China's 44-Company Export Whitelist & Silver Supply Security Favor Silver in Lower-Risk Jurisdictions

Silver deficits, China's 44-company export whitelist, and critical-mineral policies are making supply security a key investment consideration.

- The Silver Institute projects a sixth consecutive annual silver deficit of 46.3 Moz in 2026, while export controls and critical-mineral policies are increasingly influencing which silver can move between markets.

- China's reclassification of silver as a strategic material, limiting exports to 44 approved companies in 2026 and 2027, alongside the US addition of silver to its critical-minerals list in late 2025, is increasing the importance of supply security as a factor in silver asset valuation.

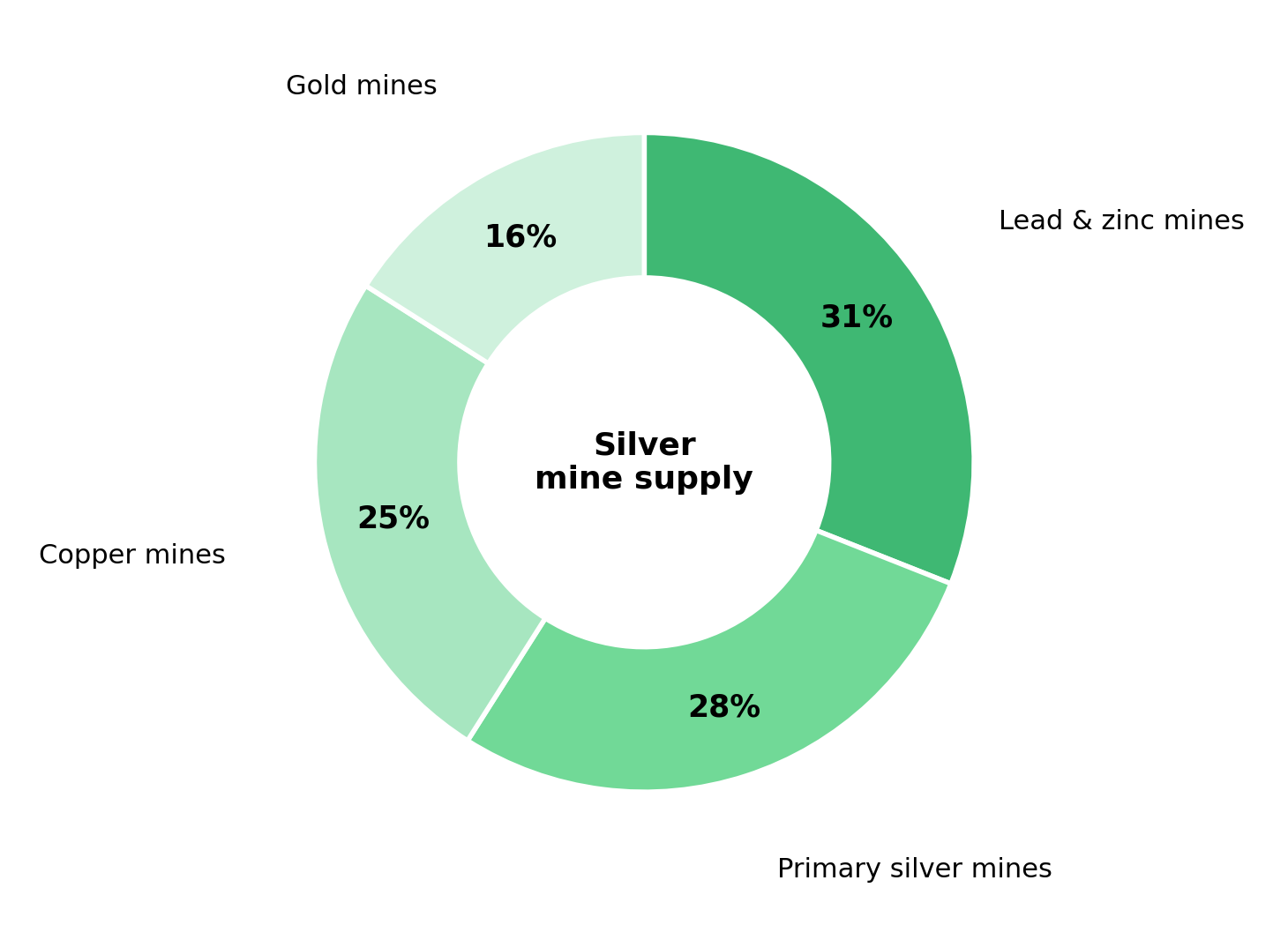

- Mine supply cannot close a projected 46.3 Moz deficit quickly because roughly three-quarters of silver production comes from lead, zinc, copper, and gold mines. Global mine output remains near 847 Moz, while new primary silver mines typically require five to ten years to permit and build.

- Export controls are increasing the importance of jurisdiction in silver asset valuation, with projects in the US and Mexico facing fewer licensing and trade restrictions than supply exposed to export controls.

- A hawkish Fed and a stronger US dollar can pressure silver prices in the near term, but they do not remove the export controls and critical-mineral policies restricting supply flows.

Export Licensing & Critical-Mineral Policies Move Silver Supply Flows

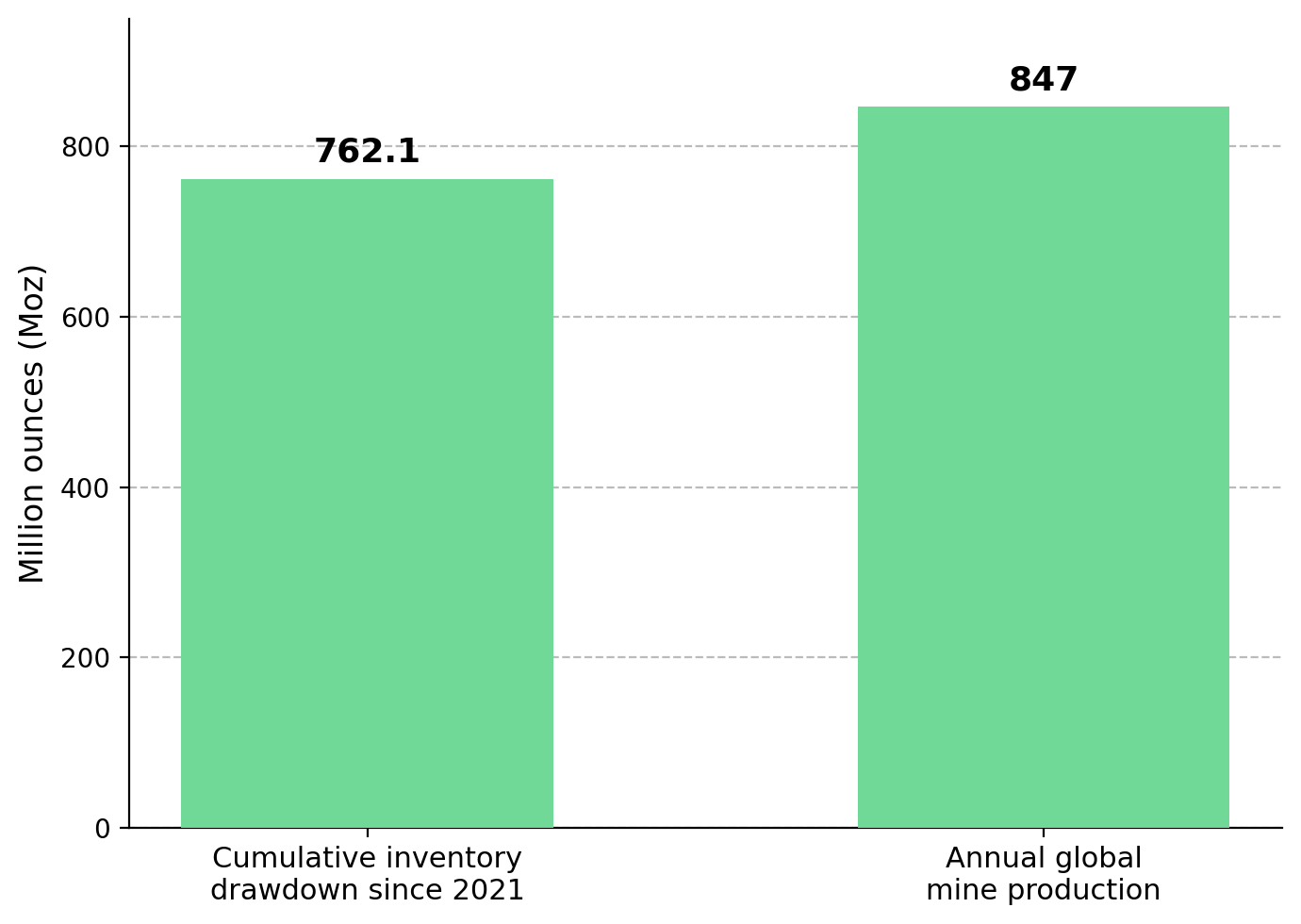

For the past decade, higher prices encouraged additional silver supply from scrap and above-ground inventories. The Silver Institute's World Silver Survey 2026 projects a sixth consecutive annual deficit of 46.3 Moz. Since 2021, cumulative drawdowns from above-ground inventories have reached 762.1 Moz, equivalent to nearly a full year of global mine production. China and the US now classify silver as a strategic material, giving governments greater scope to influence exports, stockpiling, and trade flows. As a result, export controls and critical-mineral policies are becoming a significant factor in determining which silver can enter international markets.

A critical-mineral designation can trigger government stockpiling, funding, and trade controls by classifying a commodity as essential to national security or the energy transition. Export-licensing requirements allow governments to control which companies can ship commodities into international markets. Applied to a market already facing a 46.3 Moz deficit in 2026, these policies can restrict the flow of available metal even when prices rise. For investors, supply security is becoming a more important factor in evaluating silver projects alongside commodity prices.

China Limits Silver Exports to 44 Approved Companies

Effective at the start of 2026, China replaced its quota system with a state-trading whitelist that limits silver exports during 2026 and 2027 to 44 approved companies, up from 42 in the prior year. The change places silver under export controls similar to those already applied to rare earths, tungsten, and antimony. The whitelist adds an approval layer to silver exports, which may slow shipments and limit the volume of metal available to international buyers from the world's largest producing and refining hub.

The US has also added silver to its critical-minerals list and signaled plans to build domestic stockpiles of strategic metals. With both governments prioritizing supply security, jurisdiction may become a more important factor in how investors evaluate silver projects and producers. During the October 2025 silver squeeze, unencumbered LBMA inventories fell to historically low levels while lease rates surged, showing how quickly available supply can tighten when demand exceeds immediately accessible metal.

Why Silver Supply Cannot Close the Deficit

Policy risk matters because silver supply responds slowly when demand increases. Roughly three-quarters of mined silver is produced as a by-product of copper, lead, zinc, and gold mining rather than from mines built primarily for silver. Because most supply is incidental to other mining activities, higher silver prices do not automatically increase output. As a result, global mine production remains roughly flat at 847 Moz. New primary silver mines typically require five to ten years to permit and build.

Silver supply cannot expand quickly in response to higher prices because most production comes from by-product mining and new mines take years to develop. As a result, a projected 46.3 Moz deficit can persist even when prices rise, while export controls can further restrict the metal available to international markets. Production growth and supply security become more important considerations when mine supply remains constrained and export controls restrict market access.

Primary Silver Producers Remain a Scarce Source of New Supply

Americas Gold & Silver reported record silver production of approximately 787,000 oz in Q1 2026 and guided to 3.2-3.6 Moz for the full year. In a market facing a sixth consecutive annual deficit, production growth from an operating silver producer is notable because most silver supply comes from by-product mining and global mine output remains near 847 Moz.

Oliver Turner, Executive Vice President of Corporate Development at Americas Gold & Silver, explains why silver supply remains slow to respond even when demand increases:

“70% of silver is a byproduct from other mines. You can't just turn on more silver supply when the world needs it. Primary silver producers such as ourselves are producing an increasingly critical and scarce metal that's going to be required across all these applications.”

Export Controls & Supply Security Reshape Silver Asset Evaluation

If export controls increase the importance of supply security, investors may place greater emphasis on jurisdiction when evaluating silver resources. A widening EV/oz gap between lower-risk and export-restricted jurisdictions would indicate that supply security is becoming a larger factor in valuation.

Other critical-mineral markets have shown that supply-security concerns can influence how resource assets are assessed. While it remains too early to quantify a silver-specific premium, jurisdiction may become a more important consideration alongside resource size and project economics if supply security continues to influence market access.

New silver discoveries can be revalued quickly by the market, but converting resources into production typically requires years of permitting, engineering, financing, and construction. That development timeline limits how quickly new supply can enter the market, even when investors identify economically attractive projects.

Development Timelines Delay New Silver Supply

Vizsla Silver's November 2025 Feasibility Study outlines average annual production of 17.4 Moz silver equivalent over an initial 9.4-year mine life at the Panuco project in Mexico. The study reports an after-tax NPV of US$1.8 billion, an IRR of 111%, and a seven-month payback period using silver and gold prices of US$35.50/oz and US$3,100/oz respectively. Those figures illustrate that economically viable silver projects continue to advance through the development pipeline, but permitting, financing, engineering, and construction still separate a feasibility study from new metal entering the market.

Jesus Velador, Vice President of Exploration at Vizsla Silver, outlines the work required before a silver resource can support future production:

"We started focusing on de-risking the mineral resource, particularly in the Copala area where we envision the first years of production for the Panuco project. For the first time, we put out a measured resource in the core of the high-grade central portion of Copala, where we are going to have our initial years of production."

Exploration Success Supports Future Supply

GR Silver Mining's May 2026 drill result at San Marcial, which returned 45.1 meters of true width grading 1,623 g/t silver, including 8.25 meters at 8,579 g/t. Such results can support future resource growth, but they do not demonstrate economic viability or future production. In a market where new mines can take years to develop, discoveries represent the earliest stage of future supply replacement. The Plomosas project benefits from existing mine infrastructure, road access, and permits associated with past production, which could shorten future development timelines.

Eric Zaunscherb, Interim President and Chief Executive Officer of GR Silver Mining, explains how exploration drilling can contribute to future silver supply:

"We have 134 million ounces of silver equivalent, and we believe that has a significant opportunity to grow through our 20,000-meter drill program. The resource at San Marcial averages 22 meters in thickness, which is why we can build ounces quickly, efficiently, and cost effectively."

Policy Constraints Offset Monetary Pressure

The Silver Institute projects a 46.3 Moz deficit in 2026, extending the market's deficit to a sixth consecutive year. Solar manufacturers have reduced silver loadings per panel by roughly 19% and continue to substitute where possible, but demand from AI infrastructure, data centers, electronics, and investment continues to support silver consumption. While industrial fabrication is projected to decline as manufacturers reduce silver intensity, rising investment demand is expected to offset part of that weakness.

Meanwhile, mine supply remains slow to expand, while export controls and critical-mineral policies are limiting the flow of silver into international markets. Together, these factors make it more difficult for the silver market to increase supply quickly in response to demand growth. A hawkish Fed and a stronger US dollar raise the opportunity cost of holding a non-yielding asset, which can pressure silver prices even as supply deficits and policy restrictions persist. As a result, silver prices can weaken in the short term even when supply deficits and policy constraints continue to support the longer-term market balance.

The key question for the second half of 2026 is whether supply constraints and export controls exert a greater influence on silver prices than US monetary policy. As export controls and critical-mineral policies expand, supply security, project stage, and jurisdiction may become more important factors in how investors evaluate silver assets.

The Investment Thesis for Silver

- Exposure to a sixth straight annual silver deficit is now reinforced by export licensing and critical-mineral designations, increasing the value of supply that can move freely across markets.

- Supply inelasticity increases the importance of primary silver producers that are growing output, as by-product-dependent mine supply remains roughly flat at 847 Moz, although AISC and by-product-credit sensitivity remain important considerations.

- Government support for critical minerals can increase the strategic importance of silver operations that also produce metals considered essential to domestic supply chains.

- Development-stage projects provide a measure of how higher silver prices could influence future supply, although financing, permitting, engineering, and construction can delay new production for years.

- Exploration success can support future resource growth in a market where mine supply remains constrained, although drilling results alone do not establish resources, project economics, or future production.

- If supply security becomes a larger valuation consideration, companies in jurisdictions with fewer trade restrictions could command higher EV/oz multiples than peers exposed to export controls.

The defining shift of 2026 is that silver availability depends not only on how much metal exists, but also on where it is located and whether it can be exported. A projected 46.3 Moz deficit provides the market context, while export licensing and critical-mineral policies are adding new constraints to supply flows. With China limiting silver exports to 44 approved companies and both China and the US classifying silver as strategic, investors may place greater value on silver resources and production located in jurisdictions with fewer trade restrictions. This framework focuses on long-term supply availability rather than short-term price movements, particularly while US monetary policy weighs on silver prices and export controls continue to constrain supply.

TL;DR

Silver is projected to post a sixth consecutive annual deficit of 46.3 Moz in 2026 as mine supply remains constrained and above-ground inventories continue to decline. China's new 44-company export whitelist and the US decision to classify silver as a critical mineral are increasing the importance of supply security and market access. Because most silver is produced as a by-product of other metals and new mines can take years to develop, supply cannot respond quickly to higher prices. This is increasing investor focus on jurisdiction, project stage, and production growth, even as a hawkish Fed and stronger US dollar continue to create near-term pressure on silver prices.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed