Global Bunker Inflation and North America's 25-Year Mine Gap Position Shallow-Deposit Projects to Displace Imports

Rising logistics costs and 25-year North American mine gap drive import substitution opportunity for shallow-deposit domestic salt projects.

- Industrial salt demand is anchored in non-discretionary end markets, including chlor-alkali chemical production, water treatment, and road de-icing, with global consumption targeting 1.4% compound annual growth through 2031.

- North America imports 8 to 10 million metric tonnes (MT) of de-icing salt annually, against zero new domestic mine development in approximately 25 years; rising bunker fuel costs are compressing the landed cost advantage of seaborne supply, positioning shallow-deposit, port-proximate domestic projects to displace import volumes on a delivered cost basis.

- Industrial salt economics are governed by delivered cost positioning rather than deposit grade; US FOB mine prices of approximately $60 per ton expand to wholesale delivered prices approaching $190 per MT in shortage periods, a 3x multiplier reflecting logistics rather than extraction cost.

- ASTM Designation D632-12(2012) establishes 95.0% sodium chloride as the minimum specification for pharmaceutical manufacturing, food processing, and precision industrial applications, separating specialty-grade producers from bulk commodity operators on a purity-verified cost curve.

- Shallow-deposit configurations with deep-water port infrastructure reduce haulage energy consumption and eliminate inland freight cost relative to legacy underground operations at approximately 600 meters depth; developers holding provincial environmental assessment releases compress time-to-production against greenfield entrants facing multi-year baseline permitting cycles.

Industrial Salt: From Commodity Input to Critical Infrastructure

Industrial salt consumption is directly linked to chlor-alkali chemical production, municipal water treatment systems, and government de-icing contracts; three end markets that do not contract materially during economic downturns. Global industrial salt consumption is projected to grow at a compound annual rate of 1.4% through 2031, a modest yet consistent expansion that supports long-duration asset underwriting without reliance on price-cycle assumptions.

Chain regionalization, the absence of new mine development in North America since 2001, and tightening ESG compliance standards are creating supply gaps that seaborne trade cannot efficiently fill, and that domestic, low-cost developers are advantaged to address.

Demand Stability Anchored in Industrial & Environmental Systems

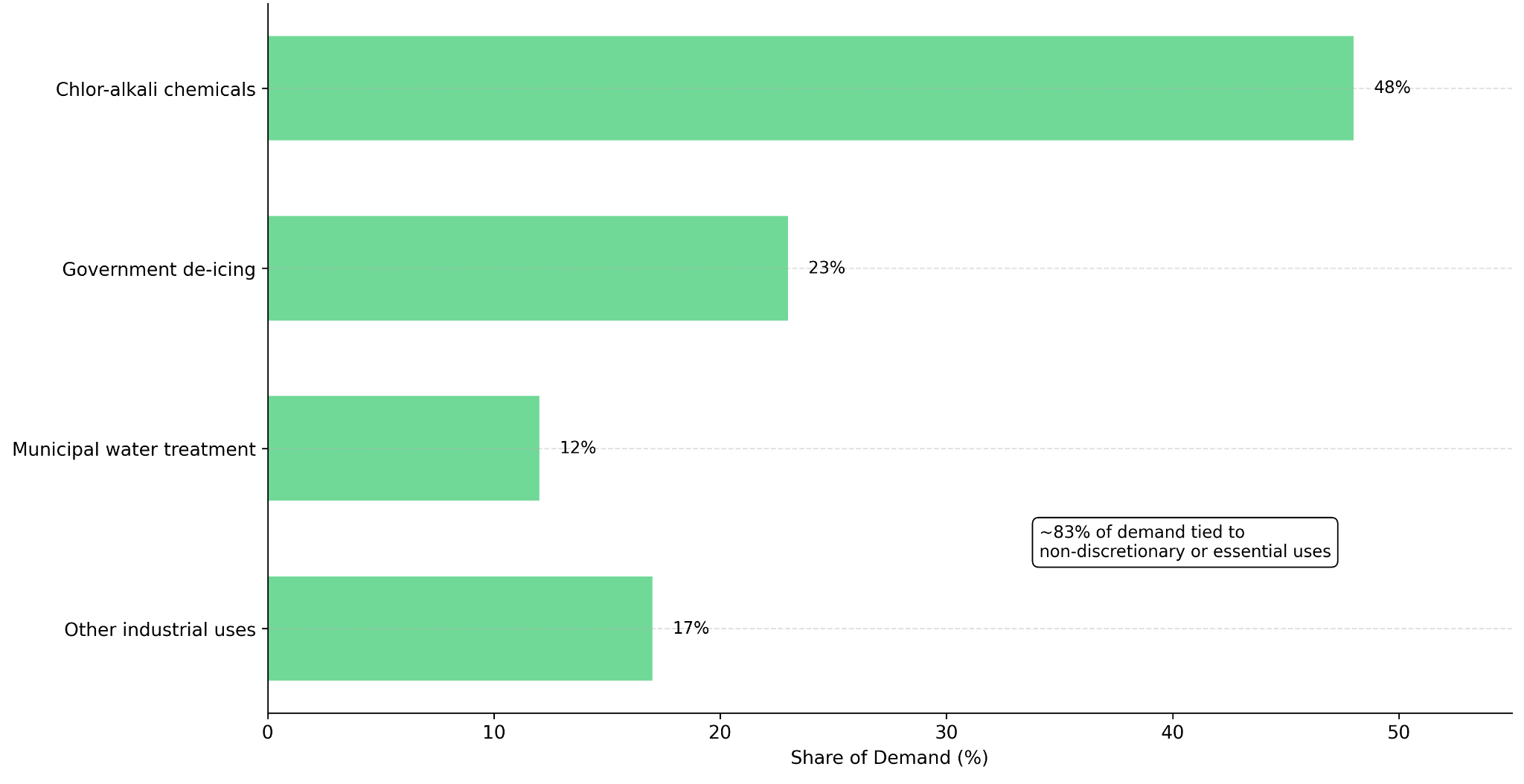

The chlor-alkali industry accounts for the largest single share of global industrial salt consumption, which identifies chemical processing as the dominant end-market segment by volume. Through electrolysis, salt is converted into chlorine and caustic soda, non-substitutable inputs to PVC production, paper and pulp processing, textile manufacturing, and industrial cleaning systems, creating a direct demand linkage to global manufacturing output.

Water treatment represents a durable and less cyclical demand driver. Salt is used in ion exchange systems for water softening across both industrial and household treatment plants, as well as in chlorination processes for municipal and industrial water supply. As governments and utilities increase investment in desalination, wastewater recycling, and potable water infrastructure in response to intensifying global water stress, each treatment category generates incremental salt demand that compounds over long infrastructure investment cycles.

De-icing represents the most weather-sensitive demand segment, concentrated in North America and Northern Europe. While mild winters introduce inventory and short-term pricing risk, the baseline demand is non-discretionary: municipal governments must maintain road safety, creating a contractually recurring buyer base. US FOB mine and plant rock salt prices have trended toward approximately $60 per ton in recent years, with wholesale road salt in Ontario spiking to approximately $190 per MT during shortage periods, a range that reflects both the logistics sensitivity of delivered pricing and the pricing power available to well-positioned domestic producers when supply tightens.

Supply Chain Regionalization: The Defining Macro Shift

The central investment thesis for industrial salt has shifted from demand growth to supply positioning. Industrial salt's low value-to-weight ratio makes long-distance ocean freight economically marginal, and increasingly so as bunker fuel costs remain elevated. Rising logistics costs are compressing the delivered cost advantage of imported salt and accelerating a structural shift toward regionalized supply.

North America’s annual imports of 8 to 10 million MTs of de-icing salt reflect a volume dependence due to decades of domestic mine closures and the absence of new mine investment. According to the corporate history of American Rock Salt, whose New York mine opened in 2001 as the newest to enter production in over 50 years, no new salt mine has entered production in North America in approximately 25 years. As logistics costs have risen, the landed cost advantage of imported salt has narrowed, creating an opening for new domestic capacity that trade flows alone cannot fill.

Atlas Salt’s Great Atlantic project is designed to target the US East Coast market via the Turf Point deep-water port, located approximately 2 kilometers from the mine site. With a planned average life-of-mine production capacity of 4.0 million MT per annum, the project is structured as an import-substitution asset, with the investment case anchored in logistics efficiency and proximity to demand rather than commodity price appreciation.

Cost Structures & Margin Sensitivities: Logistics Over Geology

Unlike precious metals or base metal porphyries, where grade continuity and metallurgical recovery rates determine cost outcomes, industrial salt economics are governed by operational and logistical efficiency. Fuel prices, port access, processing energy intensity, and deposit depth determine whether a project generates sustainable free cash flow or erodes margin during periods of price compression.

The Great Atlantic deposit sits at approximately 180 meters depth, substantially shallower than legacy underground operations such as the Goderich Mine in Ontario and the Whiskey Island Mine in Ohio, both of which operate at approximately 600 meters depth.

Shallow mining reduces haulage energy consumption and shaft capital requirements. Combined with the Turf Point deep-water port and physical processing with no chemical inputs, the project targets an all-in sustaining cost of approximately $34.90 per MT against projected net revenue of $109.40 per MT, derived from a base salt price assumption of $81.67 per MT.

Nolan Peterson frames the asset's risk profile in terms that distinguish it from conventional mining investments:

"We don't have those bottom-tier risks: metallurgical, block model, geology, and stakeholder permitting. Salt deposits are very easy to define, and permitting is advanced on this project. We have an approved environmental assessment."

The Newfoundland and Labrador Environmental Minister released the Great Atlantic Salt project from the provincial environmental assessment process in April 2024, under a Release with Conditions pursuant to the Environmental Protection Act.

ESG Pressures & Market Bifurcation

Environmental compliance is reshaping capital requirements and producer competitiveness across the global salt industry. Regulatory focus areas include brine discharge management, freshwater contamination from road salt runoff, and land-use impacts of solar evaporation operations. For institutional allocators subject to ESG screening requirements, these exposures have elevated compliance to a pre-investment diligence criterion rather than an operational afterthought.

The salt market is simultaneously bifurcating on purity. Bulk commodity salt competes primarily on delivered cost per MT. High-purity specialty salt requires profiles meeting the ASTM Designation D632-12(2012) specification of 95.0% sodium chloride, used in pharmaceutical manufacturing, food processing, and precision industrial applications.

Risk Framework: What Could Break the Thesis?

A sustained increase in fuel and logistics costs would compress margins for all producers but would disproportionately affect import-dependent end markets rather than domestically positioned, low-cost operations, intensifying rather than reversing the regionalization tailwind. Weather variability, specifically a multi-year pattern of mild winters across North America and Northern Europe, would reduce de-icing demand and cause inventory accumulation that temporarily depresses salt prices; this risk is partially mitigated by chlor-alkali and water treatment volumes, which carry no weather sensitivity.

The falsification conditions for the broader thesis are a sustained structural decline in chlor-alkali demand correlated with broad industrial contraction, or a technological substitution reducing salt dependency across multiple end markets simultaneously.

The Investment Thesis for Industrial Salt

- Industrial salt consumption is anchored in non-discretionary end markets, including chlor-alkali production, municipal water treatment, and road safety infrastructure, providing a demand foundation that is resilient across economic cycles and does not require commodity price appreciation to support asset returns.

- Supply chain regionalization is systematically reducing the cost competitiveness of long-haul imported salt in North American markets, where 8 to 10 million MT per annum on de-icing import dependence.

- Low-cost, shallow-deposit assets with deep-water port access and provincial environmental assessment releases are positioned in the lower quartile of the delivered cost curve, providing margin resilience during periods of salt price compression.

- Multi-decade mine life and contractually recurring municipal and government customers support infrastructure-like cash flow profiles that are distinct from the cyclical revenue patterns typical in metals mining.

- Hydropower-electrified project designs with physical-only processing and minimal surface footprint reduce regulatory and reputational risk for institutional allocators operating under ESG screening mandates.

- Projects that have already obtained environmental assessment releases in permitting-constrained jurisdictions represent a barrier-to-entry advantage that takes years for new entrants to replicate.

Industrial salt's demand growth remains at a projected 1.4% compound annual growth rate through 2031, but supply-side dynamics, driven by 25 years of zero new North American mine development, rising logistics costs, and tightening ESG compliance requirements, are creating structural supply gaps that seaborne trade cannot efficiently fill.

TL;DR

Industrial salt demand grows at 1.4% annually through 2031, anchored in non-discretionary chlor-alkali production, water treatment, and road de-icing. North America imports 8 to 10 million metric tonnes of de-icing salt annually against zero new domestic mine development in approximately 25 years. Rising bunker fuel costs compress the landed cost advantage of seaborne supply, positioning shallow-deposit, port-proximate domestic projects to displace import volumes on a delivered cost basis. Industrial salt economics are governed by logistics rather than geology: US FOB mine prices of $60 per ton expand to $190 per MT wholesale during shortages, a 3x multiplier reflecting freight sensitivity rather than extraction cost.

FAQs (AI-Generated)

Industrial salt demand is anchored in non-discretionary end markets that do not contract materially during economic downturns: chlor-alkali chemical production (PVC, paper processing), municipal water treatment systems, and government road de-icing contracts. These sectors generate contractually recurring demand with projected 1.4% compound annual growth through 2031, supporting infrastructure-like cash flow profiles distinct from cyclical metals markets.

No new salt mine has entered production in North America in approximately 25 years, according to American Rock Salt's corporate history, creating a structural supply gap that domestic capacity cannot fill. Decades of mine closures combined with zero new mine investment have made North America dependent on seaborne imports despite rising logistics costs that compress the delivered cost advantage of imported salt.

Industrial salt's low value-to-weight ratio makes delivered cost positioning more critical than deposit grade. US FOB mine prices of approximately $60 per ton expand to wholesale delivered prices approaching $190 per MT during shortage periods, a 3x multiplier reflecting fuel costs, port access, and inland freight rather than extraction cost. Rising bunker fuel costs disproportionately affect long-haul imports, favoring port-proximate domestic operations.

Shallow deposits at approximately 180 meters depth reduce haulage energy consumption and shaft capital requirements compared to legacy operations at approximately 600 meters depth. Combined with deep-water port infrastructure, shallow configurations eliminate inland freight cost and reduce delivered cost per metric tonne, positioning these assets in the lower quartile of the cost curve during periods of price compression.

A sustained structural decline in chlor-alkali demand correlated with broad industrial contraction, or technological substitution reducing salt dependency across multiple end markets simultaneously, would falsify the demand-side thesis. Multi-year patterns of mild winters across North America and Northern Europe would reduce de-icing demand and cause temporary inventory accumulation and price depression, though chlor-alkali and water treatment volumes carry no weather sensitivity.

Analyst's Notes

Subscribe to Our Channel

Stay Informed