Elixir Energy Drills Down Unconventional Large Unconventional Resource in Bullish Australian Market

Elixir Energy an ASX-listed gas explorer with large unconventional resource in Queensland, Australia, bullish macro, near-term farmout catalysts

- Elixir Energy recently completed an extensive appraisal well program in Queensland, Australia with mixed significant data gathered.

- The final well flow rate was lower than expected, likely due to operational issues, but the company believes the underlying geology is sound and the play is still attractive.

- Elixir is seeking farm-in partners to help fund future drilling; the company has a 15-year license and is not under immediate pressure to drill.

- Queensland natural gas prices are high at $12-15/GJ, 4x US prices, due to declining conventional production and LNG export demand.

- Elixir believes consolidation among smaller companies in the basin is likely. The company has additional conventional and Mongolian assets to help bridge to a major farm-in deal.

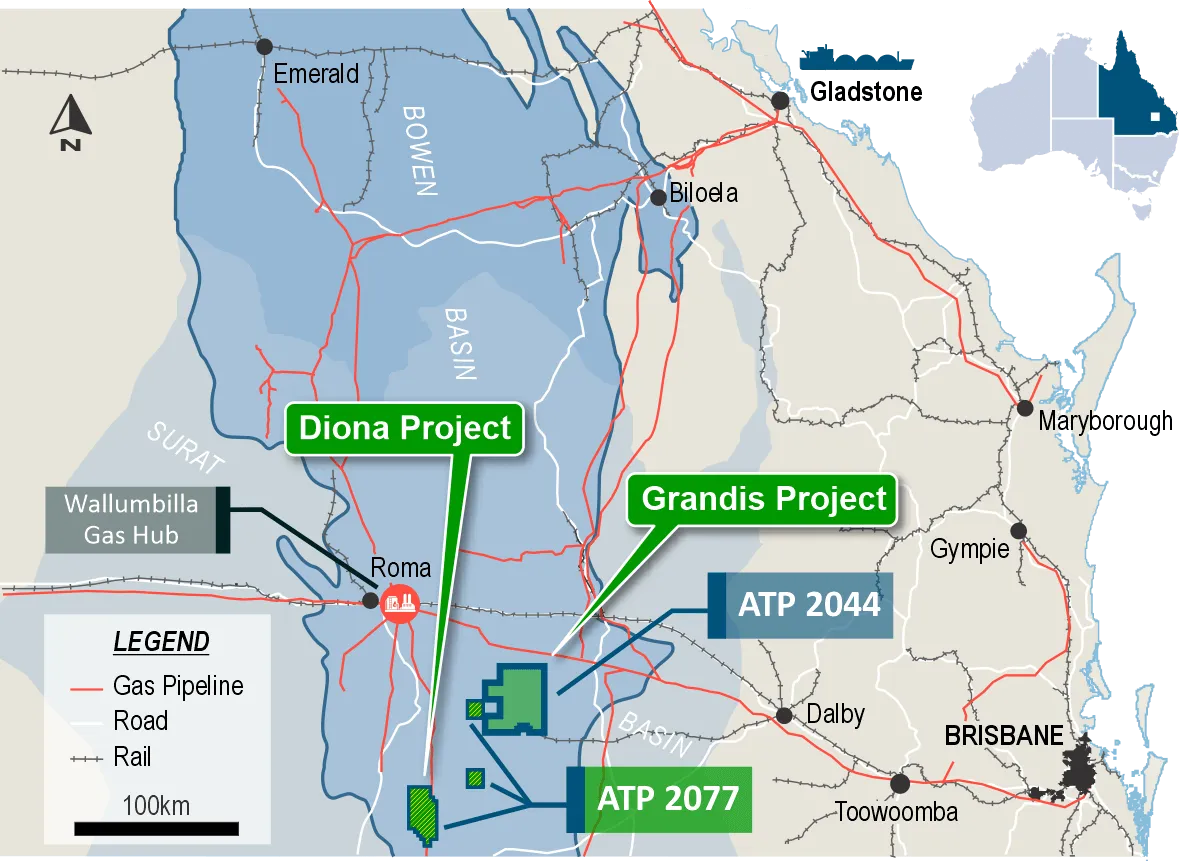

Elixir Energy is an ASX-listed gas company focused on a large unconventional gas resource in Queensland, Australia. The company recently completed an extensive one-year appraisal drilling program across its 100% owned acreage in the Bowen Basin. While the program had mixed results, significant valuable data was gathered that Elixir believes will be attractive to potential farm-in partners.

Drilling Results and Geological Potential in Queensland

The final appraisal well, which targeted the deepest and most prospective section, flowed gas from multiple zones but at a rate that was lower than expected. Elixir Managing Director Neil Young said the well encountered "a 600-meter thick Permian gas-bearing section" and "flowed five separate zones in that, sandstones and coals." Importantly, they also discovered a free-flowing zone that was unexpected. While the final flow rate was subeconomic at around 1 MMcf/d, Young attributed this to operational issues related to equipment availability and having to suspend the well for an extended period mid-completion. He is confident the underlying geology is sound.

"All of these things are remunerable by doing things more quickly, doing things in a different fashion," Young explained. "We are confident that if we had to drill exactly the same well tomorrow without interruptions, we would get a commercial flow rate and above."

Elixir believes the sub-optimal flow rate does not condemn the play. Young pointed to the experience in major US unconventional plays:

"People drill wells, they experiment, they find things out, they crack the code and then they end up drilling tens or hundreds of thousands of wells. We're at the pointy end of that journey just now."

With only a handful of wells drilled so far in this frontier play by Elixir and nearby operators like Shell, Young believes there are still many optimizations to be explored such as horizontal drilling, better stimulation and completion designs.

Farm-Out Process and Timeline

With the initial appraisal program complete, Elixir is now focused on bringing in an experienced partner to help fund the next phase of delineation and development. Young said they are talking to a range of potential partners from supermajors to large U.S. independent E&Ps. He expects the farm-out process to a major to take some time given the slower pace at which large companies evaluate deals. However, Elixir is not in a rush since the company now has appraisal drilling requirements to hold onto its acreage for 15 years.

In the meantime, Elixir is working on several smaller-scale farm-outs and asset sales to generate nearer-term cash flow. This includes a potential deal for its nearby conventional gas prospect and the possible sale of its legacy Mongolian coal bed methane asset. Elixir believes it has a strong track record of creating value through deal making and will continue to do so.

Interview with MD & CEO Neil Young

Bullish Macro Backdrop

A key part of the Elixir story is the extremely favourable macro setup for natural gas in Eastern Australia. The Queensland gas market is largely isolated from the rest of the country and is characterized by declining low-cost conventional production and growing LNG export demand from three facilities in Gladstone. As a result, domestic prices have skyrocketed to A$12-15/GJ, which is around 4x the US Henry Hub benchmark.

Young sees this supply shortfall persisting and expanding in the years ahead, necessitating the development of higher-cost unconventional supplies like Elixir's.

"The traditional sources of supply are in rapid and terminal decline," Young said. "And again, that's recognized widely and there's expected to be shortfalls within even within the next year or so."

LNG imports are one solution and several regas projects are in development. However, Young said imported volumes would likely be price around A$20/GJ. Unconventional supplies in Queensland would therefore be very competitive. Longer-term, Young believes the three LNG plants "ultimate developers" of plays like Elixir's. The plants have never reached capacity due to feed gas limitations, a problem that is only expected to worsen in the years ahead as legacy fields decline.

Risks and Uncertainties

To be sure, Elixir still has much to prove before its Grandis Basin acreage can be considered a commercial development. Additional appraisal drilling is needed to optimize the completion design and demonstrate the well performance and cost structure needed to attract a major partner. This will likely require Elixir to raise additional capital, which could be challenging in the current market environment.

There is also risk that the initial production rates from Elixir's wells to date are more indicative of reservoir quality than the company admits. If the geology proves to be inferior, securing an economic development could be very difficult regardless of the operator. Finally, the timeline and ultimate success of the farm-out process is still uncertain. Elixir may have to give up more of the project than it would like to secure a deal, limiting upside for shareholders.

Conclusion

While the initial drilling results from Elixir Energy's key Grandis Basin asset have been mixed, the company remains confident in the geological potential of its large acreage position. With an extremely tight gas market in Queensland and a 15-year appraisal license in hand, Elixir appears to have time on its side to continue derisking the play and bring in a larger partner to lead development. Securing a major farm-in deal in the coming months could be a major positive catalyst for the stock. However, investors should remain cautious given the early stage of appraisal. Additional data from future drilling will be key to watch.

The Investment Thesis for Elixir Energy

- Multi-TCF unconventional gas resource in highly prospective Grandis Basin

- Favorable Queensland gas market with A$12-15/GJ prices (4x US levels)

- Proven management team with track record of value creation via deal making

- Near-term catalysts: farm-out/asset sales, further appraisal drilling to optimize well design

- Potential very large upside if major partner secured to develop asset base

Actionable Advice:

- Suitable for risk-tolerant investors due to early-stage nature of appraisal

- Monitor catalyst path of farm-out process, additional drilling over next 6-12 months

Macro Thematic Analysis

The East Coast gas market in Australia is undergoing a structural shift as legacy conventional fields decline and LNG export demand continues to grow. This has created a significant gas supply shortfall in the region which has driven domestic prices to A$12-15/GJ, a huge premium to the US Henry Hub benchmark. This macro backdrop creates a highly compelling opportunity for companies like Elixir Energy that are exploring for new sources of supply.

While LNG imports could help fill the gap, Young expects those volumes to be prices around A$20/GJ. That means local unconventional developments would likely be very competitive. Longer-term, Young sees Elixir's acreage as a potential key feed gas source for Queensland's underutilized LNG export plants.

While this macro setup is very attractive, much still depends on the economic viability of Elixir's asset base. The company will need to demonstrate acceptable well productivity and cost structure to attract a major farm-in partner and make a development competitive in the global LNG market. However, for risk-tolerant investors, the significant price support in the East Coast market creates a potentially attractive reward/risk proposition.

Analyst's Notes

Subscribe to Our Channel

Stay Informed