Atlas Salt & the Value of its Great Atlantic Salt Project

Atlas Salt's Great Atlantic Salt Project carries a C$920M NPV8 against a C$95.5M enterprise value. CEO Nolan Peterson explains why the gap may signal mispricing.

- Atlas Salt's 2025 Updated Feasibility Study (UFS) delivers an after-tax net present value at 8% discount rate (NPV8%) of C$920 million against a current enterprise value of approximately C$95.5 million, implying a price-to-NAV ratio of roughly 0.1x.

- The Great Atlantic Salt Project holds 95 million tonnes of probable reserves grading 95.9% sodium chloride, with a 24.3-year mine life on reserves and potential for more than 50 years of production based on 868 million tonnes of inferred resource.

- Life-of-mine (LOM) average annual free cash flow (FCF) of C$188 million and average annual earnings before interest, taxes, depreciation, and amortisation (EBITDA) of C$325 million underpin a capital return strategy that targets more than 90% of FCF for shareholder returns once debt is retired in production years 9 to 24.

- North America imports 8 to 10 million tonnes of deicing salt annually, and no comparable new mine or expansion project is currently planned on the continent, positioning the Great Atlantic Salt Project's 4 million tonne per year nameplate capacity against a defined supply gap.

- Project financing remains the primary outstanding risk, with Endeavour Financial engaged for advisory and first production targeted by 2030 at a pre-production capital expenditure (capex) of C$589 million.

A Different Kind of Mining Asset

Atlas Salt’s (TSXV: SALT) The Great Atlantic Salt Project in western Newfoundland is not a typical resource sector play, and Chief Executive Officer of Atlas Salt, Nolan Peterson, states that treating it like one is the source of the valuation gap. The 2025 Updated Feasibility Study (UFS), completed in September 2025, puts the after-tax net present value at 8% (NPV8%) at C$920 million, with an after-tax internal rate of return (IRR) of 21.3% and a 4.2-year payback period. The project's current enterprise value sits at approximately C$95.5 million, implying a price-to-NAV ratio of roughly 0.1x.

The gap exists because the standard discount applied to mining projects reflects risks that are materially reduced for salt. Salt deposits require no metallurgical processing, no chemical processing, and produce a homogeneous, high-purity product. The Great Atlantic Salt deposit grades at 95.9% sodium chloride across 95 million tonnes of probable reserves, with an additional 868 million tonnes of inferred resource that the company believes could extend mine life well beyond 50 years. Environmental assessment (EA) was completed in April 2024 after roughly two months of provincial review, a timeline that reflects a project with minimal land use, no tailings, and Scope 1 greenhouse gas emissions of just 79 tonnes per year.

Why the Lassonde Curve Understates the Case

Peterson used the Lassonde Curve, the mining industry's standard framework for visualising how project valuations progress from discovery through production, as a starting point, but pushed back on its direct application to Atlas Salt. The curve's implied discount reflects block model uncertainty, metallurgical risk, permitting risk, and financing risk. Peterson's position is that the first three are materially reduced in the case of salt, leaving project financing and construction execution as the primary remaining variables.

Peterson, addressed the disconnect directly:

"If you remove those risks from the equation, the valuation should be much higher. We should be further advanced on the curve as a visual representation."

The company reinforces the point through comparable transaction data. When K+S sold its Americas salt assets to Stone Canyon Industries in 2020, the transaction closed at US$3.2 billion, representing 12.5x 2019 earnings before interest, taxes, depreciation, and amortisation (EBITDA). Against Atlas Salt's life-of-mine (LOM) average EBITDA of C$325 million, that multiple would imply a substantially higher valuation than what the current NPV-based framework produces. Compass Minerals, the one publicly traded salt producer, trades at 8.7x last-twelve-months EBITDA. Peterson stated that Atlas Salt should be valued at these multiples today, but that investors accustomed to NPV-based mining valuations may be applying the wrong framework entirely.

The Cash Flow Profile That Changes the Comparison

Where the salt project diverges most clearly from a conventional gold or copper mine is in the shape of its cash flow profile over time. A typical hard-rock mine produces front-loaded value: capital is spent, the reserve is extracted, and net asset value declines steadily as production consumes the resource. Investors must account for reinvestment risk and commodity price exposure over the full mine life.

Atlas Salt's LOM average annual free cash flow (FCF) of C$188 million, sustained over a 24.3-year mine life on current reserves alone, reduces both of those concerns. Salt prices have compounded at approximately 4% annually since 2000, according to data from the United States Geological Survey.

Peterson highlighted how stable the salt market has been, noting:

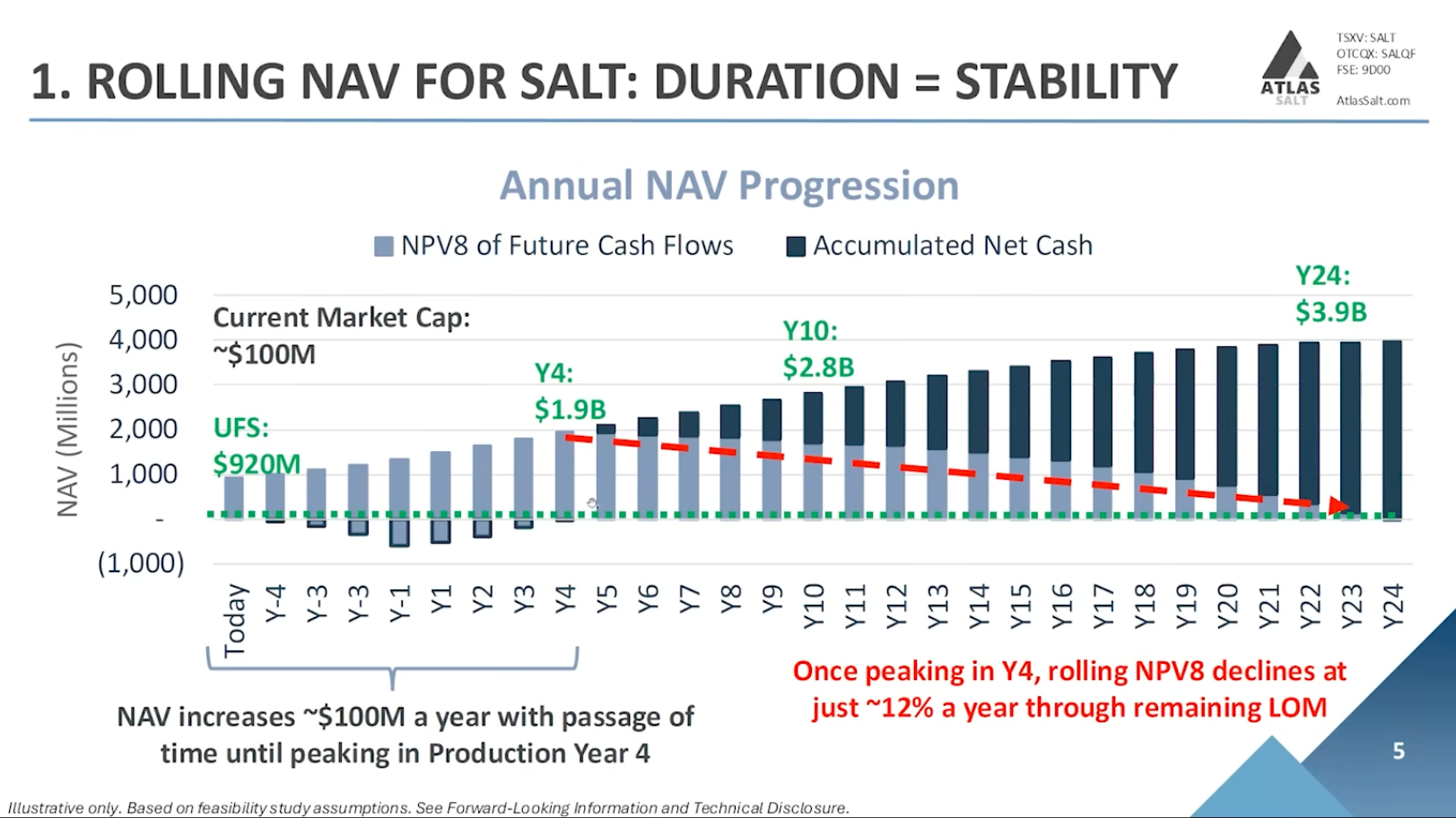

“What we bring is stability to the project, to these types of cash flows. We show a peaking of NAV ($1.9 billion) in year 8. This is our initial capital, and then the initial years of construction or operation as we ramp up. Then our NPV peaks, and then you see a shallower decline. We're not extracting as much value because we have a 25-year mine life.”

The presentation models a capital return strategy that reflects this durability. In production years 1 through 8, the company targets allocating 50% of FCF to debt repayment and 50% to shareholder returns. From year 9 onward, once debt obligations are satisfied, more than 90% of FCF, averaging approximately C$183 million annually, is targeted for dividends or buybacks.

Market Structure Supports the Supply Case

The investment case does not rest on valuation methodology alone. North America currently imports 8 to 10 million tonnes of deicing salt annually, sourced primarily from Egypt, Chile, and the Caribbean. The Great Atlantic Salt Project's nameplate production capacity of 4 million tonnes per year targets a defined import gap rather than displacing domestic production.

In January and February 2026, municipalities across Ontario reported salt shortages and wholesale price increases from $65 or $70 a tonne to almost $190 a tonne. Cargill's Avery Island mine in Louisiana closed in 2021, removing 2.5 million tonnes of annual domestic supply. Cargill's remaining assets in New York and Cleveland have remained unsold since a 2023 sale process began. No comparable new mine or expansion project is currently planned in North America.

Atlas Salt has signed a non-binding memorandum of understanding (MOU) with Scotwood Industries, targeting offtake volumes of 1.25 to 1.5 million tonnes per year. A separate non-binding MOU with Sandvik covers mining equipment and engineering support valued at C$132 million. The project site sits approximately 2 kilometres from the Turf Point deep-water port, with less than 3 days' shipping time to Boston, compared to more than 14 days from competing import sources.

What Needs to Happen Next

Peterson acknowledged that the valuation argument only closes when project financing is secured. Endeavour Financial has been engaged for project finance advisory. The company is targeting first production by 2030, with pre-production capital expenditure (capex) of C$589 million. Insider ownership sits above 40% of basic shares outstanding, which were 110.7 million as of March 2026. The case Peterson is making is not complicated: a long-life, low-risk, infrastructure-like asset is being priced like a speculative mining exploration company. Whether the market accepts that reframing depends on whether the financing package, when announced, validates the risk profile the company has been describing.

FAQs (AI-Generated)

The 2025 UFS puts the after-tax NPV8% at C$920 million, with an after-tax IRR of 21.3% and a 4.2-year payback period. LOM average annual FCF is C$188 million, and average annual EBITDA is C$325 million over a 24.3-year mine life on current reserves.

Peterson stated that the standard discount applied to mining projects reflects metallurgical, block model, and permitting risks, all of which are materially reduced for the Great Atlantic Salt Project, given its processing simplicity, completed EA, and homogeneous deposit. With those risks reduced rather than eliminated, the company argues it should be valued further along the Lassonde Curve than its current 0.1x price-to-NAV ratio suggests.

A typical gold or copper mine produces front-loaded value that declines as the reserve is extracted, requiring continuous capital recycling and exposure to commodity price volatility. Atlas Salt's C$188 million annual FCF is sustained over 24.3 years on current reserves, with salt prices compounding at approximately 4% annually since 2000.

North America imports 8 to 10 million tonnes of deicing salt annually. Ontario municipalities reported wholesale price increases from $65 or $70 a tonne to almost $190 a tonne in early 2026, and Cargill's closure of its Avery Island mine in 2021 removed 2.5 million tonnes of annual domestic supply. No comparable new mine or expansion is currently planned in the region.

The primary outstanding milestone is securing a project financing package, for which Endeavour Financial has been engaged. The company has already completed its FS, EA, and early works development plan. Strategic agreements in place include a non-binding Scotwood Industries offtake MOU targeting 1.25 to 1.5 million tonnes per year and a non-binding Sandvik equipment and engineering support MOU valued at C$132 million. First production is targeted by 2030.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed