Strategic Investment Fuels Cascadia’s Push to Build 1.5B Pound Copper Resource

Cascadia advances Yukon copper-gold deposit (651M lbs Cu) with 15K meter drill program backed by Agnico Eagle. Road access, near power, targeting resource doubling to 1.5B lbs

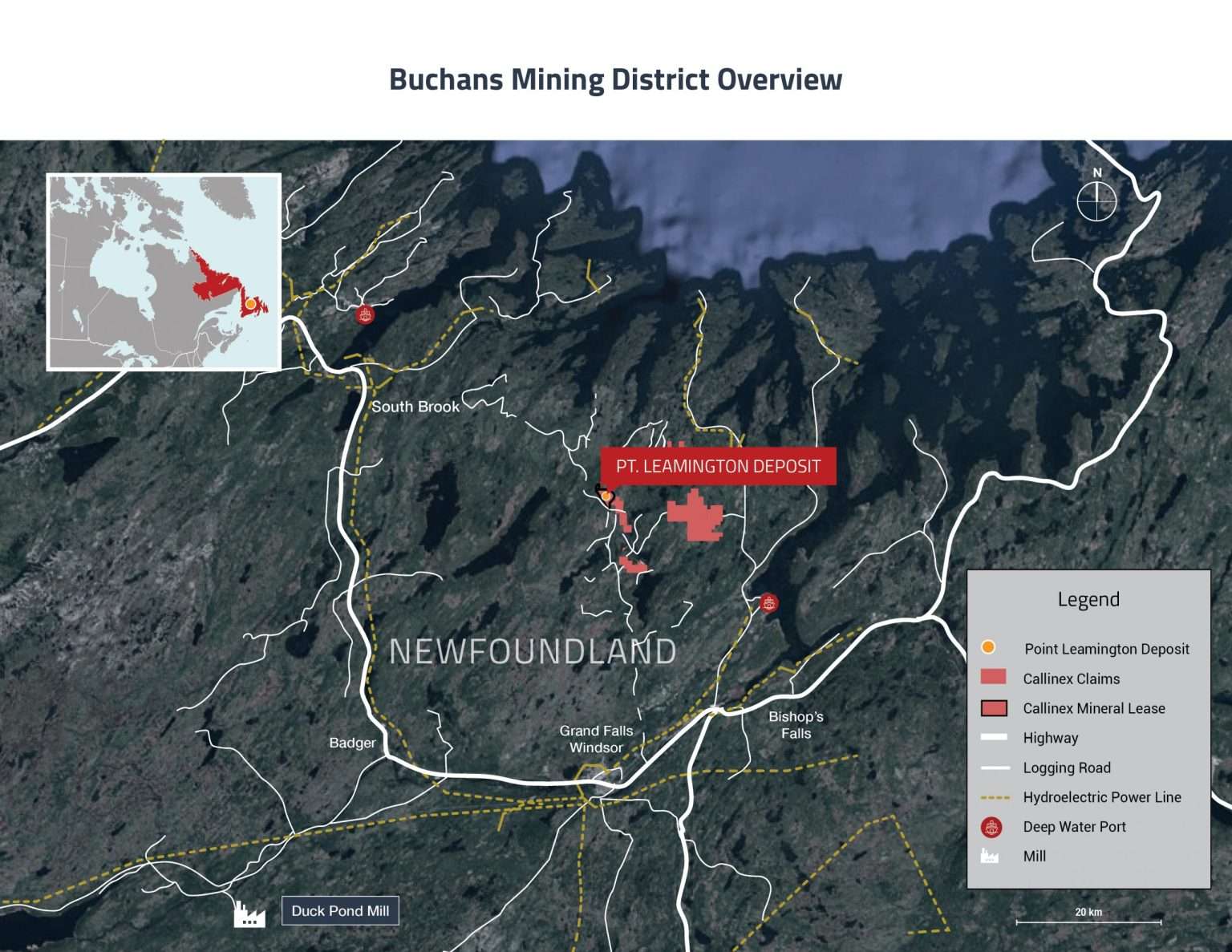

- Cascadia Minerals merged with Granite Creek Copper to acquire the Carmacks copper-gold deposit in central Yukon, a road-accessible asset 10km from grid power with 651 million pounds of copper and 300,000 ounces of gold at over 1% copper equivalent

- Company launched 15-20,000 meter drill program in April 2026 - nearly half again of the 44,000 meters of historic drilling - aiming to double the resource to 1.5 billion pounds of copper with drilling costs reduced to $400/meter compared to $500,000+ per hole at previous helicopter-accessed projects

- Agnico Eagle completed a strategic investment taking 14% ownership (19.9% fully diluted), providing funding through 2027 while also holding an option to earn 80% of Cascadia's Stikine terrain exploration projects through $12 million in expenditures

- Management could bypass Preliminary Economic Assessment and proceed directly to Pre-Feasibility Study in coming years, leveraging the mostly measured-and-indicated resource and previous baseline work to accelerate the development timeline

- Zone A, located 11km north of the main deposit, shows exceptional grades including 22 meters of 2% copper plus 2 grams/ton gold, significantly higher than the main deposit's 0.26 g/t gold average, with 3-4,000 meters of drilling planned for this target

As major mining companies increasingly seek copper assets in stable jurisdictions, Cascadia Minerals has positioned itself with a road-accessible copper-gold deposit in central Yukon. The company recently secured strategic investment from Agnico Eagle and commenced an aggressive drill program aimed at doubling its existing resource base while fast-tracking development through Pre-Feasibility Study.

The Carmacks Acquisition Rationale

Cascadia merged with Granite Creek Copper specifically to acquire the Carmacks copper-gold deposit. The asset's appeal centered on several factors: road accessibility, proximity to grid power (10 kilometers), and an existing resource that comes to surface. The deposit contains 651 million pounds of copper and 300,000 ounces of gold at over 1% copper equivalent.

The deposit characteristics distinguish it from typical porphyry systems. Rather than broadly disseminated mineralisation, Carmacks features what President & CEO Graham Downs describes as magmatised porphyry that was "melted up, upgraded, and then squeezed up a structure - so it acts more like a VMS." This results in zones averaging 50 meters wide at close to 1.5% copper - higher grades than many North American porphyries in comparable jurisdictions.

Resource Characteristics and Geology

The Carmacks deposit comprises three separate zones with clean contacts between mineralisation and barren granite wall rock, typically within one meter. This geological characteristic should facilitate mining operations. The deposit extends from surface to depth, with oxide mineralisation reaching approximately 150 meters before transitioning to sulfide.

Previous operators focused exclusively on near-surface oxide material suitable for heap leaching, often terminating holes upon encountering sulfide mineralisation. Granite Creek recognised the sulfide potential and began targeting it, though capital constraints limited their ability to fully demonstrate the deposit's extent. Cascadia's due diligence confirmed growth potential both at depth and along strike.

Zone A, located 11 kilometers north of the main deposit, presents particularly compelling grades. Historic drilling from the 1980s returned intercepts including 22 meters of 2% copper plus 2 grams per ton gold, 25 meters of over 2% copper, and 13 meters of 3% copper. Gold mineralisation at Zone A significantly exceeds the main deposit's 0.26 gram per ton average, providing additional value upside.

2026 Exploration Program

Cascadia's current drill program targets 15-20,000 meters - nearly half again of the 44,000 meters of historic drilling that defined the resource. The program allocates approximately 10,000 meters to the main deposit through systematic 50-meter step-outs both down-dip and along strike. Another 5,000 meters will test parallel zones near the deposit, while 3-4,000 meters will evaluate Zone A.

The company introduced an oriented core to the project for the first time to better understand structural controls on mineralisation. With two drills currently operating and potential to add capacity, the program can continue through October or November depending on weather conditions.

Management emphasises systematic exploration over aggressive multi-rig programs. The approach prioritises trenching and geophysical surveys to refine targets before drilling, rather than immediately testing induced polarisation anomalies. Additional drill capacity would only be warranted by discovery of significant new zones requiring simultaneous programs.

Interview with Graham Downs, President & CEO, Cascadia Minerals

Development Strategy and Timeline

Cascadia could look to bypass the Preliminary Economic Assessment stage and proceed directly to Pre-Feasibility Study in the coming years. This potential option reflects several advantages: the resource consists primarily of measured and indicated categories, minimising infill drilling requirements; previous operators completed baseline environmental work that can be restarted; and the relatively compact, high-grade nature of the deposit reduces study complexity.

"We want to make this much bigger, double it if we can and go potentially right into pre-feasibility in a couple of years."

The strategy aims to reach 1.5 billion pounds of copper and approach one million ounces of gold before advancing to PFS. Wall rock characterisation remains straightforward given the barren granite contacts. While PFS costs were not disclosed, management expressed confidence that previous work and the deposit's characteristics would keep expenses manageable compared to projects requiring extensive infill drilling or complex metallurgical studies.

The deposit's surficial expression suggests combined open-pit and underground mining scenarios, though mine planning awaits further resource expansion and engineering studies.

Agnico Eagle Strategic Partnership

Agnico Eagle's investment provides near-term financial flexibility while establishing a longer-term exploration partnership. The major acquired 14% ownership (19.9% fully diluted) through a recent financing that funded the 2026-2027 drill programs at Carmacks.

Beyond the equity position, Agnico holds an option to earn up to 80% of Cascadia's Stikine terrain exploration projects through $12 million in expenditures. This area-of-interest agreement targets early-stage grassroots exploration across a large, underexplored portion of the Stikine terrain extending from British Columbia into Yukon. After earning 80%, the agreement would continue as an 80-20 joint venture with Cascadia carried through its 20% interest during the earn-in phase.

