Persistent Platinum Deficits & 90% Supply Concentration Increase Global PGM Risk Premiums

WPIC forecasts a 297,000-ounce 2026 platinum deficit as 90% supply concentration in South Africa, Russia, and Zimbabwe lifts global PGM risk premiums.

- forecast to 297,000 ounces as above-ground inventories fell to roughly four months of demand coverage, tightening the global physical supply buffer.

- South Africa, Russia, and Zimbabwe control approximately 90% of primary platinum group element supply, while Q1 2026 production declines at Norilsk Nickel and Zimplats increased geopolitical and operational supply risk.

- Metals Focus raised its 2026 platinum price forecast to $2,190 per ounce after tightening physical inventories and elevated Guangzhou Futures Exchange delivery stress signaled constrained near-term metal availability.

- Federal Reserve repricing toward zero 2026 rate cuts pushed platinum from above $2,200 per ounce to $1,922 in five trading sessions, demonstrating how higher real yields can temporarily outweigh bullish commodity fundamentals.

- Institutional capital is increasingly targeting platinum group element projects outside South Africa, Russia, and Zimbabwe as supply concentration risk reshapes jurisdictional valuation premiums across the sector.

Fourth Consecutive Platinum Deficit Tightens Global Supply Risk

The World Platinum Investment Council's Q1 2026 Platinum Quarterly, released May 19, 2026, forecast a 297,000-ounce platinum supply deficit for full-year 2026. The revised deficit is 57,000 ounces larger than the council's prior forecast and marks a fourth consecutive annual shortfall. Above-ground platinum inventories now cover approximately four months of global demand, limiting how long supply deficits can be offset from existing stockpiles before tighter physical availability pressures prices higher.

A smaller 2026 deficit than 2025's 1.08 million ounce shortfall does not indicate that the platinum market has returned to balance. The council's inventory tracking series shows cumulative above-ground stock drawdowns of approximately 42% since 2023. Each additional annual deficit further reduces already declining above-ground inventories. Above-ground platinum inventories now provide less demand coverage than at any point since the council began tracking the market in 2014.

WPIC Inventory Data Signals Tighter Platinum Market Conditions

Q1 2026 recorded a temporary 268,000 ounce platinum surplus as South African mine supply rose 18% year over year from weak Q1 2025 comparisons while total demand fell 31%. The demand decline reflected 374,000 ounces of exchange-traded fund and exchange inventory outflows rather than weaker physical end-use demand. A platinum market deficit means primary mine supply and recycled supply cannot meet total demand, requiring the shortfall to be filled from above-ground inventories. When inventory coverage falls below five months of demand, additional buying pressure can produce larger price increases because less physical metal is available to absorb new demand.

Q1 2026 Producer Disruptions Extend Platinum Supply Deficits

Production declines outside South Africa reinforced the broader platinum group metal supply tightening trend. Russia's Norilsk Nickel reported Q1 2026 platinum production down 26% year over year and palladium production down 18%. Norilsk Nickel's full-year 2026 guidance targets palladium production declines of 10% to 11% and platinum production declines of 5% to 8%. Zimbabwe's Zimplats reported a 56% decline in Q1 2026 six-element platinum group element production due to an extended smelter shutdown.

Zimbabwe's late-April 2026 ban on exports of unrefined critical minerals added regulatory risk to an already tightening platinum group metal supply chain. Production cuts at existing mines are occurring faster than new projects outside South Africa, Russia, and Zimbabwe can add supply, increasing the likelihood of continued platinum group metal deficits into 2027.

Long Mine Development Timelines Limit Platinum Supply Growth

The platinum market remains in deficit despite prices doubling over the past 12 months, indicating that higher prices alone are not increasing supply fast enough to rebalance the market. Existing platinum supply cannot expand quickly because most new mine development requires multiple years of permitting, financing, and construction. Declining ore grades, operational disruptions, and reduced mining investment are simultaneously limiting new platinum supply growth.

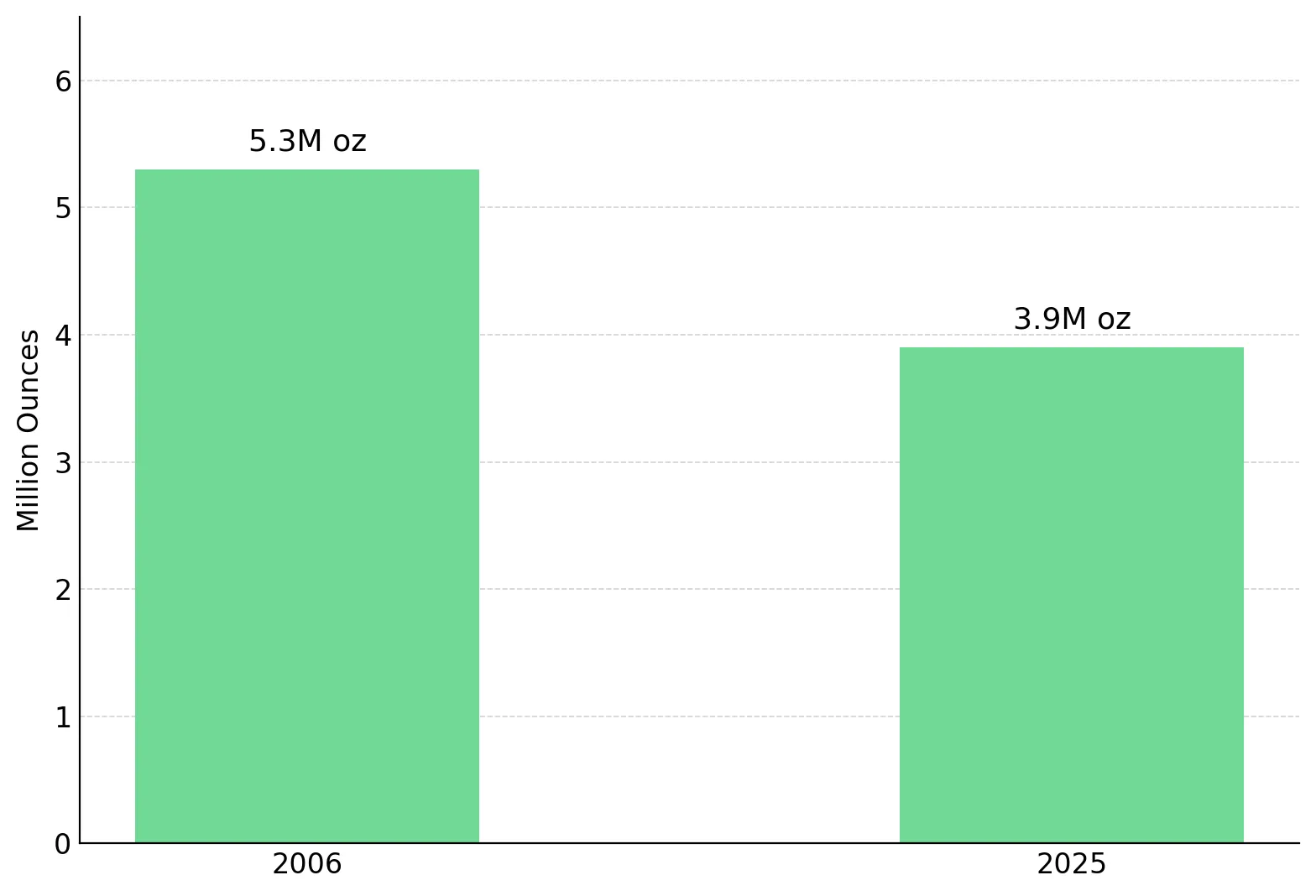

South African Output Has Contracted Despite Multiple Cycles Above $2,000 Per Ounce

South Africa hosts approximately 91% of global platinum reserves in the Bushveld Igneous Complex and accounts for 70% to 80% of annual mined supply. South African primary platinum production declined from approximately 5.3 million ounces in 2006 to 3.9 million ounces in 2025, a 26% reduction that persisted even during periods when platinum traded above $2,000 per ounce. Eskom's electricity tariffs for South African mining operations rose approximately 60% between 2021 and 2026, increasing operating costs for platinum producers.

Existing platinum producers are mining aging deep-level shafts with declining ore grades. Replacing depleted reserves requires multi-billion-dollar shaft development projects that typically take seven to ten years to build.

Nick Smart, Chief Executive Officer of ValOre Metals, describes how platinum supply has continued to decline despite sharply higher metal prices:

"The primary mine production of platinum has been in decline in the last 5 years. In 2021 it peaked at just over 6 million oz. Forecast for this year is around 5 and 1/2 million oz of primary platinum produced. And that's in the context of a metal price which has doubled over the course of the last year.”

Hybrid Vehicles & Industrial Demand Support Platinum Consumption

Faster growth in hybrid vehicle production has offset some expected platinum demand losses from battery electric vehicles. Hybrid vehicles use 10% to 20% more platinum group elements than conventional internal combustion engine vehicles and are now the fastest-growing global automotive segment. Platinum demand is also increasing in glass manufacturing, chemical processing, and Chinese investment purchases.

Guangzhou Futures Exchange Inventories Signal Platinum Delivery Stress

The Guangzhou Futures Exchange June 2026 platinum contract reached an open-interest-to-inventory ratio of approximately 24:1 in May 2026. In commodity futures markets, open-interest-to-inventory ratios above 10:1 can signal delivery stress because short-position holders may lack sufficient physical metal to settle contracts at expiry. The 24:1 ratio indicates significantly tighter physical platinum availability relative to futures positioning.

Physical platinum deliveries reduce available exchange inventories and increase future delivery risk. Some short-position holders are taking physical delivery instead of closing contracts, reducing exchange warehouse inventories. Lower inventory reduces future delivery capacity and widens the Guangzhou premium over London spot prices as available physical metal declines. China accounts for approximately 60% of global platinum demand. As Chinese exchanges absorb more physical metal from international markets, platinum price discovery increasingly shifts toward trading venues with lower Western institutional participation.

China Emissions Standards and Industrial Demand Increase Platinum Loadings

The council reported Q1 2026 industrial platinum demand up 41% year over year, led by a 94,000-ounce increase from the glass sector following recovery from Q1 2025 plant closures. The council forecasts full-year 2026 industrial platinum demand at 2,238,000 ounces, up 11% year over year, with glass-sector demand projected to rise 83%. China's China 7 vehicle emissions standards, taking effect from 2026, are expected to increase per-vehicle platinum group metal loadings to meet stricter cold-start and real-world emissions requirements.

Federal Reserve Repricing Overrides Platinum Supply Fundamentals

Tight platinum supply does not prevent short-term price volatility driven by macroeconomic and geopolitical events. This week's trading showed that changing interest-rate expectations and geopolitical risk sentiment can temporarily outweigh platinum's tightening physical supply outlook. Platinum rose above $2,200 per ounce on May 14, 2026 before falling to $1,922 per ounce on May 20, a 12% decline in five trading sessions despite the council confirming a fourth consecutive annual deficit

Warsh Confirmation Pushes Markets Toward Higher-for-Longer Rates

The Senate confirmed Kevin Warsh as Federal Reserve Chair on May 13, 2026, shifting Federal Open Market Committee pricing toward a more hawkish outlook. Three committee members had already dissented against dovish guidance, and markets now expect zero 2026 rate cuts versus four projected at the start of the year.

Higher real yields reduce the relative attractiveness of non-yielding precious metals, while a stronger US dollar typically pressures dollar-denominated commodity prices lower. US headline Consumer Price Index inflation remains near 4%, while the Federal Reserve projects 2026 core inflation at 2.7%, above its 2% target.

Higher Oil Prices Support Platinum but Pressure Auto Demand

Brent crude has traded between $95 and $118 per barrel since the February 28, 2026 conflict outbreak, according to Dallas Federal Reserve working paper WP2609 published in April 2026. The May 14-15, 2026 Trump-Xi summit produced a White House statement supporting continued access through the Strait of Hormuz, reducing some geopolitical buying pressure in precious metals. Geopolitical risk can support platinum prices through safe-haven buying, but sustained crude oil prices above $100 per barrel can weaken automotive demand by reducing consumer vehicle purchasing power. The automotive sector accounts for approximately 40% of platinum demand.

Supply Concentration Risk Redirects Capital Toward Alternative PGM Jurisdictions

Persistent platinum deficits, concentrated supply, and limited mine expansion are increasing investor interest in platinum projects outside the dominant producing jurisdictions. Institutional investors with limits on Russian exposure or country concentration risk are increasingly funding platinum group element projects in alternative jurisdictions. Investor returns and risk exposure now depend heavily on whether capital is deployed at the exploration, development, or production stage.

Three-Country Supply Concentration Is Raising Platinum Risk Premiums

South Africa, Russia, and Zimbabwe account for approximately 90% of global primary platinum group element supply, while Norilsk Nickel alone produces roughly 40% of global primary palladium. Q1 2026 supply disruptions, including Norilsk's 26% platinum production decline, Zimplats' 56% six-element output decline, and Zimbabwe's export ban on unrefined critical minerals, increased market pricing for platinum group metal supply risk. That tightening is now visible in higher London lease rates and wider Guangzhou Futures Exchange premiums.

ValOre Metals Targets Brazilian Platinum Exposure Outside Core Supply Jurisdictions

ValOre Metals Corp. is targeting completion of a maiden Preliminary Economic Assessment in Q4 2026. Near-term milestones include a resource update incorporating more than 6,000 metres of 2023 drilling across five new zones, including Salvador. University of Cape Town metallurgical testing reported platinum and palladium recoveries of approximately 73% and 74%, respectively, from weathered material using bioleaching methods. The company is also advancing the divestment of Hatchet Uranium Corp. to Future Fuels Inc., with closing expected on or before May 31, 2026 following TSX Venture Exchange conditional acceptance on May 19, 2026.

Exploration-stage mining investments carry higher financing, execution, and liquidity risks than producing miners. ValOre Metals Corp. traded between C$0.085 and C$0.10 on the TSX Venture Exchange during the week of the council’s release, reflecting the elevated volatility typical of early-stage junior explorers. Junior mining companies also commonly rely on equity financings to fund drilling, metallurgical testing, and economic studies, which can dilute existing shareholders through rising share counts.

The Investment Thesis for Platinum Group Metals

- The World Platinum Investment Council confirmed on May 19, 2026 that the platinum market will record a fourth consecutive annual deficit of 297,000 ounces in 2026. Above-ground inventories now cover approximately four months of demand, the lowest level since the council began tracking the market in 2014.

- Approximately 90% of primary platinum group element supply originates from South Africa, Russia, and Zimbabwe, concentrating global supply risk in three jurisdictions. Q1 2026 production declines and Zimbabwe's export ban on unrefined critical minerals increased concerns over physical metal availability, contributing to higher London lease rates and wider Guangzhou Futures Exchange premiums.

- South African supply inelasticity is documented in primary output that contracted 26% from 2006 to 2025 despite multiple price cycles above $2,000 per ounce, with major producers returning record cash flow to shareholders rather than expanding capacity and leaving the supply curve structurally flat through the end of the decade.

- Platinum demand remains resilient despite concerns over electric vehicle adoption. Q1 2026 industrial demand rose 41% year over year, while China's China 7 vehicle emissions standards taking effect from 2026 are expected to increase per-vehicle platinum group metal loadings. Hybrid vehicles also use 10% to 20% more platinum group elements than conventional internal combustion engine vehicles.

- Investors are assigning greater value to platinum group element projects outside South Africa, Russia, and Zimbabwe to reduce geopolitical and supply concentration risk. Exploration-stage developers in alternative jurisdictions provide exposure to that trend but carry multi-year development timelines, inferred-only resources, and shareholder dilution risk. These companies should be evaluated using junior exploration risk assumptions rather than producer-equity valuation metrics.

The World Platinum Investment Council's May 19, 2026 report confirmed a platinum supply deficit that existing mines are unlikely to close quickly because new production capacity requires years to develop. Kevin Warsh's confirmation as Federal Reserve Chair on May 13, 2026 and the subsequent shift toward higher-for-longer interest-rate expectations pressured platinum group metal equities despite tightening physical supply conditions. Investors seeking platinum group metal exposure ahead of expected Q4 2026 project milestones should distinguish between producing miners and exploration-stage developers. Producer equities are increasingly driven by dividends and share buybacks, while exploration companies carry higher execution and shareholder dilution risk. Portfolio allocations to exploration-stage companies should therefore remain smaller than positions in established producers.

TL;DR

The World Platinum Investment Council's May 19, 2026 report confirmed a fourth consecutive annual platinum deficit of 297,000 ounces, with above-ground inventories now covering only about four months of demand, the lowest since 2014. South Africa, Russia, and Zimbabwe control roughly 90% of primary platinum group element supply, and Q1 2026 production declines at Norilsk Nickel and Zimplats, alongside Zimbabwe's export ban on unrefined critical minerals, intensified supply risk. Metals Focus raised its 2026 price forecast to $2,190 per ounce, though Kevin Warsh's confirmation as Federal Reserve Chair pushed platinum from $2,200 to $1,922 in five sessions. Institutional capital is increasingly targeting PGM projects in alternative jurisdictions to mitigate concentration risk.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed