Annual USMCA Reviews Raise Salt Import Reliance, Increasing North American Supply Risk

Annual USMCA reviews, rising salt import reliance, flat domestic supply, and El Niño uncertainty increase North American salt supply risk.

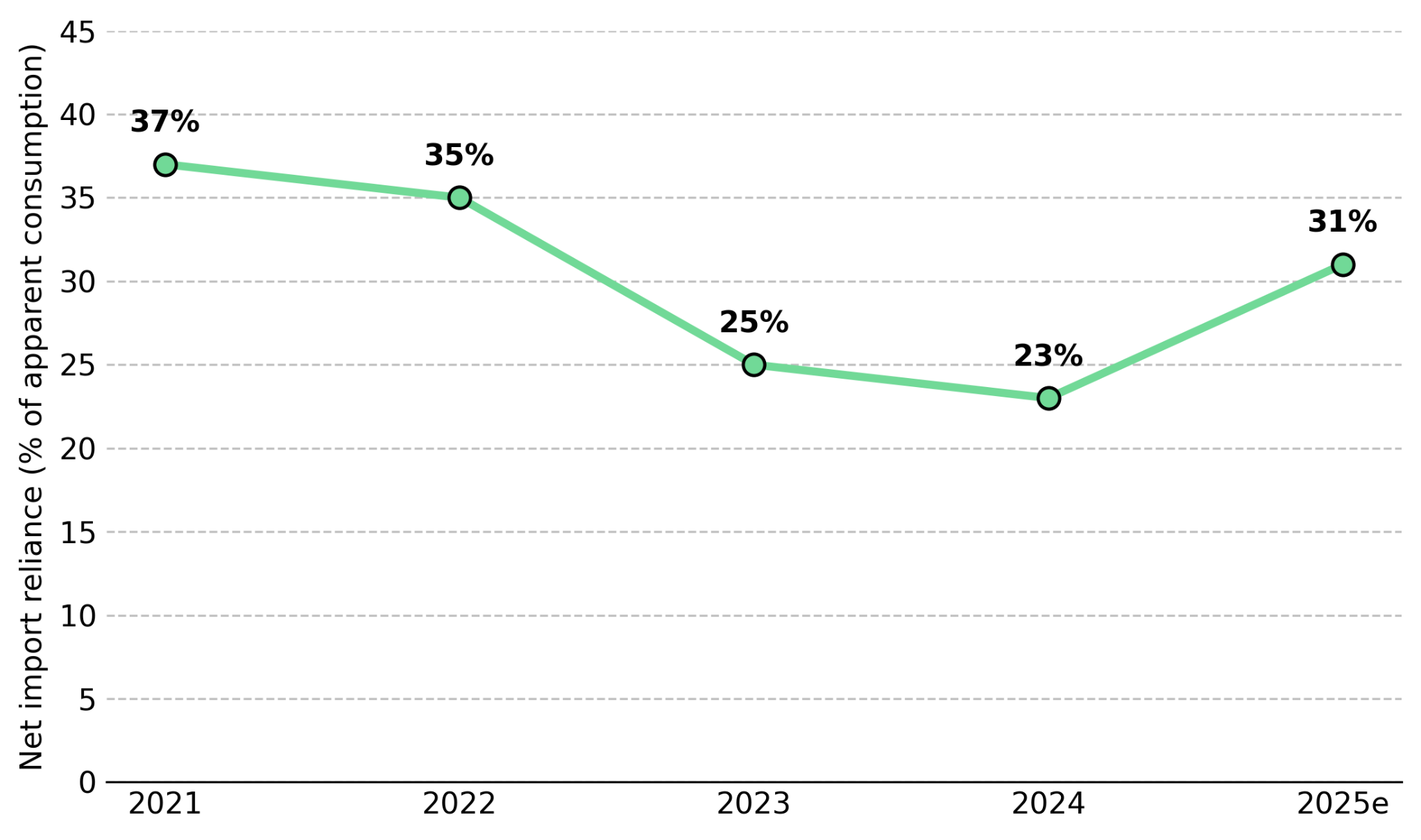

- According to the US Geological Survey (USGS) Mineral Commodity Summaries 2026, US net import reliance for salt rose from 23% in 2024 to an estimated 31% in 2025, marking the steepest single-year increase in the available series.

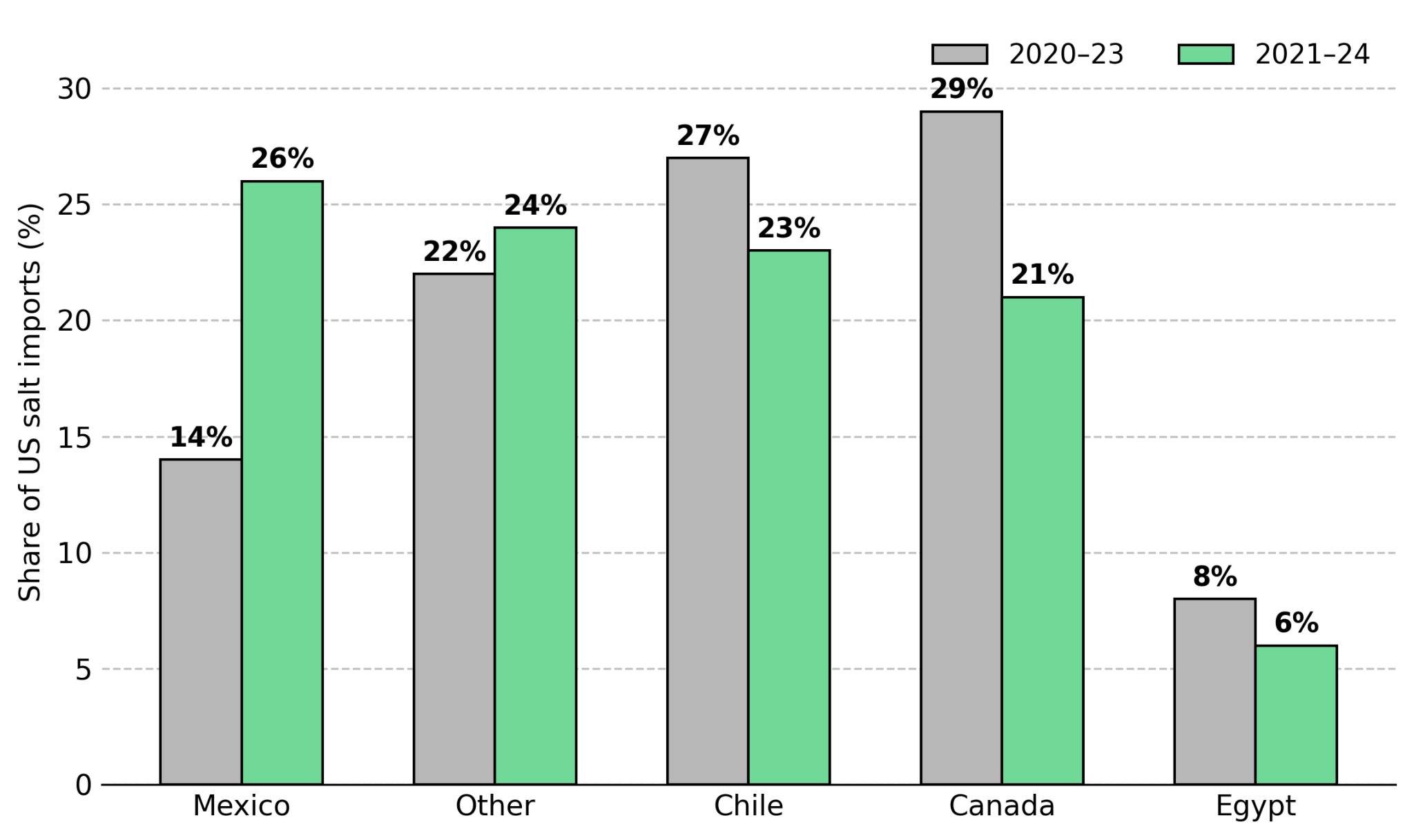

- Mexico and Canada supplied a combined 47% of US salt imports between 2021 and 2024. After the US declined to renew the US-Mexico-Canada Agreement (USMCA) on July 1, 2026, the agreement shifted to an annual review process, increasing trade-policy uncertainty across nearly half of the US salt import market.

- The National Oceanic and Atmospheric Administration (NOAA) Climate Prediction Center upgraded its outlook to an El Niño Advisory on July 13, 2026, replacing the La Niña pattern used to plan the previous deicing season and increasing uncertainty over road-salt demand ahead of the 2026-27 contracting cycle.

- No new underground salt mine has been commissioned in the US since net import reliance began rising, meaning additional domestic supply now depends largely on development-stage projects reaching production.

- The 2026-27 North American road-salt bid season will provide the first market test of tighter supply conditions, with contract prices and awarded volumes indicating whether buyers are paying more to secure supply.

Trade-Policy Uncertainty Increases North American Salt Market Exposure

On July 1, 2026, the USMCA Free Trade Commission completed the joint review required under the agreement's sixth-anniversary clause, and the US declined to renew the agreement in its current form. The Office of the US Trade Representative confirmed the decision, leaving USMCA in force but subject to annual reviews instead of the 16-year planning horizon established when the agreement was signed. While many traded goods are unlikely to be affected immediately, salt is more exposed because thin per-tonne margins and fixed rail and port logistics leave buyers and suppliers more sensitive to recurring trade-policy uncertainty.

Salt does not trade on an exchange and has no derivatives market through which buyers can hedge trade-policy risk. Mexico and Canada cannot be replaced quickly because salt's low value relative to freight costs makes alternative imports uneconomic on short notice. As a result, annual USMCA reviews create greater commercial uncertainty for the North American salt market than for higher-value industries, where trade-policy risks are more easily absorbed or reflected in pricing and valuations.

North American bulk mineral supply chains appear to reflect less trade-policy risk than higher-profile industries despite comparable exposure to USMCA uncertainty. As a result, import-reliance and supply data provide a clearer measure of trade-policy exposure than headline coverage alone.

Flat Domestic Supply & Rising Salt Import Reliance Increase Market Dependence

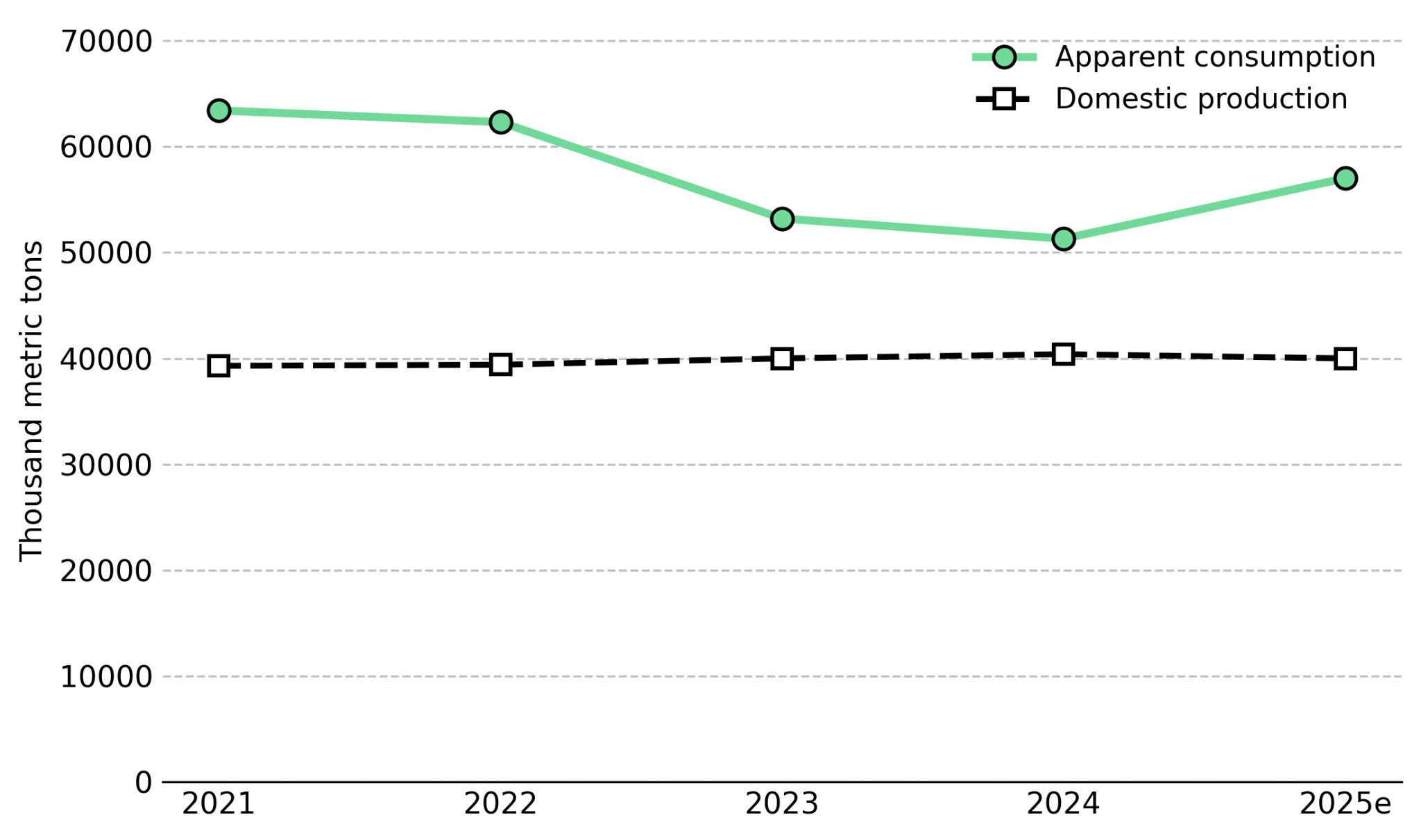

US salt production remained nearly unchanged at an estimated 40,000 thousand metric tons in both 2024 and 2025, while imports for consumption rose to an estimated 19,000 thousand metric tons in 2025. As imports increased against flat domestic production, net import reliance, measured as imports minus exports relative to apparent consumption, rose from 23% in 2024 to 31% in 2025, the steepest one-year increase in the available series.

Apparent consumption, calculated as production sold or used plus imports minus exports, rose to an estimated 57,000 thousand metric tons in 2025 while domestic production remained effectively unchanged. As a result, all incremental demand was supplied through imports rather than additional domestic production. USGS documented a regional rock salt shortage in New York in early 2025, where severe winter demand and limited supply provided an early indication of the tightening market later reflected in national import-reliance data.

No new underground salt mine has been commissioned in the US while import reliance has increased. Because underground salt mines require years of permitting and construction, domestic production capacity cannot expand on the same timeline as trade-policy decisions. As a result, even a favorable USMCA outcome would not quickly reduce import dependence because the production capacity needed to replace imported supply has yet to be built.

El Niño Outlook & Road-Salt Demand Increase Procurement Uncertainty

On July 13, 2026, the NOAA Climate Prediction Center confirmed El Niño conditions were present and estimated a 97% probability that the pattern would strengthen through the year-end and persist into early spring 2027. Because winter weather drives road-salt demand, the updated climate outlook provides an early indicator of 2026-27 procurement requirements by changing expectations for seasonal weather conditions.

Just as grade reconciliation compares mined tonnes and grades against the mine plan, changes in the El Niño-Southern Oscillation (ENSO) outlook prompt buyers to reassess road-salt procurement plans against revised winter weather expectations. The July 2026 NOAA outlook marked a second consecutive planning-cycle revision, increasing uncertainty around 2026-27 deicing requirements.

The updated NOAA outlook replaces the weak La Niña pattern that informed planning for the previous winter. Historically, La Niña favors milder and drier conditions across much of the southern US, while El Niño increases the likelihood of wetter and stormier conditions in the Gulf Coast and Southeast, where deicing infrastructure is less developed than in the traditional snowbelt. Combined with rising import reliance, this greater uncertainty around regional demand increases the incentive for buyers to secure supply through forward contracts instead of relying on spot purchases.

Trade Negotiations & New Mine Development Determine Whether Import Reliance Persists

The key question is whether higher import reliance reflects a temporary imbalance or a longer-lasting supply shortfall. A temporary imbalance would ease if domestic producers increase existing capacity or if favorable USMCA terms maintain competitive imports from Mexico and Canada. If neither occurs, import reliance is likely to remain elevated until new domestic mining capacity enters production, a process measured in years rather than quarters.

A favorable and timely outcome to US trade negotiations with Mexico or Canada would improve the competitiveness of imported salt and ease pressure on domestic supply. Alternatively, new domestic mining capacity progressing quickly through permitting, financing, and construction would reduce future import dependence. If neither development occurs, elevated import reliance is likely to persist, making trade negotiations and domestic supply expansion the key indicators to monitor.

Development-Stage Salt Projects Driving Future Supply Growth

Atlas Salt is developing the Great Atlantic Salt Project near St. George's, Newfoundland and Labrador, with planned steady-state production of 4.0 million tonnes per annum over a 25-year mine life. Its September 30, 2025 Updated Feasibility Study estimated an after-tax net present value (NPV) of $920 million at an 8% discount rate, an after-tax internal rate of return (IRR) of 21.3%, and a 4.2-year payback period. Early Works began on February 27, 2026, with the surface earthworks contractor mobilizing to site in early May 2026. Capital Works construction is contingent on closing the targeted $350 million to $400 million senior secured debt package, which remains under non-binding due diligence with prospective lenders and export credit agencies.

Nolan Peterson, Chief Executive Officer of Atlas Salt, describes plans to supply underserved regional markets:

"We're developing the Great Atlantic Salt Project on the west coast of Newfoundland, aiming to supply de-icing road salt to critically underserved markets in the northeast US, eastern Canada, and the Atlantic provinces."

Trade Policy Driving Bulk Mineral Supply Risk

Salt illustrates how trade-policy risk can affect bulk commodities with limited pricing flexibility and high transportation costs. Bulk minerals with low per-tonne margins and high freight costs are exposed to trade-policy risk that cannot be hedged through options or futures because no exchange-traded market exists for the commodity. A base-metals producer facing a tariff dispute can reference liquid forward markets to evaluate potential pricing outcomes. By contrast, North American salt supply depends on established rail and port links with Mexico and Canada and has no equivalent financial hedge. As a result, price signals typically emerge only after regional supply tightens.

The trade-policy issues affecting the North American salt market also apply to many freight-sensitive, import-reliant bulk commodities sourced from Mexico and Canada. As the USMCA review continues, these sectors face similar uncertainty around cross-border supply costs and availability. Salt serves as the clearest analytical example because USGS publishes detailed annual import-reliance data that allow changes in country-level supply exposure and net import reliance to be measured over time.

Detailed import-reliance data make salt an effective case study for evaluating how trade-policy changes affect bulk commodity supply chains. The shift from a long-term trade framework to annual reviews may introduce similar uncertainty for other freight-sensitive, import-reliant commodities sourced from Mexico and Canada, although the impact will be more difficult to measure where equivalent supply and import data are unavailable.

The Investment Thesis for Salt

- Import reliance increased from 23% to 31% in a single reporting year while domestic production remained flat, highlighting a growing dependence on imported supply regardless of the eventual outcome of the USMCA review.

- Trade-policy uncertainty is now concentrated in imports from Mexico and Canada, where annual USMCA reviews have replaced a longer-term trade framework and prolonged uncertainty around future import terms.

- The shift to an El Niño pattern increases uncertainty around seasonal demand, which can encourage buyers to secure contracted supply rather than rely on spot purchases.

- Development-stage projects with completed feasibility studies and permitted early works provide a defined pathway for adding domestic production capacity while establishing an observable benchmark for the capital required to develop new supply.

- Established producers entering the coming bid season with stronger balance sheets have greater financial flexibility to focus on commercial execution rather than balance-sheet repair as the market deficit widens.

- Jurisdictions with efficient municipal and provincial permitting processes can shorten project development timelines and reduce regulatory uncertainty when bringing new bulk mineral production capacity online.

Whether the increase in import reliance from 23% to 31% represents a temporary shift or the beginning of a sustained supply shortfall depends on two measurable developments: progress in bilateral trade negotiations between the US and Mexico, and separately between the US and Canada, under the annual USMCA review process, and financial close for development-stage domestic projects. A project's transition from Early Works to Capital Works provides tangible evidence that additional domestic production capacity is moving toward construction and establishes a clearer timeline for future supply growth. The first near-term test of both developments will be the 2026-27 North American road-salt bid season. Contract prices, committed volumes, and contract terms negotiated during the bidding process will provide early evidence of how buyers are responding to trade-policy uncertainty and elevated import dependence, establishing a measurable benchmark for assessing whether market conditions are changing.

TL;DR

US salt import reliance rose from 23% to 31% in 2025 while domestic production remained flat, increasing dependence on imports from Mexico and Canada. Annual USMCA reviews have replaced a longer-term trade framework, adding recurring trade-policy uncertainty to nearly half of US salt imports. At the same time, an El Niño outlook has increased uncertainty around road-salt demand ahead of the 2026-27 contracting season. With no new underground salt mines entering production, domestic supply growth depends on development-stage projects. Investors should monitor trade negotiations, project advancement, and the upcoming road-salt bid season to determine whether current market tightness persists.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed