Global Supply Shortages and Critical-Mineral Policy Propel Copper Toward Record Highs

Copper prices surge past $11,000/t as USGS adds it to critical minerals list. Supply deficits, mine disruptions, and policy shifts drive institutional investment.

- Copper prices have climbed above $11,000 per tonne on the London Metal Exchange, within sight of record levels, driven by supply shocks, policy momentum, and renewed trade optimism.

- The United States Geological Survey's addition of copper to the critical-minerals list marks a policy inflection point, cementing its status as a strategic material vital to energy, defense, and artificial intelligence infrastructure.

- The International Copper Study Group's downgrade of 2025 mine-supply growth to 1.4 percent from 2.3 percent signals deep structural constraints amid global mine disruptions.

- Institutional investors are responding through vehicles such as the Sprott Physical Copper Trust, whose net asset value is up 21.5 percent year-to-date, reflecting growing conviction in physical scarcity.

- Developers like Marimaca Copper and explorers such as Gladiator Metals and Fitzroy Minerals are strategically positioned to benefit as capital rotates toward high-grade, low-capex, and jurisdictionally secure projects.

A Perfect Storm of Supply Shocks and Policy Momentum

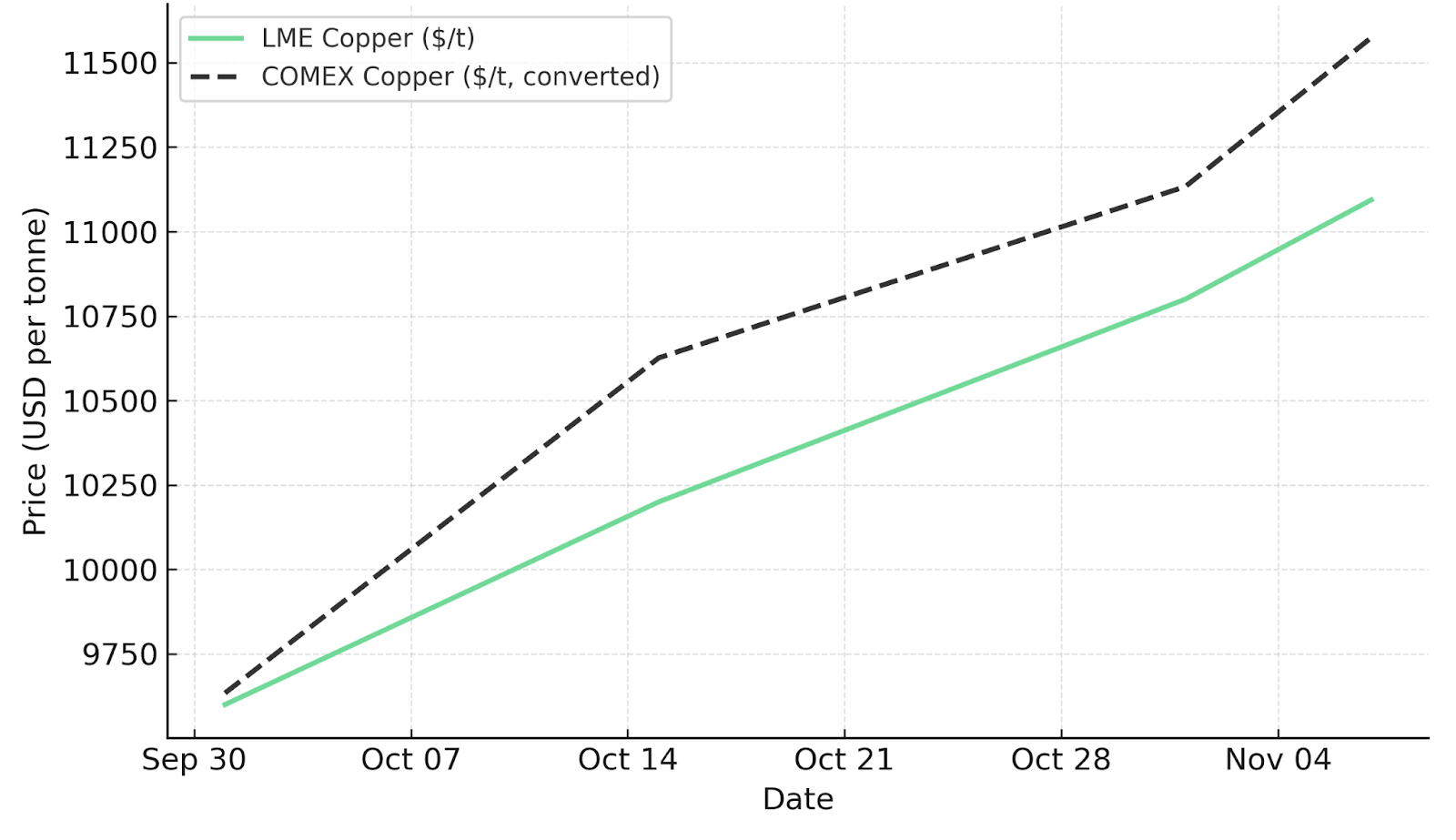

Copper's latest rally is not merely cyclical. It reflects the intersection of macro policy, geopolitics, and constrained mine supply. In early November 2025, copper futures surged to $11,094 per tonne on the London Metal Exchange and $5.247 per pound on COMEX, propelled by a weaker United States dollar and renewed optimism over a potential US-China trade accord.

At the same time, structural drivers are reinforcing this move. The United States Geological Survey officially designated copper as a critical mineral on November 6, 2025, joining silver on a list traditionally dominated by battery metals and rare earths. This reclassification elevates copper to a national-security asset, enabling policy incentives, financing mechanisms, and trade prioritization for domestic projects.

Meanwhile, operational disruptions across the Kamoa-Kakula complex in the Democratic Republic of the Congo, Grasberg in Indonesia, and multiple Chilean mines underscore how fragile global supply chains have become. These incidents amplify market fears that the industry cannot ramp production quickly enough to meet the metal's expanding role in electrification, defense systems, and data-center infrastructure.

As copper transitions from industrial commodity to strategic material, the pricing structure is reflecting this paradigm shift. Inventories on the London Metal Exchange and COMEX remain near multi-year lows, and spot premiums are emerging, a rare occurrence outside of acute demand spikes.

Structural Deficit Deepens as Supply Growth Stalls

The supply side tells a story of structural underinvestment. According to the International Copper Study Group, mine-supply growth for 2025 has been revised down to 1.4 percent, compared with 2.3 percent previously. Actual 2024 growth reached only 2.8 percent, already below expectations.

Global project pipelines remain thin. Years of capital discipline, environmental, social, and governance permitting delays, and limited greenfield discoveries have left the industry unable to offset natural depletion rates. Copper's long-term demand trajectory compounds this imbalance. BHP forecasts a 70 percent increase in global copper demand by 2050, driven by grid electrification, artificial intelligence-driven computing, renewable integration, and electric vehicle adoption. Yet, the current development queue cannot satisfy this growth without prices sustaining well above incentive levels, estimated around $10,000 per tonne.

The result is a structural deficit narrative that is rapidly replacing cyclical optimism. Producers are benefiting from high margins, but investors are increasingly focused on developers and explorers with low-capex, high-grade leverage to the next expansion phase. Hayden Locke, President and Chief Executive Officer of Marimaca Copper, frames the scarcity in actionable terms:

"What we know is there are very few actionable copper projects in the near term that can become a reasonably significant producer of copper."

This constraint is driving capital toward projects that can deliver tonnes within tight timelines and competitive cost structures.

Investor Capital Rotates Toward Physical and Strategic Exposure

Institutional sentiment has shifted decisively. The Sprott Physical Copper Trust, the world's first physical copper investment vehicle, exemplifies the new investor psychology. As of November 7, 2025, it held 10,020 tonnes of copper with a 21.5 percent net asset value increase year-to-date, nearly matching the 25.2 percent year-to-date rise in benchmark copper prices.

This correlation highlights a broad re-rating of copper as a financialized asset class. Unlike past cycles, where exposure came primarily through producers, investors are now seeking direct physical and derivative exposure to manage geopolitical and inflationary risks. The trend favors companies that can translate resource size into near-term optionality, either through de-risked Definitive Feasibility Study-stage assets or high-grade exploration success.

Low-Capex Development at the Epicenter of Policy and Electrification

Marimaca Copper's Marimaca Oxide Deposit in Chile represents one of the most advanced, low-carbon copper developments globally. Its Definitive Feasibility Study confirms 179 million tonnes at 0.42 percent total copper with a Post-Tax Net Present Value at eight percent discount of $1.1 billion, Internal Rate of Return of 39 percent, and a 2.2-year payback at $5.05 per pound copper.

The project's All-In Sustaining Cost of $1 per pound and capex intensity of $11,700 per tonne per annum of copper place it within the second quartile of the cost curve, offering margin resilience even in volatile pricing environments. Marimaca's use of recycled seawater and renewable power aligns directly with environmental, social, and governance-linked funding mandates, crucial as copper earns its green metal status under global policy frameworks. With a Final Investment Decision targeted for the second half of 2026, the company stands positioned to advance during a supply-constrained environment.

Hayden Locke emphasizes the capital efficiency:

"It confirms that we are in the bottom decile of capital intensity for copper projects, new development stage copper projects globally."

Backed by Greenstone (22.3 percent), Assore (16.3 percent), Ithaki Limited (14.1 percent) and Mitsubishi (4.0 percent), Marimaca reflects institutional readiness to fund near-term production with scalable, low-carbon credentials, precisely the type of project policymakers seek to accelerate. The company is also positioning for scale. Locke outlines the expansion vision:

"The second focus is how do we go from 50,000 tons to 70 or more thousand tons of copper for an extended period of time."

This growth trajectory aligns directly with the energy transition's copper intensity, where every megawatt of renewable capacity and every data center requires multiples of historical copper consumption.

High-Grade Exploration in a Stable Jurisdiction

While most new discoveries are found in high-risk jurisdictions, Gladiator Metals is proving the opposite. Its Whitehorse Copper Project in Yukon, Canada, sits along a 35-kilometer-long skarn belt once mined for copper and molybdenum. Drill results such as 26 meters at 3.6 percent copper and 11.5 meters at 7.5 percent copper from shallow depths underscore the project's near-surface, high-grade potential, a critical differentiator in an industry facing rising capex and permitting lead times.

With 35,000 meters completed and 15,000 meters remaining in 2025, Gladiator's objective is a Pre-Resource estimate for Cowley Park in 2026. As of October 2025, the company reported approximately $27 million in cash, supporting its planned exploration program through 2025. The project holds a Class 3 Permit Approval providing increased drill density flexibility, with a five-year Class 3 License expected in 2026. The company is advancing an Exploration Co-Operation Agreement with the Kwanlin Dün First Nation, targeted for December 2025.

Jason Bontempo, Chief Executive Officer of Gladiator Metals, frames the scale ambition in terms institutional investors require:

"Our view is that we are targeting over 100 million tons at above 1 percent copper not including any credits."

This inventory target, if realized, would position Gladiator among the top undeveloped copper assets in North America. The company's backers, including Macquarie Bank, reflect the sophistication of capital now circling high-grade, low-risk exploration plays.

Multi-Metal Leverage to Copper's Critical-Mineral Momentum

Fitzroy Minerals brings diversified leverage through its Buen Retiro Iron Oxide Copper Gold deposit and Caballos copper-molybdenum-gold-rhenium projects in Chile's established Copper Fairway. Drilling at Buen Retiro has delivered 110 meters at 1.94 percent copper, while Caballos returned 42 meters at 2.26 percent copper equivalent, including molybdenum and rhenium, both classified as strategic elements.

By combining oxide and sulphide potential, Fitzroy provides optionality: near-surface leachable material for short-cycle development and deeper sulphides for longer-term growth. The company outlined a C$8 million 12-month exploration program in its June 2025 plan, funded by an intended capital raise, targeting scale validation while its 30 percent clawback right with Pucobre offers financial de-risking uncommon in early-stage exploration.

Gilberto Schubert, Chief Operating Officer and Country Manager of Fitzroy Minerals, quantifies the multi-metal value:

"The molybdenum grade represents almost doubling the copper grade. In terms of value the amount of money is similar to the amount of grade, so if we put in terms of copper equivalent, we double the grade."

Rhenium, a byproduct at Caballos, adds another strategic dimension. Schubert explains:

"Rhenium... It's a very important material for the military aerospace industry."

As investors pivot toward assets with multi-metal exposure, Fitzroy's model demonstrates how smaller explorers can align with macro themes of critical-metal diversification and Chile's supportive infrastructure base. Schubert emphasizes the jurisdictional advantage:

"We are close to Copiapó, one of the main mining towns in Chile, close to the Panamerican Road, to the main power grids of Chile, 40 kilometers to the coast in the middle of the desert... this type of location makes the projects easier and faster to be built."

This infrastructure proximity is critical in an environment where permitting timelines and construction costs are stretching globally. Schubert also notes Chile's development speed:

"In Chile it's quite common to go into production on a prefeasibility study because there are so many small mines, there's so much copper, there's so much of an established mining industry."

Macro Risks and Investor Considerations

Despite bullish fundamentals, copper's ascent is not without risks. A resurgence in the United States dollar or higher real yields could dampen commodity inflows. Even in top jurisdictions, environmental, social, and governance and social-license challenges can extend project timelines by years.

The durability of Chinese demand remains a critical variable for near-term pricing. Concentration of supply in high-risk regions, particularly the Democratic Republic of the Congo and Indonesia, introduces potential export volatility. Investors must therefore prioritize jurisdictional stability, cost resilience, and balance-sheet discipline when allocating capital across the copper space.

The Investment Thesis for Copper

Several strategic factors support maintaining or increasing copper exposure in institutional portfolios.

- The addition of copper to the United States critical-minerals list elevates it to strategic material status, improving funding access and project prioritization for North American and allied-nation developments.

- Ongoing mine disruptions and chronic underinvestment have entrenched a long-term supply gap projected to persist through the 2030s, with mine-supply growth for 2025 revised down to 1.4 percent.

- Electrification, artificial intelligence infrastructure, defense systems, and grid modernization are driving 70 percent forecast growth in copper demand by 2050, outpacing current development pipelines.

- Rising investor participation via vehicles such as the Sprott Physical Copper Trust underscores the shift toward viewing copper as a store of value and inflation hedge beyond its industrial role.

- Developers like Marimaca provide near-term production leverage with bottom-decile capital intensity and competitive operating costs, while explorers such as Gladiator and Fitzroy offer asymmetric upside tied to discovery scale, grade quality, and multi-metal diversification.

- Projects in stable jurisdictions with established infrastructure and environmental, social, and governance frameworks are commanding valuation premiums as geopolitical risk premiums rise across commodity supply chains.

From Industrial Metal to Strategic Cornerstone

Copper's record-level rally encapsulates a broader economic transformation. What began as a cyclical upswing now reflects structural revaluation, underpinned by constrained supply, policy urgency, and institutional capital migration into tangible assets.

As the line blurs between industrial necessity and strategic security, copper's premium is no longer purely price-based, it is systemic. Investors positioned early in cost-efficient, low-carbon, and jurisdictionally stable assets stand to capture the upside of what may be the defining commodities supercycle of the decade.

TL;DR

Copper prices have climbed above $11,000 per tonne, approaching record highs as structural supply constraints collide with surging demand from electrification, artificial intelligence infrastructure, and defense systems. The United States Geological Survey's November 2025 designation of copper as a critical mineral marks a strategic policy shift, while the International Copper Study Group's downward revision of 2025 mine-supply growth to 1.4 percent underscores chronic underinvestment. Institutional investors are rotating capital into physical copper vehicles and development-stage projects offering low-capex, high-grade leverage. Developers like Marimaca Copper with bottom-decile capital intensity and explorers such as Gladiator Metals and Fitzroy Minerals in stable jurisdictions are positioned to benefit as copper transitions from industrial commodity to strategic cornerstone of the energy transition.

FAQs (AI-Generated)

The United States Geological Survey designated copper as a critical mineral on November 6, 2025, recognizing its strategic importance to national security, energy infrastructure, defense systems, and artificial intelligence computing. This reclassification enables policy incentives, financing mechanisms, and trade prioritization for domestic copper projects, elevating copper from an industrial commodity to a strategic material alongside battery metals and rare earths.

The supply deficit stems from multiple converging factors: chronic underinvestment in new mine development over the past decade, operational disruptions at major producing assets in the Democratic Republic of the Congo, Indonesia, and Chile, and natural depletion rates outpacing replacement discoveries. The International Copper Study Group revised 2025 mine-supply growth down to 1.4 percent from 2.3 percent, while demand is projected to increase 70 percent by 2050 driven by electrification, renewable energy, and data center expansion.

Institutional investors are diversifying their copper exposure beyond traditional mining equities through physical copper vehicles like the Sprott Physical Copper Trust, which holds over 10,000 tonnes with a 21.5 percent year-to-date net asset value increase. Capital is also rotating toward development-stage projects with low capital intensity and high-grade exploration plays in stable jurisdictions, reflecting copper's emerging role as both an industrial metal and a strategic asset for inflation hedging and geopolitical risk management.

Investors are prioritizing projects with bottom-quartile capital intensity (low capex per tonne of production), competitive All-In Sustaining Costs, jurisdictional stability in mining-friendly regions like Canada and Chile, established infrastructure proximity to reduce construction timelines, environmental and social governance credentials including renewable power and water recycling, and near-term production timelines within 3-5 years. High-grade deposits above 1 percent copper and multi-metal credits (molybdenum, rhenium, gold) provide additional valuation leverage.

Key risks include potential strengthening of the United States dollar or rising real interest rates that could reduce commodity investment flows, durability of Chinese industrial demand amid economic uncertainty, environmental and social permitting delays that can extend project timelines by years even in favorable jurisdictions, geopolitical concentration of supply in high-risk regions like the Democratic Republic of the Congo and Indonesia, and the possibility that sustained high prices eventually incentivize substitution in certain applications or accelerate recycling rates.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed