Distillate Stocks Are 2.3 Million Barrels From a 23-Year Floor

US distillate stocks sit 2.3M barrels above a 23-year floor. Q4 diesel costs will pressure trucking and manufacturing even if a Hormuz deal brings crude down.

- WTI settled at $96.02 and Brent at $97.81 on June 3, a third consecutive gain on US-Iran military exchanges, before a conditional Israel-Lebanon ceasefire pulled Brent 0.8% to $97.03 and WTI 1.0% to $95.32 in early European trade.

- Commercial crude stocks fell 8 million barrels to 433.7 million barrels for a sixth straight weekly draw; the Strategic Petroleum Reserve (SPR) released an additional 8 million barrels over the same period (EIA via WSJ).

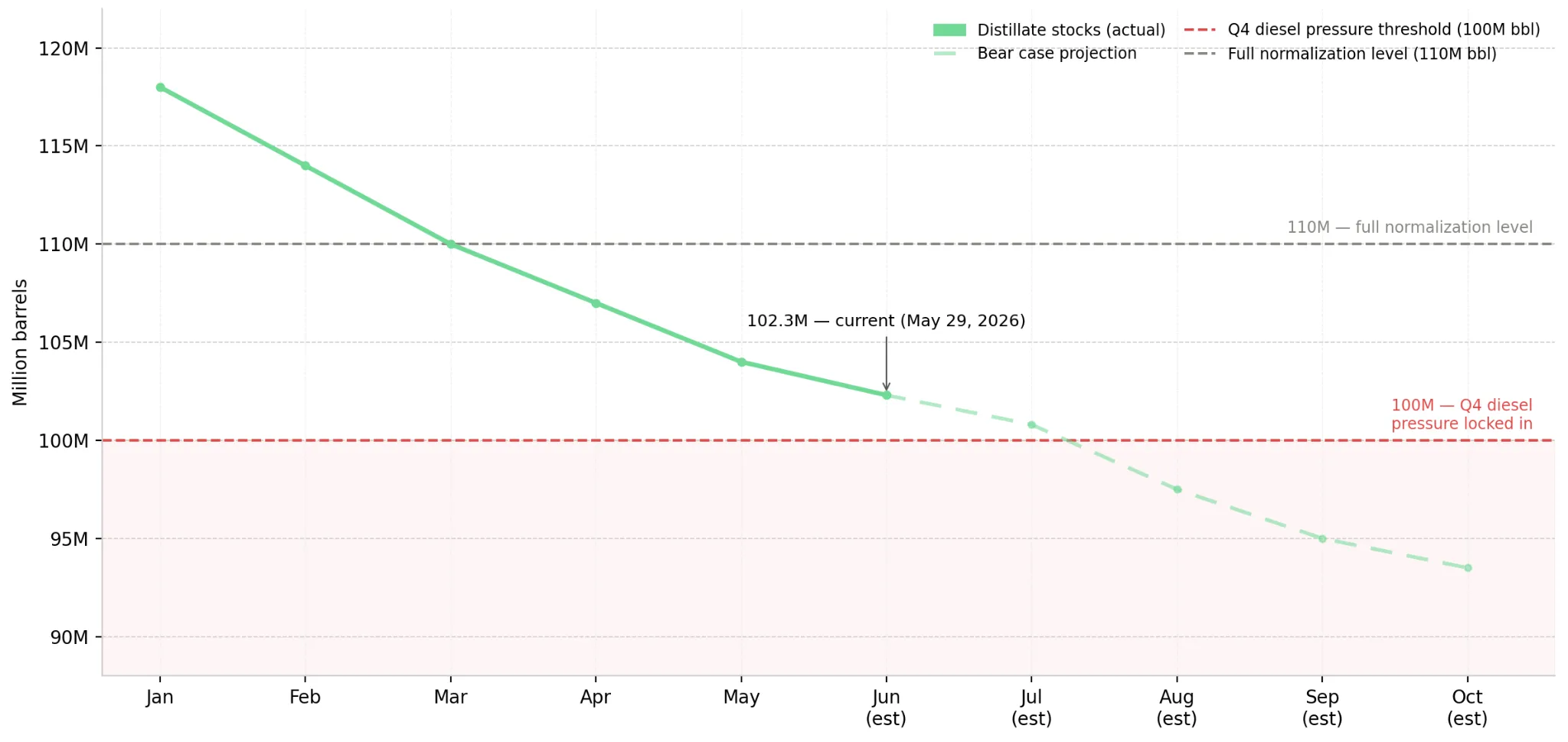

- US distillate inventories currently stand 2.3 million barrels above a 23-year floor, and analysts warn that diesel costs are likely to remain elevated through Q4 regardless of where crude prices settle after any Hormuz resolution.

- Macquarie Group economists placed the expiry of pre-war global oversupply in one to two months, positioning acute physical tightness in late July to August 2026 if Hormuz remains closed.

- Brent below $90 for five consecutive sessions after a confirmed Hormuz deal signals crude relief. Distillate stocks below 100 million barrels in the EIA Weekly Petroleum Status Report confirm Q4 diesel pressure is structural.

Ceasefire Headlines Are Moving Prices That Inventory Data Is Already Deciding

WTI settled at $96.02 and Brent at $97.81 on June 3 after US and Iranian forces exchanged fire, per the WSJ on June 3, 2026. A conditional Israel-Lebanon ceasefire announced in early European trade on June 4 reversed both benchmarks, Brent to $97.03 and WTI to $95.32, as markets read the deal as a precondition for a broader US-Iran settlement, per the WSJ.

The moves obscure a physical problem. Hormuz's closure removes 11 to 14 million barrels per day from global supply. Commercial crude stocks fell 8 million barrels to 433.7 million barrels, a sixth consecutive weekly draw, while the SPR released an additional 8 million barrels in the same week. The government is spending strategic reserves to hold prices below $100, and that capacity is finite.

Pre-War Oversupply Has Been the Buffer: Macquarie Places Its Expiry at Late July

Macquarie Group economists assessed that current withdrawal rates leave the market adequately supplied for roughly another month or two, after which physical availability is expected to tighten materially if Hormuz remains closed. Ritterbusch and Associates reinforced that timeline, noting that Trump's stated intention to maintain the blockade through Labor Day, September 1, 2026, makes near-term ceasefire negotiations largely irrelevant to the forward supply picture per the WSJ.

On the distillate side, inventories at 102.3 million barrels sit 2.3 million barrels above a 23-year floor. Muenster of Breakthrough warned that stocks are on a trajectory toward especially low levels by Q4, with diesel prices likely to remain under pressure even if a Hormuz resolution brings crude prices down.

Energy exposure is not uniform. Holding broad energy ETFs or upstream crude producers captures the Hormuz binary, prices move with ceasefire headlines, but does not isolate the distillate margin story. There is a likelihood of higher freight and fuel costs compressing margins through Q4 regardless of where crude settles.

Two Separate Clocks Are Running

The Israel-Lebanon ceasefire does not resolve the Hormuz supply gap. The operative question is whether Macquarie's late-July buffer expiry arrives before a Hormuz settlement is confirmed.

Base case: Hormuz reopens July 2026:

- Brent falls below $90 for five consecutive sessions

- Crude-linked positions retreat from current levels

- Distillate stocks remain below 100 million barrels, sustaining Q4 diesel cost pressure for trucking and manufacturing independent of crude price movement

Bear case: Hormuz closed through Labor Day, September 1, 2026:

- Trump's stated blockade timeline holds; Macquarie's oversupply buffer expires late July

- Physical availability tightens materially; Brent trades through $100 per Mizuho's Robert Yawger

- Distillate stocks cross below 100 million barrels, locking in Q4 diesel headwinds for unhedged trucking and industrial operators regardless of how crude prices resolve

Distillate below 100 million barrels confirms Q4 diesel pressure is structural. A Hormuz announcement without a five-session Brent hold below $90 is a false relief signal.

Diesel Exposure Is Not the Same Position as Crude Exposure

Integrated refiners with distillate-heavy slates benefit from widening margins as diesel diverges from crude. Unhedged trucking and industrial manufacturers face Q4 cost headwinds regardless of where Brent settles.

A long upstream crude position carries ceasefire binary risk; it moved on headlines that reversed multiple times on June 3. A distillate-exposed refining or logistics position carries the Q4 inventory clock: a 6-to-10-week timeline diplomatic outcomes cannot shorten. Muenster's Q4 call requires only that distillate stocks fail to rebuild before Q4 demand rises, a condition current inventory levels make structurally probable.

What to Monitor

Prices above $95 are sustained by six consecutive weekly crude draws plus ongoing SPR releases. Crude-linked positions benefit while draws continue and no Hormuz deal is confirmed, provided distillate stocks remain above 100 million barrels.

A confirmed US-Iran deal followed by Brent holding below $90 for five consecutive sessions reverses the crude equity premium. The reversal does not normalize diesel: distillate stocks must rebuild above 110 million barrels for full-cycle cost normalization, 6 to 8 weeks of net builds post-reopening.

EIA Weekly Petroleum Status Report every Wednesday at 10:30 ET should be monitored. Crude below 420 million barrels signals buffer expiry. Distillate below 100 million barrels confirms structural Q4 diesel pressure. A Hormuz announcement without a five-session Brent hold below $90 does not change the distillate thesis.

Analyst's Notes

Subscribe to Our Channel

Stay Informed