovery at the Tetra zone, with initial results showing 0.4% uranium grades at both conductor system ends.

- Denison Mines' final regulatory approval for its Wheeler River Phoenix ISR mine alongside its $345 million convertible bond offering demonstrates evolution. Cates estimates the structure saves over a hundred million less on interest cost compared to the best conventional project-secured project finance. This cost efficiency translates directly to improved project economics and shareholder returns.

- IsoEnergy's $85 million in cash and strategic backing from NexGen Energy provides flexibility to optimise development timing rather than being forced into premature decisions by capital constraints.

Market Timing and Price Discovery

The uranium sector has developed sophisticated financing structures that address traditional mining investment concerns, particularly dilution risk associated with capital-intensive development projects.

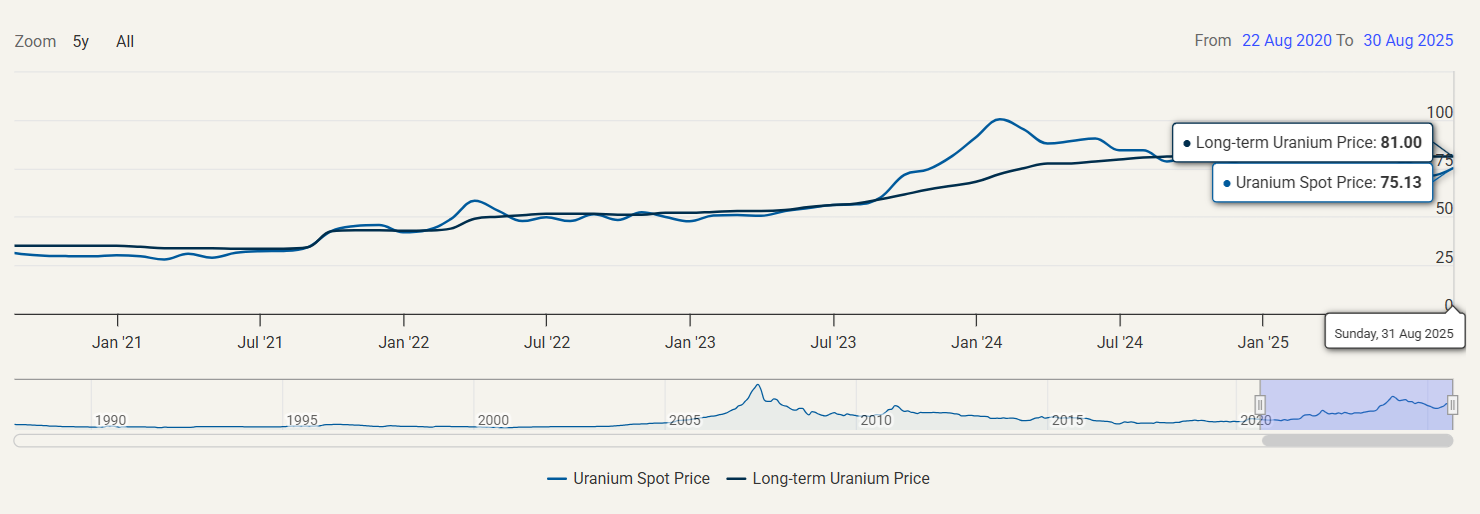

Institutional price targets suggest significant upside potential from current uranium pricing levels. Randhawa references Citibank's recent report that they expect uranium past $100 by the end of this year compared to current spot prices around $70. This price appreciation potential reflects the fundamental supply-demand imbalance rather than speculative positioning.

Companies approaching production can benefit from the incredible value to being in production having uncommitted or market exposed production during supply shortages. This first-mover advantage allows producers to capitalize on price discovery rather than being locked into historical contract terms.

Demand drivers continue strengthening from technology sector requirements and from the proliferation of AI data centers and broader electrification initiatives creates sustained electricity demand growth to which nuclear becomes the key. American Uranium Bruce Lane notes:

"Clearly the forecast for electricity demand is driving the need to find every kind of energy source and nuclear's in the frame."

The sector consolidation potential creates additional value catalysts. Established producers require additional resources to fulfil long-term utility contracts and maintain operational capacity, creating acquisition opportunities for companies with advanced projects and proven teams.

The Investment Thesis for Uranium

- Strategic Exposure Through Advanced Developers: Focus on companies with proven management teams, advanced projects in established jurisdictions, and strong balance sheets that can execute development plans without dilutive financing pressure.

- Geographic Diversification Across Allied Nations: Prioritise exposure to uranium projects in stable, allied jurisdictions including Canada's Athabasca Basin, Wyoming's established uranium districts, and Australia's uranium provinces to mitigate geopolitical risks.

- Portfolio Approach for Risk Management: Consider companies offering exposure to multiple development stages and assets rather than single-project developers to reduce execution risk while maintaining upside potential across various market scenarios.

- Technology Sector Demand Recognition: Invest in the structural demand shift from AI and data center growth rather than traditional utility-driven cycles, recognising this creates more sustained consumption patterns.

- Supply Constraint Beneficiaries: Target companies positioned to benefit from industry-wide production challenges and extended development timelines that create barriers to new supply additions.

- Government Policy Alignment: Focus on projects that align with national security objectives and benefit from government support programs including strategic reserves, Development Finance Corporation backing, and critical mineral designations.

- Balance Sheet Strength Priority: Emphasize companies with adequate funding to complete development plans without additional equity dilution during potentially volatile market conditions.

- Timing Optimization: Enter positions before regulatory approvals and production decisions that create step-change revaluations from developer to producer status.

Key Takeaways

The uranium investment opportunity reflects a convergence of structural demand growth, supply constraints, and policy support that creates compelling risk-adjusted return potential. The technology sector's embrace of nuclear energy provides demand visibility that extends beyond traditional utility procurement cycles, while persistent supply challenges and extended development timelines limit competitive responses.

Companies with advanced projects in established jurisdictions, proven management teams, and strong financial positions appear best positioned to capitalise on these favourable market dynamics. The sector's evolution toward more sophisticated financing structures addresses traditional mining investment concerns while government policy support provides additional validation for the strategic importance of uranium supply security.

Technology companies including Microsoft, Amazon, and Meta are committing unprecedented capital to nuclear energy infrastructure, creating sustained demand beyond traditional utility cycles. Simultaneously, established producers struggle with operational challenges while new project development timelines span decades, constraining supply responses. The uranium sector in 2025 presents a compelling investment opportunity driven by artificial intelligence infrastructure demands, structural supply deficits, and government policy support for domestic production. Companies with advanced projects in established jurisdictions, proven management teams, and strong balance sheets appear well-positioned to capitalsze on these fundamental market dynamics.

Analyst's Notes

Subscribe to Our Channel

Stay Informed