China's Output Cuts Tighten Rutile Supply & Adds Pressure to TiO₂ Prices

China cuts TiO₂ output 1.06% amid weak demand, tightening rutile supply. Sovereign Metals' Kasiya project offers critical Western supply chain alternative.

- Chinese TiO₂ production fell 1.06% month-over-month in July, driven by deliberate output cuts amidst weak global demand and margin pressure.

- Spot rutile prices remain flat despite lower supply, highlighting downstream demand fragility and signaling limited short-term pricing power.

- The rutile supply chain remains opaque post-benchmark discontinuation, with Chinese basket pricing adding hedging and procurement complexity.

- Strategic players like Sovereign Metals are advancing world-scale projects outside China, offering critical mineral supply optionality to the West.

- Investors should watch definitive feasibility study timing, Rio Tinto's decision on project operatorship, and potential policy shifts under US-EU critical minerals alignment.

Contraction & Feedstock Fragility

China's Output Cuts Reflect Downstream Weakness, Not Price Power

Chinese titanium dioxide production declined 1.06% month-over-month in July 2025, marking the fourth consecutive month of output reductions as producers confront narrowing margins and tepid end-use demand across coatings, plastics, and construction sectors. Regional plant outages in Shandong and Liaoning provinces contributed to the contraction, while several mid-tier producers implemented deliberate production cuts to preserve cash flow amid deteriorating export conditions.

According to Shanghai Metals Market (SMM) and SunSirs price data, rutile-type titanium prices stabilized around ¥11,800 per tonne with minimal upward traction despite reduced production volumes. This pricing stagnation underscores the fragility of downstream demand rather than supply-driven price discovery, as global construction indicators remain subdued and commodity-linked inflation continues to weigh on industrial purchasing decisions.

The disconnect between reduced Chinese output and flat rutile pricing reflects broader macroeconomic headwinds affecting the titanium feedstock market. European construction activity contracted 2.3% year-over-year in Q2 2025, while US housing starts declined 8.1% from peak levels, directly impacting paint and coatings demand that represents approximately 60% of global TiO₂ consumption. Automotive production slowdowns in key markets have further compressed demand for high-performance titanium-based pigments.

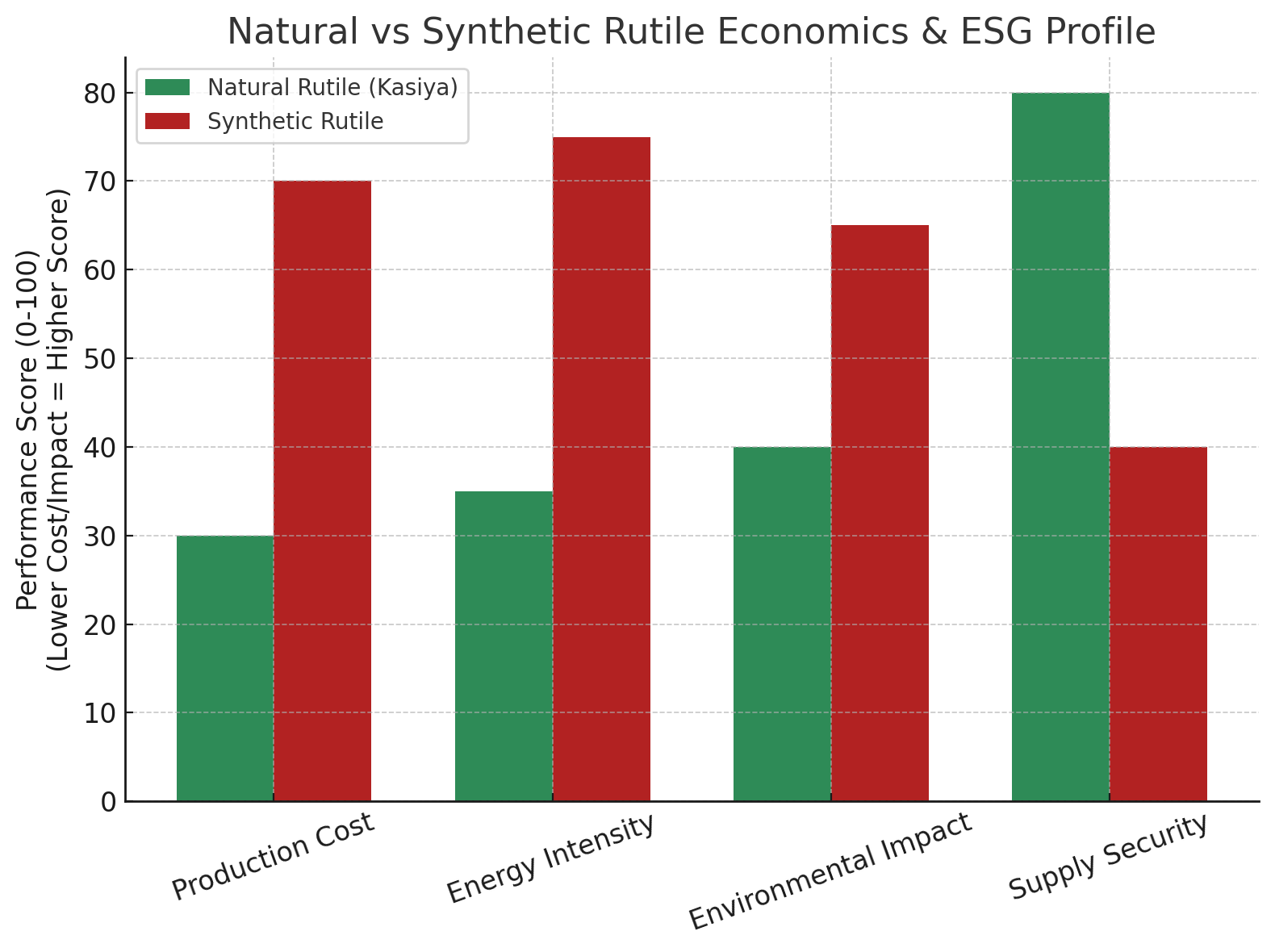

Current market dynamics indicate that producers are cutting output to defend margins rather than capitalize on pricing power, suggesting that any near-term supply tightness will likely be offset by continued demand weakness. This environment creates particular challenges for higher-cost synthetic rutile producers while potentially benefiting low-cost natural rutile developers positioned for the next market cycle.

Volatile Pricing & Lack of Benchmarking Amplify Investor Risk

The discontinuation of established rutile pricing benchmarks has introduced systematic opacity to the titanium feedstock market, forcing industry participants to adopt "basket pricing" models based on weighted averages of ilmenite, synthetic rutile, and TiO₂ slag prices. This shift has created substantial procurement risk for large pigment buyers and introduced hedging complexity that institutional investors are struggling to navigate effectively.

Market intelligence indicates severely limited liquidity in rutile futures markets compared to more established ilmenite and TiO₂ derivatives, constraining risk management options for both producers and consumers. The absence of transparent price discovery mechanisms has led to increased volatility in spot markets, with bid-offer spreads widening to 8-12% compared to historical norms of 3-5%.

Major pigment producers have responded by securing longer-term supply agreements with premium pricing structures, effectively transferring price risk to downstream customers while creating barriers to entry for new market participants. This structural shift favors established producers with diversified customer bases and robust balance sheets capable of absorbing short-term pricing volatility.

Structural Imbalances in the Titanium Feedstock Market

Global Rutile Deficit & Concentrated Supply Chains

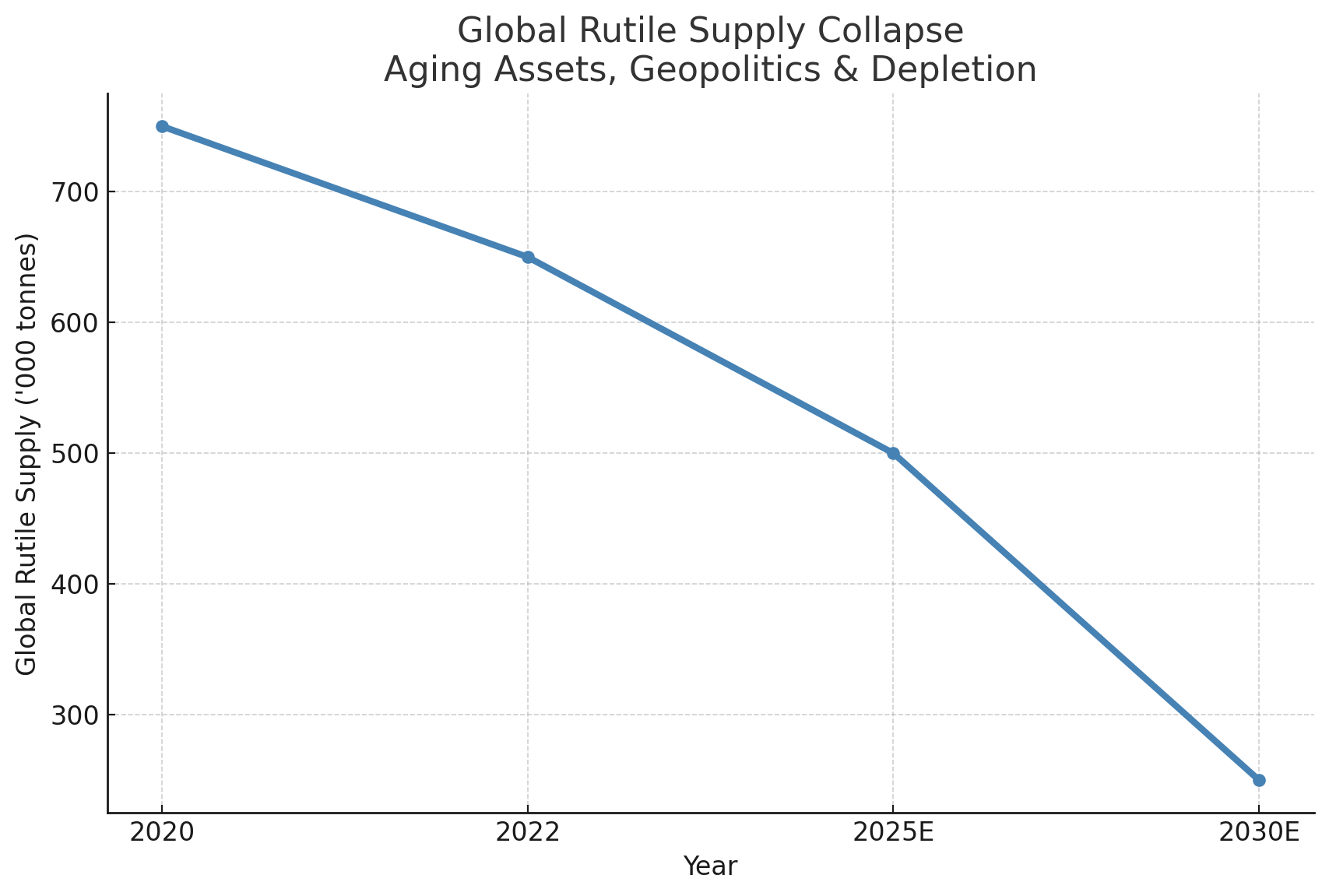

Natural rutile supply has contracted dramatically from 750,000 tonnes to approximately 500,000 tonnes over the past five years, according to United States Geological Survey (USGS) and TZMI market data. This 30% decline reflects the depletion of aging assets in Sierra Leone, production disruptions in Ukraine following the 2022 conflict, and the gradual exhaustion of high-grade deposits in Western Australia.

The supply concentration has intensified China's strategic positioning in the titanium value chain, with domestic producers increasingly adopting chloride-route TiO₂ production that requires high-purity rutile feedstock. Chinese industrial policy has encouraged strategic stockpiling of critical feedstocks, creating additional demand pressure on an already constrained market while reducing export availability for international consumers.

Geopolitical volatility has further complicated supply chain dynamics, with sanctions affecting Russian ilmenite exports and infrastructure challenges limiting African rutile production. Sierra Rutile's operations in Sierra Leone have faced recurring flooding issues, while Kenmare Resources' Moma operation in Mozambique has experienced periodic security disruptions that have constrained consistent rutile output.

The structural deficit has created particular stress for Western aerospace and defense manufacturers that require high-purity rutile for specialized applications including jet engine components and hypersonic vehicle structures. These end-uses cannot readily substitute alternative titanium feedstocks, creating inelastic demand that amplifies price volatility during supply disruptions.

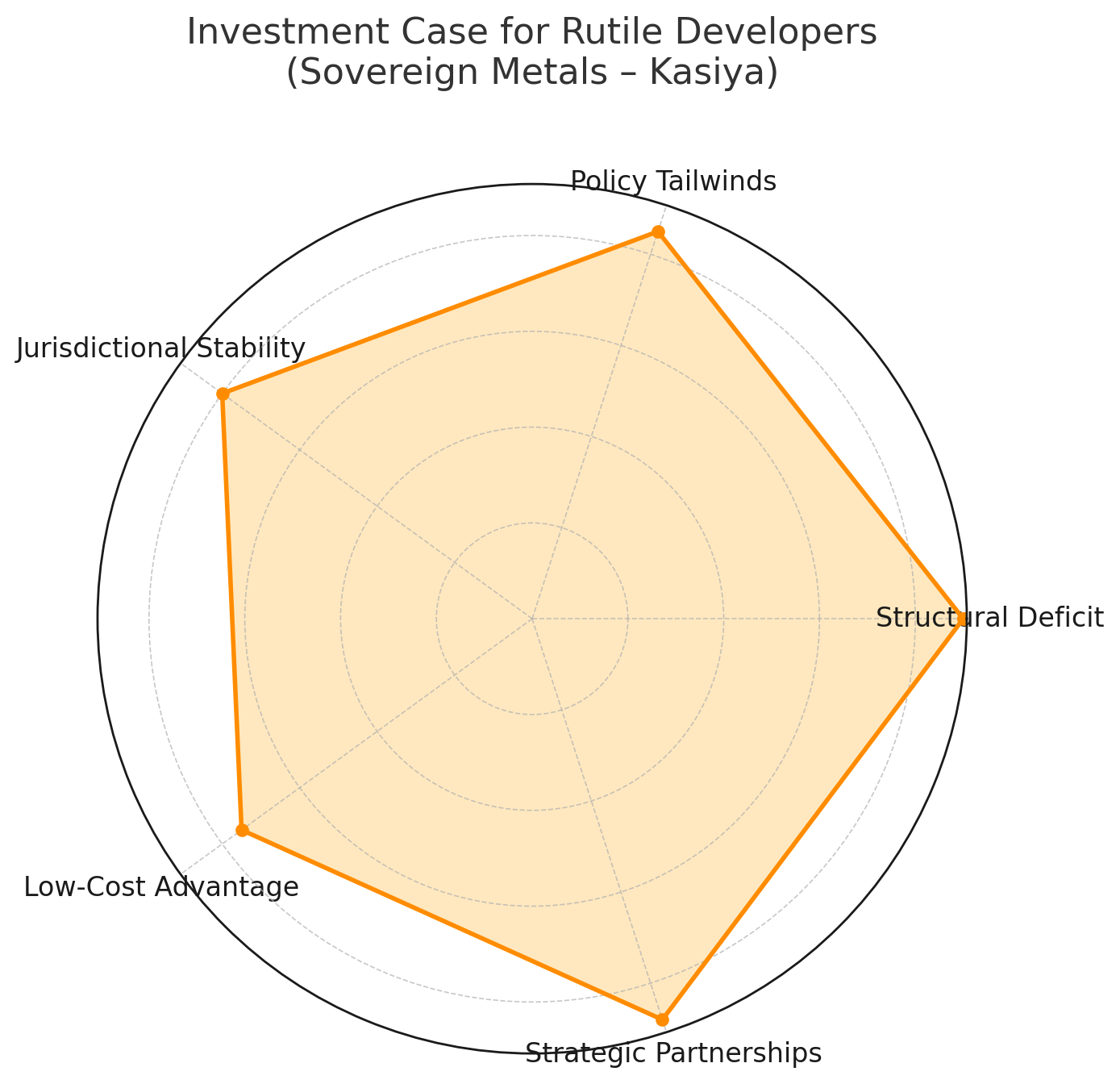

Sovereign Metals & the Push for Non-Chinese Supply Chains

Sovereign Metals represents a pivotal case study within this structural supply backdrop, developing the Kasiya project in Malawi that hosts 17.9 million tonnes of contained rutile resources, the largest globally identified deposit. The project's projected annual output of 220,000 tonnes would significantly increase global rutile supply, which has contracted to approximately 500,000 tonnes and is projected to decline further to 250,000 tonnes within five years, thereby providing critical supply optionality outside Chinese-controlled value chains.

Kasiya's co-product economics with flake graphite create a unique value proposition that enables ultra-low incremental costs for rutile production while providing commodity diversification that shields margins during market downturns. The integrated processing approach allows the company to optimize production schedules based on relative commodity pricing, enhancing project resilience across market cycles.

The deposit's geological characteristics favor both rutile and graphite recovery through a simplified beneficiation process that avoids the complex chemical treatment required for synthetic rutile production. This operational advantage translates to lower capital intensity and reduced environmental impact compared to conventional titanium feedstock operations.

Strategic positioning within Malawi's stable regulatory environment provides additional competitive advantages, particularly as Western governments prioritize supply chain diversification away from geopolitically sensitive jurisdictions. The country's membership in multiple international trade frameworks and established mining code offer institutional clarity that reduces risk premiums for project financing.

Policy Intervention & Critical Mineral Security

Western Realignment & Titanium's Strategic Role

Western governments have accelerated efforts to reduce strategic dependence on China and Russia for critical minerals following the Ukraine conflict, with rutile achieving formal designation under both the EU Critical Raw Materials Act and US Inflation Reduction Act frameworks. These legislative initiatives provide preferential financing, tax incentives, and procurement guarantees for projects that enhance supply chain resilience.

The Mineral Security Partnership (MSP), comprising 14 countries including the United States, United Kingdom, Japan, South Korea, Germany, and France, has identified titanium feedstocks as a priority commodity for strategic stockpiling and supply diversification initiatives. Malawi's alignment with MSP objectives offers Sovereign Metals preferential access to development finance institutions, export-import banks, and export credit agencies backed by member governments.

Rutile's critical role in aerospace, defense, and green technology applications has elevated its strategic importance beyond traditional industrial uses. Advanced aerospace applications require ultra-high purity rutile for titanium alloy production, while emerging technologies including hydrogen storage systems and next-generation solar panels depend on specialized titanium compounds. Defense applications, particularly in hypersonic vehicle development, create inelastic demand that supports premium pricing for qualified suppliers.

The strategic designation has catalyzed institutional investor interest in rutile projects, with wealth funds and pension systems allocating capital to critical mineral exposure as part of broader ESG and national security investment mandates. This institutional demand creates access to patient capital that can support longer development timelines and higher initial capital requirements.

Chief Commercial Officer Sapan Ghai of Sovereign Metals emphasized the geopolitical significance:

"Policy makers have woken up to the fact that actually you can't simply be dependent on the likes of China or Russia to produce critical minerals or produce end products from critical minerals that are required for anything from defense aerospace medical applications."

Export Controls & Resource Nationalism

China has progressively tightened export licensing for high-purity titanium products, creating supply uncertainty for downstream original equipment manufacturers in aerospace and defense sectors. These export controls extend beyond raw materials to encompass processed titanium alloys and specialized compounds, forcing Western manufacturers to seek alternative supply arrangements.

Sovereign resource nationalism trends across Africa and Asia have introduced additional complexity to titanium feedstock supply chains, with governments implementing policies to retain value-added processing domestically. Indonesia's raw ore export bans provide a template that other resource-rich nations may adopt, potentially constraining future rutile export availability from traditional producing regions.

Sovereign Metals' positioning within Malawi's relatively stable and investor-friendly regulatory regime contrasts favorably with higher-risk African jurisdictions experiencing increased resource nationalism pressures. The company's commitment to local beneficiation through its integrated processing approach aligns with government objectives while maintaining export flexibility for international markets.

The regulatory clarity in Malawi extends to fiscal frameworks, with established mining taxation structures that provide predictable returns for international investors. This transparency reduces political risk premiums compared to jurisdictions with evolving or uncertain mining codes, supporting more favorable project financing terms.

Development Pipelines & Market Readiness

Project Economics & Capital Positioning in a Supply-Constrained Market

Kasiya's definitive feasibility study, due in Q4 2025, underpins a pre-tax net present value of US$2.32 billion and internal rate of return of 27%, positioning the project among the most attractive undeveloped rutile assets globally. The economic metrics reflect conservative commodity pricing assumptions that provide downside protection while maintaining substantial upside exposure to market tightening scenarios.

Rio Tinto's 19.9% equity stake, acquired through staged investments totaling A$60 million, signals technical confidence in Kasiya's development potential while providing access to world-class mining expertise and global marketing capabilities. The major's option to assume project operatorship post-feasibility study completion represents potential merger and acquisition upside for existing shareholders.

The project's average earnings before interest, taxes, depreciation, and amortization of US$409 million and 64% margin structure provide resilience even under conservative rutile pricing scenarios, with breakeven analysis indicating profitability at rutile prices 40% below current market levels. This margin buffer reflects the operational advantages of natural rutile recovery compared to energy-intensive synthetic production processes.

Capital requirements of US$665 million for initial development align with Rio Tinto's typical project investment thresholds, supporting the potential for accelerated development timelines through major partnership structures. The relatively modest capital intensity compared to other large-scale mining projects reduces financing complexity while maintaining attractive returns on invested capital.

As Chief Commercial Officer Sapan Ghai noted regarding market confidence:

"I have no qualms that we could sell our product into the market and there would be potential off-takers who would happily fund this project into production."

Jurisdictional Risk & Infrastructure Resilience

Kasiya's strategic location provides direct rail access to the Port of Nacala, ensuring export scalability without the infrastructure bottlenecks that constrain other African mining operations. The established rail corridor handles substantial bulk commodity volumes, with available capacity to accommodate Kasiya's projected throughput without requiring significant additional investment.

Comparative analysis with peers operating in higher-risk zones demonstrates Kasiya's infrastructure advantages. Kenmare Resources' Moma operation in Mozambique has experienced periodic security disruptions affecting production continuity, while Iluka Resources' Sierra Leone operations face recurring flooding issues that compromise consistent output delivery.

Malawi's political stability and established mining regulatory framework provide operational predictability that supports long-term planning and investment commitment. The country's democratic institutions and rule of law offer institutional clarity that reduces risk premiums compared to jurisdictions with less established governance structures.

The fiscal transparency and permitting predictability in Malawi contrast favorably with other African mining jurisdictions experiencing frequent regulatory changes or uncertain tax environments. This stability supports more favorable project financing terms while reducing the political risk premiums that can compromise project economics.

The Investment Thesis for Rutile & TiO₂ Feedstocks

- Global rutile output has contracted 30% over the past five years, making new production like Kasiya essential to rebalance supply and meet growing strategic demand from Western aerospace and defense sectors.

- The lack of established benchmarks and inconsistent pricing methodologies increase volatility but favor producers with scale and low-cost operations capable of maintaining margins through market cycles.

- Strategic mineral designation under EU and US frameworks creates long-term demand tailwinds and de-risked capital access for aligned producers serving critical end-use applications.

- Kasiya's co-product model enables commodity cycle resilience by offsetting cost exposure across TiO₂ and battery materials markets while optimizing production schedules based on relative pricing dynamics.

- Rio Tinto's involvement increases institutional confidence while opening pathways for long-term offtake agreements and streamlined project financing through established industry relationships.

- Malawi's permitting stability and established rail access provide logistical certainty compared to politically riskier peers, supporting consistent production and export capabilities.

- Natural rutile's lower production costs compared to synthetic alternatives provide margin protection during downturns while maintaining exposure to supply-driven price recovery scenarios.

- Critical mineral exposure supports portfolio diversification objectives while addressing supply chain security concerns that align with broader ESG investment frameworks.

Macro Pressure Meets Strategic Scarcity

The rutile market faces a rare convergence of supply discipline, geopolitical bifurcation, and structural demand evolution that creates compelling investment dynamics despite near-term macroeconomic headwinds. Chinese output cuts reflect margin pressure rather than pricing power, but the underlying supply deficit continues to intensify as aging assets deplete and geopolitical tensions constrain traditional supply chains.

Western policy alignment against concentrated Chinese supply chains has elevated rutile from an industrial commodity to a strategic material, creating demand tailwinds supported by institutional capital allocation and government financing initiatives. This policy framework provides downside protection while enhancing upside exposure to supply-driven price discovery as market fundamentals tighten.

Well-capitalized, low-cost developers like Sovereign Metals, particularly those supported by Tier-1 mining partners are optimally positioned to capitalize on this structural shift. The combination of world-scale resources, favorable jurisdiction, and strategic partnership provides multiple pathways to value creation while maintaining defensive characteristics during market volatility.

Investor watch points over the next 6-12 months include Kasiya's definitive feasibility study completion in Q4 2025, Rio Tinto's operatorship decision, and potential evolution in Chinese export policy that could accelerate Western supply diversification initiatives. These catalysts will likely drive institutional recognition of rutile's strategic value while highlighting the scarcity of development-ready projects outside Chinese influence.

Analyst's Notes

Subscribe to Our Channel

Stay Informed