The partnership reflects Agnico's established Yukon presence and long-term exploration strategy in the territory. For Cascadia, it provides funding for generative exploration while allowing management to focus operational resources on advancing Carmacks.

Market Position and Jurisdictional Considerations

Cascadia operates within the broader Minto copper belt, with the Minto Silver Copper mine (Selkirk Copper) to the north working toward production restart. The company characterises the relationship as controlling much of the belt between the two operations. Regional infrastructure development, including the proximity to grid power and road access, distinguishes Yukon copper projects from many peers.

The jurisdiction has attracted increased major mining company interest, including B2 Gold and others. Management views the territory as increasingly recognised for infrastructure and permitting frameworks.

Cascadia works with multiple First Nations groups across its property portfolio, which spans 180 kilometers. Approaches vary by area depending on settlement status and community priorities. The company employs First Nations workers and contracts with development corporations for reclamation work at Carmacks. Management emphasises ongoing communication and adapting to evolving concerns as leadership changes occur within Indigenous governments.

Capital Structure and Market Awareness

Michael Gentile holds approximately 7.1% of Cascadia, having participated in financings since the Cascadia spin-out from ATAC Resources when it was purchased by Hecla Mining in 2023. His continued support through multiple funding rounds, including the Granite Creek acquisition financing, provides shareholder stability.

Management identifies market awareness as a near-term priority. Despite the infrastructure advantages and resource quality, many investors remain unfamiliar with the Carmacks project. The company's attendance at conferences aims to highlight the road-accessible nature and power proximity, characteristics that differentiate it from Yukon's historical reputation for remote, infrastructure-poor projects.

"A lot of people we're here at a conference and they're like - ‘I didn't know about Carmacks project’. Yukon has been known as bad for infrastructure. This [Carmacks] is on the road and close to power so we need to get the word out."

With two drill rigs operating and results expected through the field season, the company anticipates that successful drilling will support valuation expansion relative to regional peers with similar or larger resources but less favourable infrastructure positions.

The Investment Thesis for Cascadia Minerals

- Infrastructure Advantage: Road-accessible deposit located 10km from grid power in central Yukon, dramatically reducing operating costs compared to helicopter-accessed projects ($400/meter drilling vs $500,000+ per hole)

- Resource Growth Potential: Current 651 million pound copper resource defined by only 44,000 meters of drilling; 2026 program of 15-20,000 meters (nearly half historic total) targeting resource doubling to 1.5 billion pounds

- Higher-Grade Profile: Deposit averages over 1% copper equivalent with 50-meter-wide zones at ~1.5% copper - rare grade profile for North American porphyries in accessible jurisdictions

- Strategic Major Backing: Agnico Eagle 14% strategic investment (19.9% fully diluted) provides financial stability through 2026 and validates asset quality; partnership includes earn-in opportunity on exploration portfolio

- Valuation Disconnect: Management believes market cap undervalues company relative to regional peers, particularly given infrastructure advantages and established resource base

- Political Jurisdiction Support: Settled First Nations relationships, established permitting frameworks, and proximity to North American markets position asset favorably as majors increasingly prioritise friendly jurisdictions

Macro Thematic Analysis

Major mining companies are increasingly prioritising copper assets in stable, infrastructure-rich jurisdictions as geopolitical risks and capital intensity challenges mount in traditional mining regions. Cascadia's Carmacks deposit represents the type of asset - road-accessible, near power, in a Canadian jurisdiction with established permitting frameworks - that addresses the industry's dual mandate of copper exposure and jurisdictional risk mitigation.

Agnico Eagle's strategic investment validates this positioning, as majors seek to rebuild North American project pipelines following decades of underinvestment in domestic exploration. The electrification megatrend and copper supply constraints create urgency for discovering and advancing deposits that can reach production within reasonable timeframes and capital budgets. Road access and power proximity reduce both capital and operating costs while shortening permitting timelines compared to remote greenfield projects. As Graham noted:

"I think seeing the majors getting involved in more things is a nice thing...I think that's a signal maybe that more money is going to come into I would say in my opinion friendlier jurisdictions just the way the world is these days."

The convergence of copper fundamentals, infrastructure advantages, and jurisdictional preference positions well-located Canadian assets for sustained institutional interest.

TL;DR

Cascadia Minerals is advancing the road-accessible Carmacks copper-gold deposit (651M lbs Cu, 300K oz Au) in central Yukon with a 15-20,000 meter drill program backed by strategic partner Agnico Eagle (14% ownership). The company plans to bypass PEA and advance directly to Pre-Feasibility Study in coming years while targeting resource doubling to 1.5 billion pounds copper through systematic exploration of the main deposit and high-grade Zone A target (22m @ 2% Cu + 2 g/t Au). Infrastructure advantages - 10km from grid power, road-accessible, $400/meter drilling costs - distinguish the asset in a jurisdiction gaining favor with major mining companies seeking North American copper exposure.

FAQs (AI Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed