North America's 25-Year Salt Supply Gap: Why New Mines Haven't Been Built

Closures and environmental issues at legacy salt mines have blocked new salt mine development for 25 years, driving import dependency and wholesale price spikes in Ontario.

- North America consumed between 28.5 and 36 million tonnes of de-icing salt per year, yet the continent has not opened a new salt mine since 2001, a supply gap now filled by 8 to 10 million tonnes per year of imports from Chile, Egypt, Mexico, and the Caribbean.

- The legacy supply base is ageing and contracting: Cargill permanently closed its Avery Island mine in 2021, removing 2.5 million tonnes per year of domestic production, while its remaining New York and Cleveland assets have remained unsold since 2023 due to environmental risks, with closure threatening a further 2 million tonnes per year of supply.

- Capital intensity, logistics barriers, and environmental permitting complexity have operated in combination to make new-build salt mines in North America economically unattractive, with most accessible geology sitting beneath lakes and waterways.

- Wholesale road salt prices in Ontario spiked from $65 or $70 a tonne to almost $190 a tonne during the 2025 to 2026 winter season, with shortage reports documented across Eastern Ontario by CBC News, CTV News, and CityNews Toronto.

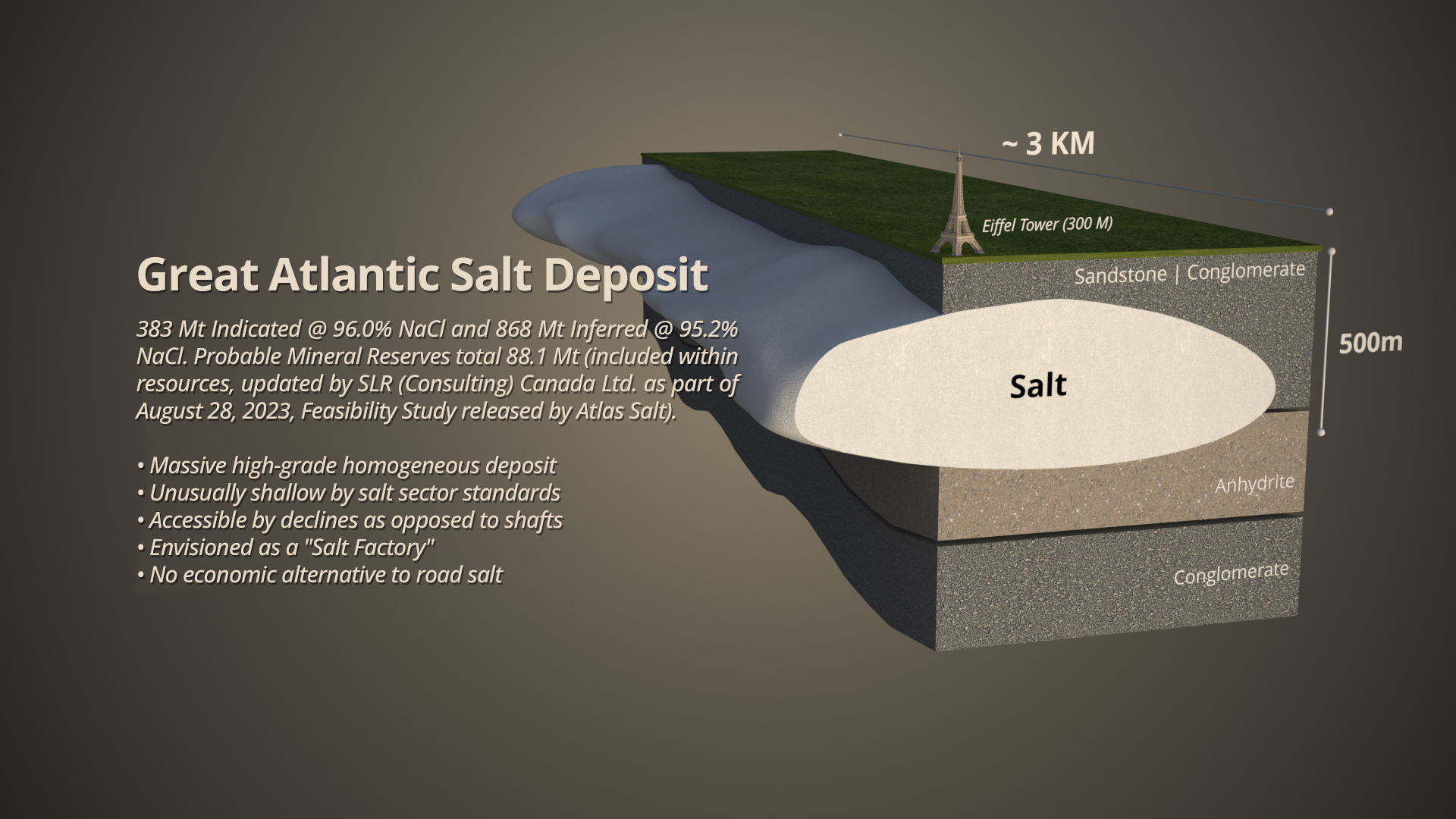

- A development-stage salt project publicly advancing in North America is the Great Atlantic Salt Project in Newfoundland, Canada, which is designed around geological and logistical characteristics that differ from legacy operations and is targeting commercial production by 2030.

A Generation of Deferred Supply

North America has not built a new salt mine in 25 years, and the market is now absorbing the cost of that deferred supply. De-icing salt is among the most operationally critical commodities in winter infrastructure, yet the supply base serving it has added no new domestic capacity since 2001. The global salt market was valued at US$26 billion in 2024, according to Fortune Business Insights, with the North American de-icing segment consuming between 28.5 and 36 million tonnes per year, based on the base salt price of $81.67 per tonne cited in the 2025 Updated Feasibility Study (UFS) for the Great Atlantic Salt Project. Rock salt prices in the US have compounded at approximately 4.2% per year since 2000, according to US Geological Survey data.

The last new salt mine to open was American Rock Salt's Hampton Corners Mine in New York in 2001, the newest mine to open in over 50 years at the time. This supply gap has been highlighted by recent shortage headlines and price spikes.

Industry Context

The mines supplying most of North America's de-icing salt were built in the mid-twentieth century and share a defining characteristic: they are deep, they sit beneath waterways, and they carry ongoing environmental risk that has made divestiture and expansion increasingly difficult. The Goderich mine in Ontario, operated by Compass Minerals and the largest on the continent at 7 to 9 million tonnes per year, sits approximately 600 metres beneath Lake Huron and has been producing since 1959. The Cayuga Salt Mine in New York, operated by Cargill, runs approximately 700 metres below Lake Cayuga, with production in the area tracing to 1915. The Ojibway Mine in Windsor, Ontario, operates at roughly 250 metres beneath Lake Erie and has been producing since 1955.

The K+S Americas salt assets, including Morton Salt and Windsor Salt, were sold to Stone Canyon Industries Holding in 2020 for US$3.2 billion, representing 12.5x 2019 earnings before interest, taxes, depreciation, and amortisation (EBITDA). That transaction reflects the scarcity of existing permitted operations in a market that has not added new capacity in a generation.

The Three Barriers That Blocked 25 Years of New Supply

Three constraints have operated in combination to prevent new salt mine development across North America.

Chief Executive Officer of Atlas Salt, Nolan Peterson, addressed this directly:

"It's a relatively low-margin product, bulk tonnage, low margin, high cost, and environmental challenges from new mines because they tend to be under lakes and waterways and very deep as well."

Capital intensity is the primary constraint. Salt is a low-priced bulk commodity. The 2025 base salt price of $81.67 per tonne reflects the thin margin environment that makes pre-production capital expenditure (capex) of $589 million difficult to justify without a deposit geometry that avoids costly shaft sinking. The Great Atlantic Salt Project's deposit is accessible via a decline at approximately 180 metres depth, illustrating the cost differential when sub-lake shaft requirements are removed from the equation.

Logistics creates a separate and compounding barrier. End market proximity results in lower-cost transportation and reduced capital and operating expenditure. A new mine without access to established road, port, and electricity infrastructure faces significantly higher costs to reach end markets and those logistics investments are difficult to justify without long-term contracted offtake, which itself is difficult to secure before a mine is built.

Environmental permitting introduces a third and distinct constraint. The closure of Cargill's Avery Island mine and the stalled divestiture of its remaining assets due to environmental risks have reinforced regulatory caution around new approvals in similar geological settings, extending timeline and cost uncertainty for any project attempting to develop comparable geology, independently of the capital and logistics hurdles it also faces.

What 25 Years Without a New Mine Has Cost the Market

The closure of Cargill's Avery Island mine removed 2.5 million tonnes per year of domestic supply to the US East Coast de-icing market. Its remaining assets in New York and Cleveland have remained unsold since the 2023 sale process began, with a potential closure threatening a further approximately 2 million tonnes per year of supply. The result is a continent that imports 8 to 10 million tonnes per year of de-icing salt, predominantly from Canada, 29% of US imports from 2020 to 2023, Chile 27%, Mexico 14%, and Egypt 8%, with a total of 67.5 million tonnes imported to the US alone over those four years.

The public safety consequences became visible during the 2025 to 2026 winter season. Wholesale road salt prices in Ontario spiked from $65 or $70 a tonne to almost $190 a tonne, according to CityNews Toronto reporting from January 2026. CBC News documented shortages across Eastern Ontario municipalities in February 2026, and CTV News reported more than 100 empty delivery trucks with Canadian salt being redirected to US buyers. In New York, the decision not to implement the Buy American Salt Act preference in a new contract was based on many factors, including shortages experienced the prior winter. These shortages and price increases highlight the fragility of existing supply and the need for additional capacity.

Emerging Development Models

A rare example of a project attempting to address these constraints highlights the conditions that appear necessary to make a new salt mine viable in the current environment. One of such is the deposit geometry that allows decline access rather than costly shaft sinking, supports rapid development and reduces upfront costs. Proximity to established deep-water port infrastructure reduces capital and operating expenditure, and access to established road, port, and electricity infrastructure is cited as a direct cost advantage. A short environmental approval pathway helps reduce timeline risk. In Newfoundland and Labrador, the Great Atlantic Salt Project was released from the provincial environmental assessment process in April 2024 after roughly two months of review. Projects of this type are likely to rely heavily on debt financing and long-term offtake visibility, reflecting the infrastructure-like nature of the asset class.

The Great Atlantic Salt Project in Newfoundland, Canada, operated by Atlas Salt (TSXV: SALT)is one example attempting to align with these conditions. Early works construction has commenced following government approval of an early works package, with the company targeting commercial production by 2030. Whether a project meeting these conditions can be financed and constructed on that timeline remains the open question the current development cycle will test.

Regional & Jurisdictional Context

Where a deposit is located determines what permitting pathway it faces, what infrastructure it can access, and how far its product must travel to reach end markets. Those differences are material for assessing where a new domestic supply could realistically emerge.

In the US, the political appetite for domestic supply is clear. New York declined to enforce the Buy American Salt Act preference in a 2025 procurement decision specifically because shortage conditions made import reliance unavoidable. That decision reflects a market reality where domestic supply has not kept pace with demand.

The eastern Canadian seaboard presents a different set of conditions. Atlantic Canada, Quebec, and the US East Coast consume an estimated 11 to 16 million tonnes per year of de-icing salt. Newfoundland & Labrador was ranked 9th globally by the Fraser Institute's 2025 annual survey of mining investment attractiveness based on mineral content and government policy alignment. For Atlas Salt’s Great Atlantic Salt Project, these regional characteristics translate into a clear logistical and sustainability advantage. The province's west coast geography provides coastal access that shortens delivery distances to northeastern US and Atlantic Canadian markets to less than 3 days to Boston, compared to more than 14 days from Egypt or Chile. End market proximity minimises the cost, insurance, and freight spread that disadvantages overseas imports, while access to clean hydroelectric power supports a fully electric mine operation, reducing both operating costs and the carbon footprint of production relative to fossil-fuel-dependent alternatives.

Industry Outlook

North America's de-icing salt supply gap is structural. Closures at legacy operations have reduced domestic production, and no new capacity has replaced what has been lost. The import dependency that has filled that gap is not a temporary condition, and there is no self-correcting mechanism at current commodity prices.

The open question is whether a viable new build can be financed and executed at scale. The conditions that have prevented new development for 25 years, capital intensity, logistics barriers, and environmental permitting complexity, have not changed. Atlas Salt’s Great Atlantic Salt Project is now attempting to demonstrate they can be navigated. Whether it succeeds will determine whether North America's salt supply gap narrows or deepens further as legacy mines continue to age.

Analyst's Notes

Subscribe to Our Channel

Stay Informed