Inside Cartier's Transitional Year: Three New Gold Zones and a September PEA

Cartier Resources grows Cadillac gold resource to 3.2M oz with new discoveries; updated PEA due Sept. 2026 amid talk of a strategic transaction.

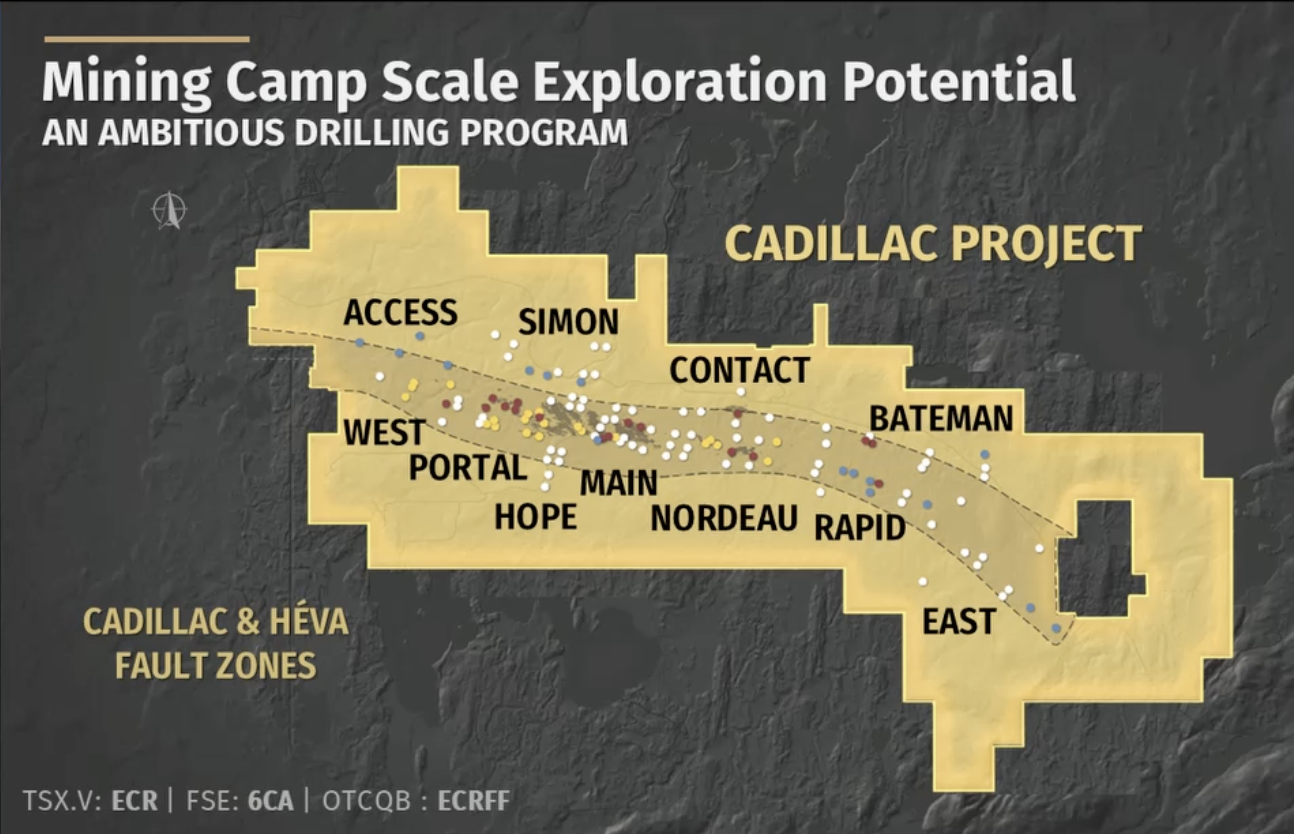

- Cartier Resources has redesigned its exploration program after early drilling on its Cadillac project in Abitibi Greenstone Belt, Quebec confirmed multiple new gold discoveries beyond the past-producing Chimo mine, including the Contact Zone, the Portal area, and a new high-potential zone south of the main deposit.

- An updated Preliminary Economic Assessment (PEA) is targeted for September 2026 replacing the 2023 study to reflect a larger resource base of 3.2 million ounces versus 2.3 million in 2023, higher metallurgical recoveries, and a materially stronger gold price environment.

- The company is evaluating toll milling, processing ore at nearby third-party mills rather than building one on site, as a way to reduce capital costs and accelerate permitting timelines.

- Management indicates the most likely path forward is attracting a strategic partner, developer, or acquirer rather than self-funding full mine development, citing capital, permitting, and team-building constraints in the current market. Agnico Eagle already holds a 27% stake in Cartier.

- Cartier holds over $5 million in treasury and plans an active investor outreach schedule through the fall, including events in Europe, Asia, and the United States alongside recent OTCQB trading in the U.S.

Cartier Resources (TSXV:ECR) is a junior gold exploration company focused on the Cadillac project, which spans 15 to 20 kilometers of the Cadillac fault in Quebec's Abitibi Greenstone Belt - a district with a long history of gold production. In a recent interview, President and CEO Philippe Cloutier described 2026 as a transitional year for the company, marked by unexpectedly strong drilling results, a substantially changed gold price environment, and a shift in strategic direction. Cloutier summarised the year's developments directly:

"The economic situation of the gold price and the project metrics have changed considerably since the publication of our PEA in 2023. We're working on that and we should get that across the finish line with the new significant resource that we put out that has been a gamechanger."

The interview covered exploration results, the rationale for redesigning the drill program, the timeline for an updated economic study, and the company's positioning relative to potential strategic partners.

Drilling Results Beyond the Historic Chimo Mine

The Cadillac project's central asset is the Chimo mine, a past-producing gold operation that closed in 1997 due to low gold prices rather than resource depletion. A key question entering this year's drill program was whether Chimo represented the only significant mineralization on Cartier's 15-to-20-kilometer land package. Cloutier stated plainly that the answer is no. Approximately 5 kilometers northeast of Chimo, drilling identified a new mineralized environment along a fault parallel to the Cadillac fault, referred to as the Contact Zone discovery. Historical geophysical data suggests this trend may extend up to 7 kilometers further along the Héva fault.

A second area, the Portal zone, sits roughly 1 kilometer west of the Chimo shaft and benefits from existing underground ramp infrastructure built in the 1980s, which management notes has already delivered high-grade intervals at shallow depth.

A third area , the Hope area at the south of the main deposit, has drawn comparisons in scale of opportunity to the Canadian Malartic and Odyssey mining systems operated by Agnico Eagle nearby. With roughly 35% of the planned 100,000-meter, 600-hole drill program completed, the company reports having already met its primary objective of demonstrating an additional mining camp on the property.

Redesigning the Exploration Program

The scale and diversity of these results prompted Cartier to redesign its drilling strategy. Rather than continuing uniformly across the original 11 planned targets, the company is now considering how to allocate meters across four distinct program areas: continued in-fill drilling around the main Chimo resource, focused "sniper-style" drilling at the shallow, high-grade Contact and Portal zones, and a larger-scale, multi-year program for the deeper southern target, which Cloutier suggested would require drilling comparable in scope to the Malartic camp - potentially hundreds of holes and hundreds of thousands of meters.

Management is weighing the trade-offs between pursuing this expanded drilling immediately, preserving the original program as designed, or pausing to publish updated economic figures before committing further capital. Cloutier noted the company held over $5 million in treasury, which is informing the pace of this decision-making over the summer.

The Upcoming Preliminary Economic Assessment

Cartier's next major disclosure will be an updated PEA, targeted for release in September 2026, ahead of the fall conference season. The 2023 PEA was built using a gold price of $1,750 per ounce, a resource base of 2.3 million ounces, an on-site mill, and historical metallurgical recovery rates of 93%. The updated study will incorporate a gold price that has traded above $4,000 per ounce, a resource base that has grown to 3.2 million ounces, and metallurgical test results showing recoveries near 97%, based on independently monitored composite sample testing conducted at a lab in Vancouver. The new study is also expected to evaluate toll milling - using existing third-party mills along the regional highway network - as an alternative to building a mill on site, a scenario management believes could reduce capital expenditure and shorten permitting timelines. Cloutier described the shift in inputs concisely:

"Those are two different economic environments, the 2023 environment and the 2026 environment. We're going to make use of that for sure and I'm pretty sure this going to impress a lot of our shareholders."

Interview with Philippe Cloutier, President and CEO, Cartier Resources

Strategic Positioning and the Case for Consolidation

Asked directly about the company's exit or monetisation strategy, Cloutier indicated that pursuing a strategic transaction, rather than self-funding mine development, was the preferred and more likely route. He pointed to a wave of foreign capital moving into Quebec gold assets over the past 18 months as evidence the district is attracting outside interest, citing Gold Fields' acquisition of Osisko Mining's Windfall project, an African-focused operator's purchase of a project in the region, and Fresnillo's acquisition of Probe Gold.

Cloutier also addressed Agnico Eagle's existing 27% stake in Cartier, acknowledging the competitive tension inherent in Agnico's own portfolio, which spans investments in more than 100 exploration companies, but was clear that Cartier isn't sitting back and waiting for Agnico to provide development impetus. Rather than commit to one path prematurely, he described the company's current approach as "paper engineering": modelling the economics of several scenarios in parallel before choosing between them. That modelling operates on two levels at once. On the drilling side, it means weighing how to allocate the remaining metreage of the 100,000-metre programme - whether to keep testing the original eleven targets or redirect capital toward the newer Contact, Portal and southern discoveries - against the dilution cost of raising fresh capital to fund both. On the corporate side, the same discipline is being applied to the exit question itself, with management running the numbers on a straight sale, a spin-out of specific assets, or a partnership structure, so that whichever route the board ultimately recommends to shareholders is grounded in tested economics rather than a preferred narrative.

Market Outreach and Near-Term Catalysts

Beyond the technical program, Cartier has expanded its investor outreach this year, including engagement in Europe, inbound interest from Asia, and the recent start of trading on the OTCQB market in the United States. Management outlined a busy fall schedule including the Denver Gold Show, the Beaver Creek Precious Metals Summit in mid-September, and the New Orleans Investment Conference, alongside continued travel in Europe and Asia. The updated PEA, expected in September, is positioned as the next major catalyst, intended to give the market a clearer basis for comparing Cartier's project economics against peers and potential acquirers.

The Mining Camp Thesis

Cloutier framed Cartier's broader thesis around the concept of a "mining camp" - a cluster of deposits along a single geological trend that historically has been developed piecemeal by multiple companies over decades. He described Cartier's land consolidation along the Cadillac fault as a rare opportunity to hold and advance several such deposits under one company, rather than the more typical scenario where each is discovered and developed separately by different operators over 50 to 60 years.

This framing underpins management's argument that the company's current asset base - spanning at least four distinct mineralization types across 15 kilometers of strike length - represents a more advanced and differentiated story than in prior years, even though the company remains in the exploration and assessment phase rather than construction.

The Investment Thesis for Cartier Resources

- Resource growth: Resource base has grown from 2.3 million to 3.2 million ounces of gold since the 2023 PEA, with an updated economic study expected in September 2026.

- Improved economics inputs: New PEA will reflect a gold price environment above $4,000/oz (versus $1,750/oz in 2023) and improved metallurgical recoveries of ~97% (versus 93%).

- Multiple new discoveries: Contact Zone, Portal area, and a southern target add optionality beyond the historic Chimo resource, with existing ramp infrastructure at Portal potentially reducing future development costs.

- Capital efficiency options: Toll milling under evaluation could lower capex requirements and shorten permitting timelines relative to building an on-site processing facility.

- Financial position: Treasury of over $5 million supports near-term work programs without immediate financing pressure, according to management.

- Strategic shareholder base: Agnico Eagle holds a 27% equity stake, and management has flagged consolidation activity by other producers in the region as a relevant industry backdrop.

- Stated strategic preference: Management has indicated a preference for a strategic transaction (sale, partnership, or spin-out) over standalone mine development, citing capital, permitting, and team-building constraints.

- Expanding investor access: Recent OTCQB listing in the U.S. and planned attendance at major fall investment conferences (Denver Gold Show, Beaver Creek, New Orleans) aim to broaden the shareholder base.

Cartier's update reflects a broader dynamic in the junior gold sector: rising gold prices and constrained new mine supply have increased strategic and M&A interest in advanced-stage exploration assets located in established, low-risk mining jurisdictions. Management cited recent regional transactions - including acquisitions of Quebec-area gold assets by international producers - as evidence that permitting complexity and capital costs elsewhere are pushing larger companies toward jurisdictions like Quebec. For explorers, this has shifted incentives away from full self-development and toward positioning assets for acquisition or partnership. As Cloutier put it, describing the company's approach to project economics: "there's a lot of paper engineering and thinking... and we have over $5 million in the bank."

TL;DR

Cartier Resources' Cadillac project has expanded well beyond the historic Chimo mine, with new discoveries at Contact, Portal, and a southern target adding to a resource base that has grown to 3.2 million ounces. An updated economic assessment due in September 2026 will incorporate a much higher gold price and improved metallurgical recoveries than the 2023 study. Management has signalled a preference for a strategic transaction over standalone development, supported by a $5 million-plus treasury and an expanding investor outreach program.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed