Critical Battery Metals: Strategic Investment Opportunities in the Energy Transition

Battery metals tin, nickel, graphite face supply disruptions, demand shifts from EVs. Investment outlook for 2025-2030 with price forecasts and risks.

- Tin prices have surged 17.7% year-over-year to approximately $34,626-34,993 per tonne by July 2025, driven by significant supply disruptions in Myanmar and the Democratic Republic of Congo that have removed nearly 14% of global production capacity.

- Nickel markets face headwinds as prices have declined to around $15,200-15,300 per tonne, pressured by oversupply from Indonesian expansions and the rapid adoption of lithium-iron-phosphate (LFP) batteries that eliminate nickel content entirely.

- Carbon and graphite product manufacturing shows modest inflation at 1.8% year-over-year with the Producer Price Index reaching 242.15 in June 2025, reflecting stable cost pass-through despite growing demand from electric vehicle battery anodes and energy storage applications.

- Supply chain vulnerabilities remain acute across all three metals, with geopolitical risks in key producing regions including Indonesia, Myanmar, and the Democratic Republic of Congo creating potential for significant price volatility through 2030.

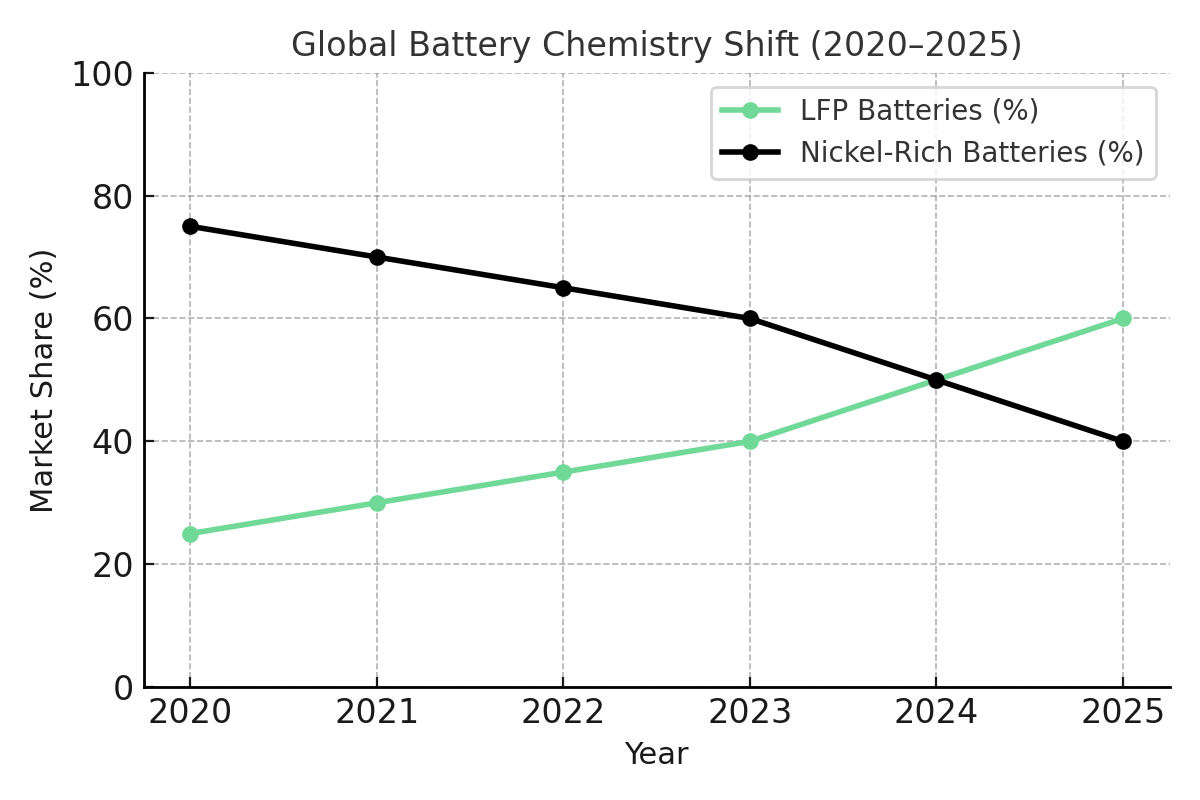

- The structural shift toward LFP battery chemistry is fundamentally reshaping demand patterns, reducing nickel and cobalt intensity by approximately one-third over four years while maintaining strong growth prospects for specialized graphite products in battery anodes.

Market Overview & Current Positioning

The battery metals complex has experienced dramatic shifts in 2024-2025 as the electric vehicle revolution encounters both technological evolution and supply chain disruptions. These three critical materials - tin, nickel, and graphite - serve distinct but interconnected roles in the energy storage ecosystem, each facing unique market dynamics that present both opportunities and challenges for investors.

Tin, historically known for its role in electronics soldering, has emerged as a critical component in renewable energy infrastructure, with approximately 50% of demand still concentrated in solder applications essential for solar ribbon technology and electronic components. The metal's price performance has been remarkable, climbing from around $30,000 per tonne in late 2024 to current levels exceeding $34,600 per tonne, representing one of the strongest performances among industrial metals. Development companies like Rome Resources are advancing high-grade tin projects in the Democratic Republic of Congo, with their Mont Agoma and Kalayi prospects targeting maiden resource estimates by September 2025.

Rome Resources - Resource Definition & Exploration

Rome Resources is currently executing an intensive second-phase resource drilling program with over 5,000 meters completed across 26 holes at their Mont Agoma and Kalayi prospects in the Democratic Republic of Congo. The company operates three drill rigs on site with approximately 40 personnel at peak operations, targeting maiden resource estimates expected by September 2025. Their exploration efforts received significant validation in June 2025 with the discovery of a substantial 40-meter tin zone, positioning the projects as high-potential assets located just 8km from Alphamin's producing Mpama Tin Mine in Eastern DRC.

"The IRH acquisition of Alphamin is showing that the outside world... is now bought into [the DRC]. And I think the US getting involved as well -it's all positive actually for DRC critical minerals." - Paul Barrett, CEO, Rome Resources

Nickel markets tell a different story, with prices retreating from earlier highs as the battery industry undergoes a fundamental chemistry shift. The rapid adoption of LFP batteries, particularly in China and increasingly in stationary storage applications, has reduced nickel's strategic importance in the energy transition. This technological disruption has coincided with significant supply additions from Indonesian nickel pig iron production, creating a perfect storm for price weakness. However, companies like Canada Nickel are positioning for the next cycle with their Crawford Nickel Sulphide Project, targeting construction decisions by late 2025 and representing the world's second-largest nickel reserve outside of Indonesian and Chinese control.

Canada Nickel - Advanced Development & Pre-Construction

Canada Nickel has successfully completed a comprehensive Bankable Feasibility Study for their Crawford Nickel Sulphide Project, demonstrating robust economics with an after-tax NPV of US$2.5-2.8 billion and a 41-year mine life. The company is progressing toward a critical construction decision by late 2025, with final permits and funding packages currently being finalized for first production anticipated by end of 2027. Strategic validation comes from notable investors including Agnico Eagle (10.4%), Samsung SDI (7.5%), and Anglo American (6.5%), while the company simultaneously develops NetZero Metals, their downstream processing strategy expected to begin production by 2027.

"We've done very well through permitting... There aren't that many projects. And that's the best part... Those of us who have great First Nation community support and infrastructure in place, those are the projects that can quickly get done." - Mark Selby, CEO, Canada Nickel

Carbon and graphite products occupy a unique position in the battery metals landscape, serving as the primary anode material in lithium-ion batteries across all chemistries. Unlike nickel, graphite demand remains robust regardless of cathode chemistry choices, providing more stable long-term growth prospects. The Producer Price Index for carbon and graphite product manufacturing has shown steady but modest increases, suggesting healthy demand absorption without the extreme volatility seen in other battery metals. Strategic developments include projects like Sovereign Metals' Kasiya operation in Malawi, which represents the world's second-largest flake graphite resource produced as a by-product of rutile mining.

Sovereign Metals - Feasibility Study & Pre-Development

Sovereign Metals has completed an Optimised Prefeasibility Study in January 2025 for their Kasiya project in Malawi, demonstrating exceptional economics with an NPV of US$2.3 billion and 27% IRR through their innovative by-product model. The company is advancing toward a Definitive Feasibility Study expected in Q4 2025, having successfully completed pilot trials involving 170,000 cubic meters mined across a 10-hectare site that validated their unique approach to producing graphite as a by-product of rutile mining. Rio Tinto's strategic 19.9% investment provides both technical validation and potential development support for what represents the world's second-largest flake graphite resource.

Supply Dynamics & Geopolitical Risks

Supply chain vulnerabilities represent perhaps the most significant investment consideration across the battery metals complex. Recent disruptions have highlighted the concentration risks inherent in global production patterns, with far-reaching implications for price stability and long-term security of supply.

Tin supply has been severely impacted by the suspension of the Man Maw mine in Myanmar, which historically contributed 7-8% of global production, and ongoing conflicts affecting the Bisie mine in the Democratic Republic of Congo, representing approximately 6% of world output. These disruptions have been compounded by Indonesian regulatory actions that reduced tin exports by 33% in 2024 while domestic mine output dropped 28% due to quota restrictions. The combined effect has created a supply deficit that has supported prices despite broader commodity market weakness. Companies operating in these regions, such as Rome Resources with their projects located just 8km from Alphamin's Mpama Tin Mine in Eastern DRC, face both significant opportunities and elevated geopolitical risks.

Indonesia's dominance in nickel production presents both opportunities and risks for investors. The country produces approximately 2.2 million tonnes annually out of global production of 3.7 million tonnes, representing nearly 60% of world output. This concentration has enabled rapid supply expansion through new hydrometallurgical and pyrometallurgical projects, but also creates geopolitical dependency risks. The Indonesian government's resource nationalism policies, including export restrictions and downstream processing requirements, add additional layers of complexity for international investors. This concentration risk is driving strategic investments in alternative supply sources, with Canada Nickel's Crawford project representing a significant development outside the Indonesia-China sphere of influence.

Graphite supply chains face different but equally significant challenges. While production is more geographically distributed than nickel or tin, the specialized processing required for battery-grade graphite creates bottlenecks in the supply chain. China dominates graphite processing and purification, controlling over 70% of global capacity for spherical graphite used in battery anodes. This dependency has prompted Western governments to prioritize domestic graphite processing capabilities, creating investment opportunities in alternative supply chains. Projects like Sovereign Metals' Kasiya deposit in Malawi offer strategic advantages through their unique by-product model, delivering graphite at incrementally low costs of US$241 per tonne while maintaining tier-1 jurisdiction benefits.

The development of copper-focused projects also presents indirect exposure to battery metals trends. Companies like Gladiator Metals, advancing the Whitehorse Copper Project in Yukon, Canada, benefit from the electrification megatrend driving copper demand while operating in stable jurisdictions with established infrastructure and strong community relationships.

Gladiator Metals - Active Exploration & Resource Development

Gladiator Metals is executing an aggressive drilling campaign at their Whitehorse Copper Project in Yukon, Canada, having completed Phase 1 with 22 holes totaling 4,377 meters and Phase 2 with 35 holes spanning 6,734 meters. The company has ambitious H2 2025 targets including 12,000 meters of drilling at Cowley Park, 10,000 meters at Little Chief, and 5,000 meters at Arctic Chief and Best Chance prospects, with an initial inferred resource for Cowley Park planned for H1 2026. Preliminary metallurgy work is currently underway at ALS Chemex, while the project benefits from proven historical production and established infrastructure in the stable Yukon jurisdiction.

"I would much rather engage in positive community engagement and acceptance and social license than be remote and have overbearing capital requirements or other challenges with what being remote brings." - Jason Bontempo, CEO, Gladiator Metals

The environmental and social governance implications of battery metals mining cannot be ignored by institutional investors. Nickel mining in Indonesia and the Philippines has contributed to significant deforestation and water pollution, while cobalt mining in the Democratic Republic of Congo continues to raise human rights concerns. These ESG considerations are driving increased investment in recycling technologies and alternative supply sources, potentially reshaping long-term market dynamics. Companies with strong ESG credentials, such as Canada Nickel with their NetZero pathway and 89% lower GHG intensity targets, may command valuation premiums in an increasingly ESG-conscious investment environment.

Demand Evolution & Technology Disruption

The battery metals demand landscape is experiencing rapid transformation as energy storage technologies evolve and scale. Understanding these shifts is crucial for investors seeking to position portfolios for the next phase of the energy transition.

Electric vehicle demand remains the primary growth driver for battery metals, but the technology mix is changing rapidly. The surge in LFP battery adoption has fundamentally altered the demand equation for nickel and cobalt while maintaining strong growth for lithium and graphite. LFP batteries now represent the majority of new electric vehicle installations in China and are gaining market share globally due to cost advantages and improved safety characteristics.

This chemistry shift has reduced battery nickel intensity by approximately one-third over the past four years, with further declines expected as LFP technology improves and manufacturing scales. Energy storage systems, projected to account for 20% of the total battery market by 2030, increasingly favor LFP chemistry due to longer cycle life and lower costs, further reducing nickel demand relative to earlier projections.

Tin demand patterns reflect broader digitalization trends beyond electric vehicles. While automotive applications remain relatively modest, the expansion of renewable energy infrastructure, 5G telecommunications networks, and artificial intelligence hardware creates sustained demand for high-quality solder applications. The metal's role in solar panel manufacturing and energy storage system interconnections provides exposure to the broader energy transition beyond just electric vehicles.

Graphite demand exhibits the most consistent growth trajectory among the three metals, as all lithium-ion battery chemistries require graphite anodes. The shift toward LFP batteries actually increases graphite intensity per unit of energy storage compared to nickel-rich chemistries, providing a natural hedge against the chemistry transition affecting other battery metals. Emerging applications in advanced electronics, thermal management systems, and next-generation battery technologies suggest continued demand growth through the decade.

Recycling is emerging as a significant demand offset for battery metals, particularly nickel and cobalt. Advanced recycling technologies, including hydrometallurgical processing and direct recycling methods, are achieving recovery rates exceeding 95% for some metals. As the installed base of electric vehicles reaches end-of-life in the 2030s, recycled content could satisfy 20-30% of battery metals demand, potentially moderating price volatility and supply security concerns.

Price Forecasting & Market Outlook

Near-term price trajectories for battery metals reflect the interplay between supply disruptions, demand evolution, and macroeconomic factors. Each metal faces distinct drivers that suggest different investment strategies and risk profiles.

Tin prices are expected to remain elevated through 2025-2026, with potential for peaks near $36,000 per tonne if supply disruptions persist in Myanmar and the Democratic Republic of Congo. However, normalized production from these regions and increased Indonesian output could pressure prices toward $27,000 per tonne in the medium term. Long-term structural analysis suggests potential supply deficits of approximately 13,000 tonnes by 2030 if industrial and clean technology demand accelerates without matching supply investment. Development projects like Rome Resources' Mont Agoma prospect, with its significant 40-meter tin zone identified in June 2025, represent potential supply additions that could help address these deficits, though execution risks remain elevated in the DRC operating environment.

The International Tin Association projects global demand growth of 2-3% annually through 2030, driven by renewable energy infrastructure, electronics manufacturing, and emerging applications in advanced materials. This growth rate exceeds likely supply additions from new mining projects, suggesting fundamental support for prices above $30,000 per tonne over the investment horizon. The MIT identification of tin as the metal most likely to benefit from electrification, combined with International Tin Association forecasts of 40% demand growth by 2030, supports the structural bull case for tin prices.

Nickel markets face continued pressure from oversupply and demand substitution effects. Current prices around $15,200 per tonne reflect these headwinds, with limited upside potential until either supply discipline emerges or non-battery demand sectors provide additional support. The stainless steel industry, which consumes approximately 70% of global nickel production, offers some demand stability, but growth rates lag far behind historical battery metal expectations. However, the concentration of supply in Indonesia, which now controls 61% of global output—exceeding OPEC's oil dominance in 1973—creates potential for supply management and price support over time.

Canada Nickel's Crawford project represents a significant potential catalyst for North American nickel supply, with first production anticipated by end of 2027 and peak production of 48,000 tonnes annually over a 41-year mine life. The project's first-quartile cost position with C1 costs of US$0.39 per pound provides strong margins even at current price levels, while the company's NetZero pathway offers potential carbon credit revenues and ESG premium pricing.

Medium-term nickel price recovery depends critically on the pace of LFP substitution and overall electric vehicle adoption rates. Scenario analysis suggests prices could remain range-bound between $14,000-18,000 per tonne through 2026-2027, with upside potential if battery chemistry evolution stabilizes or if major supply disruptions occur in Indonesia or other key producing regions. The structural demand growth of approximately 9% CAGR from 2020-2024, with forecasts for doubling to 5-6.4 million tonnes annually by 2030, provides fundamental support for higher prices once current oversupply conditions normalize.

Carbon and graphite pricing shows the most stability among battery metals, with the Producer Price Index advancing modestly and consistently over time. This stability reflects more balanced supply-demand fundamentals and less speculative investment activity compared to other battery metals. Industrial demand provides a solid foundation, while battery applications offer growth potential without the extreme volatility seen in nickel or lithium markets.

The graphite outlook suggests continued modest price appreciation in line with industrial inflation rates, with periodic spikes possible if battery demand growth exceeds processing capacity additions. Specialized battery-grade graphite commands significant premiums over industrial grades, creating opportunities for investors in value-added processing capabilities. Sovereign Metals' Kasiya project offers unique advantages with its by-product model delivering graphite at incremental costs of US$241 per tonne, well below China's weighted average cost of US$257 per tonne, while maintaining 96-98% carbon concentrate grades that exceed typical industry standards of 94-95%.

Copper markets provide indirect exposure to battery metals trends through electrification demand drivers. Gladiator Metals' Whitehorse project targets over 100 million tonnes of high-grade copper resources in a tier-1 jurisdiction, positioned to benefit from structural copper deficits intensifying due to declining ore grades and slower mine development timelines. With copper demand expected to double by 2050 to 40 million tonnes annually, projects like Whitehorse with low capex requirements and near-surface, high-grade mineralization offer attractive risk-adjusted returns.

Investment Strategies & Risk Management

Battery metals investing requires careful consideration of exposure methods, risk management techniques, and portfolio construction approaches. The sector's volatility and complexity demand sophisticated strategies beyond simple commodity price exposure.

Direct commodity exposure through futures markets or exchange-traded funds provides the most straightforward investment approach but requires careful attention to contango, storage costs, and roll yield effects. Physical commodity storage is generally impractical for individual investors, making financial instruments the preferred exposure method.

Equity investments in mining companies offer operational leverage to commodity prices while providing additional sources of return through operational improvements, reserve expansion, and development project success. However, company-specific risks including operational disruptions, regulatory changes, and capital allocation decisions can significantly impact returns independent of underlying commodity prices. The current development pipeline includes several notable projects across different stages of advancement and risk profiles.

Early-stage exploration and resource definition projects like Rome Resources' Mont Agoma and Kalayi prospects in the DRC offer high-risk, high-reward exposure to tin markets.

The Rome Resources is currently in its second-phase resource drilling program with over 5,000 meters drilled across 26 holes, targeting maiden resource estimates expected in September 2025. With three drill rigs on site and approximately 40 personnel at peak operations, Rome Resources represents the highest-risk, highest-potential-reward category of battery metals investment, particularly given the significant 40-meter tin zone discovery in June 2025.

Advanced development stage projects like Canada Nickel's Crawford Nickel Sulphide development represent lower execution risk with substantial scale advantages.

The Canada Nickel is progressing toward a construction decision by late 2025, with final permits, funding packages, and first production anticipated by end of 2027. The project's completed Bankable Feasibility Study shows an after-tax NPV of US$2.5-2.8 billion and 41-year mine life, while strategic investors including Agnico Eagle (10.4%), Samsung SDI (7.5%), and Anglo American (6.5%) provide validation and potential strategic support. Canada Nickel is simultaneously developing NetZero Metals, their downstream processing strategy expected to begin production by 2027.

Active exploration within the established resources category includes Gladiator Metals' Whitehorse Copper Project, which benefits from proven historical production and is currently executing an aggressive drilling campaign.

Gladiator Metals has completed Phase 1 (22 holes, 4,377m) and Phase 2 (35 holes, 6,734m) drilling programs, with H2 2025 targets including 12,000m at Cowley Park, 10,000m at Little Chief, and 5,000m at Arctic Chief/Best Chance prospects. An initial inferred resource for Cowley Park is planned for H1 2026, while preliminary metallurgy work is underway.

Pre-feasibility and feasibility stage projects offer moderate risk with clearer development timelines.

Sovereign Metals' Kasiya project completed an Optimised Prefeasibility Study in January 2025 showing NPV of US$2.3 billion and 27% IRR, with a Definitive Feasibility Study expected in Q4 2025. The company has successfully completed pilot trials involving 170,000 cubic meters mined across a 10-hectare site, demonstrating the viability of their unique by-product model. Rio Tinto's 19.9% strategic investment provides technical validation and potential development support.

Diversification across the battery metals complex helps manage individual commodity risks while maintaining exposure to the broader energy transition theme. A balanced approach might include exposure to established producers with diversified metal portfolios, development companies with high-quality projects, and processing companies that capture value-added margins.

Geographic diversification proves challenging given the concentrated nature of battery metals production, but investors should consider the regulatory and political stability of operating jurisdictions. Projects in Canada's Yukon Territory or Malawi present different risk profiles than operations in the Democratic Republic of Congo or Indonesia, requiring careful due diligence and risk-adjusted return analysis.

Environmental, social, and governance considerations increasingly influence investment flows in the battery metals sector. Companies with strong ESG practices and sustainable mining approaches may command valuation premiums and face lower regulatory risks over time. Canada Nickel's carbon-negative potential and First Nations partnerships, Gladiator Metals' community engagement initiatives including bi-monthly newsletters and local hiring programs, and Sovereign Metals' low-impact processing methods represent emerging best practices that may become industry standards.

For Investors

The battery metals investment landscape presents both significant opportunities and substantial risks as the global economy transitions toward electrification and renewable energy. Tin, nickel, and graphite each face distinct market dynamics that require tailored investment approaches and careful risk management.

Supply chain vulnerabilities and geopolitical concentrations create the potential for significant price volatility across all three metals, while technological evolution in battery chemistry adds another layer of complexity to demand forecasting. Investors must balance the growth potential of the energy transition against the very real risks of technological disruption and supply chain reconfiguration.

The most compelling investment opportunities likely exist in companies and assets that can adapt to changing technology requirements while maintaining cost competitiveness across multiple market scenarios. This suggests focusing on diversified producers, value-added processors, and companies with strong balance sheets capable of weathering commodity cycles.

As the energy transition continues to evolve, battery metals will remain critical components of the global decarbonization effort. However, success in this sector requires sophisticated analysis, careful risk management, and the flexibility to adapt to rapidly changing market conditions. Investors who can navigate these complexities while maintaining long-term perspective stand to benefit from one of the defining investment themes of the coming decade.

Analyst's Notes

Subscribe to Our Channel

Stay Informed