China's Demand Slowdown & Rising Inventories Are Repricing Copper's Near-Term Outlook

Copper outlook shifts as China demand weakens and inventories rise, pressuring prices short term while long-term electrification demand remains strong

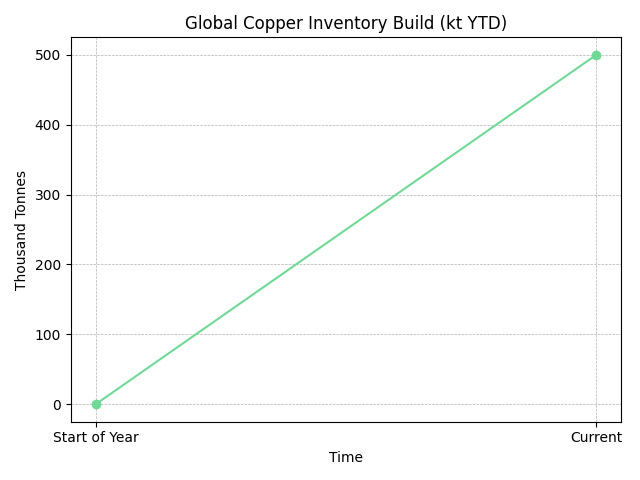

- The collapse of the Yangshan premium and a year-to-date inventory build exceeding 500,000 tonnes signal a transition from supply tightness to improving physical availability.

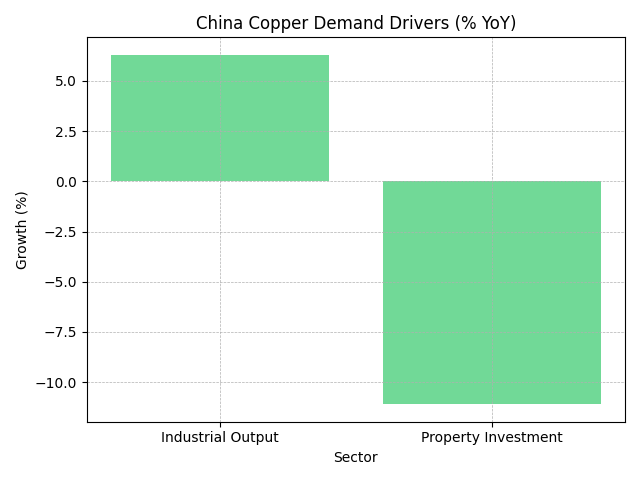

- China's macro divergence, industrial output growth of 6.3% year-over-year contrasted with property investment contraction of 11.1%, is generating conflicting demand signals that complicate near-term price forecasting.

- Macro headwinds including US dollar strength, elevated energy prices, and geopolitical uncertainty are reinforcing downside pressure on copper below the $13,000 per tonne threshold.

- Despite short-term price weakness, structural demand from artificial intelligence infrastructure, electrification, and grid expansion continues to underpin the long-term investment case for copper.

- Project quality, cost structure, capital adequacy, and jurisdictional stability are increasingly determining investor outcomes in this environment, not commodity price direction alone.

Copper's Macro Reset: From Structural Bull to Cyclical Reality

The copper market is entering a near-term regime shift, moving from a scarcity-driven narrative to a more macro-sensitive, cyclical phase. After a prolonged period where supply constraints dominated pricing, the market is now responding to a broader and less directional set of signals.

Prices have fallen in four of the last five sessions, breaking below the $13,000/t level, with weakness driven primarily by demand, not geopolitics. Copper is increasingly behaving as a global growth proxy, reacting to the US dollar, interest rates, and forward growth expectations.

This signals a recalibration of valuation frameworks. While the long-term structural case remains intact, near-term positioning must reflect greater macro sensitivity rather than pure supply-driven dynamics.

China's Demand Weakness: The Dominant Driver

China accounts for ~50% of global copper demand, making it the key driver of near-term price formation. Current indicators are weakening across the board: the Yangshan import premium has fallen to its lowest since mid-2024, fabricator demand is slowing, and import volumes are declining, signaling real-time softness in the physical market.

The more complex issue is China’s internal divergence. Industrial output remains strong at ~6.3% YoY, supporting manufacturing demand, but property investment is down 11.1% YoY, weighing on one of copper’s most intensive sectors. This creates a dual-speed dynamic where headline growth appears resilient while core demand segments weaken.

Copper demand in China is no longer uniformly cyclical, it is increasingly policy-driven and sector-fragmented, making top-down demand forecasting more difficult.

Development Exposure to Chinese Demand Cycles

For companies at the development and exploration stage, exposure to Chinese demand is primarily indirect, channeled through commodity price levels, financing conditions, and investor risk appetite rather than direct offtake relationships. Developers such as Marimaca Copper Corp. , which are advancing projects toward construction decisions, are most sensitive to price volatility as it affects project financing feasibility and the discount rates applied in net asset value assessments. Explorers operating earlier in the capital cycle face a different but related dynamic: risk appetite in capital markets tends to compress during periods of commodity price softness, making resource delineation and project advancement more capital-intensive on a relative basis.

Marimaca Copper Corp. has reached a pivotal development milestone that positions it ahead of the financing cycle, with Chief Executive Officer Hayden Locke commenting on the significance of the definitive feasibility study completion:

“We confirmed what we already knew: industry-leading capital costs, very competitive operating costs, and industry-leading return on invested capital metrics.”

Inventory Builds Signal a Market Rebalancing

One of the most institutionally significant signals in current copper market structure is the scale of the inventory build that has accumulated year-to-date. Global copper inventories have increased by more than 500,000 tonnes, with Shanghai Futures Exchange (SHFE) inventories reaching record highs and London Metal Exchange (LME) inventories at their highest levels in 17 months. These are not marginal adjustments; they represent a fundamental shift in the physical supply-demand balance.

The inventory build is being driven by a combination of rising Chinese refined copper production and reduced import dependency. As domestic output has expanded, the need to draw down exchange inventories or source additional imports has diminished. This dynamic is reinforced by weak fabricator demand, creating a compounding effect on visible supply metrics. The LME cash-to-three-month spread has normalized from backwardation toward contango, reducing the premium previously associated with prompt physical availability.

For market participants, these signals indicate that the tightness narrative that supported copper prices through much of 2023 and 2024 has materially weakened. The market is transitioning toward balance and potentially toward a short-term surplus in refined copper, even if mined supply constraints persist at the concentrate level. This distinction, between refined copper availability and mined copper supply, is important and is often conflated in more generalist market commentary.

Impact on Valuation Metrics

Rising inventories typically compress valuation multiples for copper assets. EV/lb contracts as spot prices soften, while NAV models apply higher discount rates as forward price expectations weaken.

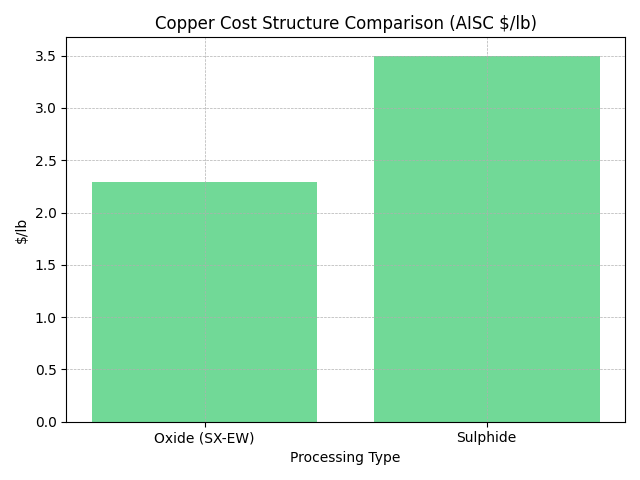

Marimaca Copper Corp. remains relatively insulated, with DFS economics showing AISC of $2.29/lb and IRR of 31%, supporting margins even at lower prices. For explorers like Abitibi Metals Corp., valuation is driven more by resource scale and in-situ value, creating some decoupling from short-term price moves as long as growth catalysts are delivered.

Macro Headwinds: Dollar, Energy & Geopolitics

Beyond China, copper is being pressured by broader macro headwinds. A stronger US dollar is reducing purchasing power in non-dollar markets, while elevated energy prices are raising AISC and compressing margins, particularly for higher-cost operations.

Geopolitical tensions, especially in the Middle East, are driving risk-off sentiment that weighs on equities. The declining copper-to-oil ratio points to weakening global growth expectations, and although lower real rates are supportive, this is currently outweighed by soft demand and rising inventories.

Cost Inflation & Margin Sensitivity

Higher energy prices have an asymmetric impact across copper operations depending on processing method and project configuration. Diesel costs affect open-pit mining fleets, while power costs are material for electrowinning and solvent extraction processes. Heap leach oxide operations, which rely on lower capital intensity and simpler processing circuits, tend to exhibit greater margin resilience in inflationary cost environments relative to sulphide concentrator operations.

Fitzroy Minerals Inc.. has structured its project development to prioritize capital efficiency and near-term cash generation, with Chief Executive Officer Merlin Marr-Johnson describing the strategic rationale for the Chile asset:

“Bertrero is at low elevation with superb surrounding infrastructure, making it a highly attractive project location. We are currently working on terms with PCORE for a heap leach joint venture. This operation has the potential to generate near-term, non-operated cash flow, which we believe will distinguish us from many other explorers in the market.”

Structural Bull Case vs. Cyclical Weakness

Near-term headwinds should be weighed against a structurally strong demand outlook. AI-driven data center buildout is emerging as a meaningful new source of copper demand, while electrification trends, particularly electric vehicles, continue to accelerate. Grid expansion alone is expected to account for over 60% of incremental demand growth in the next decade, according to Goldman Sachs.

On the supply side, structural constraints remain unresolved. Declining ore grades, longer permitting timelines, and rising capital costs continue to limit new supply. The International Copper Study Group estimates a current deficit of around 150,000 tonnes, although forecasts diverge, with Goldman Sachs modeling potential near-term surplus scenarios depending on Chinese demand and project ramp-ups.

The market is in a transitional phase where cyclical pressures are masking intact long-term fundamentals, potentially creating an entry opportunity for long-term investors.

Long-Term Optionality in Exploration Assets

Exploration assets with meaningful scale and strong discovery economics offer leveraged exposure to long-term copper upside while mitigating near-term price volatility. Abitibi Metals Corp. has delineated a 25.3 million tonne resource at approximately 2.1%-2.2% copper equivalent, with over 125% year-over-year growth. Multi-metal credits from gold, silver, and zinc further enhance project economics by lowering effective costs.

Abitibi Metals Corp. has pursued a disciplined capital efficiency strategy throughout its resource expansion program. Chief Executive Officer and Founder Jon Deluce addresses the company's approach to discovery cost and competitive positioning:

“Discovery cost is 2.5 cents per pound of copper equivalent. I would put us up against any of our competitors to find someone who has done it more cost-efficiently.”

The company has a fully funded 40,000-metre drill program planned for 2026, providing a near-term catalyst for continued resource expansion independent of commodity price direction. For investors, the combination of scale, discovery efficiency, and funding certainty positions the asset as a potential acquisition target for major producers seeking to replenish depleting reserve bases.

Capital Markets Are Repricing Risk

Copper equities are entering a valuation reset as tighter financing conditions and weaker commodity prices compress risk appetite. Investors are shifting focus toward balance sheet strength, near-term catalysts, and proven management, rather than speculative resource potential.

Companies with secured funding or sufficient capital to reach key milestones are commanding valuation premiums, while underfunded peers face dilution and execution risk. In this environment, capital structure discipline has become a key driver of competitive positioning.

Fitzroy Minerals Inc. has raised approximately $26 million, funding feasibility work and drilling through key milestones. Its financing structure, including warrants at $0.80 versus a $0.50 placement price, aligns dilution with higher valuation thresholds, highlighting the importance of financing terms in a repricing market.

Jurisdiction & Infrastructure as Macro Buffers

As macro volatility rises, jurisdictional quality is becoming a key valuation driver. Projects in stable, well-developed mining regions attract lower discount rates and broader institutional capital.

Chile offers strong permitting frameworks, infrastructure, and technical expertise. Marimaca Copper Corp. benefits from this, with environmental approval in place and a targeted 2026 construction start. Similarly, Quebec provides a Tier-1 jurisdiction with low political risk and strong infrastructure. Abitibi Metals Corp. operates within this environment, enhancing risk-adjusted returns through lower execution risk and financing costs.

The Investment Thesis for Copper

- Copper's long-term demand trajectory remains structurally supported by electrification, artificial intelligence infrastructure, and grid investment, with demand growth driven by applications that are policy-mandated or economically irreversible.

- Marimaca Copper Corp. offers near-term production leverage through a fully permitted, low-cost oxide project in Chile with a 31% internal rate of return and all-in sustaining costs of $2.29 per pound, providing meaningful margin resilience across a wide range of copper price scenarios.

- Fitzroy Minerals Inc. is differentiated by its combination of Chilean jurisdictional advantage, near-term non-operated cash flow potential through a heap leach joint venture structure, and a fully funded work program that removes dilution uncertainty over the near-term development horizon.

- Abitibi Metals Corp. provides long-duration exploration optionality through a large-scale copper-gold-silver-zinc volcanogenic massive sulphide system in Quebec, with a discovery cost of 2.5 cents per copper-equivalent pound and a fully funded 40,000-metre drill program providing near-term resource growth catalysts.

- Multi-commodity deposits with meaningful gold and silver credits offer investors a natural hedge against copper price volatility, as the economic viability of the project is less sensitive to the performance of any single metal.

- Tier-1 jurisdictions in Chile and Quebec reduce the discount rates embedded in net asset value models and support access to lower-cost project financing, providing a structurally lower cost of capital relative to assets located in higher-risk environments.

- Companies with adequately capitalized balance sheets are positioned to execute on development milestones and resource delineation programs without dilutive equity raises at depressed valuations, creating a meaningful performance differential relative to underfunded peers in the current environment.

The copper market is not experiencing a structural breakdown. It is undergoing a valuation reset that reflects the convergence of cyclical demand weakness, inventory normalization, and macro headwinds. China's property sector contraction is real, but it is occurring alongside persistent industrial output growth and an expanding pipeline of electrification-linked demand. The inventory build that has accumulated year-to-date signals improving physical availability, not the emergence of structural oversupply.

The analytical distinction between cyclical normalization and structural deterioration is the critical variable. The supply-side constraints that have been building for years, declining ore grades, extended permitting timelines, capital cost inflation, have not been resolved. They have merely been temporarily obscured by weaker near-term demand. When the demand cycle turns, as China's property investment eventually stabilizes and electrification demand continues its compound growth trajectory, the supply response will remain constrained.

What separates the investment opportunities that will generate differentiated returns in this environment are project economics, capital structure, jurisdictional quality, and management execution. Copper remains the clearest macro proxy for global industrial activity and the energy transition, but in 2026 it is increasingly evident that timing, balance sheet discipline, and asset quality, not commodity price direction alone, will determine where value accrues.

TL;DR

Copper is undergoing a near-term reset, driven by weakening Chinese demand and a sharp rise in inventories (+500kt YTD), shifting the market from tight supply to improving availability. Macro headwinds, USD strength, energy costs, and geopolitics, are reinforcing downside pressure below $13,000/t, while China’s split economy (strong industry vs weak property) complicates demand visibility. Despite this cyclical softness, the long-term bull case remains intact due to electrification, AI, and grid demand. In this environment, returns will be driven less by copper prices and more by project economics, capital discipline, and jurisdictional quality.

FAQs (AI generated)

Copper is softening primarily due to weak Chinese demand and rising inventories, not supply shocks. The collapse in the Yangshan premium, slowing imports, and record exchange stocks all point to a physical market where supply is currently outpacing demand. This marks a shift away from the tightness seen in 2023-2024 and explains the recent price decline below $13,000/t.

Yes. China accounts for ~50% of global demand, but its impact is now more complex. Industrial output remains strong, but the property sector (a major copper consumer) is contracting sharply, creating a fragmented demand profile. This means copper is no longer purely cyclical in China; it is increasingly policy-driven and sector-specific, making forecasting more difficult.

Not necessarily. The current inventory build reflects short-term rebalancing in refined copper, driven by higher Chinese production and weaker demand. However, structural constraints in mined supply, such as declining grades and permitting delays, remain unresolved. The key distinction is that refined supply is temporarily abundant, but long-term supply risks persist.

Copper equities are undergoing a valuation reset, with lower EV/lb multiples and higher discount rates applied to projects. Investors are prioritizing low-cost assets, strong balance sheets, and near-term catalysts. Companies with solid economics, funding visibility, and Tier-1 jurisdictions are outperforming, while underfunded or high-cost projects face greater pressure.

Yes. Structural demand from electrification, AI infrastructure, and grid expansion continues to grow and is largely policy-driven. While near-term macro conditions are masking this trend, the underlying supply-demand imbalance remains unresolved. For long-term investors, the current weakness represents a cyclical reset rather than a structural breakdown, with opportunities concentrated in high-quality assets.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed