China's Copper Foil Operating Rates Signal a Demand Inflection That Supply Cannot Meet

Copper demand is rising as China’s foil utilisation tops 90%, while supply constraints tighten the market and drive re-rating potential.

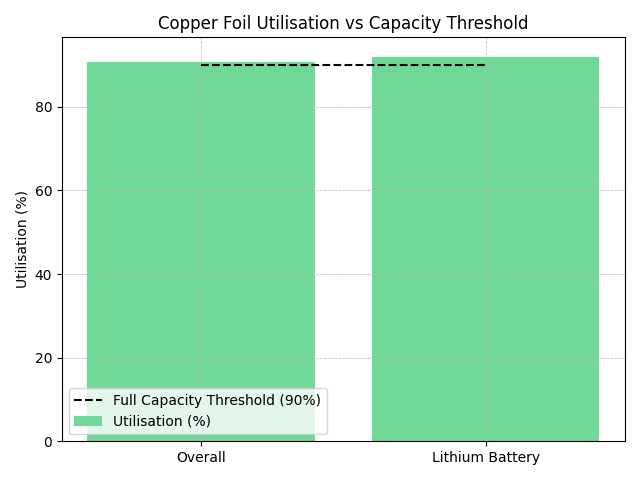

- China's copper foil operating rates exceeded 90.7% overall and 92% in the lithium-battery segment in April 2026, confirming a sharp acceleration in physical downstream consumption.

- Utilisation data provides real-time demand validation that headline PMIs and property sector indicators have consistently failed to deliver in the current cycle.

- Electrification, not construction, is now the primary structural driver of copper demand, making demand progressively less cyclical and more anchored to multi-decade infrastructure buildout.

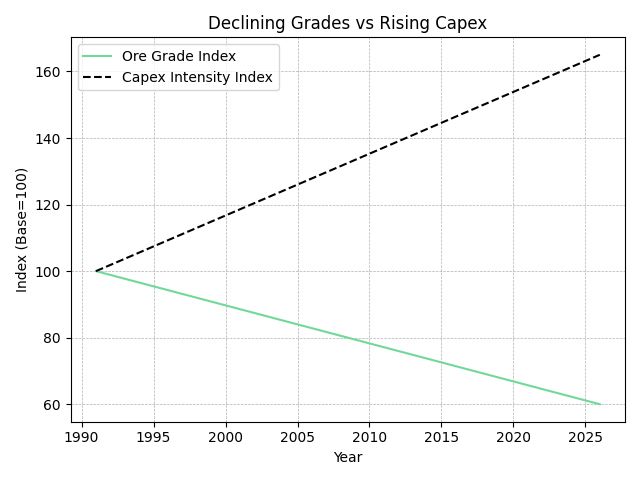

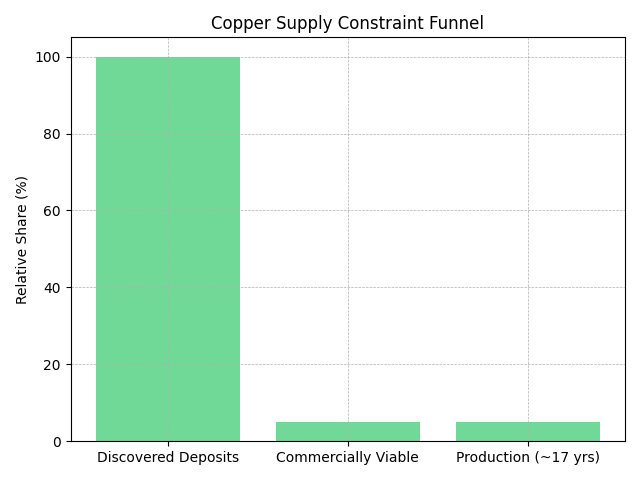

- Supply cannot respond at speed: ore grades have declined approximately 40% since 1991, lead times average 17 years from discovery to production, and only around 5% of deposits discovered in the last decade are commercially viable.

- Developers and explorers with low-cost oxide projects, high-grade polymetallic systems, and near-term catalysts carry the strongest re-rating potential in a demand-led copper cycle.

Fabrication-Level Utilisation Replaces PMI as the Operative Demand Signal

For most of the past decade, copper demand assessments relied on China's manufacturing PMI, property starts data, and infrastructure budget announcements. Those indicators remain contextual inputs, but they are insufficient as primary signals when the underlying demand structure is changing at the fabrication level.

China's copper foil operating rates crossing 90.7% in aggregate and 92% in the lithium-battery segment in April 2026 constitute a materially different class of information. At that utilisation level, order books are well-supported, lead times for downstream customers are extending, and the margin for additional throughput without capital investment is exhausted. That is a physical signal embedded in the value chain, not a survey-based sentiment reading.

The investment implication is direct: when fabrication capacity for a critical input material runs near-full, the incremental unit of refined copper required to sustain that output must be sourced regardless of broader macro conditions. Institutional commodity trading desks have shifted their monitoring frameworks toward fabrication-level utilisation metrics because they measure actual consumption, not anticipated consumption.

Electrification Has Replaced Construction as Copper's Structural Demand Driver

The composition of copper demand has shifted materially over the past five years. China’s property sector, previously a dominant end-market for refined copper, has contracted, while incremental demand is now anchored in EVs, grid modernisation, electronics manufacturing, and AI infrastructure, consistent with the IMF’s April 2026 World Economic Outlook.

As a critical input in lithium-ion battery anodes and printed circuit boards, its demand is a direct function of EV production and electronics output, not residential construction. The implication is that copper demand now scales with energy policy execution and grid investment timelines, structurally more durable than credit-driven cycles.

Grid expansion, driven by renewable integration and data centre load growth, represents a long-duration demand source. Fabrication utilisation above 90% confirms that procurement is already occurring at scale, rather than remaining a forward-looking assumption.

Fabrication Utilisation Provides Demand Confirmation That LME Prices Cannot

LME copper prices are influenced by macro risk sentiment, dollar strength, speculative positioning, and exchange warehouse inventory levels. Prices can diverge significantly from physical demand reality over any given quarter when financial flows dominate futures markets. Fabrication utilisation data does not carry those distortions.

When copper foil operating rates exceed 90%, the operational reading is specific: manufacturers are running near-full capacity, order books are supported, downstream customer lead times are extending, and additional throughput without capital investment is not available. In battery-grade copper foil, where product specification tolerances are tightly controlled and the number of qualified suppliers is limited, redirecting demand to an alternate source is not a straightforward option.

Supply Constraints Are the Product of Decades of Structural Deterioration, Not a Cyclical Dip

The demand signal from China's copper foil sector would be less significant if the supply side of the copper market were elastic. It is not. Average copper ore grades at operating mines have declined by approximately 40% since 1991, according to industry data compiled by the International Council on Mining and Metals (ICMM). That grade deterioration means more ore must be processed to produce the same quantity of refined copper, increasing both energy consumption and operating costs per unit of output; the all-in sustaining cost (AISC) per pound has risen accordingly.

Capital expenditure intensity has increased materially. Since 2020, the cost per pound of installed copper capacity has risen ~65%, driven by input cost inflation, more complex orebodies, and stricter permitting. These dynamics discourage marginal projects and concentrate investment in only the most robust assets.

As a result, the pipeline has thinned: ~5% of deposits discovered in the past decade are commercially viable, with an average ~17-year timeline from discovery to production.

The structural implication is that confirmed demand surges, like the one currently visible in China's copper foil operating rates, cannot be met by supply responses within any investment-relevant timeframe.

Projects that are already permitted, de-risked, or in late-stage development carry a scarcity premium that the market has historically taken time to reflect in equity valuations. That lag creates the conditions for re-rating cycles when demand confirmation arrives before supply can respond.

Capital Efficiency and By-Product Credits Determine Which Projects Attract Financing First

Not all copper assets benefit equally in a demand-led tightening cycle. The distinction between oxide and sulphide projects is particularly relevant. Oxide deposits, typically near-surface and processed via heap leaching and SX-EW, have lower capex and shorter build times than large-scale sulphide systems, which require concentrators and smelter offtake. In a market where demand is confirmed but financing remains selective, capital efficiency becomes a key advantage.

High-grade polymetallic systems provide a different form of cost resilience. By-product credits from zinc, gold, or silver reduce effective AISC per pound of copper, strengthening economics across a wider range of price scenarios. In NPV sensitivity terms, projects with multiple revenue streams should be weighted more favourably during copper price uncertainty, as their IRR profiles are more stable.

The metrics likely to drive re-rating in this cycle are AISC, project-level IRR versus a mid-cycle copper price, NPV at current versus spot prices, and capex intensity ($/lb of annual production). Projects with AISC below $1.50/lb, IRR above 25% at $4.00 copper, and sub-$1.50/lb capex intensity are more likely to attract institutional financing than larger but weaker-profile assets.

Developers & Explorers Leveraging the Demand Signal

As fabrication-level utilisation tightens and supply remains structurally constrained, capital is increasingly directed toward projects with clear development pathways, capital efficiency, and scalable resource potential. The current environment favours assets that can either deliver near-term production or demonstrate economically efficient resource growth aligned with evolving demand drivers.

Near-Term Oxide Development with Infrastructure Advantage

Marimaca Copper’s oxide deposit in Chile’s Antofagasta region illustrates the oxide advantage. It is a near-surface, SX-EW cathode project with infrastructure proximity, less than 30 km to port, reducing logistics costs relative to most development-stage peers. The Definitive Feasibility Study is complete, and environmental approval (RCA) has been secured

Hayden Locke, President & Chief Executive Officer, on the DFS outcome and cost positioning:

"Confirmed what we already knew, which is industry-leading capital costs, very competitive operating cost, industry-leading return on invested capital metrics. We're pretty comfortable we can deliver a project for sub $600 million in the current market environment."

The company is targeting construction commencement in 2026, with a base-case production profile of ~50,000 tonnes of copper cathode per annum. Exploration at Pampa Medina introduces sulphide upside, with potential to add ~25,000 tonnes annually and expand total production toward ~75,000 tonnes. This combination of near-term development readiness and district-scale optionality is relatively uncommon at this stage.

High-Grade VMS Exploration with M&A Optionality

At the exploration stage, Abitibi Metals is advancing the B26 Cu-Zn-Au volcanogenic massive sulphide (VMS) deposit in Québec, a top-tier mining jurisdiction. The project has delivered 124% resource growth in under three years, with 13Mt indicated at 2.1% CuEq and 12.3Mt inferred at 2.2% CuEq.

Chief Executive Officer Jonathon Deluce on the discovery efficiency achieved through the drill program and the competitive cost position it has created:

"It's also been at a discovery cost of 2.5 cents per pound copper equivalent. I would put us up against any of our competitors to try to find somebody that's done it more cost-efficiently."

The company has secured 80% ownership and operator control, with a fully funded 40,000-metre drill program underway. The investment case is increasingly tied to M&A dynamics: high-grade polymetallic VMS systems with low discovery costs and expanding resources are among the most sought-after assets for producers evaluating growth pipelines.

Early-Stage Development with Low-Capex Pathway

Fitzroy Minerals is advancing the Buen Retiro copper system in Chile along a low-capex development pathway, with metallurgical work underway and a maiden resource targeted for 2026. The company has strengthened its balance sheet through a recent capital raise and warrant exercise, funding ongoing drilling and technical studies.

Merlin Marr-Johnson, Chief Executive Officer, on the project’s development profile and capital efficiency:

"This would give us non-operated cash flow and a very, very low capital intensity. This is a low-cost operation to bring into production. We think we can do it super quickly."

Its transition toward a copper-focused pure play positions it for potential re-rating as resource definition progresses and heap leach potential is quantified, typically the stage at which early-stage developers in established Chilean mining districts begin to attract broader investor attention.

The Investment Thesis for Copper

- Copper foil operating rates exceeding 90% in China provide real-time, fabrication-level demand confirmation that validates the electrification thesis with physical evidence rather than modelled projections.

- The structural supply deficit, driven by declining ore grades, 17-year average development lead times, and limited commercially viable new discoveries, means demand surges cannot be met by supply response within any near-term investment horizon.

- Oxide development projects in Chile with completed feasibility studies, secured environmental permits, and sub-$600 million capital requirements offer the fastest path from confirmed demand to production, reducing financing execution risk relative to sulphide peers.

- High-grade polymetallic VMS systems in top-tier jurisdictions such as Québec provide by-product credit resilience and M&A optionality that supports valuation floors independent of copper price cyclicality.

- Jurisdiction quality, measured by Fraser Institute Policy Perception Index rankings, permitting transparency, and infrastructure proximity, materially reduces execution risk and cost of capital for development-stage copper assets.

- The re-rating catalyst sequence in this cycle favours developers with near-term construction decisions ahead of explorers still defining resource scale, but both categories benefit from the same underlying supply-demand imbalance as it becomes more institutionally legible.

The copper market has entered a phase where demand confirmation is no longer dependent on extrapolating EV adoption curves or modelling grid investment timelines. China's copper foil operating rates, exceeding 90% across the sector and surpassing 92% in the lithium-battery segment, provide a high-frequency, fabrication-level signal that physical consumption is occurring at a pace that strains available capacity. That signal is more reliable as an investment input than any forward-looking macro indicator currently available.

The structural supply constraint, the product of decades of declining ore grades, underinvestment in exploration, and the irreducible lead time between exploration and production, means the market's ability to equilibrate through new supply is limited to a horizon well beyond the current demand cycle. The operative question has shifted from whether copper demand will grow to which assets are positioned to respond fastest to confirmed, ongoing consumption. Projects with completed feasibility work, secured permits, capital-efficient development structures, and alignment with the fabrication-level demand now visible in China's copper foil sector carry the most immediate re-rating potential in the cycle ahead.

TL;DR

China’s copper foil utilisation exceeding 90% provides real-time, fabrication-level confirmation that copper demand, now driven by electrification, EVs, and grid expansion rather than construction, is accelerating faster than supply can respond. With structural constraints such as declining ore grades, rising capex intensity, and ~17-year development timelines, the market cannot quickly add new supply, creating a sustained imbalance. As a result, capital is rotating toward projects with low capex, strong economics, and near-term production potential, positioning select developers and high-grade explorers for re-rating as physical demand continues to materialize.

FAQs (AI Generated)

Copper foil utilisation reflects actual, real-time consumption at the fabrication level, unlike PMI or macro indicators which are survey-based or lagging. When utilisation exceeds 90%, it indicates that manufacturers are operating near full capacity, with strong order books and limited ability to increase output without new investment. This makes it a direct and reliable proxy for current demand rather than future expectations.

Copper demand has shifted away from China’s property sector toward electrification-driven end markets such as EVs, renewable energy systems, grid infrastructure, and electronics. This transition makes demand less cyclical and more tied to long-term policy and infrastructure commitments, which are structurally more stable than credit-driven construction cycles.

Supply constraints are structural, not cyclical. Ore grades have declined significantly over decades, increasing costs, while permitting, development, and construction timelines average around 17 years. Additionally, only a small fraction of newly discovered deposits are economically viable, limiting the pipeline of new projects. These factors prevent supply from scaling in line with demand within any near-term timeframe.

Projects with low capital intensity, fast development timelines, and strong economics are best positioned. This includes oxide projects using SX-EW processing and high-grade polymetallic systems that benefit from by-product credits. Key financial metrics such as low AISC, high IRR, and efficient capex per pound of production are critical in attracting institutional capital in a selective financing environment.

The current setup creates a lag between demand confirmation and supply response, which historically leads to re-rating cycles in copper equities. Developers with near-term production readiness and explorers with scalable, high-quality resources are likely to benefit most. As fabrication-level demand becomes more visible and persistent, capital increasingly flows toward assets that can realistically deliver supply into a constrained market.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed