Fed Rate & Hormuz Blockade Compress Margins for Import-Dependent Salt Consumers While Favoring Domestic Supply

Salt's 2.30% CAGR masks margin compression from rising rates and shipping costs. North American projects with low costs gain advantages as legacy mines exit.

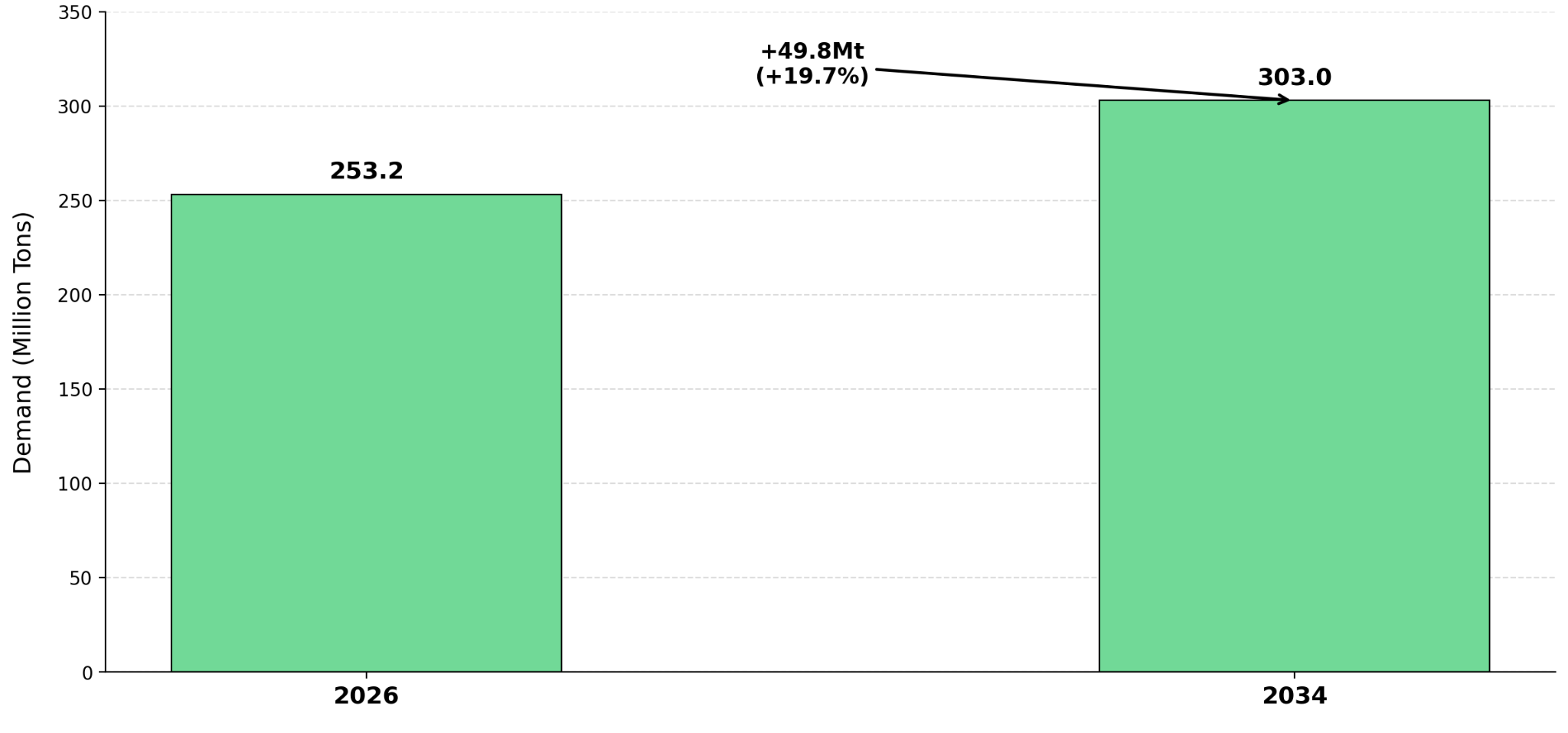

- Industrial salt remains a structurally stable but margin-sensitive commodity, with demand anchored in chlor-alkali chemicals, agriculture, and de-icing, supporting a projected $39.42 billion market by 2034.

- Elevated global interest rates - Federal Reserve effective rate at 3.64%, US 10-year Treasury at 4.34% - are increasing discount rates, forcing a reassessment of capital-intensive mining projects and favoring low-cost, high-margin assets.

- Geopolitical disruptions, particularly the US naval blockade targeting Iranian-linked shipping through the Strait of Hormuz, are exposing the fragility of global bulk commodity logistics, disproportionately impacting low-margin commodities like salt.

- A shift toward supply chain localization is emerging, with the EU steel import regime changes signaling policy direction that creates a premium for domestic production and import substitution strategies.

- Development-stage salt mining companies in top-tier mining jurisdictions with low all-in sustaining costs and proximity to North American markets demonstrate how cost structure and geographic positioning can provide competitive advantages under current macro conditions

Low-Margin Bulk Commodities Cannot Absorb Logistics Costs High-Value Metals Tolerate

In 2026, the Federal Reserve effective rate at 3.64%, and the US naval blockade targeting Iranian-linked shipping through the Strait of Hormuz are increasing discount rates and shipping costs for capital-intensive, logistics-sensitive bulk commodities.

Sodium chloride is the primary feedstock for the chlor-alkali process, which produces chlorine and caustic soda consumed in plastics (PVC), water treatment, paper, textiles, and industrial manufacturing. Demand of ~253Mt in 2026, anchored in these non-discretionary industrial applications supports a 2.30% compound annual growth rate through 2034, but delivered cost sensitivity to energy prices and shipping disruptions exposes margins to macroeconomic volatility.

For bulk commodities where transport costs can account for a significant portion of total delivered cost, shipping disruptions and energy price increases materially compress margins where higher-value commodities can absorb the same absolute cost increases.

Chlor-Alkali, Agriculture & De-Icing Anchor Non-Discretionary Demand

The chlor-alkali industry consumes salt as the primary feedstock for chlorine and caustic soda, which are deployed in plastics (PVC), paper, textiles, rubber, and water purification. Agriculture requires salt for irrigation systems, fungicides, and livestock nutrition. De-icing represents a critical infrastructure function in North America and Europe.

Nolan Peterson, Chief Executive Officer of Atlas Salt Inc. characterizes the customer base as non-discretionary:

"The primary customer for our salt is cities and governments. In many cases, they are legally obligated to purchase salt to deice roads for liability reasons. This is kind of the best customer anybody could ever ask for, that they're forced to buy your product."

Cities and governments, particularly in North America, are often legally obligated to purchase de-icing salt to maintain road safety, creating a customer profile with limited discretion and predictable offtake volumes.

Atlas Salt Inc., a development-stage project in Newfoundland, is targeting this North American de-icing market. The company has secured a memorandum of understanding with Scotwood Industries, the largest US distributor of packaged retail de-icing salt—for 1.25 to 1.5 million tonnes per annum. Nolan Peterson frames the supply dynamic:

"We aim to supply deicing road salt to the North American market and we will be the first new salt mine built in North America in 25 years."

The Constraint Is Not Demand - It's Delivery

The limiting factor in 2026 is not consumption, but how efficiently the supply reaches end markets. Transport can account for a significant portion of total delivered cost, shipping delays or fuel cost increases can materially compress margins, and long-distance imports introduce timing risk.

Geopolitical Disruptions & the Rising Cost of Moving Bulk Commodities

Geopolitics in 2026 is a direct driver of commodity cost curves, particularly for bulk materials where logistics represent a disproportionate share of delivered value.

The US naval blockade targeting Iranian-linked shipping through the Strait of Hormuz, initiated April 13, 2026, has increased insurance premiums for cargo vessels, extended shipping routes and transit times, and elevated fuel and freight costs. For bulk commodities like salt, these costs represent a disproportionately large share of total value.

Salt production and transportation are energy-intensive: mining operations rely on diesel and electricity, and shipping costs are directly tied to fuel prices. Shipping disruptions lead to rising input costs and lengthening delivery times.

Eco-Friendly Applications & ESG Mandates Create Distinct Market Impacts

Mining industry ESG frameworks favor operations that eliminate tailings through non-chemical processing, implementing closed loop water systems and utilizing renewable energy sources. These operational characteristics reduce regulatory risk exposure and align with institutional investor screening criteria, as financial institutions managing over $22 trillion in assets have adopted nature-risk screens and sustainability performance metrics.

Salt operations with clean production profiles, tailings-free extraction and renewable energy sources, position to meet these capital access criteria as mining sector ESG disclosure requirements tighten under GRI 14: Mining Sector 2024 standards, which became enforceable January 1, 2026.

Domestic Salt Capacity Faces 4.5 Mtpa Exit Risk While North America Imports 8-10 Mtpa Annually

According to American Rock Salt industry data, North America imports approximately 8 to 10 million tonnes per annum of de-icing salt. Legacy North American salt operations are aging: Goderich (producing since 1959), Detroit Salt Mine (since 1906), and Cayuga (since 1915). Cargill's Avery Island mine recently ceased production, removing 2.5 million tonnes per annum of supply, and Cargill's New York and Cleveland mines remain unsold due to environmental risks, threatening an additional 2 million tonnes per annum.

Commodity pricing risk remains material, as salt prices demonstrate a steady 4% compound annual growth rate since 2000, limiting upside leverage compared to higher-beta commodities. Cost inflation risk persists, as energy and labor cost increases may compress margins.

Financing risk is inherent to development-stage assets, which face dilution or debt pressure during capital raise and construction phases. Execution risk includes delays in permitting, construction, or production ramp-up.

The Investment Thesis for Salt

- Industrial salt demand anchored in chlor-alkali chemicals, agriculture, and de-icing provides resilience across economic cycles, but low unit value and high transport costs mean returns are determined by cost structure differentials rather than volume growth in a 2.30% CAGR market.

- Development-stage projects with internal rates of return above 20% and payback periods under five years maintain investment viability under the current 3.64% Federal Reserve effective rate.

- Geographic proximity to North American end markets reduces exposure to Strait of Hormuz shipping disruptions and provides 10+ day delivery time advantages over South American or Middle Eastern imports, translating to lower logistics costs and reduced supply chain volatility.

- Projects in top-tier mining jurisdictions (top 10 on Fraser Institute Policy Perception Index) with advanced permitting status reduce regulatory risk and timeline uncertainty, providing competitive advantages in capital raise and construction execution phases where development-stage assets face financing and dilution risk.

- Operations utilizing clean energy sources and eliminating tailings through non-chemical processing methods align with institutional ESG mandates, improving access to capital from investors subject to environmental reporting requirements and reducing long-term regulatory risk exposure.

Industrial salt in 2026 is a margin compression story where cost structure and supply chain positioning determine winners and losers. The commodity demonstrates how even stable, non-discretionary end-use demand cannot insulate low-margin bulk producers from rising capital costs and geopolitical logistics disruption.

In a higher-rate, supply-chain-constrained environment, proximity to end markets and capital efficiency become first-order competitive advantages. As monetary tightening and geopolitical fragmentation persist, the criteria for evaluating industrial commodities are shifting from volume growth to operational resilience and geographic positioning.

TL;DR

Industrial salt's 2.30% CAGR growth through 2034 masks a structural shift where returns depend on cost position, not volume. The 3.64% Federal Reserve rate and Strait of Hormuz naval blockade are compressing margins for bulk commodities unable to absorb rising logistics costs. North America imports 8-10 million tonnes annually while legacy mines face 4.5 Mtpa exit risk. Development-stage projects with sub-$50/tonne costs, proximity to North American markets, and clean production profiles gain competitive advantages as capital costs rise and supply chains localize. In 2026, industrial salt demonstrates how stable demand cannot protect low-margin producers from macro headwinds—cost structure and geographic positioning determine winners.

FAQs (AI-Generated)

Industrial salt has low unit value where transport costs represent a significant portion of delivered price. Unlike high-value metals that absorb logistics cost increases, salt margins compress when shipping disruptions or fuel prices rise. The 2026 Strait of Hormuz blockade exemplifies how geopolitical events disproportionately impact bulk commodities even when underlying demand from chlor-alkali, agriculture, and de-icing remains non-discretionary.

North America imports approximately 8-10 million tonnes per annum of de-icing salt according to American Rock Salt industry data. This import dependence creates supply chain vulnerability as legacy domestic mines age and exit production—Cargill's Avery Island removed 2.5 Mtpa, with an additional 2 Mtpa at risk. Domestic production gaps create opportunities for new low-cost projects with geographic proximity advantages.

Cities and governments in North America are legally obligated to purchase de-icing salt for road safety and liability reasons. This creates a customer base with predictable offtake volumes and limited purchasing discretion, providing demand stability across economic cycles unlike discretionary commodity markets subject to demand destruction during downturns.

The Federal Reserve's effective rate at 3.64% and US 10-year Treasury at 4.34% increase discount rates applied to future cash flows, making capital-intensive mining projects less attractive unless they demonstrate high returns. Development-stage salt projects require internal rates of return above 20% and payback periods under five years to maintain investment viability under these elevated cost-of-capital conditions.

Proximity reduces logistics costs, eliminates exposure to Strait of Hormuz shipping disruptions, and provides 10+ day delivery time advantages over South American or Middle Eastern imports. For bulk commodities where transport represents significant delivered cost, shortened supply chains directly improve margins and reduce volatility from fuel price fluctuations and geopolitical events affecting global shipping routes.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

Stay Informed