Calidus Resources (CAI) - Gold Production YE/21

Calidus Resources is an ASX listed gold exploration and development company which controls the 1.25 M ounce Warrawoona Gold Project in Western Australia.

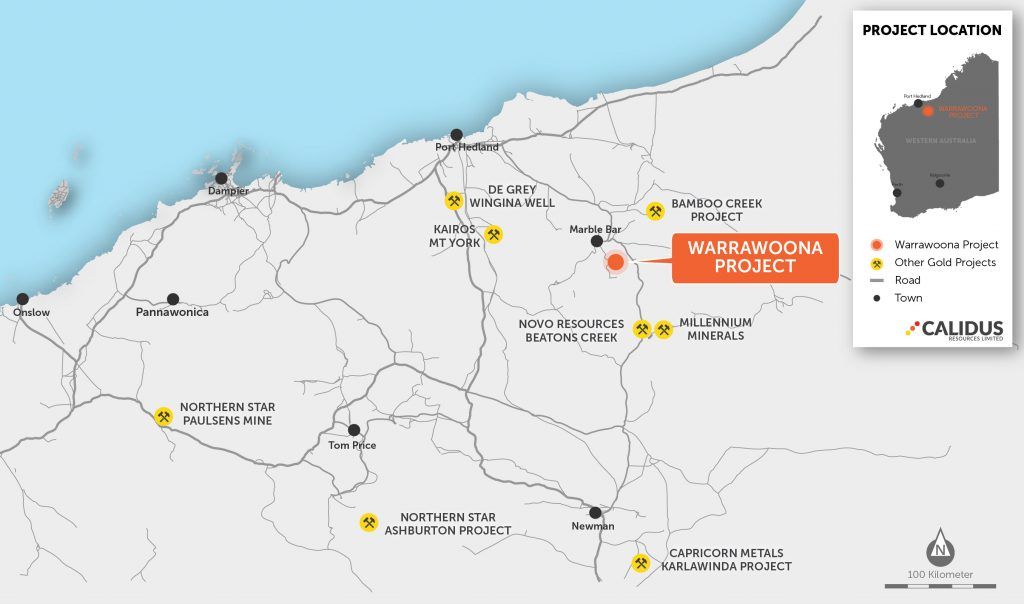

Calidus Resources (ASX:CAI) is an ASX listed gold exploration and development company which controls the 1.25Moz Warrawoona Gold Project located in the East Pilbara district of the Pilbara Goldfield in Western Australia.

The Directors believe that the recent consolidation of this goldfield will transform the Company into a new Australian gold development company with significant potential to unlock further resources and new discoveries within the emerging gold belt of the Pilbara Goldfields district, which is a historically proven gold mining region.

This experienced team of mine builders at Calidus are planning an accelerated time frame for plant build, which means that Calidus is aiming to be in production by YE/21. Reeves is succinct and to the point and is tight-lipped about how they are progressing with regard to the timing and costs of financing.

What we discuss and when:

0:00 - Introduction

1:11 - Market VS Company: Reasons for Doubling of the Share Price

1:40 - Company Overview

2:11 - Short-cutting the Process: Update on Progress

4:22 - Cost of Money: Raises, Debt, & Market Reaction

7:26 - Red Flags & Potential Issues to Overcome

9:16 - Ramp Up & Growth; Production Levels & Aims

11:21 - Acquisition of Blue Spec: Reasoning & Plans. More M&A to Come?

14:36 - Re-Rate Potential; Why Should Investors Consider Calidus?

17:49 - Alkane Resources: Importance of Relationship

Overview

Calidus Resources, listed on the ASX, is developing the Warrawoona gold mine next year in Western Australia, in the Pilbara, at around a 90,000oz per annum mine, peaking up to 105,000oz per annum. It will be a low-cost, high-margin mine now starting construction.

A lot has happened recently, and it’s obviously a great market for gold so Calidus did tap into that with a A$25M raise. In the meantime, they have the Environmental Protection Agency approval and ministerial sign offs that have allowed them to commence the building work. He says that the access road, the village installation, water and comms, etc. is happening right now and that they’ve applied for the operating permits for next year. The other big news is that Calidus has signed a binding term sheet to acquire a very high-grade satellite deposit nearby that they see bringing in to the greater Warrawoona project and increasing ounce production per annum and cash flows.

Calidus realise that the more debt you take on, the better for current shareholders, the less dilution and the better NPV per share. They are trying to minimise future equity Reeves says and that if you look at the cheapest debt versus the most expensive, on an NPV per share basis, it's less than 5% difference between them. So, the cost of that debt, is actually irrelevant and it's the quantum of the debt that really impacts returns for current shareholders.

Pilbara Goldfields - Calidus Resources Ltd. Oct '20

Warrawoona

Calidus has an experienced team of mine builders and they are taking ownership of this development. They have 2 very well-known contractors in Australia, who've built the last few gold plants in Western Australia and are tried and tested contractors with good balance sheets.

Reeves states that they are aiming for up to 90,000oz for the first 6-years of the 8-year life of the mine (LOM) on average and they aim to peak at 105,000oz in the 6th year of production. On top of this, their Blue Spec acquisition is where they see another 30,000oz-40,000oz per annum coming on top. So they are in the region of 120,000oz-130,000oz per annum in that time. Those deposits are open, the Klondyke is open, and the mine life will go for a lot longer, he says, but what they want to do is add production in the near term, add cash flow and leverage that infrastructure they'll be putting in to maximise returns.

Location of the Warrawoona Gold Project - Calidus Resources Ltd. Oct '20

Blue Spec

Reeves tells us that as part of the project, they have a big conventional free milling plant which produces gold bars at sort of 2Mt-2.4Mt per annum, but on the side of it they have a little 100,000t per annum flotation plant for small high-grade refractory deposits like at Blue Spec. They plan to start that plant up for a year, produce a concentrate for sale from one of these ore bodies they have nearby, and shut it down. Blue Spec has stibnite, antimony, so they can produce an antimony gold concentrate, at a very high-grade and get paid 100% of the gold value. The antimony pays for that smelting, and they can utilise that infrastructure for another 5 to 7-years so they can use their infrastructure to its maximum.

Reeves says that if they are looking at 40,000oz per annum for instance and you used a similar all in sustaining cost (AISC), at about AUD$60M to AUD$70M a year. Even if we say US$50M a year, extra cash flow, without any extra CAPEX bar the start of the underground at Blue Spec.

Land Acquisition

Calidus made the land acquisition because of its huge accretive value explains Reeves. There will be increased production, increased cash flow and it will pay for itself for a few months once it's in production. Once they have a mill, and become the dominant player in the East Pilbara, they can leverage off it and potentially buy more land. In the short term though, they have lots of exploration to do on their current tenement package but if an opportunistic acquisition comes up, they will look at it. The focus is on building, producing gold, producing money and at the same time doing exploration to show extra mine life.

Market Excitement

Calidus has looked at a few other companies that have been going through development recently and trying to work out what was the catalyst that released the hand brakes for them. Certainly, getting the funding in place, finalising the permits and just building is important. As you get closer to gold production, the market becomes more excited.

Alkane Involvement

Alkane have been very helpful in getting Calidus into production and Reeves thinks that they will make a lot of money, if they decide to then sell out and can use that money on their own projects. For the Calidus shareholders, the most sensible thing is to get into production and get that value into the share price, comments Reeves and then there will be discussions with Alkane and others.

Reeves concludes by advising us that the next 3-months will be very exciting times for Calidus and that it should be a Happy Christmas for all Calidus shareholders.

To find out more, go to the Calidus Resources website.

Analyst's Notes

Subscribe to Our Channel

Stay Informed