Copper Price Surpassing $10,000 Signals Supply Crisis & Mine Timeline Lead Time Lengthens

Copper faces critical supply shortage with inventories at 6-day coverage vs 12-day average. Multiple development projects advancing amid structural demand growth.

- Copper markets are experiencing unprecedented supply-demand dynamics, with exchange inventories plunging 44% since late February and visible copper inventories covering only six days of global copper demand, versus a long-term average of 12 days

- Spot treatment charges for copper concentrate have dropped to record lows, even turning negative, indicating severe scarcity of mined copper and strengthening the investment case for copper miners

- Multiple copper development projects are advancing while junior copper companies are discovering significant new zones highlighting the benefits of operating in tier-one jurisdictions with established regulatory frameworks and mining-supportive communities.

- Infrastructure development and systematic exploration programs are identifying untested targets revealing multiple large-scale, untested copper skarn targets to aid the demand as lead times continues to extend to open more copper mines.

The copper market is facing acute physical tightness that has reached levels not seen since the COVID-19 supply disruptions. Global exchange copper inventories have plunged 44% since late February, signaling a sharp tightening in supply, according to recent market analysis. This dramatic inventory drawdown has created a precarious situation where total visible copper inventories have precipitously declined to cover only six days of global copper demand, versus a long-term average of 12 days.

Source: Sprott's Copper’s Bullish Setup Strengthens. Bloomberg, Includes inventories on the LME, SHFE and COMEX.

Spot treatment charges for copper concentrate have dropped to record lows, even turning negative, meaning smelters are now paying miners to secure raw material rather than charging processing fees. This reversal, which was almost unheard of until the past year and a half, signals fundamental scarcity in mined copper production.

With this supply cushion rapidly eroding, any modest shock may instigate price-driven rationing to balance the market. Industry analysts note that when deep backwardation is paired with a surging import premium, it's a classic signal of genuine global tightness, suggesting prices may need to rise significantly to incentivize new supply.

Long Lead Time for Supply Response

The demand side presents equally compelling fundamentals for copper investment. Electrification is the dominant force fueling U.S. copper demand in 2025, while construction and manufacturing remain critical. The growing investments in electrical grids, the rapid buildout of AI data centers, urbanization in emerging economies, and the energy transition all point to sustained copper demand growth.

China is investing heavily in grids, renewable energy, electronics and EVs—all of which require significant copper. This demand profile represents a fundamental shift from cyclical construction and manufacturing demand toward structural, technology-driven consumption that is likely to persist regardless of broader economic conditions.

The supply response to this demand however growth faces significant constraints. Long lead times hamper the supply response, as it takes on average 17 years to move from discovery to first production, over double the 7 years it took in the 1990s. This extended development timeline, combined with project deferrals and capital discipline seen across the mining sector, severely limits the industry's ability to respond to growing demand.

Copper Supply Developments Aiding to Meet Demand

The copper sector presents investment opportunities across various stages of project development: from early-stage exploration, operational turnarounds, and advanced development projects approaching production decisions. Companies successfully defining substantial copper resources are attracting significant institutional attention.

Kodiak Copper announced its maiden mineral resource estimate, revealing 300 million tonnes of mineralization with grades of 0.42% copper equivalent for indicated resources and 0.33% for inferred resources. The company's founder noted that the project contains between 2 and 3 billion pounds of copper equivalent roughly, and that's worth more than $10 billion in the ground in resource.

Chris Taylor points out:

"At this time the pipeline of projects of exploration projects development projects in the copper sector are at an all-time low. There haven't been many discoveries. There haven't been any major discoveries in the last decade, so we know that there will not be a major big mine built in the next 10 years or so, because if it hasn't been discovered in the last 10 years it won't be built in the next 10 years. There's really a dearth of good copper projects out there and obviously lots of copper demand on the horizon from AI technology green revolution etc etc"

He also adds, a compelling geopolitical dimension:

"The geopolitics of the world has changed and now having a copper asset in a safe jurisdiction like Canada has extra value"

Together, these quotes present the key macro themes: supply scarcity, growing demand from megatrends, and the premium value of politically stable jurisdictions.

The resource scale positions projects like this among significant copper deposits in established mining regions. As Kodiak's executives explained, the grades measure up very well compared to other projects and mines in BC, while the location in British Columbia provides jurisdictional advantages increasingly valued by strategic buyers.

Chris Taylor, Chairman & Claudia Tornquist, CEO of Kodiak Copper

Early-stage exploration continues to yield significant discoveries, particularly in established mining districts with proven geological potential. Pan Global Resources has demonstrated this through systematic exploration at its Cármenes Project in northern Spain, where recent drilling intercepted wide gold intervals from near surface, including 56m at 0.37 g/t Au and higher-grade intervals of 4m at 2.19 g/t Au.

Moody observes the quality of ore body matters when it comes to the recoveries and margin, "Because of the higher recovery higher concentrate grades we have lower sulfides and we have lower delletterious metal content at its coarse grain when you put all those things together it means that the net value of that 1% or half% copper at La Romana is worth a lot more than all the other mines"

Pan Global is focused primarily on copper assets while recently adding a significant copper-gold discovery in northern Spain that is reshaping the company's exploration priorities. President and CEO Tim Moody emphasized the discovery potential, noting that the wide zones of breccia mineralization highlight the potential for significant hydrothermal breccia-hosted gold, copper, nickel, and cobalt mineralization. This type of systematic exploration in proven districts offers investors exposure to discovery upside while maintaining relatively lower geological risk.

Tim Moody, CEO of Pan Global Resources

The sector also presents opportunities in operational turnarounds, where management teams identify fundamental mismatches between asset quality and operational strategy. FireFly Metals exemplifies this approach, having acquired the Green Bay copper-gold project through administration proceedings. The company's CEO identified that there was nothing wrong with the ore body. This was a large scale ore body. But what it suffered from was a lack of capital investment and a lack of a coherent strategy.

Cooke is optimistic about the opportunities for junior miners with quality assets stating:

"A lot of the the major copper discoveries and the copper deposits are large scale porphyries, like you get in South America. They require a lot of time and billions of dollars in capital to get them up and running and the time frames can be 20 years from discovery to production. The advantage we've got is we can be in production in a very short time frame, for very limited capital and generate more cash flow because our grades are so high so we can take advantage of the current strong copper market."

Since acquisition, Firefly has demonstrated significant resource expansion capabilities, growing the deposit from 40 million tons to 60 million tons through an aggressive 90,000-meter drilling program. The company's approach addresses infrastructure scaling issues that plagued previous operators, planning an initial 1.8 million ton per annum processing plant constructed on-site rather than the undersized facilities that contributed to previous failures.

Darren Cooke, CEO of Firefly Metals

Modern exploration companies are increasingly leveraging advanced geophysical techniques to identify previously unrecognized mineralization. Gladiator Metals' recent gravity survey at their Whitehorse Copper Project has identified multiple high-density anomalies potentially relating to untested copper-gold skarn mineralization.

The systematic application of geophysical methods in established mining districts is revealing significant exploration potential. As Gladiator noted in a news release, the Whitehorse Copper belt is a target-rich environment that is significantly underexplored, away from areas of outcropping mineralization which were the focus of historical exploration efforts.

Jason Bontempo, CEO of Gladiator Metals

Similarly, Pacific Empire's exploration team has made a critical reinterpretation of known mineralization on the property, determining that copper-gold mineralization wherein insights has led to a focused drilling strategy targeting what the company believes could be a much larger main porphyry body. The company's 2025 exploration program, supported by a multi-year exploration permit, targets a primary area where over 50 years of exploration suggests the most prospective ground lies immediately north of historical drilling. As President and CEO Brad Peters explained, "What excites us the most about Trident is the gold and copper grades encountered by previous operators. We believe the most significant advancement on the property to date is the recognition that mineralization appears to be directly associated with these porphyry dikes."

With historical intersections including 33.4m at 1.18% Cu and individual intervals reaching 2.73% Cu, Pacific Empire represents the type of systematic re-evaluation of proven districts that can generate significant discovery value while operating in the tier-one jurisdiction of British Columbia.

Market Dynamics & Pricing Outlook

Geopolitical factors are increasingly influencing copper investment decisions, with stable mining jurisdictions commanding premium valuations, highlighting projects in British Columbia, Spain, and Canada's Yukon Territory, all representing what industry participants describe as tier-one jurisdictions with established regulatory frameworks and mining-supportive communities.

The institutional investment perspective on copper markets is exemplified by Olive Resource Capital's strategic positioning and recent performance wherein the group reported over $1.1 million net return in Q1 2025. Olive Resource's analysis reveals a critical constraint in copper investing: the investable universe of mid-cap copper companies is extremely narrow, with only 5-8 meaningful names available, each presenting specific drawbacks that lead to stretched valuations due to limited choice for copper exposure. As Pelaez explained:

"When you look at each one of them, you could give yourself excuses not to buy any of them because they all have something."

Despite operational issues at major assets like Ivanhoe's Kamoa-Kakula mine (a top-five global copper asset), copper prices haven't moved significantly, potentially creating entry points for sophisticated investors. The fund maintains exposure through junior developers like Arizona Metals (backed by Rio Tinto and Hudbay) and Sterling Metals demonstrating how institutional capital is increasingly focusing on development-stage opportunities in the constrained copper investment landscape.

Sam Palez & Derek Macpherson of Olive Resource Capital

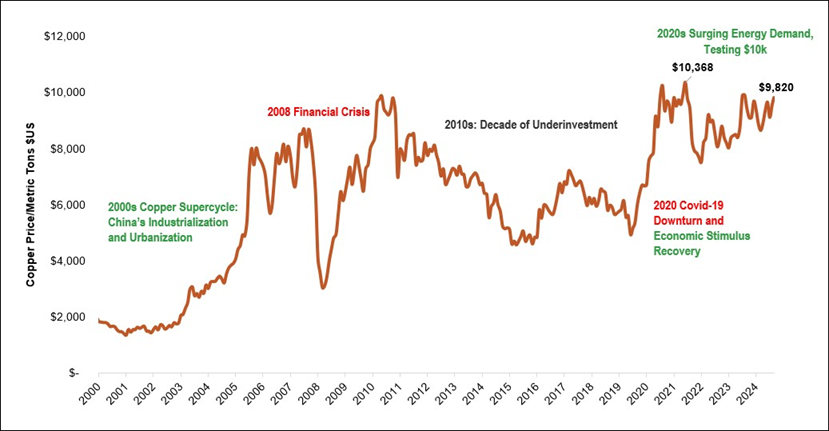

Current market conditions suggest copper prices may need to rise significantly to incentivize new supply development. Copper enters the second half of 2025 with strong momentum and mounting pressure. Prices are within striking distance of the key resistance level of US$10,000 per metric ton threshold.

The combination of inventory depletion, negative treatment charges, and persistent backwardation in forward curves indicates market participants expect continued tightness. In such conditions, prices may need to break above the US$10,000 per metric ton mark to unlock new supply and restore market balance.

The Investment Thesis for Copper

The scale requirements for developing major copper projects typically necessitate involvement from larger mining companies, creating acquisition opportunities for successful exploration companies. This dynamic creates a clear path to value realization for successful exploration companies, as porphyry projects of this scale are typically acquired by majors rather than developed by juniors. The resource quantification process provides concrete data for potential acquirers to evaluate strategic value.

- Supply-Demand Imbalance: Invest in copper exposure through companies positioned to benefit from structural supply constraints, with global inventories at critically low levels and new mine development facing 17-year lead times

- Electrification Megatrend: Target companies with copper assets positioned to serve growing demand from data centers, renewable energy infrastructure, and electric vehicle adoption, representing multi-decade growth drivers

- Resource-Stage Opportunities: Focus on companies successfully defining substantial copper resources in tier-one jurisdictions, particularly those approaching maiden resource estimates or demonstrating resource expansion capabilities

- Operational Turnarounds: Consider companies acquiring distressed copper assets with strong geological fundamentals but operational challenges, offering potential for significant value creation through strategic repositioning

- Discovery Exposure: Maintain exposure to systematic exploration programs in proven copper districts, leveraging modern geophysical techniques to identify previously unrecognized mineralization zones

- Jurisdictional Premium: Prioritize projects in stable mining jurisdictions such as Canada, Australia, and parts of Europe, where regulatory certainty and community acceptance reduce development risk

- Strategic Acquisition Potential: Target exploration companies advancing projects toward resource definition, as successful porphyry copper discoveries typically attract acquisition interest from major mining companies

- Technology Integration: Favor companies utilizing advanced exploration technologies including AI-driven target generation, helicopter geophysics, and gravity surveys to enhance discovery probability while reducing exploration costs

The convergence of supply constraints, structural demand growth, and technological advancement in exploration creates a compelling investment environment for copper-focused companies. Investors should consider portfolio exposure across development stages while prioritizing jurisdictional quality and management execution capability. The current market dynamics suggest significant value creation potential for companies successfully advancing copper projects toward development decisions, particularly as treatment charges remain negative and global inventories approach critically low levels.

Analyst's Notes

Subscribe to Our Channel

Stay Informed