Undervalued? Why Pampa Medina Could Transform the Marimaca Investment Case

Marimaca Copper CEO argues MOD's DFS value is priced in leaving Pampa Medina's Kamoa-Kakula-style copper discovery as a free option.

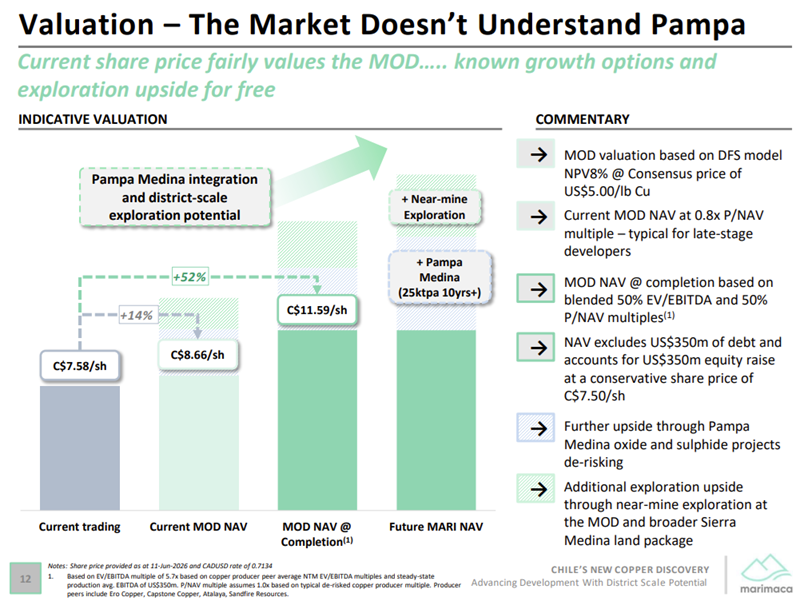

- Marimaca Copper's CEO Hayden Locke highlights how the market is valuing Marimaca Copper roughly in line with its flagship Marimaca Oxide Deposit alone and where the Pampa Medina exploration story is currently being priced at close to zero.

- The Marimaca Oxide Deposit is fully DFS-complete and holds its key environmental approval, addressing several of the risk factors Locke says typically cause junior miners to trade at a discount.

- Ongoing step-out drilling at Pampa Medina continues to extend a high-grade, stacked sediment-hosted copper-silver system that management compares directly to the world-class Kamoa-Kakula deposit in the Democratic Republic of Congo.

- A recently strengthened board, including former First Quantum Minerals projects director Zenon Wozniak and former Mantos Copper CEO Giancarlo Bruno, is intended to support Marimaca through its next phase of construction execution.

- Investors should watch for a project financing announcement expected before the end of 2026, Sectorial Permit approvals targeted for Q4 2026, and a maiden Pampa Medina sulphide resource due in early 2027.

Copper is trading near all-time highs, and investors are once again hunting for developers that combine scale, jurisdiction and a credible path to production. Marimaca Copper Corp. (TSX:MARI) President and CEO Hayden Locke has laid out a straightforward argument where the company's flagship Marimaca Oxide Deposit (MOD) is trading roughly at fair value on its own as the market is attaching little to no value to Marimaca's second, potentially larger, asset at Pampa Medina.

Why Junior Miners Trade at a Discount

Locke opened the interview by outlining the reasons junior miners typically trade cheaply: early-stage status without completed studies, unresolved permitting, a lack of exploration upside, high execution risk tied to remote or difficult jurisdictions, financing overhangs relative to market capitalisation, and weaker perceptions of board and management capability. Running through that checklist against Marimaca, he argues the company doesn't fit the pattern. The MOD has a completed Definitive Feasibility Study (DFS), it has its key environmental approval with the Resolución de Calificación Ambiental, or RCA granted in November 2025, and the company holding a significant cash balance to keep advancing the project.

Marimaca sits in Chile's Antofagasta region, the world's largest copper-producing jurisdiction, and within 25 kilometres of the Port of Mejillones thus materially reducing infrastructure and execution risk relative to more remote developments.

A Fully Costed Path to Production

The DFS underpinning the MOD points to a 13-year mine life on Proved and Probable reserves of 179 million tonnes at 0.42% Cu for 748,000 tonnes of contained copper, supporting steady-state production of roughly 50,000 tonnes of copper cathode a year. Using the DFS's more conservative long-term price assumption of US$4.30/lb, post-tax NPV8 is at US$709 million with a 31% IRR. At a three-month average COMEX copper price of US$5.05/lb, the project could generate a post-tax NPV (8%) of US$1.1 billion, 39% IRR with a 2.2-year payback. Initial capital intensity of roughly US$11,700 per tonne of annual copper production ranks among the lowest of any global greenfield copper project of comparable size, and the project's profitability index places it among a small group of sub-US$1 billion-capex developments generating more than 1.5 times their capital cost in net present value.

Locke's central point is that this asset alone roughly explains the current share price.

"We're trading at a significant discount to the eventual fully financed value of the MOD. And then the reality is all of the exploration potential that we've seen at Pampa Medina and all of that near mine exploration potential and tier one discovery potential of this project is completely for free to investors who are owning our shares today."

Pampa Medina: The Ignored Free Option

Pampa Medina, a sediment-hosted copper-silver system located approximately 28 kilometres from the MOD, has six drill rigs currently running step-out and infill programmes. Locke drew a direct comparison to the Kakula selective mining zone within the Kamoa-Kakula complex in the Democratic Republic of Congo which is widely regarded as one of the best copper discoveries of the past two decades, and a deposit he says is broadly misunderstood by generalist investors.

Kakula itself spans roughly 6km by 1.5km and hosts 400 million tonnes at approximately 3% copper at a 1% cut-off, with an average true thickness of around 12 metres. Locke argues Pampa Medina is already showing comparable, and in places thicker, high-grade intervals across a growing footprint.

"We're not talking about one horizon. If we go back and have a look at the Kakula example, one horizon which is mineralized, and we're talking about stacked horizons like this in a vertical sense. All of which are economic widths and grades for an underground sediment hosted copper deposit," Locke said.

That comparison has since been reinforced by drilling. Most recent assay results returned 20 metres at 2.65% copper and 13.9 g/t silver from 564 metres including 6 metres at 6.11% copper and 24.0 g/t silver, plus 104 metres at 1.01% copper and 4.7 g/t silver from 664 metres, including 40 metres at 2.04% copper and 11.1 g/t silver. A second hole, SPRD-08B, intersected mineralisation in basement metasediments for the first time at the project, reaching a total depth of 1,052 metres and hinting at further extension potential beyond the previously modelled host units. Unlike Kamoa-Kakula, which sits beneath a large overlying aquifer that has complicated mining, Locke notes Pampa Medina has no comparable water constraint.

Crucially, none of this exploration upside nor the identified oxide extensions at Pampa Medina, which Locke separately believes could add 20,000-25,000 tonnes a year of additional cathode production without further exploration success, is reflected in Marimaca's current share price, in his view.

Interview with Hayden Locke, President & CEO of Marimaca Copper Corp.

A Strengthened Board Onto the Execution Phase

Locke also pointed to recent additions to Marimaca's board as addressing another discount driver: perceived management capability. Chairman Giancarlo Bruno is a former CEO of Mantos Copper and former VP of Anglo American's Norte division, with direct experience building the Mantoverde mine. Non-executive director Zenon Wozniak spent 23 years at First Quantum Minerals as director of projects, overseeing development of nearly every mine the company built. Project Director Josh Watson, based in Santiago, brings large-scale project execution experience to the in-country team. Locke frames this as building out the operational capability the market may not yet be crediting to a relatively young management team.

The Investment Thesis for Marimaca Copper

- The MOD's DFS economics: Up to 39% IRR range and a sub-2.5-year payback,a valuation floor that appears to be roughly reflected in the current share price, according to management's own analysis.

- Pampa Medina's exploration success, if it continues at the current pace, represents largely unpriced upside, maiden sulphide resource is targeted for early 2027.

- Environmental approval (RCA) is in hand and Sectorial Permits were submitted on schedule in April 2026, with approvals expected in Q4 2026.

- Project financing progress, led by advisor Endeavour Financial, is expected to be finalised by Q4 2026; the terms and mix of debt versus equity will materially affect per-share dilution.

- The sulphuric acid MOU covering the company's PADA Plant could improve the MOD's operating cost profile if it converts to a binding joint venture with updates to watch following the initial six-month evaluation period.

- Near-mine oxide targets (Cindy, Mercedes, Roble, Tarso, Sierra) offer additional, currently unquantified resource growth close to existing infrastructure.

- Construction is targeted for 2027 with first cathode guided for 2029; any slippage in permitting or financing timelines is a risk to monitor closely.

Macro Thematic Analysis

Copper's structural demand story driven by electrification, grid infrastructure and data centre build-out has pushed prices toward record levels through much of 2026, even as short-term volatility linked to Middle East tensions has periodically weighed on sentiment. Within that backdrop, the pool of copper developers with permitted, financeable, near-production-scale assets has thinned considerably: Locke notes that since Arizona Sonoran's acquisition by Hudbay and Foran's acquisition by Eldorado, there are few remaining junior copper developers targeting roughly 50,000 tonnes per annum of production with a clear line of sight to construction.

As Locke put it: "This project on which we which we are about to take into production is very valuable in the current copper environment. Investors are effectively getting a free option, in my view, on Pampa oxide growth, which I have a high degree of confidence in."

The mineral scarcity combined with Chile's status as the world's largest copper-producing jurisdiction, underpins Locke's argument that Marimaca deserves re-rating toward peers that have already reached the construction and financing stage, a dynamic he illustrates by pointing to gold developers such as Montage Gold, which have traded well above net asset value once fully financed.

TL;DR

Marimaca Copper's CEO Hayden Locke argues the company's share price roughly reflects only the value of its fully permitted, DFS-complete Marimaca Oxide Deposit — leaving the fast-growing Pampa Medina discovery effectively unpriced. Recent drilling (SPRD-07, SPRD-08B, SPRD-09) extended a high-grade, stacked sediment-hosted copper-silver system Locke compares to the world-class Kamoa-Kakula deposit in the DRC. With environmental approval in hand, Sectorial Permits submitted, project financing expected by year-end 2026, and construction targeted for 2027, Marimaca is positioning itself among a shrinking pool of financeable, near-production-scale copper developers in a Tier 1 jurisdiction.

Frequently Asked Questions (FAQs) AI-Generated

Analyst's Notes

Subscribe to Our Channel

%20(1).png)

Stay Informed