China's Export Curbs Deepen Global Rare Earth Divide: Western Supply Chains Gain Investor Premium

Beijing's Strategic Controls Create 500%+ Price Premiums as Governments Accelerate Ex-China Capacity Investments

- China’s April 2025 rare earth export curbs triggered a sharp price bifurcation between Chinese and ex-China markets, driving investor capital toward Western-aligned supply chains.

- Prices for dysprosium, terbium, and samarium have surged outside China due to scarcity, while Chinese domestic prices remain stable, highlighting the strategic leverage of export controls.

- Governments in the U.S., EU, Japan, and Brazil are accelerating investment in midstream and downstream REE capabilities, introducing pricing floors, grants, and equity support for new refining capacity.

- Four companies, Energy Fuels, Ionic Rare Earths, Ucore, and Namibia Critical Metals, are executing on near-term catalysts to deliver critical rare earth supply outside of China, particularly heavy REEs.

- Investors are placing premiums on non-China REE producers with jurisdictional strength, downstream integration, and near-term cash flow visibility in refining and magnet materials.

Strategic Fragmentation Reshapes Rare Earth Price Discovery

The global rare earth market has entered a new phase of strategic fragmentation as China leverages export controls to maintain dominance over critical technology inputs. This shift represents more than temporary supply disruptions, it signals a fundamental restructuring of how rare earth elements are priced, traded, and valued across geopolitical boundaries.

China's Export Controls & Policy-Led Price Bifurcation

April 2025 export license restrictions on terbium, dysprosium, yttrium, samarium, gadolinium, and lutetium have deepened supply fragmentation between Chinese domestic markets and international buyers. The implementation of these controls has created unprecedented price divergence that underscores Beijing's strategic control over critical mineral flows.

Domestic Chinese prices remain stable under government oversight, but ex-China markets have experienced dramatic surges: yttrium prices increased 598%, samarium jumped 6,000%, terbium rose 195%, and dysprosium climbed 168%. This bifurcation reflects ex-China markets repricing supply risk, with premiums placed on origin and processing jurisdiction rather than purely on mineral quality or grade.

The cause-effect relationship is clear: restricted export licenses have forced international buyers to compete for limited allocations while Chinese manufacturers maintain access to stable, government-controlled pricing. This dynamic has accelerated Western government intervention and private sector investment in alternative supply chains.

Strategic Resource Leverage in the "Made in China 2025" Era

China's export control strategy aligns with broader national policy objectives to dominate value addition across the rare earth supply chain. Rather than simply exporting raw materials, Beijing aims to secure control over mining, separation, and magnet manufacturing, maintaining leverage over electric vehicles, wind turbines, robotics, and defense technology inputs.

The export restrictions represent calculated policy implementation designed to force foreign manufacturers to either source finished products from China or accept significant cost premiums for alternative supply. This approach supports China's "Made in China 2025" strategy by ensuring domestic manufacturers maintain competitive advantages in critical technology sectors.

Policy Response & Capital Formation in Ex-China Markets

Western governments have responded to China's strategic controls with unprecedented policy coordination and capital deployment. This response extends beyond traditional trade measures to include direct equity investments, pricing floors, and industrial capacity building programs designed to establish independent rare earth supply chains.

United States, European Union & Allied Industrial Policy Accelerates

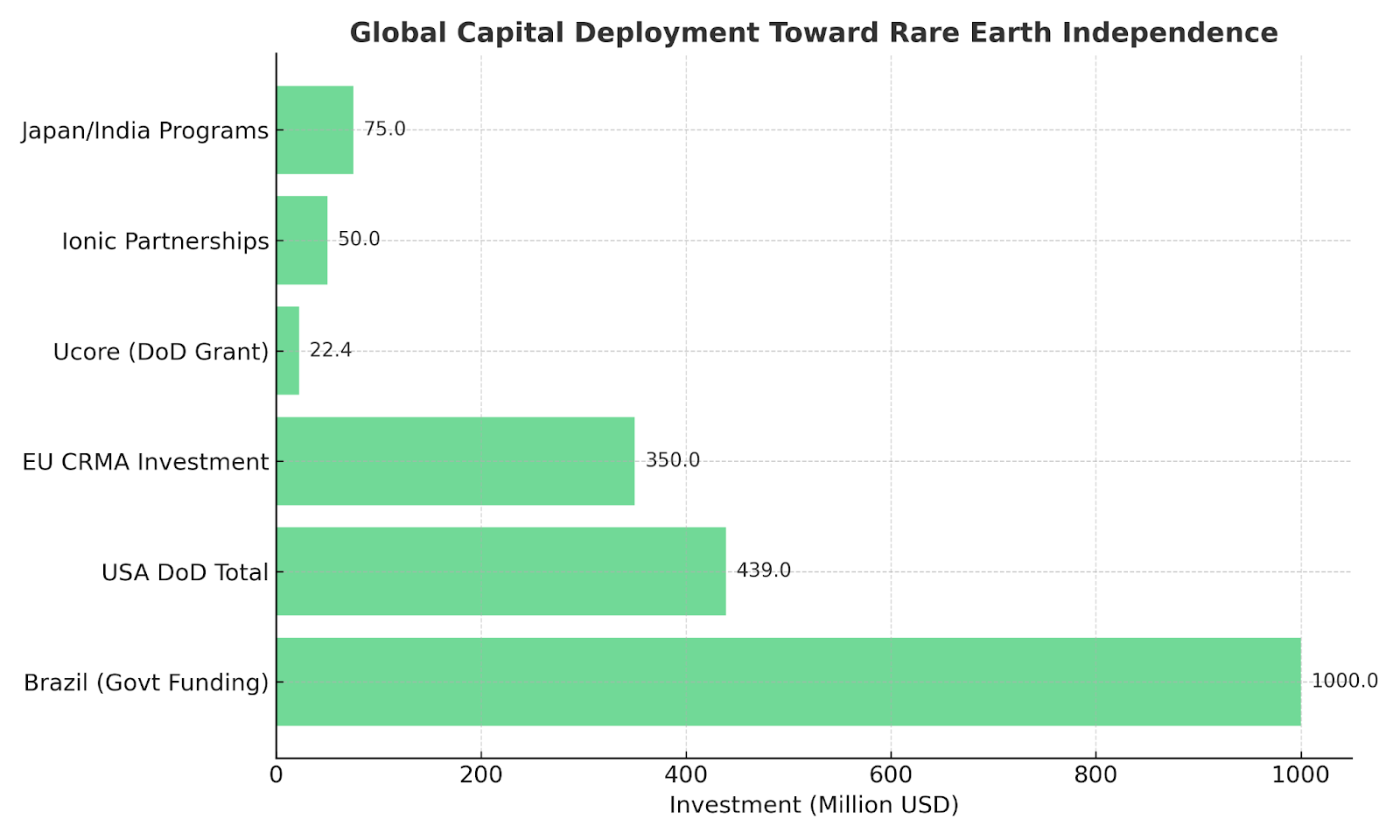

The United States Department of Defense has committed $439 million to mine-to-magnet initiatives, including equity positions and direct grant funding. Ucore Rare Metals received $22.4 million in Department of Defense grants to advance commercial deployment of rare earth separation technology. The European Union Critical Raw Materials Act mandates 10% domestic mining and 40% processing capacity by 2030, supported by co-investments in Estonia and Zambia.

Japan and India are forming magnet supply partnerships while Brazil commits nearly $1 billion to rare earth infrastructure development. Energy Fuels and Ionic Rare Earths have established partnerships with national programs including POSCO, Chemours, and United Kingdom and Brazilian government funding initiatives.

These policy responses represent coordinated efforts to establish processing capacity outside Chinese control, with governments providing both financial support and regulatory frameworks to accelerate private sector investment.

Pricing Floors & Supply Security Premiums

The Department of Defense pricing floor of $110 per kilogram for neodymium praseodymium led to significant production scaling at MP Materials, which increased neodymium praseodymium output by 120%. This pricing mechanism demonstrates how government intervention can provide investment certainty for rare earth producers operating outside China.

Investors now actively value off-take visibility, policy co-alignment, and price insulation when evaluating rare earth investments. Companies with government partnerships and long-term supply agreements command premium valuations compared to those dependent on volatile spot markets.

Energy Fuels Chief Executive Officer Mark Chalmers emphasizes the importance of government recognition:

"Energy Fuels has positioned itself really well. We've designed the project to produce a mixed rare earth carbonate, which is a midstream product. This material doesn't have to go to China—it can be sent somewhere else to be turned into an oxide and ultimately a metal getting recognition from the United States government or the Australian government and European Union for support"

Midstream Processing & Recycling Define the Next Bottleneck

While mining projects capture investor attention, the critical constraint in rare earth supply chains lies in processing and separation capabilities. China controls over 90% of global rare earth separation capacity, creating a strategic chokepoint that Western supply chains must address to achieve meaningful independence from Chinese imports.

Separation Capacity Remains the Hardest Constraint

Mining rare earth elements, while capital-intensive and subject to long development cycles, represents only the first step in creating usable materials for technology applications. The true bottleneck exists in processing and separation facilities that convert raw rare earth concentrates into purified oxides suitable for magnet manufacturing and other high-technology applications.

Western supply chains must solve the midstream bottleneck to unlock neodymium praseodymium and heavy rare earth elements for domestic consumption. This requirement has shifted investor focus from pure-play mining companies toward integrated operators with processing capabilities or established partnerships with separation facilities.

Strategic Company Integration in the Value Chain

Energy Fuels operates the only commercial rare earth oxide production facility in the United States at its White Mesa Mill, currently piloting dysprosium and terbium separations. The company has commercially produced neodymium praseodymium and is recovering dysprosium and terbium in heavy rare earth concentrates.

Ionic Rare Earths has commercialized 99.9%+ neodymium praseodymium, dysprosium, and terbium separation from recycled magnets, completing physical demonstrations in Brazil. The company's recycling technology provides immediate access to separated rare earth oxides without requiring new mining operations.

Ucore is deploying RapidSX™ technology at its Louisiana Strategic Metals Complex, featuring low capital expenditure and modular design backed by Department of Defense funding.

Heavy Rare Earths Emerge as the Market's High-Conviction Trade

Heavy rare earth elements have emerged as the highest-conviction investment opportunity within the broader rare earth complex. These materials are essential for permanent magnet applications in electric vehicles, wind turbines, and defense systems, with limited supply alternatives outside Chinese control.

Magnet Metals & Defense-Critical Elements in Focus

Dysprosium and terbium serve essential functions in electric vehicle traction motors, wind turbine generators, F-35 fighter jets, missile guidance systems, and unmanned aerial vehicles. Over 80,000 components in United States defense systems rely on Chinese rare earth elements, creating strategic vulnerabilities that government agencies are actively addressing through supply chain diversification.

The magnetic properties of dysprosium and terbium cannot be easily substituted, making these elements critical inputs for technologies requiring high magnetic strength and temperature stability. Electric vehicle manufacturers and renewable energy companies are increasingly seeking supply agreements for these materials outside Chinese control.

Supply Chain Optionality Gains Premium Value

Namibia Critical Metals is developing the Lofdal project with Japan Organization for Metals and Energy Security backing, targeting a scalable heavy rare earth deposit capable of producing 5% of global dysprosium and terbium demand. The project benefits from Namibia's stable mining jurisdiction and established mineral export infrastructure.

Ionic Rare Earths operates commercial-scale recycling of dysprosium and terbium from permanent magnets using patented processes that recover materials from end-of-life applications. This approach provides immediate supply without requiring new mining development.

Ucore's Louisiana Strategic Metals Complex is designed to deliver commercial separation of heavy rare earth elements using proprietary technology that reduces capital requirements compared to traditional solvent extraction methods.

Ionic Rare Earths Managing Director Tim Harrison highlights the value of recycled heavy rare earth elements:

"We've seen a huge increase in inbound inquiries about the dysprosium and terbium from our commercial recycling facilities"

Resource Readiness, Jurisdiction & Execution Matter More Than Ever

Jurisdictional advantages, permitting clarity, and execution capability have become primary investment criteria as governments prioritize supply chain security over purely economic considerations. Companies operating in stable jurisdictions with established regulatory frameworks command premium valuations compared to those facing permitting uncertainties or political risks.

Namibia ranks No. 26 globally in the Fraser Institute Policy Perception Index (2022), with Namibia Critical Metals holding a 25-year mining license for the Lofdal project. Utah provides Energy Fuels with fully permitted operations and established production capabilities. Louisiana offers Ucore's facility access to Foreign Trade Zone benefits for input and output flexibility.

Uganda, Belfast, and Brazil provide Ionic Rare Earths with a global footprint allowing diverse sourcing, recycling, and refining across allied jurisdictions.

These jurisdictional advantages provide certainty for long-term capital deployment and reduce regulatory risks that have historically challenged rare earth development projects.

Project Delivery Visibility

Energy Fuels produced neodymium praseodymium in 2024 and is currently piloting dysprosium and terbium recovery from heavy rare earth concentrates. Ionic Rare Earths delivered physical recycled products in Brazil in May 2025, demonstrating commercial-scale processing capabilities.

Namibia Critical Metals expects to complete its Preliminary Feasibility Study for Lofdal in October 2025, providing detailed engineering and economic assessments for development planning.

Ucore Chief Executive Officer Pat Ryan emphasizes the company's execution timeline:

"By mid-2026 we're looking to have that stage one of the Louisiana plant commissioned and start to deliver product to the western world"

The Investment Thesis for Rare Earths

The investment case for rare earth elements reflects fundamental shifts in global supply chain architecture driven by geopolitical considerations and technological demand growth. Multiple factors support premium valuations for Western-aligned rare earth producers:

- Accelerating bifurcation creates premium value as China's export curbs make pricing origin-dependent, driving institutional capital toward Western producers with established government relationships and secure offtake agreements

- Midstream chokepoint represents the critical bottleneck where separation and refining capacity matter more than mining volume, favoring integrated operators and recycling technologies over pure-play mining investments

- Original equipment manufacturer and government demand pull drives active seeking of secure offtake arrangements, with capital flowing to early movers demonstrating commercial-scale processing capabilities and established customer relationships

- Recycling provides strategic leverage through Ionic's magnet recycling and Ucore's low-capital expenditure RapidSX™ model, reducing time-to-market compared to traditional mining development timelines

- Heavy rare earth elements command scarcity premiums as companies capable of supplying dysprosium and terbium outside China benefit from limited alternative supply sources and increasing defense and technology demand

- Jurisdiction, permitting, and policy support create sustainable competitive advantages for companies like Energy Fuels, Ucore and Namibia Critical Metals executing in stable jurisdictions with visible policy alignment and government backing

From Concentration to Compensation: What the Market Is Pricing In

China's policy lever has demonstrated clear effectiveness, by restricting export flows, Beijing forces foreign buyers to pay premiums for supply chain diversification while maintaining domestic manufacturing advantages. The rare earth market no longer operates as a unified global commodity market but rather as segmented regional markets with distinct pricing mechanisms and supply relationships.

Origin, separation capability, and off-take optionality now define rare earth investment valuations more than traditional mining metrics. For institutional investors, exposure to downstream-ready and government-backed producers represents structural positioning rather than speculative investment as Western governments commit resources to supply chain independence.

As neodymium praseodymium and heavy rare earth element demand accelerates toward 2030 and beyond, the price bifurcation established in 2025 may mark the beginning of a broader re-rating cycle for Western-aligned rare earth assets positioned to serve non-Chinese markets.

Analyst's Notes

Subscribe to Our Channel

Stay Informed