East Star Resources Secures Major Partners to Fund Path Towards Cash Flow in Kazakhstan

East Star Resources offers low-dilution exposure to Kazakhstan's copper and gold potential, backed by Shinghai and Endeavor Mining partnerships.

- East Star Resources (LSE:EST) is a copper and gold exploration and development company operating exclusively in Kazakhstan, one of the world's most mineral-rich but underexplored jurisdictions with world-class deposits demonstrating the scale of endowment available.

- The company has signed a joint venture agreement with global mine-builder Xinhai Mining which will fund the Verkhuba copper deposit through to production in exchange for a 70% interest, with East Star retaining a 30% free-carried stake and bearing no capital cost exposure.

- Endeavour Mining has committed up to $25 million in phased exploration funding with East Star retaining a 20% free-carried interest to prefeasibility providing exposure to a potential major gold discovery at no further cost to shareholders.

- East Star's advanced project generator model enables the company to advance multiple projects simultaneously whilst minimising capital expenditure and dilution risk.

- Beyond the two flagship joint ventures, East Star holds 100% interests in Rulikha (with 23 million tonnes at approximately 2.4% copper equivalent), Rulikha North, Telescope, Picket, and Snowy, providing a diversified project pipeline with independent value creation potential and multiple near-term catalysts.

East Star Resources (LSE:EST) is positioned at the intersection of two significant investment themes: the global structural demand for copper and gold, and the untapped potential of Kazakhstan as one of the world's last great unde rexplored mineral frontiers. Alex Walker, Director and CEO of East Star Resources, outlined a business model that has evolved considerably from the company's origins as a traditional junior explorer.

The company has now secured partnerships with some of the mining industry's most recognised names: Xinhai Mining, a global mine-builder with over 2,500 projects completed worldwide, and Endeavour Mining, a FTSE 100 gold producer that has delivered six mines on time and under budget in recent years.

The Business Model: Advanced Project Generation

Walker describes East Star not as a conventional project generator, but as an advanced project generator. While standard project generators typically farm out assets early and retaining only small royalties or nominal stakes, East Star's approach is to take projects further along the development pathway before seeking partners, retaining substantially larger economic interests in the process.

The company's evolution was catalysed by participation in the BHP Xplor programme, which Walker credits as transformational. This shaped East Star's approach to geological targeting, large-scale soil sampling, and belt-scale reconstruction work which the kind of systematic, costly exploration that major mining companies undertake but that the junior market rarely rewards in market valuation.

Walker is candid about the rationale for partnerships: when the market cap of a company significantly undervalues the through-value of an asset, bringing in a capable partner at a premium to that implied value is a better outcome for shareholders than attempting to self-fund development at the cost of ongoing dilution. As Walker noted:

"Getting a value of certainly about 3-4 times our market cap with the joint venture partnership and bringing in someone who we certainly believe could do it a lot cheaper and a lot faster than we would made a lot of sense for us."

Alongside its JV-backed projects, East Star retains 100% of a number of prospects, including Rulikha, Rulikha North, Telescope, Picket, and Snowy. Walker is clear that the company intends to remain an active explorer in its own right, not merely a passive royalty holder.

Interview with Alex Walker, Director & CEO of East Star Resources

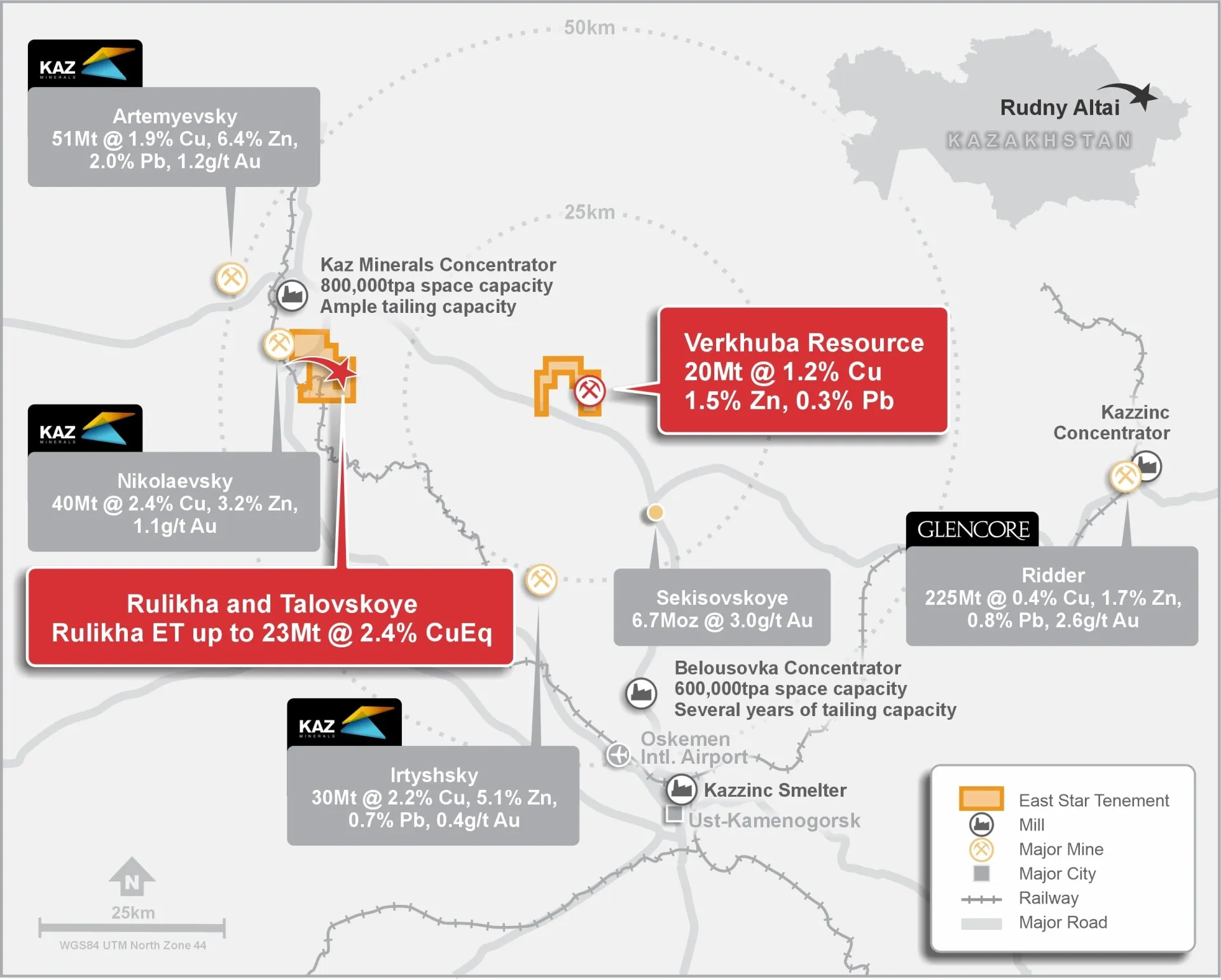

The Verkhuba Copper Deposit

Verkhuba is East Star's most advanced asset situated in the Rudny Altai belt of Kazakhstan. It is a JORC-compliant volcanogenic massive sulphide (VMS) deposit containing over 20 million tonnes grading 1.2% copper equivalent, with zinc and lead credits. East Star has signed a joint venture agreement with Xinhai. Under the terms of the agreement, Xinhai will fund the project through to production, earning up to 70% of the asset. East Star retains a 30% free-carried interest. Critically, East Star bears no capital cost exposure as the 30% production interest is delivered without further dilution to East Star shareholders.

The timeline outlined by Walker points to a mining licence application being submitted this year, with construction beginning by end-2027 and first cash flow potentially by 2028. The brownfield nature of the site with historic workings and existing community relations reduces permitting risk compared with a greenfield project. Walker has personally maintained relationships with local mayors and regional authorities, reporting consistently positive feedback on the prospects of renewed industrial development.

Importantly, East Star has not closed off further exploration potential at Verkhuba. Walker notes that as a distal VMS, the primary sulphide source has not yet been located. The massive sulphide endowment could represent material additional resource upside, a consideration that influenced the decision to joint venture rather than sell the project outright.

The Endeavour Mining Partnership

Alongside Verkhuba, East Star has entered a separate joint venture with Endeavour Mining which is expanding its geographic footprint from Africa into new jurisdictions, with Kazakhstan selected as a priority. The agreement covers two exploration belts in Kazakhstan: the Stepnogorsk region and the Karaganda region, covering a substantial portion of the Balkash-Ili magmatic arc.

Walker contextualised the scale of the opportunity:

"If we had a 20% of something that Endeavour was building, even with financing, that's a billion dollar company for just East's percentage and that's something that I'm really excited to to maintain and try and deliver."

Endeavour is funding an initial $5 million programme over approximately 2 years for greenfields project generation work. A subsequent $20 million phase earns Endeavour 70%, with East Star free-carried through to prefeasibility study. This prospect illustrates the potential magnitude of value that a successful Endeavour JV outcome could deliver to East Star shareholders.

Rulikha and the 100% Owned Project Pipeline

Beyond the two flagship JVs, East Star retains full ownership of several assets that represent additional optionality. The most advanced is Rulikha, a historic copper deposit with an exploration target implying more than 23 million tonnes at approximately 2.4% copper equivalent — a notably higher grade than Verkhuba.

Walker is candid about the development complexity at Rulikha, given its proximity to a village and the permitting requirements that entails. However, he notes that all required surface access permits have been obtained, that community relations are positive, and that an environmental and social governance framework has been developed with the support of a specialist who previously worked with the European Bank for Reconstruction and Development and the World Bank.

Walker also highlights Picket and Snowy in the Karaganda region as earlier-stage assets with the potential to be advanced towards JV discussions. Telescope and Rulikha North represent further VMS exploration targets, with Rulikha North having returned 120 metres of disseminated sulphide mineralisation in drilling, pointing to a potentially significant hydrothermal system.

Kazakhstan: The Jurisdictional Context

Walker repeatedly returns to the quality of Kazakhstan as a mineral province. The country is home to some of the world's largest copper and gold deposits, including Zhezkazgan (22 million tonnes of contained copper), Aktogay (10–12 million tonnes of contained copper), and Vasilkovskoye (15 million ounces of gold).

Walker draws a direct comparison to Western Australia as a jurisdiction with extraordinary deposit diversity, significant but underutilised historical data, and large areas still available for licensing:

"It's like getting into Western Australia and having the entire state almost available to peg. You're a bit of a kid in a candy store."

Walker acknowledges that regulatory risk and community relations are real considerations in any emerging market, but his experience in annual in-person meetings with local mayors and regional officials has been consistently positive. He describes Kazakhstan as having the political will for industrial development, with permitting timelines for comparable projects running from approximately six to twelve months.

The Investment Thesis for East Star Resources

- Non-dilutive path to copper production: The Verkhuba JV with Xinhai provides East Star shareholders with a 30% interest in a mine expected to commence production by end-2028, funded entirely by the partner. Investors gain copper production exposure without the capital raise risk that typically accompanies junior mine development.

- Tier-1 discovery optionality via Endeavour Mining: The Endeavour JV provides access to a $25 million funded exploration programme across some of Kazakhstan's most prospective gold belts, with East Star free-carried to prefeasibility at 20%. A 2-million-plus ounce gold discover would represent a company-making event for East Star.

- Multiple shots on goal from the 100%-owned pipeline: Rulikha, Telescope, Rulikha North, Picket, and Snowy each represent independent value creation opportunities. Walker's stated intention to pursue further JV structures or advance projects independently means East Star's portfolio provides diversification against single-project failure.

- Major company validation: The involvement of Endeavour Mining as both JV partner and shareholder, and Xinhai lends institutional credibility to East Star's asset quality and management capability. Endeavour's position as a major East Star shareholder aligns the interests of a large, well-resourced mining company with those of smaller EAR investors.

- First-mover advantage in an underexplored jurisdiction: East Star has built a substantial proprietary database, digital archive of historic drill results, and in-country operational infrastructure that would take years and significant capital to replicate. The next 12–24 months of target generation and early-stage drilling across multiple prospects offers the potential for surprise discovery announcements.

- Copper price tailwind: With copper prices at elevated levels and structural demand from electrification and energy transition continuing to grow, a company with near-term copper production exposure and advanced exploration assets is well positioned relative to the commodity cycle. Walker noted the potential for copper at $20,000 per tonne by the time Verkhuba reaches first production, though investors should treat commodity price forecasts as illustrative rather than guaranteed.

TL;DR

East Star Resources (LSE:EST) holds a 30% free-carried interest in the Verkhuba copper deposit, funded to production by Xinhai Mining with first cash flow targeted by end-2028 at zero further cost to shareholders. Separately, Endeavour Mining is spending up to $25 million searching for a major gold deposit across two Kazakh belts, with East Star free-carried at 20% to prefeasibility. A portfolio of 100%-owned copper prospects provides additional optionality. The company offers near-term copper production exposure, major-funded gold discovery upside, and first-mover advantage in one of the world's most underexplored mineral jurisdictions, all without the ongoing dilution risk typical of junior explorers.

Macro Thematic Analysis: The Kazakhstan Opportunity

East Star Resources is shaped by two converging forces: long-term structural demand for copper driven by the global energy transition, and a significant undersupply of new copper and gold projects in the development pipeline globally.

Copper is central to the build-out of electric vehicles, grid infrastructure, and renewable energy generation. The International Energy Agency and major industry bodies have consistently projected that existing mine supply will be insufficient to meet demand through the 2030s and beyond without substantial new development. This creates a premium environment for companies with credible, near-term copper production assets. Verkhuba, with its JORC resource, Xinhai-funded development pathway, and a target production commencement of end-2028, sits within this demand window.

Gold continues to perform as a reserve asset and inflation hedge, with central bank accumulation at multi-decade highs. For gold explorers, the combination of elevated prices and increasing corporate M&A activity as mid-tier and major producers seek to replace depleting reserves which has created a favourable environment for discovery-stage assets. Endeavour Mining's expansion into Kazakhstan is itself a signal that the major gold producers are looking beyond traditional geographies to find new endowment.

Kazakhstan's positioning within this macro context is often under appreciated. The country holds the world's largest proven reserves of several minerals, and its copper and gold endowment anchored by world-class deposits such as Zhezkazgan, Aktogay, and Vasilkovskoye places it among the top tier of global mineral provinces. Yet its exploration expenditure remains a fraction of comparable jurisdictions such as Western Australia, creating genuine first-mover advantages for companies with established in-country presence.

That combination of world-class geology, low competition, and improving infrastructure makes Kazakhstan a macro thematic with significant longevity for investors in the resource sector.

Analyst's Notes

Subscribe to Our Channel

Stay Informed