Chemical Demand Surpasses De-Icing & 42% Market Share Changes How Investors Value Salt Assets

Chemical demand reached 42% of US salt sales in 2025, overtaking de-icing demand and shifting salt-sector risks toward industrial activity.

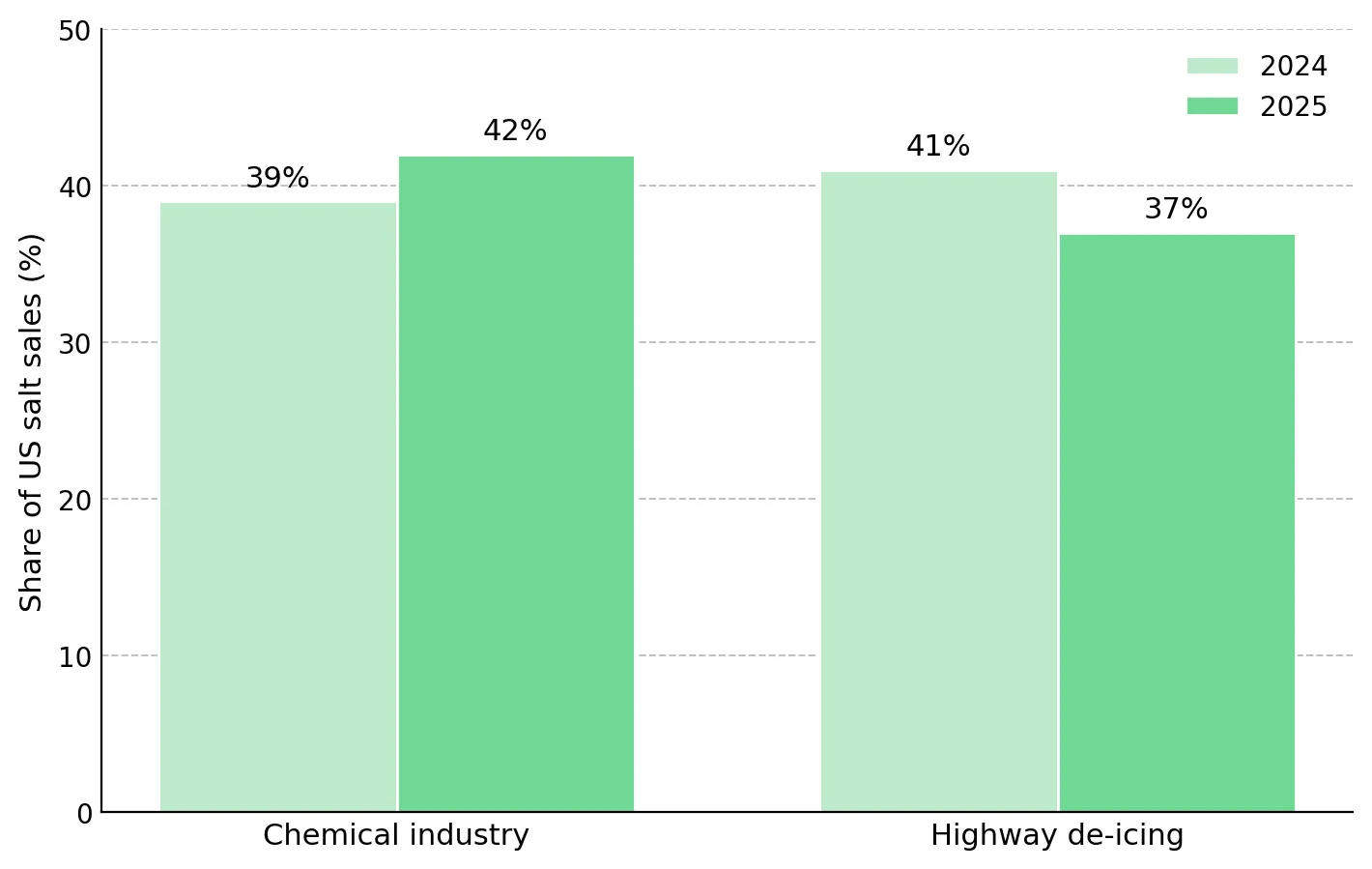

- According to the United States Geological Survey (USGS) Mineral Commodity Summaries 2026, chemical-industry uses accounted for about 42% of US salt sales in 2025, while highway de-icing accounted for about 37%, compared with roughly 39% and 41%, respectively, in 2024.

- Chemical-grade demand tracks industrial output and chlor-alkali production, while de-icing demand depends on winter severity and a North American road-salt market that imports an estimated 8-10 million tonnes annually. As a result, chemical-grade and de-icing salt demand are driven by different end markets and carry different revenue risks.

- Berkshire Hathaway's completed US$9.7 billion acquisition of OxyChem, a top-three US chlor-alkali producer, highlights institutional capital allocation to the chlor-alkali value chain.

- Investors should size positions by end-market and development stage rather than by commodity label, and account for the financing, construction, and execution risks that separate a feasibility study from a producing mine.

Chemical Demand Overtakes De-Icing & Reshapes Salt Market Exposure

USGS Mineral Commodity Summaries 2026 show chemical-industry demand overtook highway de-icing as the largest end market for US salt in 2025, requiring investors to distinguish between chemical-grade and de-icing exposure.

According to the USGS Mineral Commodity Summaries 2026, about 39 million tonnes of salt were sold or used in the US in 2025, with a total value of roughly $2.6 billion. The chemical industry accounted for about 42% of salt sales, with brine representing roughly 90% of that demand. Highway de-icing accounted for about 37% of salt sales. In 2024, those shares were about 39% chemical and 41% de-icing, making 2025 the first year chemical demand exceeded de-icing demand.

The demand shift reflects the fact that de-icing salt and chlor-alkali feedstock serve different end markets. Rock salt serves the de-icing market. Brine is the feedstock for chlor-alkali production, which produces chlorine and caustic soda. USGS free-on-board benchmark values place salt in brine near $11 per tonne, rock salt near $54 per tonne, solar salt near $150 per tonne, and vacuum or open-pan salt near $260 per tonne. As a result, salt assets can face different demand drivers and pricing dynamics despite producing the same commodity.

Chlor-Alkali Demand Becomes the Primary Driver of Salt Market Growth

Chlorine and caustic soda are used in PVC, water treatment, pulp and paper, and alumina refining. As chemical demand becomes the largest end market for salt, sector demand becomes more dependent on industrial output and chlor-alkali margins than on winter weather. This shifts demand risk from weather patterns toward industrial activity and chlor-alkali profitability.

China, the world's largest chlor-alkali market, has more than 53 million tonnes of caustic soda capacity, while industry trackers report weak alumina-sector demand. While the capacity figure comes from industry sources rather than official government data, it points to oversupply risk in the chlor-alkali market. Because chemical demand now exceeds de-icing demand, chlor-alkali oversupply poses a larger risk to salt demand than a mild winter.

Salt Demand Splits Into Industrial & De-Icing Markets With Different Risk Profiles

The demand shift has created two salt markets with different demand drivers and risk profiles. Valuation depends on whether an asset is exposed to chemical-grade demand or the de-icing market.

Chemical-grade salt demand is driven by industrial activity rather than weather. Demand is linked to manufacturing and construction through PVC production and is less affected by winter weather than de-icing salt demand. More predictable demand can support more stable revenue and cash-flow expectations.

Consolidation in the chlor-alkali industry provides one indication of investor interest in chemical-grade demand. Berkshire Hathaway completed its US$9.7 billion acquisition of OxyChem, a top-three US producer of PVC, chlor-alkali, and chlorinated organic chemicals. The transaction suggests large-scale capital remains willing to invest in chlor-alkali assets despite cyclical demand risks. The acquisition reflects confidence in chlor-alkali cash-flow generation rather than a view on short-term salt prices.

A 25-Year Supply Gap Supports New De-Icing Salt Development

De-icing demand is driven by weather and supply availability rather than industrial activity. Demand varies with winter severity, while North American road-salt supply remains constrained by limited new production. No major North American salt mine has opened in roughly 25 years, Cargill's Avery Island closure removed about 2.5 million tonnes of annual East Coast supply, and the region imports an estimated 8-10 million tonnes of road salt each year. As a result, pricing and project economics depend more on supply constraints than on demand growth.

Nolan Peterson, Chief Executive Officer of Atlas Salt Inc., said the long-standing lack of new mine development has created an opportunity to serve a large and undersupplied de-icing market:

"We aim to supply de-icing road salt to the North American market. We will be the first new salt mine built in North America in 25 years."

CityNews Toronto and CBC News reported Ontario wholesale salt prices rising from roughly $65-$70 per tonne to nearly $190 per tonne, with municipalities citing shortages as a public-safety concern. While these reports are regional rather than a national pricing index, they show that supply shortages can drive sharp price increases in the de-icing market.

Producers & Developers Respond to Different Salt Market Drivers

Compass Minerals generates revenue from de-icing, consumer, industrial, and chemical salt markets, giving it exposure to multiple demand drivers. In its fiscal second quarter of 2026, Compass Minerals reported adjusted EBITDA of $86.4 million, up about 3% year over year, and net income of $12.7 million versus a $32.0 million loss a year earlier.

Lower highway de-icing volumes reduced salt-segment operating earnings and adjusted EBITDA by about 3%, prompting Compass Minerals to lower Salt segment guidance while maintaining full-year adjusted EBITDA guidance of $212 million to $236 million.

Diversification reduces exposure to weather-driven earnings swings but does not eliminate it. Chemical and consumer salt sales can offset weaker de-icing demand, allowing investors to value producers against guided cash flows and EBITDA rather than a single winter season.

Single-Asset Exposure Increases Both Upside & Execution Risk

Atlas Salt provides concentrated exposure to the North American de-icing market through a single development-stage asset. The company is developing the Great Atlantic Salt Project in Newfoundland for the North American de-icing market, leaving its future cash flows dependent on road-salt supply and pricing conditions rather than chemical demand. The project contains 95.0 million tonnes of salt at 95.9% purity, with an additional 868 million tonnes reported elsewhere on the property. Because the resource classification of the additional tonnage is not disclosed, it should be treated as upside potential rather than attributable value.

An independent SLR Consulting study estimated an NPV8 of about $920 million, based on an 8% discount rate, with projected after-tax profit of about $188 million per year, initial capital costs of $589 million, and a 4.2-year payback period. All of these figures depend on financing and construction and should be treated as projections rather than realized performance; first production is targeted around 2030.

Cash Flow, NPV & End-Market Exposure Shape Salt Equity Valuations

Valuation approaches can vary depending on a company's stage of development and business profile. For project developers, net present value (NPV) is often used to estimate the value of future cash flows and should be assessed alongside the discount rate assumptions applied. Market capitalization reflects equity value, while enterprise value (EV) provides a broader measure that incorporates net debt.

For a developer, valuation depends on how investors assess the gap between market value and study-stage project value. As of 26 May 2026, Atlas Salt had a market capitalization of roughly $161.1 million versus a study NPV8 of about $920 million. The gap reflects project risk rather than an automatic valuation discount. Investors apply execution and financing risk to a project that has not yet been built, so the study NPV should not be treated as realized value.

Valuation metrics should align with a company's stage of development. For development-stage projects such as Atlas Salt's Great Atlantic Salt Project, risk-adjusted NPV is commonly used to assess potential future value. The project's reported 4.2-year payback period provides an additional indicator of its economics, while the recently announced $10 million bought-deal financing supports continued advancement toward development milestones.

Chemical Demand, Chlor-Alkali Margins & Financing Remain Key Risks

The shift toward chemical demand could prove temporary if 2025 reflects an unusually mild winter, since a severe winter could raise de-icing demand back toward its historical share. Excess Chinese caustic-soda capacity could pressure chlor-alkali margins, while lower shipping costs and greater petrochemical feedstock availability could reduce industry profitability.

The thesis weakens if USGS 2027 data shows de-icing demand exceeding chemical demand, if Chinese oversupply compresses chlor-alkali margins, or if Atlas Salt fails to secure construction financing within its targeted timeline. Junior developers can lose substantial value if financing terms are highly dilutive or project milestones are delayed, making position sizing and diversification important risk-management tools.

The Investment Thesis for Salt

- Chemical demand accounted for about 42% of US salt sales in 2025, exceeding de-icing demand and increasing the sector's exposure to manufacturing, construction, and chlor-alkali activity.

- Chemical-grade demand is tied to industrial activity, while de-icing demand is more sensitive to weather and North American supply shortages.

- North America has not added a major salt mine in roughly 25 years, leaving a supply gap that developers may address if they secure financing and complete construction.

- Berkshire Hathaway's US$9.7 billion acquisition of OxyChem highlights continued investment in chlor-alkali assets despite cyclical demand risks.

- Producers generate current cash flow and can be valued on EV/EBITDA, while developers depend on financing and construction before project economics can be realized.

- Investors should size positions by end-market and development stage rather than by commodity label, because diversified producers and single-asset developers face different cash-flow, financing, and execution risks.

The key development in salt this year is the shift in demand from de-icing toward chemical feedstock. As chemical demand exceeds de-icing demand, salt assets become more dependent on either industrial activity or weather and supply constraints, requiring different valuation approaches. Producers and developers can operate in the same commodity while facing different cash-flow, financing, and execution risks. End-market exposure and development stage, rather than commodity label, should drive position sizing and risk budgeting.

TL;DR

Chemical-industry demand became the largest end market for US salt in 2025, accounting for 42% of sales and surpassing highway de-icing demand for the first time. This shift makes salt markets increasingly dependent on industrial activity and chlor-alkali profitability rather than winter weather alone. As a result, investors must distinguish between chemical-grade and de-icing salt exposure, as each faces different demand drivers and risks. Diversified producers such as Compass Minerals benefit from multiple revenue streams and can be valued using cash-flow metrics, while developers such as Atlas Salt offer leveraged exposure to North American road-salt shortages but carry financing, construction, and execution risks. The key investment takeaway is that end-market exposure and development stage now matter more than the salt commodity label itself.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed