China’s 2025 Rare Earth Controls Continue to Reprice Western Critical Mineral Assets

China’s rare earth controls, AI power demand, and Western smelter weakness are reshaping critical mineral markets and supply chain valuations.

- China’s April 2025 heavy rare earth export controls continue disrupting global supply chains, with dysprosium, terbium, and yttrium exports remaining materially below pre-control levels as Western governments accelerate domestic processing and refining strategies.

- AI-driven electricity demand growth and grid infrastructure expansion are intensifying structural demand for copper, nickel, specialty alloys, transformers, and transmission equipment, while IEA modeling points to a potential 30% global copper supply deficit by 2035.

- Western copper smelting economics have deteriorated sharply, with 2026 TC/RC benchmark contracts settling at $0 per tonne as Chinese smelters maintain significant cost advantages over US and allied processing facilities.

- Indonesian nickel supply growth and rising lithium iron phosphate battery market share are reshaping nickel markets, shifting investor focus toward jurisdictionally secure sulfide projects with advanced permitting visibility across North America and allied jurisdictions.

- Governments across the US, Canada, and allied markets are increasingly deploying sovereign financing, permitting support, and strategic offtake structures to localize rare earth, graphite, titanium, nickel, copper, and platinum group metal supply chains outside China.

Heavy Rare Earth Shortages Intensify Under China’s Export Control Framework

Article 49 of China’s 2024 dual-use export regulations, which took effect for selected rare earth products on October 9, 2025, requires export licenses for foreign-made goods containing at least 0.1% Chinese-origin rare earth content or produced using Chinese rare earth processing technologies. Although Beijing suspended the October 2025 measures for one year during the October 30, 2025 APEC summit in Busan, the April 4, 2025 export controls on seven medium and heavy rare earth elements remained in force, preserving licensing authority over dysprosium, terbium, yttrium, samarium, gadolinium, lutetium, and scandium. According to International Energy Agency (IEA) data cited in the same commentary, China accounts for roughly 70% of global critical mineral refining capacity and leads processing across 19 of 20 strategic mineral supply chains.

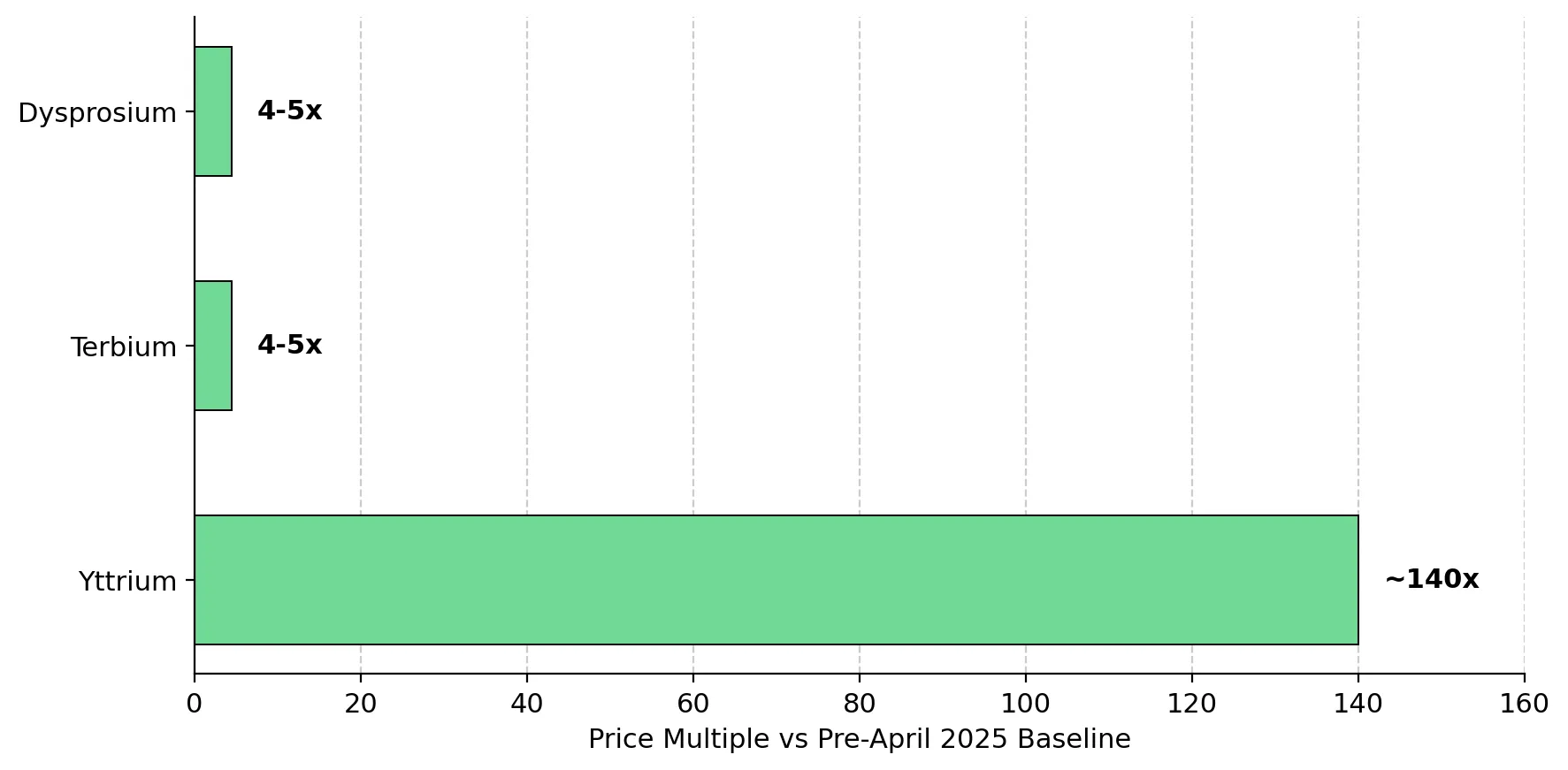

Exports of yttrium, dysprosium, and terbium from China remain about 50% below pre-April 2025 control levels. Japan received only 4% of its prior 12-month dysprosium import volume, while Germany reportedly received none. Argus data show dysprosium and terbium prices outside China rising four- to five-fold since April 2025, while yttrium prices increased by roughly 140 times. Manufacturers are also paying between 1.5 and 3 times more for permanent magnets compared with pre-control pricing. Reuters further reported in February 2026 that yttrium shortages forced temporary production pauses at several US aerospace companies.

Energy Fuels has engaged in discussions with magnet manufacturers and original equipment manufacturers for both light and heavy rare earth offtake outside Chinese supply chains, according to its Q1 2026 release. Mark Chalmers, Energy Fuels' Chief Executive Officer, described the urgency behind the procurement shift:

“What these governments want is to see us get there as quickly as possible.”

AI Infrastructure Expansion Intensifies Copper Processing & Grid Equipment Bottlenecks

Goldman Sachs forecasts global data center electricity consumption doubling to approximately 945 terawatt-hours by 2030. J.P. Morgan estimates data centers could account for nearly 9% of US electricity demand by 2035, while IEA modeling projects a 30% copper supply deficit by 2035 and J.P. Morgan forecasts global copper demand growing 2.6% year-over-year. AI cluster build-outs require transformers, high-voltage substations, transmission upgrades, and dedicated backup power systems, mapping demand directly onto copper, nickel, and specialty alloy supply chains where Western processing capacity is contracting.

Western Copper Smelter Economics Collapsed As 2026 TC/RC Benchmark Settled At Zero

A commentary from the Center on Global Energy Policy noted that Chinese copper smelters operate at less than half the cost of comparable facilities in the US and allied countries. Germany-based Aurubis also reported that energy costs at its German smelters are roughly three times higher than at its US operations.

At the same time, profitability across the global copper smelting industry has deteriorated sharply. The annual treatment and refining charge (TC/RC) benchmark between Antofagasta and Chinese smelters fell to a record low of $0 per tonne and $0 per pound for 2026 contracts signed on December 20, 2025, while spot treatment charges dropped further to negative $90 per tonne in March 2026. Governments are increasingly stepping in to support domestic smelting capacity. The Australian federal government announced AUD$395 million in support for Glencore’s Mount Isa copper smelter on October 8, 2025, while Glencore is also reviewing the potential closure of its Horne smelter in Canada.

The Canadian federal government has paired smelter-side measures with upstream financing. Mark Selby, Chief Executive Officer of Canada Nickel, highlighted the strain already emerging across electrical equipment supply chains:

“Electrical equipment, transformers, and related systems have been chronically long-lead items, and the AI boom is not making them any less constrained.”

Indonesian Nickel Oversupply Shifts Investor Focus Toward Permitted Western Sulfide Projects

London Metal Exchange records nickel trading below $15,000 per tonne for only the second time since 2021, with LME warehouse stocks reaching 338,900 tonnes as Indonesian high-pressure acid leach and nickel pig iron production continued expanding through 2025. Macquarie Bank's revised forecast that lithium iron phosphate batteries would reach 65% of global EV battery market share by 2029, a sharp upward revision from the prior 49% forecast, compressing near-term battery nickel demand. The bifurcation has shifted Western nickel valuation toward jurisdictionally secure sulfide projects with named federal permitting catalysts rather than marginal laterite operations exposed to Indonesian oversupply.

Canada Nickel announced on May 12, 2026 that the Impact Assessment Agency of Canada published the draft Impact Assessment Report for the Crawford Nickel Project, with the final federal permitting decision targeted for early summer 2026. Crawford is the first mining project to reach this stage under Canada's 2019 Impact Assessment Act, which requires demonstration of positive outcomes across health, social, and economic dimensions and Indigenous peoples' rights. The Company extended its US$32 million senior loan facility with Auramet International to August 9, 2026 from May 9, 2026, bridging financing to the targeted permitting decision.

US Rare Earth & PGM Processing Expansion Advances the Domestic Integration Strategy

Energy Fuels reported $956.6 million in working capital as of March 31, 2026, including $108.4 million in cash and $802.2 million in marketable securities per its Q1 2026 results. The Phase 2 separation circuit bankable feasibility study, released January 2026, sets initial capital cost at approximately $410 million and projects combined Phase 1 and Phase 2 capacity of 6,229 tonnes per annum of NdPr oxide, 80 tonnes per annum of terbium oxide, and 288 tonnes per annum of dysprosium oxide. The Company produced terbium oxide at pilot scale in March 2026 at approximately 99.9% purity, the first US primary production of terbium in decades.

Lifezone Metals reported that 1,179 locked-cycle and pilot batch tests over 24 months delivered platinum and palladium recoveries above 99% and rhodium recovery of 95% from US-sourced spent automotive catalytic converters, with a financial investment decision targeted for Q2 2026. The Company closed a $25 million registered direct offering on April 23, 2026 at $4.40 per share, while drawing $25 million of its $60 million Taurus senior secured bridge loan facility as of March 31, 2026. The US imports approximately 2 million ounces of platinum group metals annually, primarily from South Africa and Russia, with rhodium ranked in the highest US supply chain risk category by the US Geological Survey.

Chris Showalter, Chief Executive Officer of Lifezone Metals, quantified the production scale of a single recycling module against the only significant primary PGM mine in the United States:

"Our first module alone could produce 220 thousand ounces of 3E PGMs annually, nearly matching the only significant primary PGM mine in the U.S."

By-Product Streams & The Heavy Rare Earth Value Layer At Kasiya

Sovereign Metals' Definitive Feasibility Study for the Kasiya rutile-graphite project, completed April 2026, returns a pre-tax net present value at an 8% discount rate of US$2.2 billion and a pre-tax internal rate of return of 23.4%, with Phase 1 capital to first production of US$727 million and operating cost of US$450 per tonne of product free on board Nacala. Kasiya's incremental graphite operating cost is US$216 per tonne, positioned below the Chinese weighted-average cash cost range of US$257 to US$288 per tonne. Rio Tinto holds a 19.9% strategic stake following a US$60 million investment, plus an option to become project operator with exclusive marketing rights to 40% of annual production.

Sovereign Metals' offtake architecture connects directly to US Department of Defense critical minerals financing programs. Frank Eagar, Managing Director and Chief Executive Officer of Sovereign Metals, identified the strategic significance of the Traxys North America offtake:

“Having someone like Traxys involved as part of Project Vault is very meaningful as we enter the US market.”

Kasiya's monazite concentrate, recoverable from the project's non-conductor tailings stream at near-zero incremental cost, averages 2.9% combined dysprosium and terbium and 11.9% yttrium, approximately 7x the average across Mt Weld, Mountain Pass, Bayan Obo, Weishan, and Maoniuping, the five largest global rare earth operations. The monazite stream is entirely excluded from the published DFS economics, with formal economic evaluation and recovery rate assessment pending. The compositional profile addresses precisely those heavy rare earth elements where Japan approaches 100% Chinese supply dependency and the US imports 100% of its yttrium requirements.

The combination of AI-driven electrification demand, tightening Chinese heavy rare earth export controls, and growing Western supply chain localization efforts is increasingly elevating the value of projects capable of supplying dysprosium, terbium, and yttrium outside China, particularly where by-product recovery can be integrated into existing critical mineral development platforms at low incremental cost.

The Investment Thesis for Critical Minerals & Battery Metals

- Advanced-stage developers with named permitting catalysts under verifiable regulatory frameworks carry valuation premiums tied to approval timelines rather than discounted cash flow assumptions alone.

- Domestic refining and processing capacity attracts premiums independent of underlying commodity prices, given Chinese smelter cost advantages of approximately 50% per Columbia CGEP and Western copper treatment and refining charges at $0 per tonne for 2026 term contracts.

- Hydrometallurgical recycling technologies with verified pilot-scale recoveries above 99% for platinum group metals offer dual decarbonization and supply-security exposure while reducing dependence on Chinese refining capacity.

- By-product exposure to dysprosium, terbium, yttrium, titanium, and graphite carries multiple overlapping industrial policy financing tailwinds where US Department of Commerce national security determinations have been issued.

- Battery chemistry divergence carries directional consequences, with lithium iron phosphate forecast to reach 65% of global EV battery share by 2029 per Macquarie Bank, compressing nickel and cobalt demand while supporting copper, graphite, and heavy rare earth demand from grid, AI, and defense end markets.

- Developers aligned with US, Canadian, Australian, and allied industrial policy programs are accessing federal sovereign funds, production tax credits, and offtake-linked financing structures not available during prior commodity cycles.

The cumulative effect of China's April 2025 rare earth controls, the October 30, 2025 Busan suspension of the broader October 9 measures, and Western industrial policy programs targeting domestic processing has repriced critical mineral valuation around named regulatory frameworks and quantified federal capital programs rather than resource scale. Permitting visibility under Canada's 2019 Impact Assessment Act, copper treatment and refining charges at $0 per tonne for 2026 term contracts, and federal funding programs deploying multi-billion-dollar sovereign capital have replaced resource size as the primary valuation input across nickel, rare earths, graphite, titanium, and platinum group metals.

TL;DR

China’s 2025 heavy rare earth export controls, combined with accelerating AI-driven electricity demand and weakening Western smelting economics, are reshaping global critical mineral markets around processing security, permitting certainty, and domestic supply chain integration. Governments across North America and allied markets are increasingly supporting copper, nickel, rare earth, graphite, titanium, and platinum group metal projects through sovereign financing, permitting reforms, and strategic offtake agreements, while investors shift toward jurisdictionally secure developers with downstream refining, recycling, and processing exposure outside China.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed