Cerro de Pasco's Quiulacocha DFC Agreement Explained: What a No-Mining Cost Structure Means for Project Economics

Cerro de Pasco’s Quiulacocha project removes ~40% mining costs via tailings reprocessing, backed by DFC funding and potential $300M financing upside.

- Cerro de Pasco Resources secured up to US$5 million in milestone-based development funding from the US International Development Finance Corporation (DFC), which is also evaluating up to US$300 million in potential construction financing for the Quiulacocha Tailings Reprocessing Project.

- The project eliminates what management estimates as roughly 40% of typical mining production costs by extracting already-mined tailings via pontoon-mounted slurry pumps rather than conventional drilling, blasting, and haulage.

- Phase 1 drilling across 40 holes returned an average grade of 5.5 ounces per tonne silver-equivalent, including gallium at 53.2 grams per tonne, a critical mineral for which the US is entirely import-dependent and China controls approximately 98% of global supply.

- The deposit carries a historic estimate of approximately 423 million ounces silver-equivalent across approximately 75 million tonnes, with internal projections suggesting annual profit between $151 million and $650 million depending on throughput and recovery rate.

- Key milestones to monitor include delivery of metallurgical results and recovery upside, Phase 2 drilling across copper, silver, and gold tailings, and any formalisation of the DFC's construction financing beyond its current evaluation stage.

What Has Happened

Cerro de Pasco Resources (TSXV: CDPR) announced a Project Development Funding Agreement with the US International Development Finance Corporation (DFC). The DFC will provide up to US$5 million in milestone-based development funding, with CDPR contributing matching funds on a 1:1 basis, to advance sonic drilling, geotechnical and hydrogeological drilling, a Feasibility Study (FS), and an Environmental and Social Impact Assessment (ESIA) at the Quiulacocha Tailings Reprocessing Project in Peru's Pasco Region. The DFC is also evaluating the possibility of up to US$300 million in long-term direct loan financing for construction, subject to due diligence and final approvals.

The agreement is a material development for a junior company at the pre-feasibility stage. The more instructive signal for investors is what the DFC chose to back: a project whose cost structure is defined by the near-total absence of conventional mining, the activity management estimates account for roughly 40% of typical production costs.

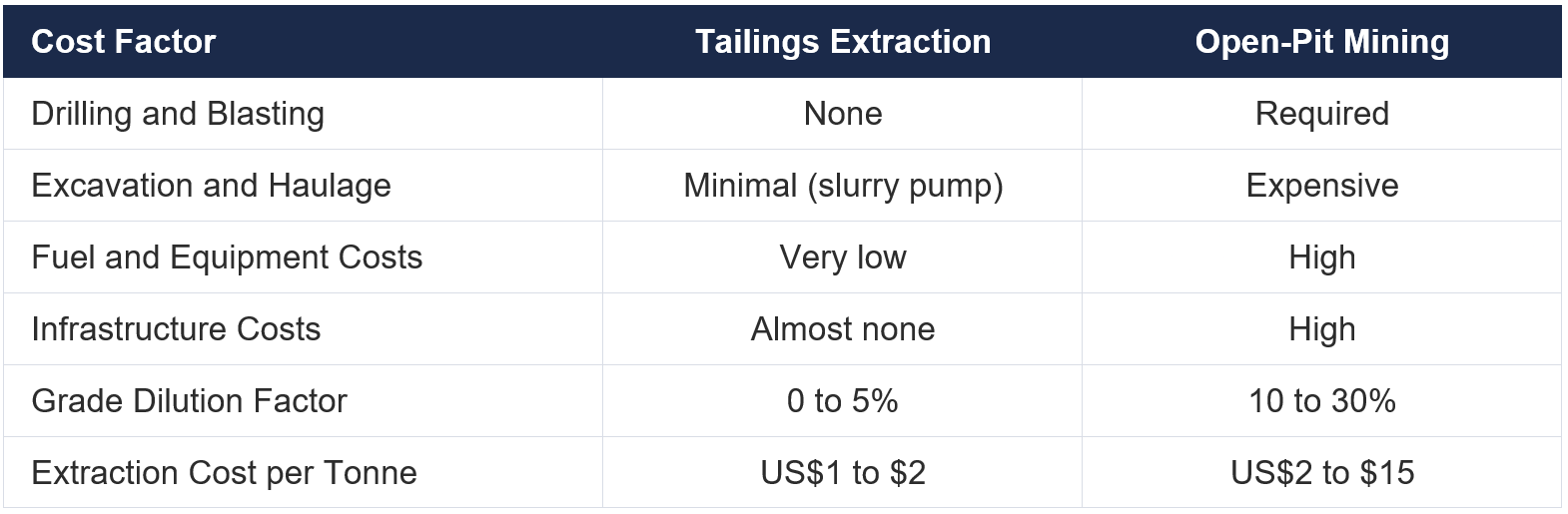

The 40% Problem & Why Quiulacocha Doesn’t Have It

In conventional mining, whether open pit or underground, drilling, blasting, loading, and hauling collectively represent what management estimates as roughly 40% of total production costs. That cost burden is precisely what Quiulacocha does not carry. The project's approximately 75 million tonnes of legacy tailings, held within the El Metalurgista mining concession covering 95.74 hectares in Peru's Pasco Region, have already been mined, processed through flotation circuits, and deposited into a former lake bed. No drilling, blasting, haulage fleet, or waste rock management is required to recover the material.

Chief Executive Officer of Cerro de Pasco Resources, Guy Goulet's assessment of the extraction cost is direct:

"You know what's the problem in the mining business? It's mining. There's no mining here. Count $1 per tonne."

That figure, $1 to $2 per tonne for extraction, against $2 to $15 per tonne for open-pit operations and $30 to $200 per tonne for underground, is the structural foundation of the Quiulacocha investment case, and a key consideration in the DFC's decision to provide structured pre-feasibility development financing.

How You Move 75 Million Tonnes Without a Truck

Because the Quiulacocha tailings sit in a former lake bed, they are fully saturated with water, making conventional dry excavation impractical. A pontoon-mounted submersible slurry pump agitates and draws up a mixture of water and solid material, which is then piped continuously to a processing facility. There are no explosives, no haulage fleet, and no blast-load-haul-dump cycle.

Goulet describes the operational model plainly:

"We're going to bring a pontoon and, we're going to sink those slurry pumps, and we're going to smoothly pump this slurry to either the neighbour facilities or eventually the facilities we're going to build by ourselves."

The contrast with the site's own history is significant. At its peak, the Cerro de Pasco pit extracted 20,000 tonnes per day through round-the-clock blasting, trucking, and haulage. The slurry pump model eliminates all of that, a consideration that carries weight in a district where 67,000 people live directly adjacent to the deposit.

The Cost Comparison in Concrete Terms

The company's internal economic projections, which are not compliant with National Instrument 43-101 (NI 43-101) and should be read as illustrative rather than definitive, outline two scenarios. The base case uses a processing facility at 10,000 tonnes per day, a 40% average metal recovery rate, and a total operating cost of $10 per tonne. At silver priced at $30 per ounce and gold at $2,500 per ounce, that produces an estimated net smelter return (NSR) of $52 per tonne, implying $42 per tonne profit, or approximately $151 million per year at 3.6 million tonnes per annum throughput, and a projected life-of-mine profit of $3.2 billion across 75 million tonnes.

The upper case assumes a purpose-built facility at 20,000 tonnes per day, or 7.2 million tonnes per annum, 70% average metal recovery inclusive of gallium and indium, and an operating cost of $15 per tonne, lifting projected annual profit to approximately $650 million and a projected life-of-mine profit of $6.8 billion across 75 million tonnes. The spread between the two scenarios is driven entirely by recovery rate and throughput, not extraction cost, which remains marginal in both cases.

Why The Tailings Are Rich Enough To Reprocess

The grade of Quiulacocha's residual material is a direct result of how the original operation was run. During the copper era (1906 to 1965), approximately 16,369 thousand tonnes were processed at head grades of 4.0% copper, 200 grams per tonne (g/t) silver, and 3.0 g/t gold. During the polymetallic era (1952 to 1992), approximately 58,299 thousand tonnes were processed at 3.3% lead, 8.6% zinc, and 98 g/t silver. Average flotation recoveries across both periods were approximately 60% for most metals, not because higher recoveries were unachievable, but because extending residence time offered no economic advantage.

Goulet frames the consequence directly:

"When you do flotation, you rapidly recover 60% of your metals within the first 24 hours. If you keep the flotation going for 72 hours, you will end up recovering 85% to 87% of your metals. So why should they avoid an extra 48 hours to recover an extra 25% while they can recover 60% every 24 hours? They were throwing that rich material away."

The 40-hole Phase 1 drilling campaign confirmed the result: an average grade of 5.5 ounces per tonne (oz/t) silver-equivalent across all holes, with silver at 1.66 oz/t, zinc at 1.47%, lead at 0.89%, and gallium at 53.2 g/t. Across all metals, the deposit carries a historic estimate of approximately 423 million ounces of silver-equivalent. Phase 2 drilling, targeting copper, silver, and gold tailings, is a stated 2026 priority as the company advances toward feasibility.

What the DFC Agreement Signals About This Cost Structure

The US International Development Finance Corporation (DFC) is the United States government's development finance institution, mandated to finance projects advancing US strategic and foreign policy interests in emerging markets. The agreement's structure is notable: the US $5 million in development funding is disbursed in milestones tied to defined technical deliverables, including sonic drilling, geotechnical and hydrogeological drilling, the FS, and the ESIA, with Cerro de Pasco contributing matching funds on a 1:1 basis. These disbursements are reimbursable upon a qualifying financing event. This is structured project development capital with repayment provisions, not grant funding.

The DFC's separate evaluation of up to US$300 million in construction financing is framed explicitly around the US critical minerals supply chain security. Gallium grades of 53.2 g/t across the tailings place the deposit in a strategically relevant category: the US is entirely import-dependent for gallium, and China controls approximately 98% of global primary production.

Executive Chairman Steven Zadka addressed the significance of the agreement directly:

“Few development-stage mining projects rarely receive direct support from the US Government through a structured project development facility of this scale. Quiulacocha combines significant silver and base metals with strategic technology metals in one of Peru’s most historic mining districts.”

The agreement signals that the project's cost structure, strategic metal content, and environmental remediation rationale cleared an institutional due diligence threshold before the FS was complete.

What to Watch Next

The absence of conventional mining costs removes one major variable, but not all of them. The delivery of metallurgical results and recovery upside will determine whether the upper-case economic scenario is technically achievable, defining the most effective processing route for recovering the project's polymetallic resource, including gallium. The FS and ESIA, both required before any development or construction decision, will follow the completion of this technical foundation.

The company's stated 2026 catalysts include Phase 2 drilling across copper, silver, and gold tailings, the formalisation of the claim on surrounding tailings, and progress toward feasibility and development. Any formalisation of the DFC's potential construction financing of up to $300 million, which remains subject to satisfactory due diligence, internal credit approvals, and execution of definitive financing documentation, would represent a material disclosure. Investors should also monitor whether the company moves to expand its mineral rights to government-owned surface areas adjacent to the current El Metalurgista concession boundary, which management has flagged as capable of materially increasing the total resource base.

FAQs (AI-Generated)

The project eliminates drilling, blasting, and haulage by reprocessing already-mined tailings using slurry pumps, removing roughly 40% of typical mining production costs and significantly lowering operating expenses.

The DFC’s milestone-based funding and potential $300 million construction financing signal institutional validation of the project’s economics, strategic relevance, and technical viability before feasibility is complete.

Profitability is primarily driven by recovery rates and processing throughput rather than extraction costs, which remain minimal. Higher recoveries and scale materially increase annual and life-of-mine returns.

Historic processing methods prioritized speed over maximum recovery, leaving significant residual metals in the tailings. Modern techniques can extract this previously unrecovered value.

Key risks include metallurgical recovery performance and feasibility outcomes, while catalysts include Phase 2 drilling, metallurgical results, feasibility study completion, and potential confirmation of DFC construction financing.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed