Endeavour Silver (TSX-V: EDR) - Growth Incoming Despite Headwinds

Interview with Dan Dickson, CEO of Endeavour Silver (TSX: EDR, NYSE: EXK)

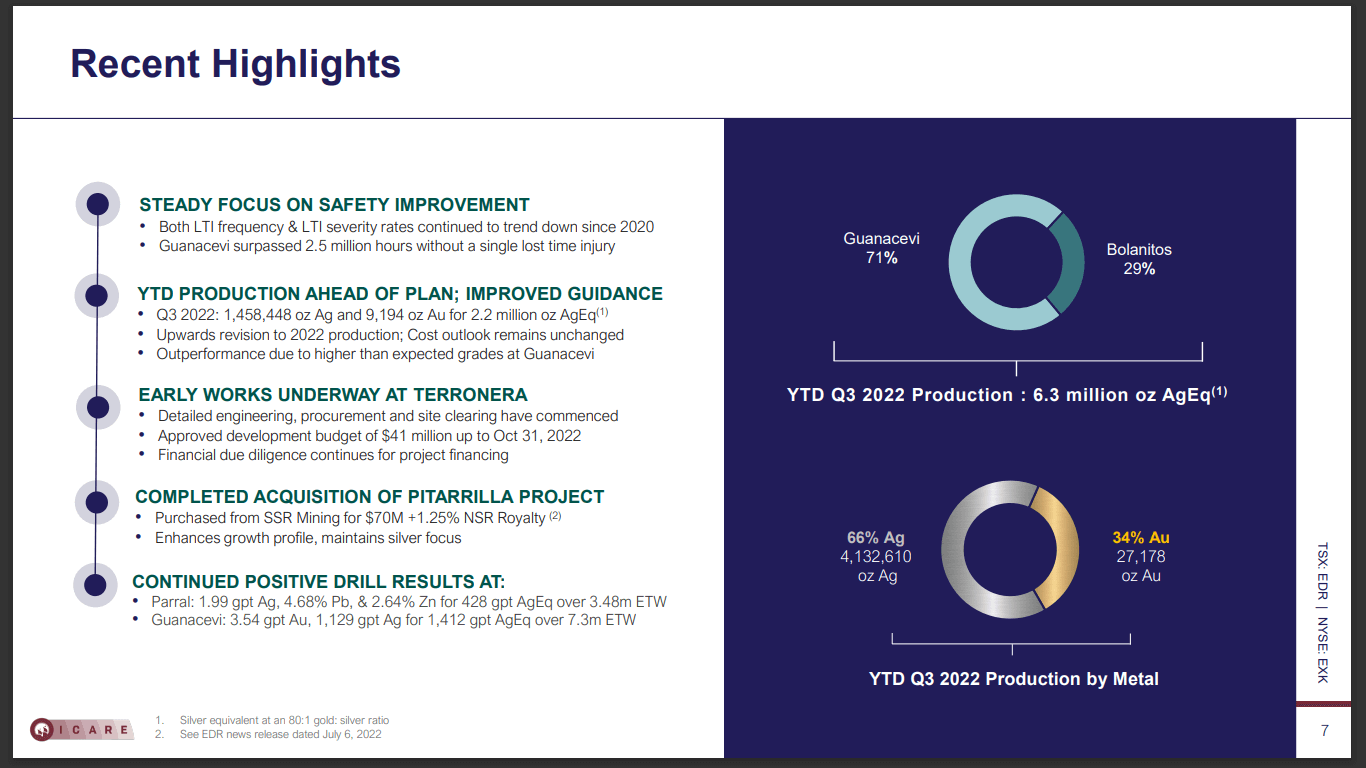

Endeavour Silver Corporation is a mid-tier precious metals mining company. The company produced 1,458,448oz silver and 9,194oz gold for 2.2M oz silver equivalent in Q3 2022. The company’s business strategy balances short-term profitability with long-term investments in exploration and development to extend mine lives and build new mines to drive future profitability. The company is focused on creating value for all its stakeholders. It is committed to sustainable production and aims to responsibly explore and manage its mining properties. It seeks to ensure the success of its people, the local communities, and its business.

Matt Gordon caught up with Dan Dickson, CEO, and Director, Endeavour Silver. Dan was appointed as CEO in May 2021 and is responsible for the company’s strategic direction, vision, growth, and performance, with a focus on creating shareholder value. In his previous role as CFO of Endeavour Silver, he was responsible for financial reporting, leading financing solutions, steering M&A (Mergers and Acquisitions), and overseeing the IT, legal, and administration functions. He also has a solid track record in supporting and guiding the company’s executive board. Dan has been instrumental in building Endeavour’s financial infrastructure as the company grew over the past 15 years from four employees to a team of more than 2,000. Prior to joining the company, Dan worked with KPMG LLP in the assurance group where he focused on publicly traded precious metal companies. Dan holds a Bachelor of Commerce Accounting from the University of British Columbia and is a member of the British Columbia Institute of Chartered Accountants (CPA, CA).

Company Overview

Established in 2004, Endeavour Silver Corp. is a mining company focused on discovering and mining silver, with projects and operations in three countries: Mexico, Chile, and the United States. The company’s purpose is to be a leading silver producer that creates value for its stakeholders by discovering, developing, and operating its mines in a sustainable way. It is listed on the Toronto Stock Exchange (TSX-V: EDR) and the New York Stock Exchange (NYSE: EXK). The company is headquartered in Vancouver, Canada. SSR Durango, S.A. de C.V., Recursos Villalpando S.A. de C.V., Guanacevi Mining Services S.A. de C.V., Terronera Precious Metals S.A. de C.V., Endeavour Management Corp, Minas Lupycal S.A. de C.V., Minera Plata Carina S.P.A., Endeavour USA Corp., Endeavour USA Holdings, MXRT Holdings Ltd., Servicios Administrativos Varal S.A. de C.V., Oro Silver Resources Ltd., Minera Santa Crux y Garibaldi S.A. de C.V., Minera Plata Adelante S.A. de C.V, Edr Silver De Mexico S.A. de C.V Sofom Enr, Minas Bolanitos S.A. de C.V, Metalurgica Guranacevi S.A de C.V., Endeavour Gold Corporation S.A. de C.V., and Recursos Humanos Guanacevi S.A. de C.V. are the company’s subsidiaries.

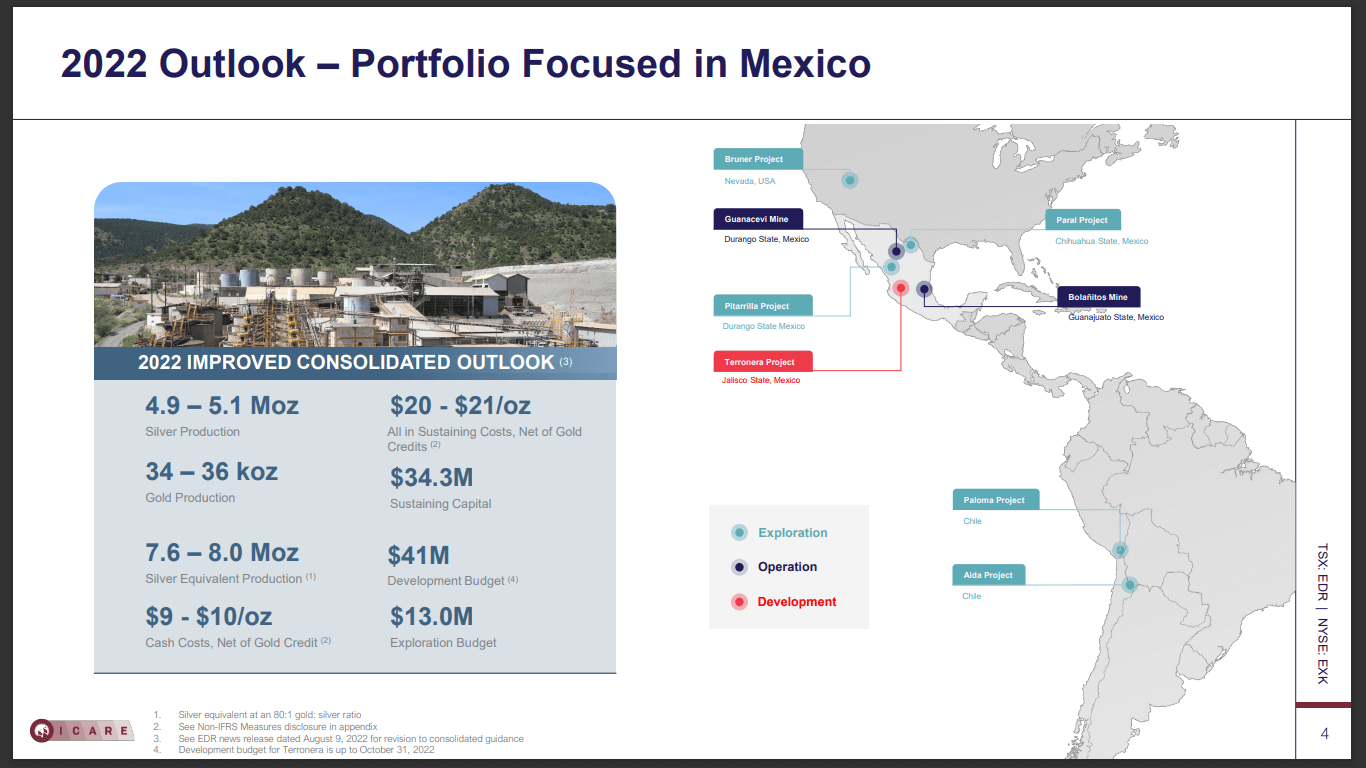

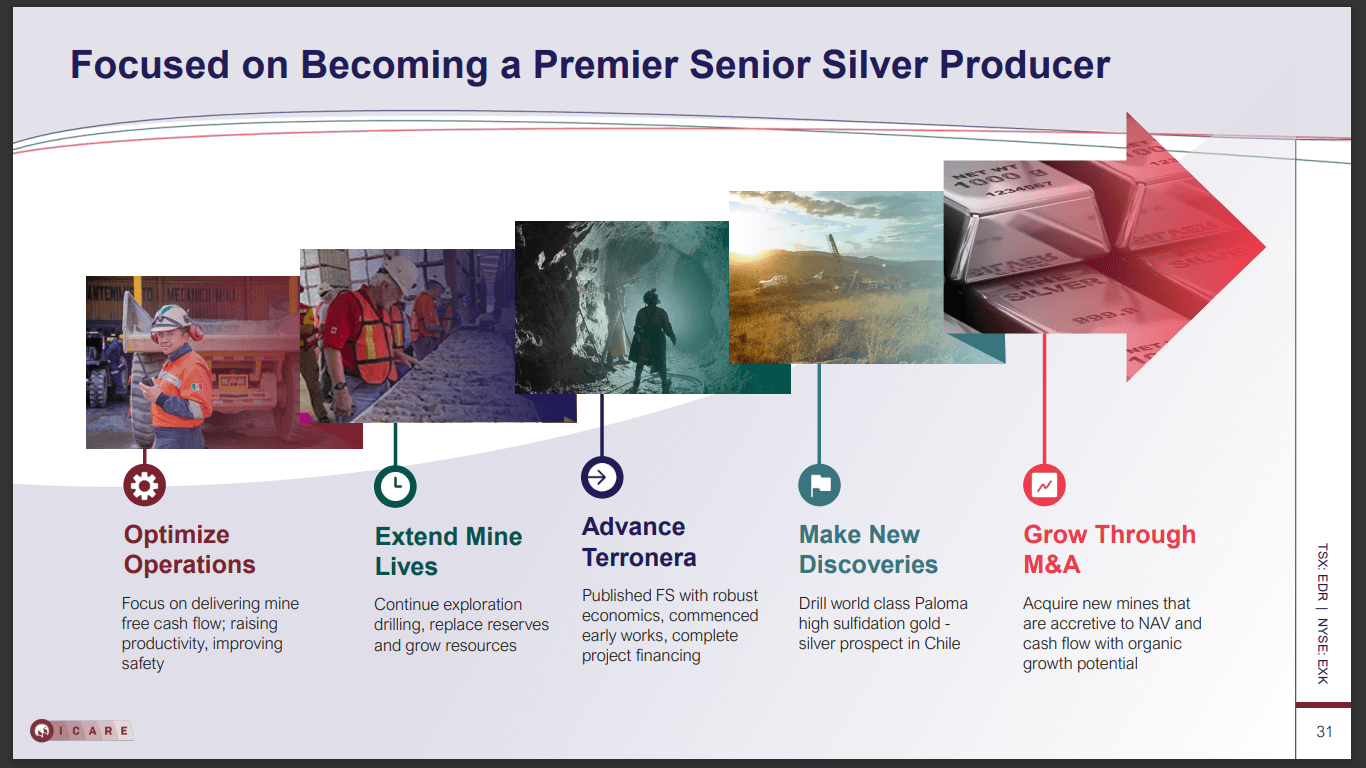

Endeavour Silver is a mid-tier silver producer with two main operating assets in Mexico that are producing about 8Moz/year silver equivalent. 60% of the company’s revenue comes from silver, while the other 40% comes from gold. The company is currently in a very important part of the cycle, as it seeks to bring its Terronera project online in the next 2 years. It is close to making a construction decision. For the past 2 years, the company has been focused on building out its pipeline, a highly compelling growth story.

Financial Considerations

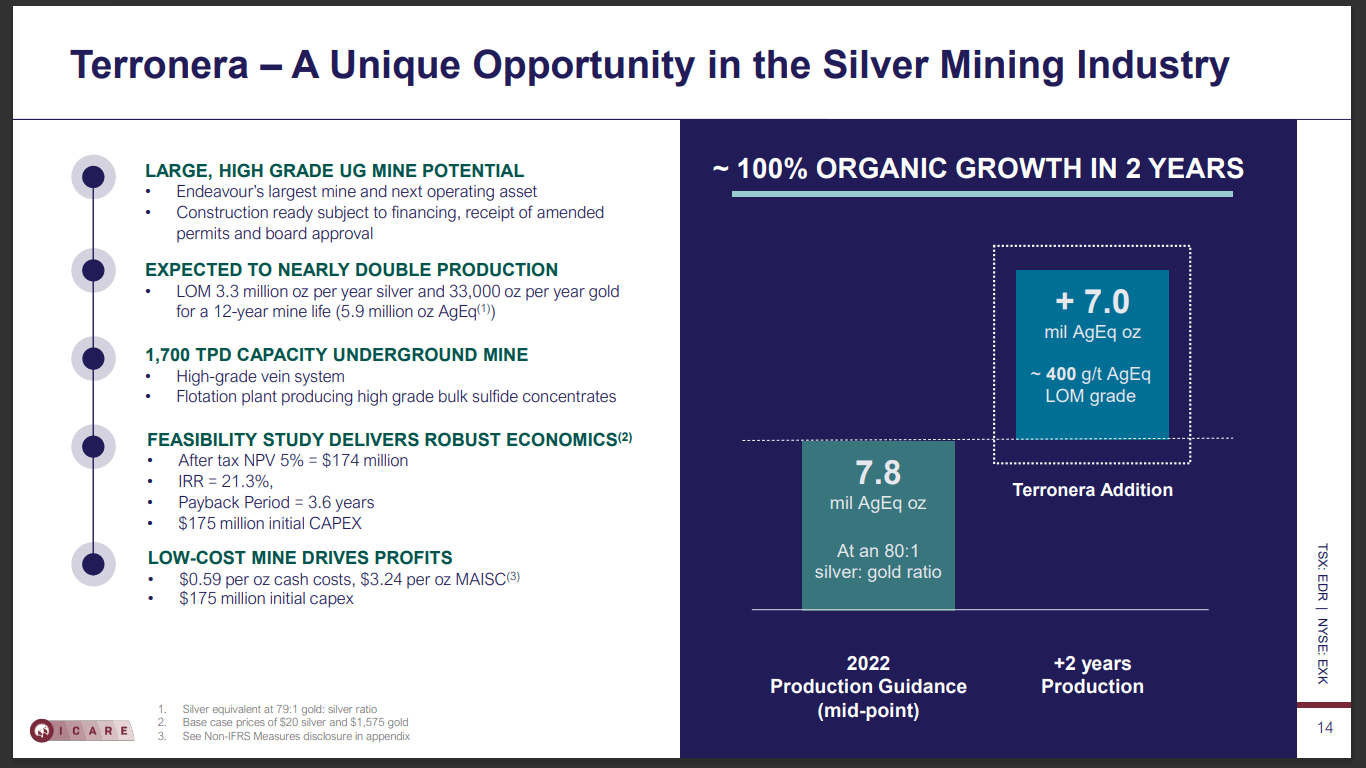

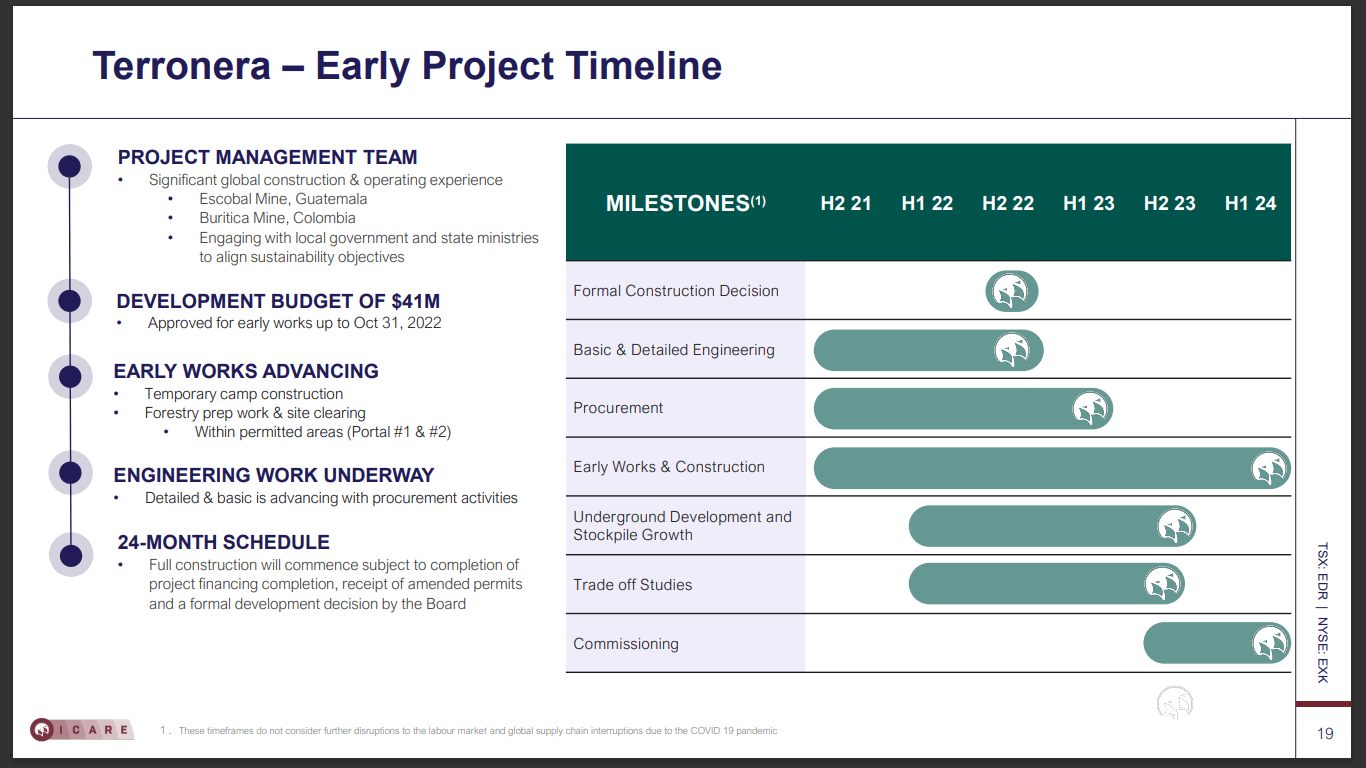

In mid-2021, Endeavour Silver published a Feasibility Study on its Terronera project located in Jalisco State, Mexico. The company has been working with commercial banks to acquire the lowest cost capital possible for the project.

The company continues to have a strong balance sheet. At the end of Q2, it had $155M in working capital with no long-term debts and limited leased mining equipment. In order to work with commercial banks, the company needs to get through a lot of regulations. The company has worked on its ESG (Environmental, Social, and Governance) documentation, and equator principles that qualify it for a commercial-level debt at the lowest cost of capital. The company anticipates that it will be able to reach the finish line and make a construction decision on Terronera by Q4, 2022.

Endeavour Silver has pushed the safety culture within the company, which has gone extremely well so far. In fact, the company was able to surpass 2.5 million man-hours at the Guanacevi asset with no LTI (long-term incidents). Before this, the company was able to achieve the same results for 2M hours. This demonstrates that the company has massively improved its culture from a safety and operating standpoint. The company has also maintained really good safety standards at the Bolanitos asset.

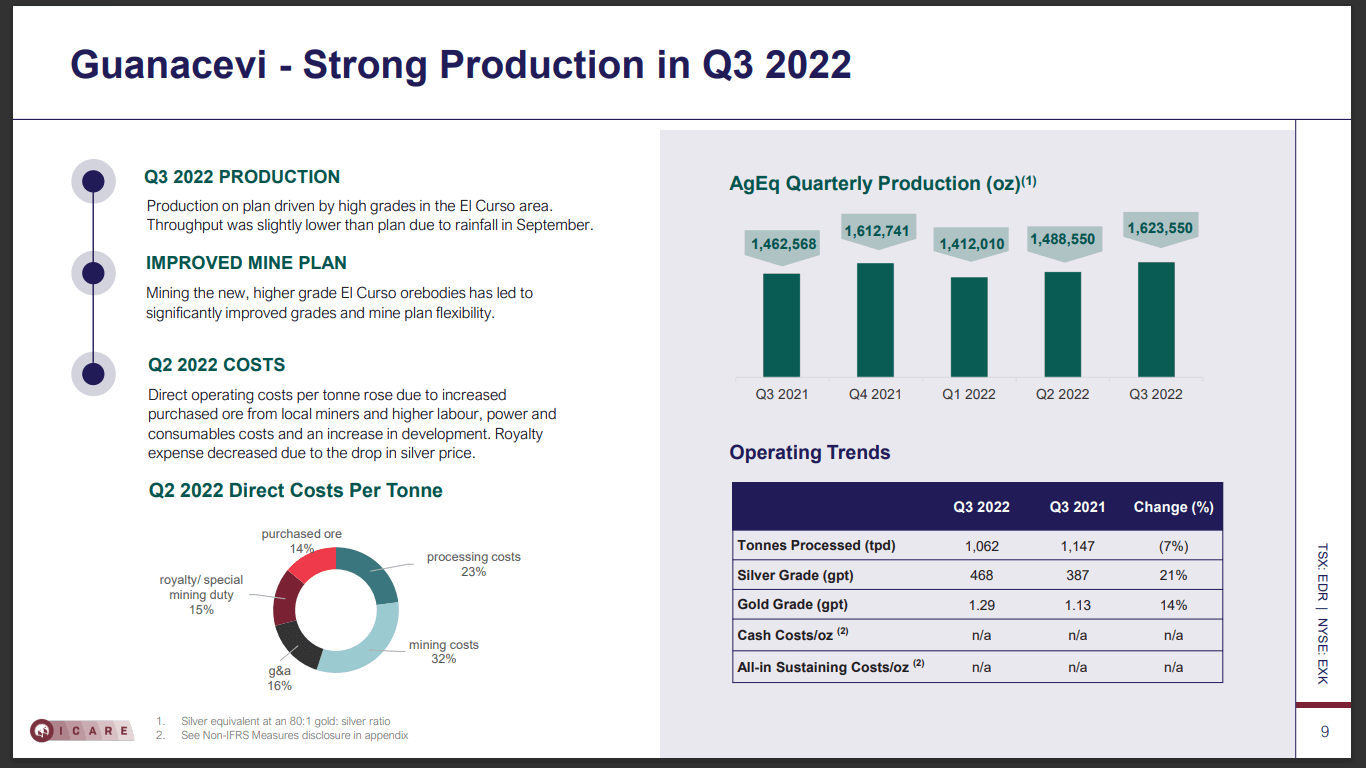

In 2020, the company revised its guidance upwards and it was able to surpass the production goals. In 2022, the company once again revised its guidance upwards. This showcases the company’s operational strategy and the grades it is getting out of the Guanacevi asset. The company has a strong team, and everyone is moving in the same direction.

According to Endeavour Silver, the market sentiment across the space and within the company goes with the silver pricing and the share price, both of which have seen improvements in recent times. As a management group, the company is focused on the long-term from a safety, offering, and development purview.

The share price serves as an internal barometer of success. It is important to note that the company also has other KPIs (Key Performance Indicators) to measure the business’ performance. The company focused on day-to-day activities that it can directly control, such as mocking a stope, blasting a stope, going over engineering reports, and redefining the ongoing work at the Terronera project. The company anticipates that if the internal aspects of the company are well-managed and taken care of, the share price will self-adjust over time.

The Impact of Inflation

Being in an inflationary environment, the company has seen cost increases in steel, energy, and wages. During such an environment, it is very difficult to control the costs, which can lead to probable risks in the macro environment. The company is focused on hitting targets to ensure that the production goals are met. In a case where the company can successfully exceed the set targets, the economies of scale will push that down. The company is focusing on energy, steel, and labour to ensure safe production.

In the short term, a company can potentially cut back costs on exploration and certain administrative activities, however, in the long term, the strategy is to bring in new assets that have a different cost profile. Interestingly, the current gold and silver market prices serve as a nice hedge against inflation. The company anticipates that the prices for both metals are going to increase further due to the current environment.

The Terronera project is going to be one of the lowest-cost assets in its space. In comparison to the company’s peers, the costs are expected to sit in the lowest decile from an AISC (All-in Sustaining Costs) standpoint. Both Guanacevi and Bolanitos are mature assets that are on the higher end of the cost curve. Compared to other primary silver producers, the company’s costs for these two projects are in the middle of the pack. Interestingly, the company’s AISC in the first half of 2022 has been slightly north of $20. Currently, the company has a $19/oz silver AISC. It is important to note that the company also has a significant royalty cost at Guanacevi, which is going to come down with time. While this is a part of the short-term cost measures, the company is breaking even.

The company is in active discussions with institutions for the long term. It is focused on managing the day-to-day, week-to-week, and quarter-to-quarter movement as a management team. The company’s vision is to bring assets with different cost profiles into its portfolio. The company anticipates that silver prices will be even higher in the future. It is currently working on controlling costs on an internal level from a business standpoint. This helps in bringing assets on a cost curve that is expected to be lower with time. Endeavour Silver is working on a budget for 2023 and is finalising the mining plans despite the market dynamics and volatility.

At the Guanacevi asset, the company is in a strong position. The project is well-advanced and features very high-grade areas. The company has the flexibility to increase production from the high-grade area based on market prices. While it has a lot of levers that can be pulled in order to generate free cash flow in the short term, it usually catches up. Between 2016 and 2018, the company reduced mine development, which enabled it to develop the mine in advance. This gave the company 2 years’ time worth of access to the ore. Though this move helped the company in improving its cash flow, it eventually caught up. At the Bolanitos asset, the company’s cost profiles are slightly at the higher end. The company has the option to cut development in the short term in order to improve the free cash flow.

As the company continues to step out, it realised that both assets have exceptional exploration potential. Notably, the company has been operating at Guanacevi for 17 years, and it has never had more than a 2-3 years reserve life. The company has continued to deplete resources, convert resources into reserves and find new resources. It is taking a similar approach at the Bolanitos asset as well. As both assets are mature, the company now has limited options when it comes to cutting costs.

Cash Position

At the end of Q2, 2022, Endeavour Silver had $115M in cash flow, out of which, deployed $35M to acquire the Pitarrilla asset. It has $80M in current cash flow.

Through October 31st, 2022, the company deployed a $41M budget at Terronera, which is currently being advanced. While the construction decision is yet to be made, there are a number of lead works that are already ahead of the lead time. Notably, 95% of the mobile equipment is already on-site. The company has also purchased a ball mill. It has already placed purchase orders for 12 key items that will be crucial for the plant’s operation. Purchases made in advance enabled the company to lock prices, saving costs from an inflation standpoint.

For the Terronera asset, the company is looking to acquire project loan financing. The Board is yet to give a development decision as the company is looking to acquire the entire $175M project CapEx (Capital Expenditure) in hand before deciding to build the mine.

In its current position, the company benefits from the project upside. Since it’s a 2-year bill, the delays make it hard to forecast whether the inflated costs will actually come down. While the company has locked in a lot of the equipment, the mine development is expected to be highly labour-intensive. It is looking to advance the project on time and within budget based on future cost estimations.

Following last year’s Feasibility Study, the company has been working on optimising the Terronera project. It has seen some inflationary pressure on various items. The resultant project is expected to be close to the Feasibility Study with some cost increases.

In its current position, the company’s balance sheet is healthy. While there aren’t a lot of levers that the company can pull off its balance sheet, it does hold a lot of bullion. As it gets closer to building the Terronera asset, the company is looking to sell off its inventory to build up cash balances as a short-term strategy.

The company does not have any long-term debts at the moment. It is looking to acquire $80-$100M in debt through a commercial bank at a low cost of capital in order to get cash on the balance sheet for Terronera. In the case of potential overruns, the company has the cash flow from its existing operations along with other options that it could possibly explore. It is looking to build the project on time and within the allocated budget. Notably, the company has already built a buffer into the balance sheet that factors in project loan financing.

Due to a dip in share prices, Endeavour Silver has faced a challenging year and a half. The shareholders have been highly supportive of the company. The company is cognizant that the share price movement is a function of silver pricing. Currently, the market sentiment is shifting towards lower silver prices. The company is regularly involved in discussions with the shareholders and institutions that are in favour of the company’s current direction. According to the company, the shareholders are excited about the Terronera project and its future potential. Overall, the shareholders have shown confidence in Endeavour Silver’s management team.

Targets 2022 and Beyond

Endeavour Silver is a 60% silver, 40% gold company. All of the company’s peers in the silver space have been acquiring gold assets in recent times. The companies also have base metals in their portfolio. Endeavour Silver has the best leverage on its stock price. In fact, it is rated almost 3:1 to silver.

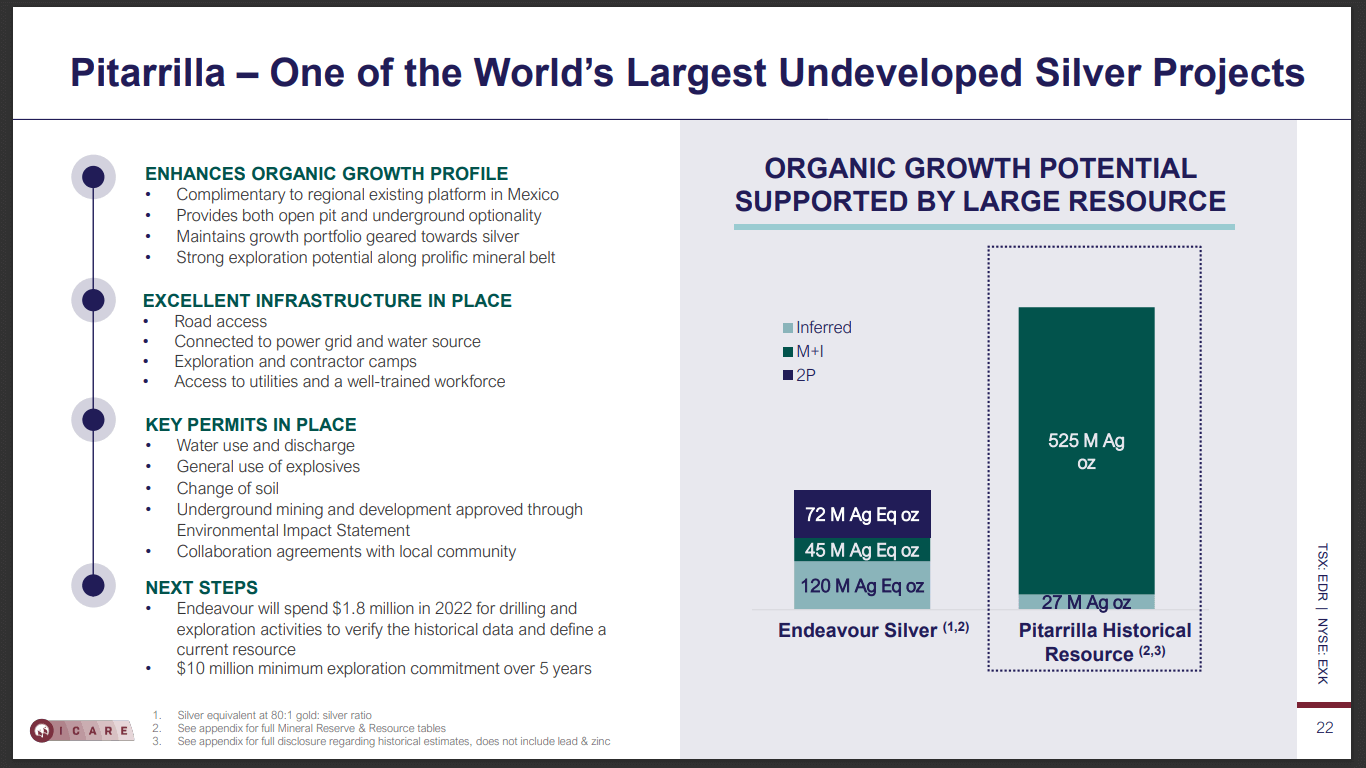

The company is working towards bringing its assets to the market. The Terronera project will take the company from 8Moz silver equivalent to about 15Moz silver equivalent. The company also has a growth profile following the acquisition of the Pitarilla project, one of the world’s largest undeveloped silver projects. Notably, the Pitarilla project has a historically-defined 525Moz silver resource.

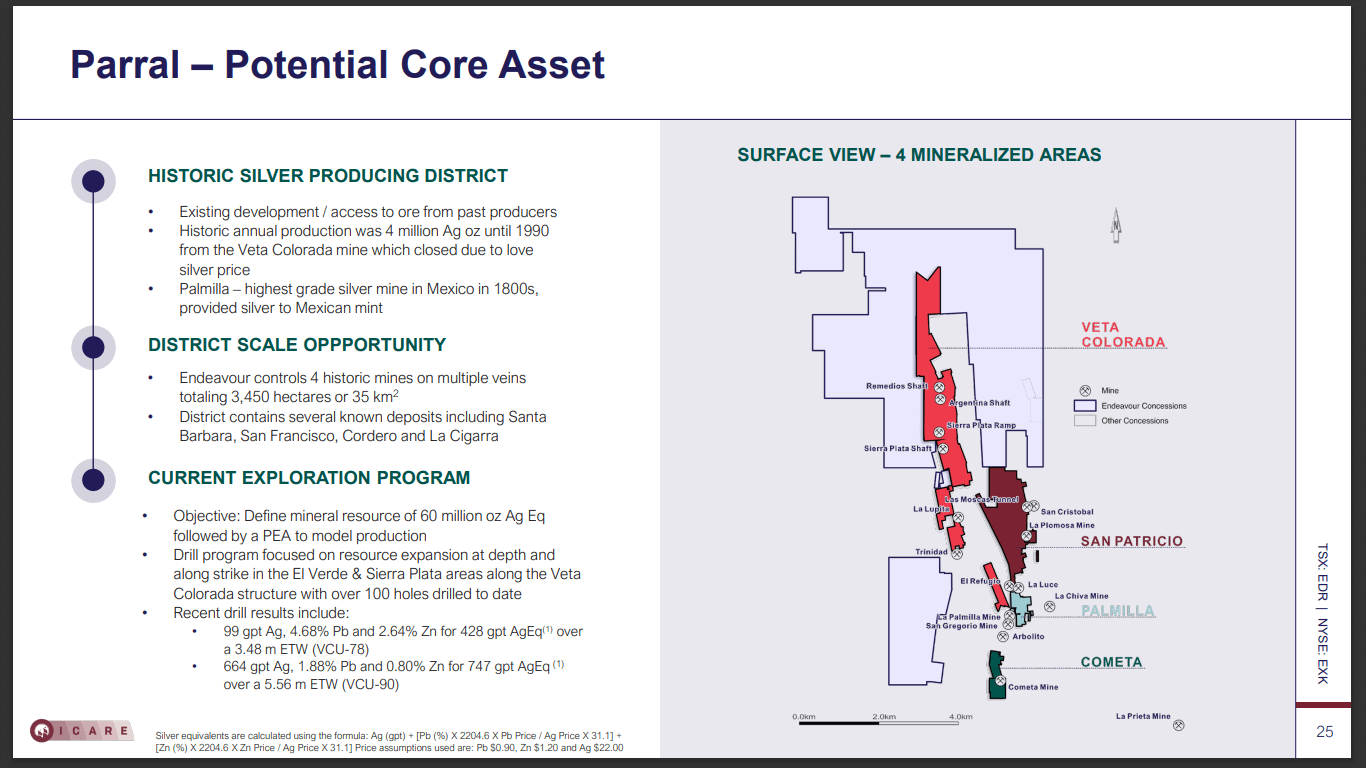

Endeavour Silver is also looking to grow the Parral project to 60Moz. This project comprises 90% silver and 10% base metals, providing a lot of optionality. Following the work on the Terronera project, the company is looking to work on either Pitarlila or the Parral asset. The company’s growth profile in the space remains unmatched. Its story resonates with people that anticipate higher silver prices in the future.

Endeavour Silver is cognizant that accretive growth is the ideal way to build a business. The company is focused on an 8-10 year growth plan. It realizes that silver prices will cause huge market volatility. In the past year-and-a-half, silver went down from $28 to $19. The company anticipates that silver prices would see an upward movement in the next year and a half, which would directly impact the company’s share price, helping it achieve rapid growth. The company seeks to continue managing the business through the highs and lows. While it is focused on slow and steady growth, the company is still open to the idea of quick growth achieved through increased silver market prices.

To find out more, go to the Endeavour Silver website

Analyst's Notes

Subscribe to Our Channel

Stay Informed