Copper Falls Below US$13,400/t as China Demand Weakens & US$110 Oil Collides With a 17-Year Global Supply Shortage

Copper fell below US$13,400/t as weaker China data and US$110 oil hit sentiment, while long-term supply shortages continue supporting developers.

- Copper fell below US$13,400/t after weaker Chinese factory output, rising SHFE inventories, and Brent crude above US$110 tightened financial conditions for industrial metals.

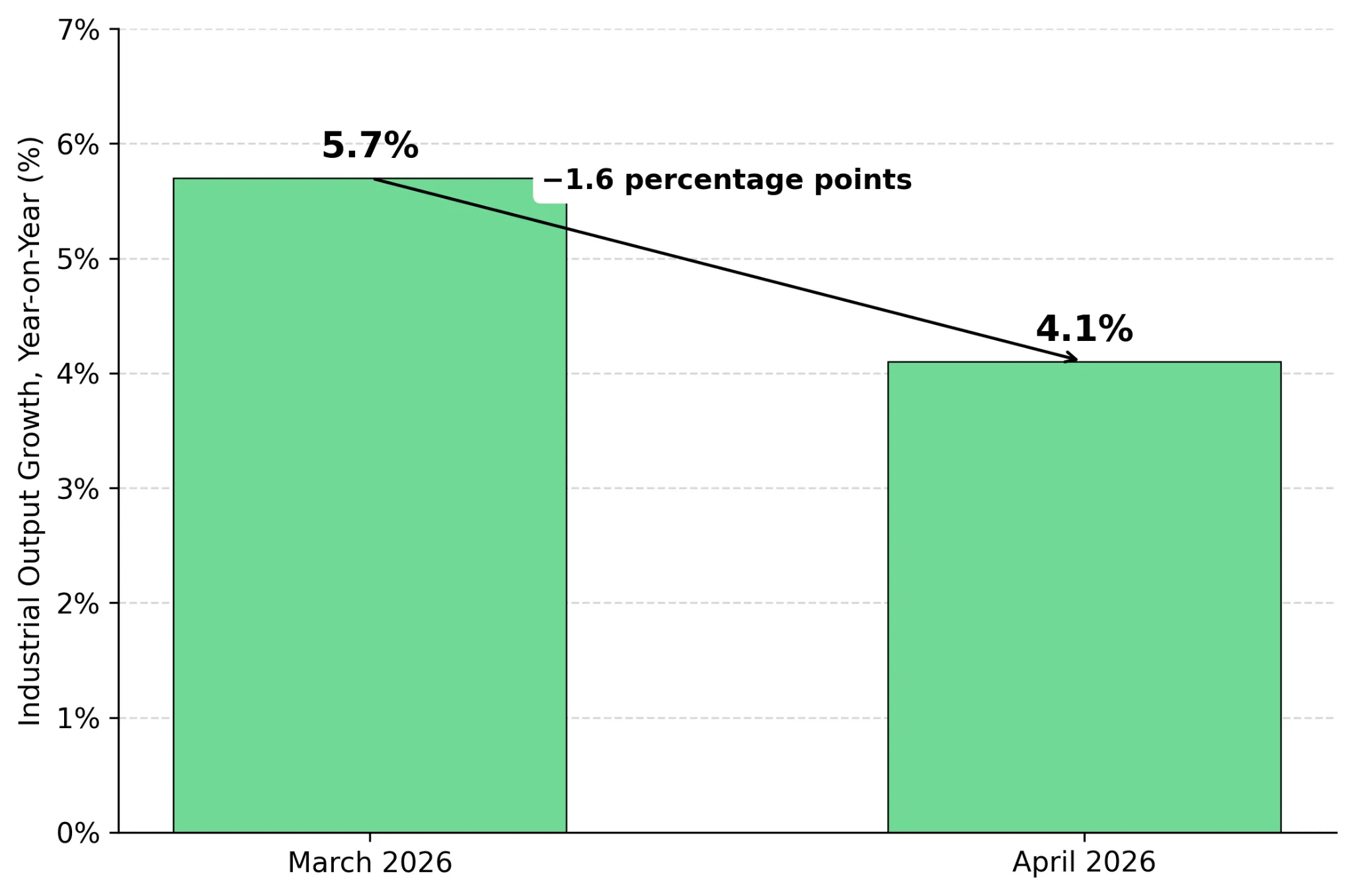

- China’s factory output slowed to 4.1% year-on-year in April 2026 from 5.7% previously, while spot copper premiums flipped into discounts, signalling demand destruction above US$13,500/t.

- Supply constraints remain intact as average copper mine development timelines extend to 17 years and Chile faces zero forecast production growth between 2031 and 2040.

- Capital continues flowing into advanced copper development assets despite volatility, as investors position for a projected 450,000-tonne refined copper deficit in 2026.

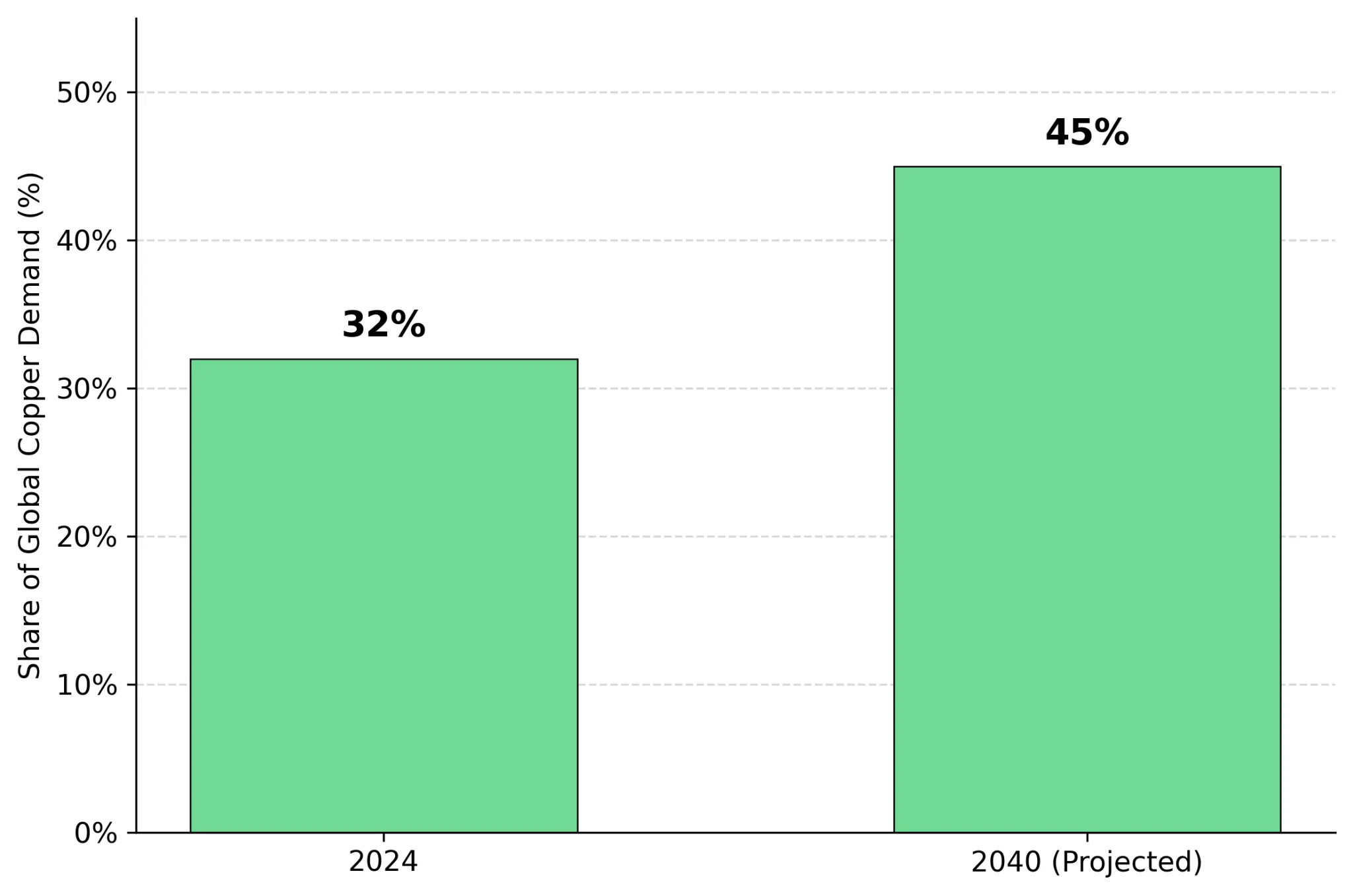

- AI data centres, grid expansion, and electric vehicles are projected to increase strategic copper demand from 32% of global consumption in 2024 to 45% by 2040.

Copper Falls to US$13,394/t as Oil, Dollar & China Slowdown Trigger Short-Term Liquidation

London Metal Exchange three-month copper fell 0.35% to US$13,507.50 per tonne and hit an intraday low of US$13,394.50 per tonne, while the Shanghai Futures Exchange most-active contract dropped 1.40% to 104,330 yuan per tonne. Two forces are now operating on different timeframes: short-term liquidity stress from oil, the dollar, and softer Chinese activity data, against a 2026 refined copper deficit forecast of approximately 450,000 tonnes that no single macro variable can resolve.

UAE Drone Attacks Push Brent Above US$110 & Lift US Dollar to One-Month High, Pressuring Copper and Mining Equities

Brent crude moved above US$110 per barrel on May 18, 2026 after reported drone attacks on the United Arab Emirates over the weekend, lifting near-term inflation expectations and pushing the US dollar index to its strongest level in more than a month. Higher oil raises inflation prints, inflation prints delay Federal Reserve rate-cut pricing, higher real rates support the dollar, and a stronger dollar reduces the affordability of dollar-priced copper for buyers transacting in yuan, euro, or rupee.

Copper equity valuations modelled at long-term price decks above the US$12,000 per tonne minimum incentive level for new mine development become temporarily disconnected from spot during these episodes. Funded developers can hold their feasibility price assumptions through the volatility because their construction timelines extend well past current Federal Reserve rate-decision windows.

China’s 4.1% Factory Output Growth & Rising SHFE Inventories Signal Copper Demand Destruction Above US$13,500/t

China factory output grew 4.1% year-on-year in April 2026, down from 5.7% in March, while retail sales rose only 0.2%, with both readings missing consensus per data from the National Bureau of Statistics. China accounts for approximately 60% of global refined copper demand, which means a 160 basis point industrial production deceleration translates directly into measurable order-flow reductions at the cathode and rod level.

Shanghai Futures Exchange on-warrant copper stocks rose from 88,077 tonnes on May 11 to 97,011 tonnes on May 14, ending a decline that had run since mid-March, and Chinese spot copper premiums over Shanghai Futures Exchange prices flipped into a discount. These two indicators jointly signal price-induced demand destruction above US$13,500 per tonne.

Declining Ore Grades, Long Mine Timelines & Codelco Risk Continue Tightening Global Copper Supply

Mine development timelines, declining head grades, and operational risk at the largest state-owned producer are tightening the available supply base over a multi-year horizon, and these constraints operate independently of the dollar index or monthly Chinese activity data.

BHP Forecasts Zero Chile Copper Production Growth Through 2040

BHP forecasts zero net copper production growth in Chile from 2031 to 2040. The average copper mine development timeline now runs approximately 17 years from discovery to production. Ore grades continue to decline across Chile and Peru, which raises strip ratios, lifts processing costs per tonne of contained metal, and shrinks reserve life at existing operations.

Fitzroy Minerals President and Chief Executive Officer Merlin Marr-Johnson pointed to BHP’s August 2025 outlook, which forecast zero production growth from Chile between 2031 and 2040 despite rising capital intensity across both greenfield and brownfield developments. He stated:

“Production growth within Chile, and globally, is difficult. It’s a very mature industry that is struggling to maintain production. BHP said there’s going to be zero growth from Chile between 2031 and 2040. All of this shows that copper prices have to materially rerate.”

BHP’s outlook increases the strategic value of advanced copper projects outside Chile, particularly in Canada, Australia, and the United States, as supply deficits deepen into the late 2020s. It also strengthens the economics of lower-cost restart projects and suggests current copper price assumptions in many feasibility studies may be too conservative.

Chile Replaces Codelco Chairman After 20,000t Copper Reporting Discrepancy, Raising Governance Risk Across Global Supply Chains

Chile's government on May 14, 2026 named Bernardo Fontaine to replace Maximo Pacheco as chairman of Corporación Nacional del Cobre de Chile effective May 26, with Mining Minister Daniel Mas tasking the new board with an investigation and external audit. Diario Financiero reported that nearly 20,000 metric tons of copper were improperly included in Codelco's 2025 production report based on a preliminary internal audit.

Codelco is the world's largest copper producer and is targeting 1.7 million tonnes of output by 2030 after recording multi-decade production lows in 2022 and 2023. Governance instability and audit risk at the marginal supplier of refined copper raises the political risk premium applied to large state-owned producers and increases the relative valuation appeal of smaller scalable development assets with shorter timelines to first production.

Copper Prices Above US$5/lb Are Driving Major Financings Into Development Assets

Capital markets remain open for copper developers with defined assets. Equity raises and strategic investments executed during the May 2026 volatility window indicate that institutional and strategic capital is pricing through near-term spot weakness to a multi-year supply deficit. Current prices above the US$12,000 per tonne incentive level materially improve internal rate of return assumptions on projects that were already viable at lower price decks.

Copper Prices Above US$5/lb Are Expanding Project Economics Beyond Feasibility Base-Case Assumptions

Marimaca Copper closed a global treasury and secondary offering on February 26, 2026, raising C$409 million gross, including C$129.2 million in net proceeds to the company from the Canadian treasury component. Cash net of working capital increased to US$147.7 million at March 31, 2026 from US$62.7 million at year-end 2025, funding operations for at least the next 12 months. The Marimaca Oxide Deposit in Chile’s Antofagasta region is targeting 50,000 tonnes per year of copper production within three years, with potential silver by-product credits identified across the Pampa Medina drill database.

The Definitive Feasibility Study was modelled at US$4.30 per pound copper, a price deck the spot market has already breached on the upside.

Hayden Locke, President and Chief Executive Officer of Marimaca Copper, quantifies the impact of the move from feasibility-deck pricing to current spot:

“We ran at a US$4.30-per-pound copper price, which now seems awfully low given how much the copper market has moved. Obviously, everything looks a lot better with the copper price where it is today.”

C$30.75M Strategic Financing Funds 80,000m Drill Campaign at a 775Mlb Copper-Equivalent VMS System in Québec’s Abitibi Belt

Abitibi Metals closed a C$30.75 million private placement on May 15, 2026, with Discovery Silver Corp. acquiring a 9.9% stake and participation rights in future financings. The B26 deposit in Québec’s Abitibi Belt hosts 25.3 million tonnes at 2.1% copper equivalent, containing 775 million pounds of copper alongside gold, zinc, and silver credits. Canadian mining M&A activity rose 220% in 2025 to C$62.1 billion, with Eldorado Gold Corporation’s ~C$4 billion acquisition of Foran Mining Corporation highlighting rising valuations for scalable VMS projects in Tier-1 jurisdictions.

The financing funds a 40,000-metre Phase 4 drill program through the first quarter of 2027, advancing concurrent resource expansion, infill conversion of inferred resources to indicated category under National Instrument 43-101, and a Preliminary Economic Assessment.

Jon Deluce, Chief Executive Officer and Founder of Abitibi Metals, sets the operational scale of the deployed capital:

“This injects US$31 million into a market that is still volatile. We now have a war chest to deliver more than 80,000 meters of drilling, complete the PEA, and put a huge dent into our feasibility study.”

Explorers With Scalable Drill Programs Are Leveraging Copper Scarcity to Accelerate Resource Growth

Exploration-stage companies with near-surface mineralisation and infrastructure-adjacent locations are also drawing capital. The market is pricing geological scalability and reduced capital intensity into valuations that previously discounted exploration-stage equity heavily.

78m at 1.70% Copper & a 5km Seismic Target Corridor Support Low-Capex Development Potential in Chile’s Copiapó District

Fitzroy Minerals reported 78 metres at 1.70% copper, including 40 metres at 3.02% copper, from drill hole BRT-DDH059 at the Buen Retiro Project near Copiapó, Chile. Hole BRT-DDH058 returned 75 metres at 0.82% copper, including 8 metres at 3.77% copper. An Ambient Noise Tomography survey by Fleet Space Technologies confirmed major geological structures across a 5km by 5km corridor at depths of 1-2km. The 13,400-hectare project also benefits from a potential heap-leach partnership with Pucobre, providing a possible low-capex route to production.

Marr-Johnson outlines the operational and capital-intensity advantage:

“This would give us non-operated cash flow with very low capital intensity. It’s a low-cost operation to bring into production.”

US$330M of Existing Infrastructure Lowers Restart Capital to ~US$225M at a High-Grade Yukon Copper Restart Project

Selkirk Copper launched a 50,000-metre Phase 2 drill program at Yukon’s past-producing Minto Mine on May 1, 2026. The new 117 Lens returned 12.6 metres at 1.98% copper equivalent within 86.8 metres at 0.58% copper equivalent. Existing infrastructure worth more than US$330 million lowers estimated restart capital to roughly US$225 million versus US$800-900 million for a comparable greenfield project. The operation is targeting 91% copper recovery, 39-40% concentrate grades, and first production by mid-2028 at approximately 30,000 tonnes per annum copper equivalent.

Colin Joudrie, President and Chief Executive Officer of Selkirk Copper Mines Inc., quantifies the capital efficiency:

“Most major mining operations today... they’re massive infrastructure undertakings, where companies are building ports, roads, power lines, and power plants. We don’t have to do that.”

AI, Grid Expansion & EV Demand Are Reshaping Copper Equity Valuations

Strategic copper demand from AI data centres, grid expansion, and electric vehicles is projected to rise from approximately 32% of global demand in 2024 to 45% by 2040, supported by multi-year infrastructure spending that is less price-sensitive than traditional construction demand.

Solar installations require roughly 4,000-5,000 tonnes of copper per gigawatt, offshore wind requires 8,000-10,000 tonnes, and hyperscale data centres require up to 4,000 tonnes for power distribution infrastructure. As supply visibility tightens, developers with funded treasuries, scalable district assets, strong jurisdictions, and existing infrastructure are increasingly attracting valuation premiums and merger-and-acquisition interest ahead of first production

The Investment Thesis for Copper

- Copper deficits projected at approximately 450,000 tonnes for 2026 remain structurally supported by electrification demand regardless of quarterly Chinese activity data.

- Oil-driven inflation prints and delayed Federal Reserve rate cuts are creating spot-price volatility without resolving the multi-year mine supply shortage.

- Advanced developers with treasuries funding programs into 2027 carry lower equity-issuance risk than peers requiring near-term capital raises into volatile markets.

- District-scale volcanogenic massive sulphide systems in stable jurisdictions are pricing at premiums established by the C$4 billion Foran Mining transaction in 2025 and the 220% surge in Canadian mining merger and acquisition activity to C$62.1 billion that year.

- Restart assets with existing processing and power infrastructure can target restart capital at roughly 25% of greenfield-equivalent build cost, materially compressing time to cash flow.

- Long-duration electrification demand from solar at 4,000 to 5,000 tonnes per gigawatt, offshore wind at 8,000 to 10,000 tonnes per gigawatt, and hyperscale data centres at 2,000 to 4,000 tonnes each anchors valuations in policy-driven rather than purely cyclical demand.

Near-term pressure from US$110 Brent, a one-month-high dollar index, and softer April Chinese data is exposing undercapitalised projects while leaving the 17-year copper development timeline and 450,000-tonne 2026 deficit intact. Investors are distinguishing between speculative copper exposure and funded development platforms targeting production into the late 2020s supply window. The intersection of oil-driven inflation, China demand cyclicality, governance risk at Codelco, and electrification demand sharpens rather than dilutes the investment case for copper developers and explorers with disciplined capital structures and defined assets.

TL;DR

Copper prices corrected after weaker Chinese factory data, rising SHFE inventories, and Brent crude above US$110 tightened financial conditions and strengthened the US dollar. Despite short-term demand weakness, the long-term copper investment thesis remains intact because mine supply growth is constrained by 17-year development timelines, declining ore grades, and governance risks at major producers including Corporación Nacional del Cobre de Chile. Developers and explorers continue raising capital into volatility, with Marimaca Copper Corp. and Abitibi Metals Corp. securing major financings as investors position for deficits driven by electrification, AI data centres, and grid expansion.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed