Export Restrictions & Input Cost Inflation Lifting Critical Mineral Price Floors

Export restrictions, rising input costs, and supply-chain realignment are driving higher critical mineral prices and concentrating capital into Tier-1 assets.

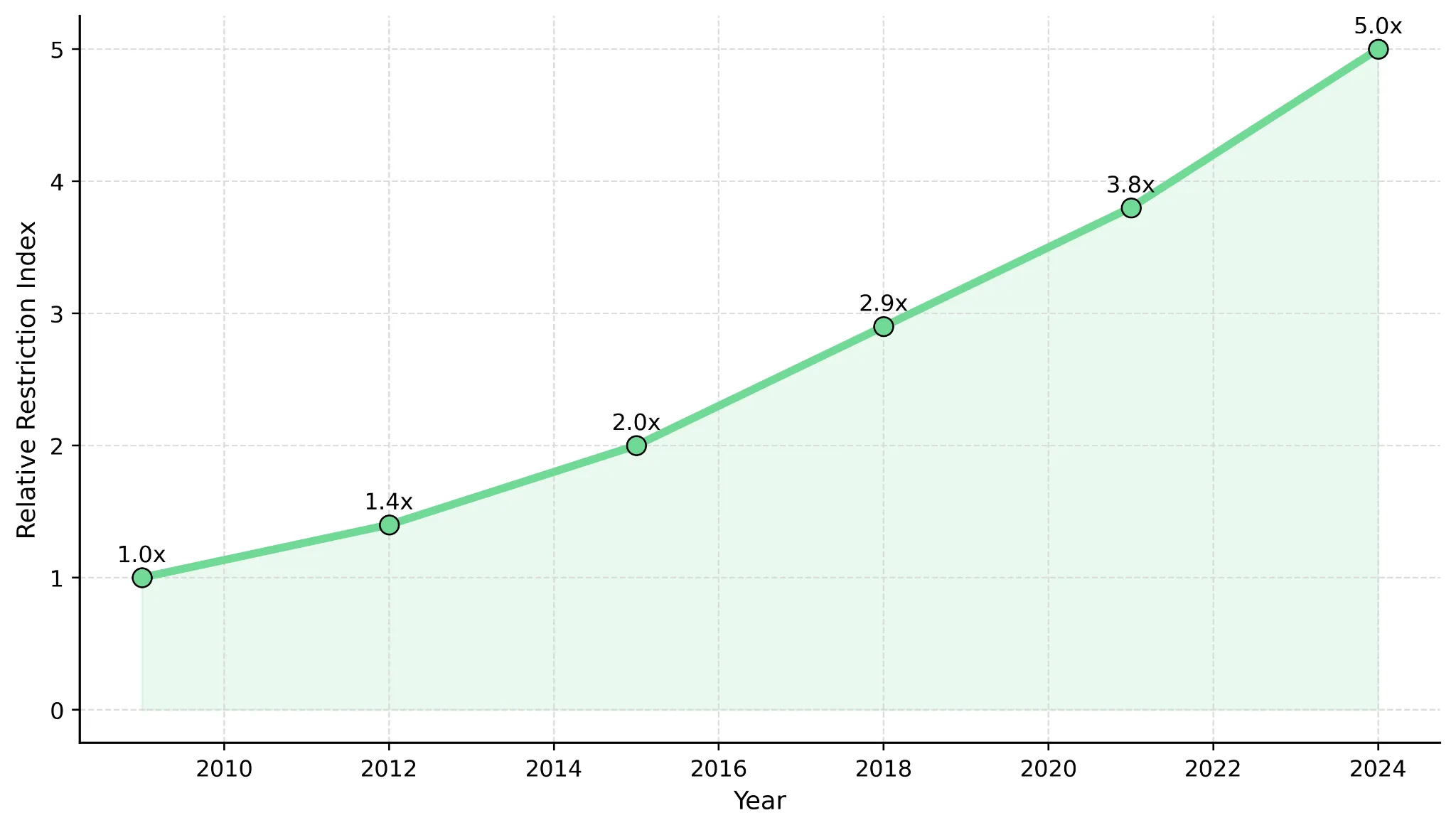

- The OECD Inventory of Export Restrictions on Critical Raw Materials (April 2026) records an approximately fivefold increase in restrictive measures between 2009 and 2024, reducing volumes available for international trade and forcing buyers to pay risk premia in long-term supply contracts.

- Three countries control more than 75% of mined production across several critical minerals per the OECD inventory, with the Democratic Republic of Congo supplying approximately 70% of cobalt and Indonesia dominating refined nickel, increasing pricing power for producing jurisdictions.

- Sulfur prices above $1,000 per tonne against a historical baseline near $150 per tonne have added $1,000 to $3,000 per tonne of nickel to HPAL production costs, raising laterite breakeven prices and shifting the global nickel cost curve upward.

- The WWF EU Battery Supply Chain Report (March 2026) estimates recycling could meet 24% to 68% of demand by 2040, leaving a near-term supply gap that primary mining must fill against 10 to 18 year project development timelines.

- Capital is concentrating in advanced projects, evidenced by Energy Fuels' $700 million convertible note raise at a 0.75% coupon with demand seven times oversubscribed and Lifezone Metals' Q1 2026 drawdown of $25 million from a $60 million facility, lifting valuation multiples for first-quartile-cost OECD assets.

Export Restrictions Are Removing Supply from International Markets & Resetting Delivered Costs

Export restrictions reduce the volume of material available for international trade, forcing buyers to secure supply through alternative channels at higher unit costs. The OECD Inventory of Export Restrictions on Critical Raw Materials (April 2026) documents an approximately fivefold increase in such measures between 2009 and 2024, with the largest concentration in battery and energy transition minerals. Producers in restricting jurisdictions prioritise domestic processing, reducing seaborne supply and lifting the price buyers pay for the remaining tradable volumes.

The Democratic Republic of Congo introduced cobalt export curbs in February 2025 and replaced its full ban with strict quotas in October 2025, driving benchmark cobalt prices more than 160% higher and quadrupling the price of cobalt hydroxide. Zimbabwe banned exports of lithium concentrates in February 2026 to compel local sulfate production, and Guinea has announced plans to control the volume of bauxite ore supplied to international markets to encourage domestic alumina conversion. Each policy step removes intermediate-stage supply from international markets, raising input costs for downstream manufacturers and lifting realized prices for upstream producers operating outside the affected jurisdictions.

Chinese miners hold material capital exposure to these policies. Sinomine Resource Group, Zhejiang Huayou Cobalt, and other Chinese firms have committed approximately $2.8 billion to Zimbabwean lithium projects since 2020, and CMOC has invested approximately $9 billion into two Congolese copper-cobalt operations since 2016. CMOC can currently export only approximately a quarter of its 2024 cobalt production volumes under the Congolese quota, demonstrating that policy intervention can compress export volumes faster than producers can adjust mine schedules. Africa contributes 10.6% of global critical mineral exports according to OECD data published in April 2026, the majority leaving the continent in raw or semi-processed form, leaving downstream margin available for capture by integrated producers operating processing assets aligned with allied-sourcing requirements.

Indonesia's Quota System Is Constraining Nickel Supply Growth & Lifting Prices

Indonesia has shortened its mining quota allocation period from three years to one year, allowing more frequent policy intervention and reducing supply predictability across the nickel value chain. Nickel prices traded at approximately $19,200 per tonne within an $18,500 to $20,000 range in early 2026, attributable to supply tightening from quota changes and inventory drawdowns rather than a cyclical demand pulse.

The policy change is permanent, supporting higher long-term nickel price assumptions in feasibility models and lifting Net Present Value (NPV) and Internal Rate of Return (IRR) for advanced sulfide projects in OECD jurisdictions.

Mark Selby, Chief Executive Officer of Canada Nickel, frames the durability of the shift:

"This is a sustained fundamental shift in the nickel market. The Indonesian government has been taking lots of steps to maximize value as opposed to maximizing volume."

Sulfur Cost Inflation Is Shifting the Nickel Cost Curve Upward

High Pressure Acid Leach (HPAL) processing depends on sulfuric acid, and sulfur prices above $1,000 per tonne represent more than a sixfold increase relative to a historical baseline near $150 per tonne. The increase adds approximately $1,000 to $3,000 per tonne of nickel to laterite production costs, raising breakeven prices for HPAL producers and compressing margins for operators reliant on imported reagent sulfur. The same sulfuric acid supply constraint is increasingly influencing copper markets, where spot prices have doubled and suspended Chinese sulfuric acid exports to Chile have emerged as a critical supply-side bottleneck.

The cost increase shifts the global nickel cost curve upward because marginal HPAL producers require higher commodity prices to remain cash-positive. Sulfide deposits do not face this exposure because sulfur is contained within the orebody, eliminating the requirement to purchase and transport reagent sulfur. Canada Nickel's Crawford project reports a C1 cash cost of $0.39 per pound per its 2025 Feasibility Study, placing it in the first quartile of the global nickel cost curve and sustaining positive operating margins at nickel prices where HPAL laterites operate at or below breakeven.

Long Development Timelines Are Locking in Near-Term Supply Deficits

The WWF EU Battery Supply Chain Report states that lithium-ion batteries will remain the dominant battery technology through at least 2030, sustaining demand for lithium, nickel, graphite, and manganese. Battery energy storage systems are forecast to account for 30% to 36% of total lithium demand by 2030, layering grid-scale storage demand on top of electric vehicle requirements and reinforced by US defense procurement directed toward critical mineral stockpiling under Project Vault.

Mine development timelines of 10 to 18 years prevent rapid supply responses, because projects must progress sequentially through exploration, feasibility, permitting, financing, construction, and ramp-up. Recycling could meet 24% to 68% of demand by 2040 according to the WWF report but cannot close the gap before 2030 given current end-of-life battery volumes, leaving primary mining as the binding supply constraint. Projects reaching production between 2026 and 2030 are positioned to sell into a primary supply deficit, supporting realized prices above feasibility-study assumptions and shortening capital payback periods relative to base-case models.

Jurisdiction & Value Capture Determine Discount Rates & Financing Outcomes

Projects in OECD jurisdictions receive lower risk premia than those ranked lower on the Fraser Institute index, lifting NPV at constant cash-flow assumptions. Africa generates more than 50% of its export revenues from mining according to the April 2026 OECD data but captures only approximately 40% of the potential mineral value, with the gap attributable to limited domestic processing capacity. Projects that integrate processing within Africa and secure offtake agreements capture margin that would otherwise be realized offshore.

Sovereign Metals' Kasiya project illustrates the impact of scale and cost position on valuation. The Definitive Feasibility Study, summarised in the company's March 2026 Quarterly Report, records a pre-tax NPV at an 8% discount rate of $2.2 billion, an IRR of 23.4%, and operating costs of $450 per tonne, supporting positive operating margins under price scenarios applied in the DFS sensitivity analysis.

The project is targeting 275,000 tonnes per annum of graphite and 222,000 tonnes per annum of rutile, both classified as critical by the US and the European Union. Large-scale projects in commodities designated critical qualify for government-backed financing facilities such as Export-Import Bank loan structures and EU Critical Raw Materials Act preferential financing channels, lowering blended cost of capital relative to comparable projects in non-designated commodities.

Ben Stoikovich, Chairman of Sovereign Metals, argues that Kasiya’s low-cost position changes the financing profile relative to higher-cost graphite developments that require downstream integration to achieve acceptable returns:

“Where other companies need to go downstream to capture margin and make a return on investment, we don’t need to. We have no intention to. We are a mining company, not a chemistry company.”

Vertical Integration Is Capturing Processing Margins & Lifting EBITDA

China controls approximately 90% of global critical metals processing capacity, 80% of the world's cobalt supply, and 70% of rare earth mining, establishing a non-Chinese capacity shortage that integrated Western producers are positioned to fill at premium pricing aligned with US allied-sourcing mandates.

Scale & Cost Position Expand Financing Optionality

Energy Fuels' White Mesa Mill is the only US facility licensed by the Nuclear Regulatory Commission to process monazite into rare earth oxides, supporting premium contract pricing for output qualifying under US allied-sourcing requirements. The company produced 1.015 million pounds of uranium oxide in 2025 and is targeting 1.5 to 2.5 million pounds in 2026 per its 2025 annual reporting, with long-term contracts priced around $90 per pound. Energy Fuels also raised $700 million in convertible notes at a 0.75% coupon, with demand exceeding supply by more than seven times, evidencing institutional demand for integrated platforms with non-Chinese processing capacity.

Mark Chalmers, Chief Executive Officer of Energy Fuels, argues that fragmented Western rare earth supply chains lack the integration required to compete with vertically integrated Chinese operators, positioning fully integrated platforms to capture greater downstream value:

“To really compete with China you have to have all those steps. You can't be missing a step in the middle of it. The world wants to see fast and quick and you don't get there with a fragment if you just have one island in the middle of this.”

Capital Markets Are Concentrating Funding into a Narrow Set of Advanced Projects

Project finance is being directed toward assets that meet criteria for scale, first-quartile cost position, and OECD jurisdictional siting, narrowing the fundable universe of critical mineral projects and lifting Enterprise Value-per-Resource and Enterprise Value-per-Production multiples for the qualifying cohort while sub-quartile-cost projects defer or cancel financings. The launch of the US Project Vault stockpile programme, paired with a $10 billion Export-Import Bank facility and $2 billion in private finance, reinforces this concentration by anchoring offtake demand to projects that meet allied-sourcing criteria.

Approximately $10 billion has been committed to Zambian mining over the past four years, including KoBold Metals' $2.3 billion Mingomba copper project, which is targeting more than 300,000 tonnes per annum of copper production. Lifezone Metals advanced its Kabanga nickel financing in Q1 2026 with a $25 million drawdown from a $60 million facility and $380 million in contracts released, advancing the project toward its construction-decision financing milestone. Pilot testwork at the company's PGM recycling operation achieved 99% recovery rates for platinum and palladium, validating the metallurgical assumptions in the recycling operation's economic model.

Ingo Hofmaier, Chief Financial Officer of Lifezone Metals, argues that Western governments and financing institutions are increasingly prioritizing high-grade critical mineral projects capable of supplying non-Chinese industrial supply chains:

“We are in regular touch with European capitals, Washington and Tokyo through the MSP, the Mineral Security Partnership. We are very well advanced in due diligence exercises with several of them, and there’s a very strong realization or understanding in these places that this is a strategic asset for the MSP.”

The Investment Thesis for Critical Minerals

- Export restrictions in the Democratic Republic of Congo, Zimbabwe, Indonesia, and Guinea are removing intermediate-stage supply from international markets, raising delivered commodity costs and long-term price assumptions in project revenue models.

- Three countries control more than 75% of mined production across several critical minerals per the OECD inventory (April 2026), increasing pricing power for producing jurisdictions and adding contract premia for diversified supply.

- Sulfide deposits eliminate reagent-sulfur exposure, lowering AISC by an estimated $1,000 to $3,000 per tonne of nickel relative to HPAL operations.

- Mine development timelines of 10 to 18 years are creating supply deficits that support realized commodity prices above feasibility-study assumptions for projects entering production between 2026 and 2030.

- Recycling could meet 24% to 68% of battery metals demand by 2040 per the WWF March 2026 report but cannot close the gap within the decade, leaving primary mining as the binding supply constraint.

- Vertical integration captures processing margins, lifting EBITDA and reducing reliance on third-party processors concentrated in China across rare earth oxides, lithium chemicals, and cobalt sulfate.

Export restrictions and input cost inflation are raising delivered commodity costs by quantifiable amounts across cobalt, lithium, nickel, and bauxite, lifting the price floors used in project economics. The cost gap between sulfide and HPAL laterite operations, combined with jurisdictional risk pricing in discount rates and the shortage of permitted non-Chinese processing capacity, is determining which assets secure financing and which command valuation premia. Returns are concentrated in projects that combine first-quartile operating costs, alignment with allied-supply policy frameworks, and scalable production, because these factors govern both profitability and access to capital in supply-constrained markets that policy intervention is reinforcing rather than relieving.

TL;DR

Governments are tightening control over critical mineral exports, while rising sulfur and processing costs are increasing global production breakevens for nickel, cobalt, lithium, and rare earths. These pressures are lifting long-term commodity price floors and concentrating capital into large-scale, low-cost projects located in OECD or allied jurisdictions. Companies with vertically integrated processing capacity, strategic offtake alignment, and first-quartile cost structures are securing financing and valuation premiums, while higher-cost or fragmented projects face delayed funding and weaker economics.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed