Government Financing & Higher Rates Reward Funded Battery Metals Developers as China Controls 70% of Refining

Government financing, higher interest rates and supply security are making access to capital the decisive advantage for battery metals developers.

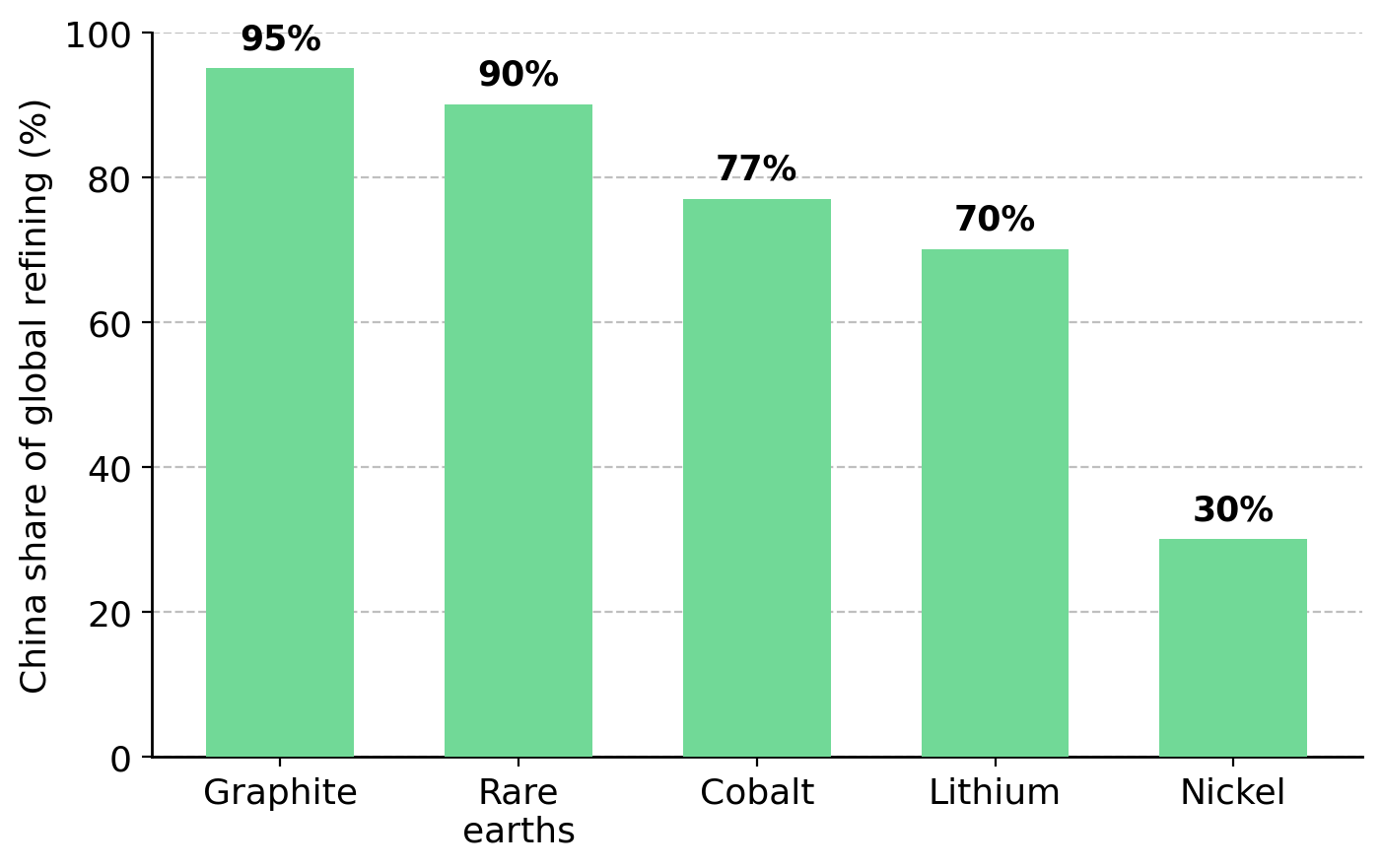

- China controls about 70% of global refining capacity for strategic minerals, prompting Western governments to fund alternative supply chains through loans, tax credits and offtake agreements.

- Higher US interest rates and a stronger US dollar have increased financing costs, making access to capital more important than resource size for development-stage battery metals companies.

- Government-backed financing can cover more than half of project equity requirements, reducing shareholder dilution and improving the likelihood of reaching a final investment decision.

- Developers with low-cost assets, secure jurisdictions and vertical integration are attracting financing because lenders prioritize resilient cash flows and traceable non-Chinese supply.

- The biggest risks are weaker nickel and cobalt demand from battery chemistry shifts, easing Chinese export controls, and financing or permitting packages that fail to close.

Financing Has Become the Binding Constraint on Battery Metals

Over the past decade, lithium, nickel and rare-earth projects were primarily evaluated on grade, tonnage and metallurgy. Many of the sector's largest deposits are already defined, while export controls, production quotas and processing concentration have become the main constraints on bringing new supply to market. Today, project value depends increasingly on whether a developer can secure enough funding to reach a final investment decision, the formal board approval to build a mine, without issuing enough new equity to significantly dilute existing shareholders.

Financing has become the primary constraint on new battery-metals projects because governments are reshaping supply and higher interest rates have increased the cost of capital. Chinese export controls, Congolese cobalt quotas and Indonesian ore limits have made government policy a primary driver of battery-metals pricing. The International Energy Agency reported that China controls refining for 19 of 20 strategic minerals, with an average market share of about 70%, reinforcing the strategic value of non-Chinese supply. At the same time, higher interest rates have increased the cost of capital, making equity financing more dilutive and harder to secure. State-backed financing can now cover more than half of a project's equity requirement, reducing shareholder dilution and making government support a key determinant of which projects reach construction.

Development-stage and exploration-stage mining companies carry higher financing, permitting and execution risk, making their shares more volatile, less liquid and more exposed to equity dilution.

Government Capital Is Driving New Battery Metals Supply

Western governments are actively financing critical-minerals supply chains rather than relying on market incentives alone. Governments are using loans, refundable tax credits, export-credit support and defense-stockpile offtake to lower borrowing costs and reduce the amount of equity developers must raise to build new projects.

State-Backed Debt Reduces Equity Dilution

Canada Nickel is advancing the Crawford nickel-cobalt sulfide project in Ontario and has appointed a lead arranger for a debt facility of up to US$600 million backed by refundable investment tax credits and government reimbursements for eligible construction spending under Canada's critical-minerals framework. The bridge facility converts future tax-credit receipts into upfront construction capital and is designed to fund more than half of Crawford's equity requirement, leaving only about US$10-15 million of additional equity to raise. The financing package depends on a federal construction permit targeted for the second half of 2026. If approved, Crawford would become the first project permitted under Canada's 2019 Impact Assessment Act.

Mark Selby, Chief Executive Officer of Canada Nickel, explains how government-backed financing strengthens Crawford's capital structure:

"This bridge financing is central to Crawford's overall capital structure. It allows us to deploy Canada's generous investment tax credits available for critical mineral projects in Canada to fund more than half of the equity capital we need to build Crawford."

Vertical Integration Strengthens Critical Minerals Supply Chains

Energy Fuels, a US uranium and rare-earth producer has secured a conditional 20-year US$725 million loan from the US Office of Strategic Capital to expand the White Mesa Mill in Utah, the only commercial-scale US facility that separates rare-earth oxides from monazite. It has also secured a US$250 million term-loan commitment from Goldman Sachs to support its US$1.9 billion acquisition of magnet manufacturer Vacuumschmelze. Controlling each stage of production, from rare-earth oxide to finished neodymium-iron-boron magnets, allows Energy Fuels to capture more value in a market where China produces roughly 94% of finished neodymium-iron-boron magnets.

Mark Chalmers, then Chief Executive Officer of Energy Fuels, explains why controlling the entire rare earth supply chain strengthens competitiveness:

"To really compete with China, you have to have all those steps. You can't be missing a step in the middle of it, so we've been very focused on the integration at least through alloys."

Supply Security Is Driving Financing for Non-Chinese Critical Minerals

Government capital and commercial debt are flowing to these projects because security of supply now outweighs near-term commodity prices in financing decisions. When one country controls most refining or processing capacity for a critical mineral, buyers and lenders place a premium on secure, traceable supply from alternative jurisdictions. Projects are most likely to secure financing when they combine a differentiated supply position with operating costs low enough to service debt across commodity-price cycles.

Supply Concentration Is Driving Critical Minerals Financing

Lifezone Metals combines a US platinum-group-metals recycling business with the development-stage Kabanga nickel sulfide project in Tanzania, giving lenders exposure to traceable nickel supply outside Indonesia. Nickel sulfide ore is upgraded into concentrate before refining, while Indonesia's laterite ores require energy-intensive smelting or high-pressure acid leaching that increases sulfuric acid, energy and reagent costs. Lower processing costs make nickel sulfide projects more attractive to lenders and strategic buyers seeking non-Indonesian supply. That financing includes support from the Minerals Security Partnership, the US Development Finance Corporation, Société Générale and a US$60 million Taurus bridge facility.

Ingo Hofmaier, Chief Financial Officer of Lifezone Metals, explains how supply concentration is reshaping critical minerals markets:

"If you compare this with OPEC, the bigger countries produce 15 to 18% of oil output. If the development continues in Indonesia, you will have 75 to 80%."

Low-Cost Projects Are Better Positioned to Secure Financing

A project's ability to secure financing also depends on its position on the cost curve, because lower operating costs protect margins and support debt repayments when commodity prices fall. Sovereign Metals is advancing the development-stage Kasiya rutile and graphite project in Malawi, where a soft, weathered orebody eliminates the need for drilling, blasting and hard-rock grinding. Those operating advantages support a pre-tax net present value of about US$2.2 billion at an 8% discount rate in the project's definitive feasibility study. The project may also recover a heavy rare-earth monazite stream from existing tailings with minimal additional capital, although that potential by-product is not included in the definitive feasibility study's base-case economics.

Ben Stoikovich, Chairman of Sovereign Metals, explains how low operating costs support profitability during periods of price weakness:

"What's important for Sovereign is that Kasiya is right at the bottom end of the real cost curve, and we'll always be able to sell graphite into the market at healthy margins."

Fed Policy & the US Dollar Are Driving Near-Term Battery Metals Prices

Higher US interest rates and a stronger US dollar are tightening financing conditions for battery-metals projects. At its June 2026 meeting, the Fed, under Chair Kevin Warsh, held its policy rate at 3.50% to 3.75%, removed its easing bias and raised its median year-end policy-rate projection to 3.8%, according to the Fed and CNBC. A stronger US dollar increases the cost of dollar-denominated metals for overseas buyers while higher interest rates keep borrowing costs elevated, increasing the value of government-backed financing that reduces reliance on new equity issuance.

Near-term battery-metals prices have weakened even as supply remains constrained by government policy and financing conditions. A de-escalation between the US and Iran pushed oil to its lowest level since the conflict began, reducing energy and reagent costs for high-pressure acid leach nickel projects. Meanwhile, Chinese new-energy-vehicle sales fell 7.5% year over year in May even as electric vehicles increased their market share to 62.9%, indicating slower volume growth rather than weaker market penetration. Battery-metals demand is shifting from passenger electric vehicles toward grid-scale energy storage and data-center power infrastructure, changing which metals and processing routes attract new investment.

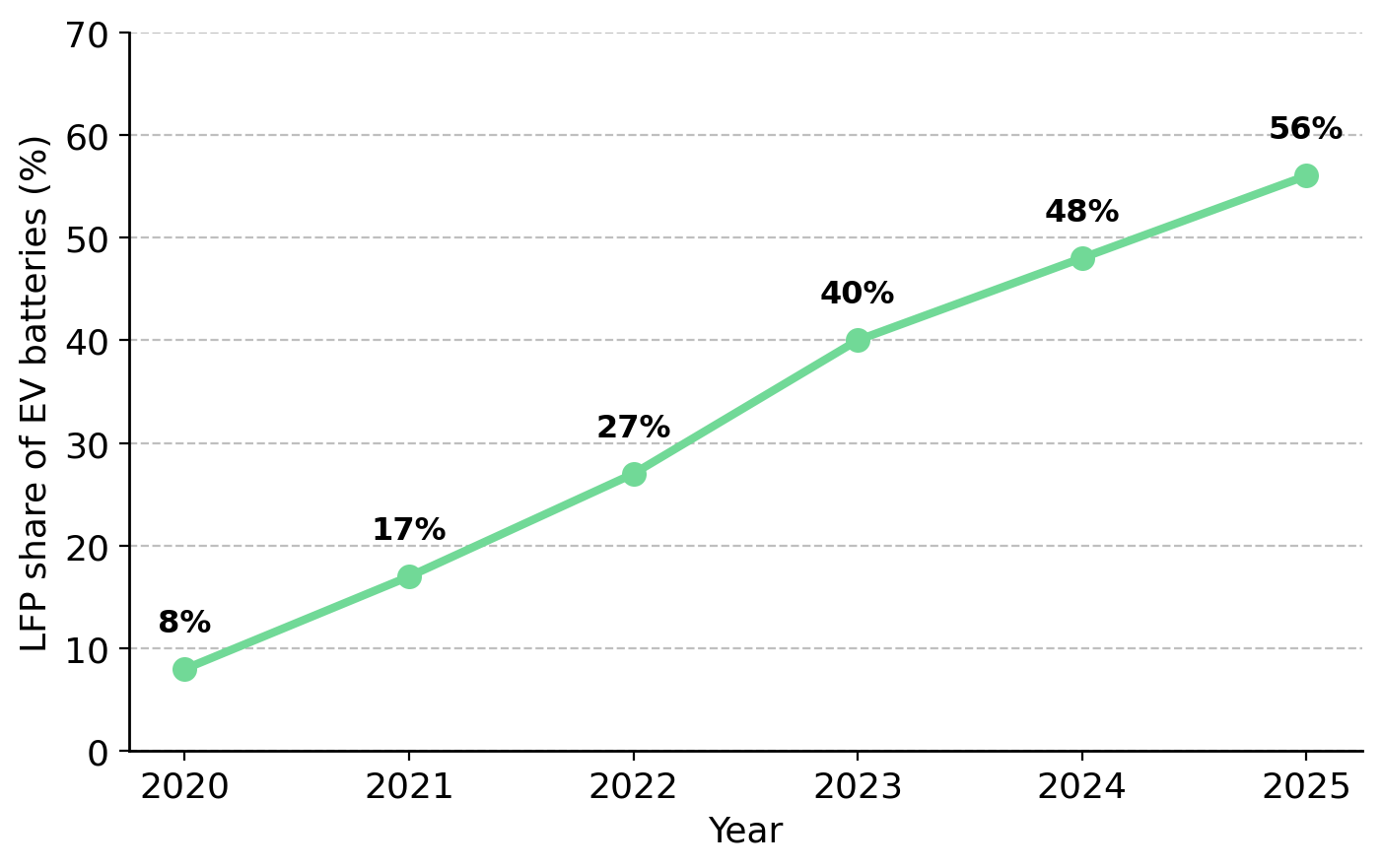

Battery Chemistry Shifts & Financing Risks Could Weaken the Investment Thesis

Faster adoption of battery chemistries that use less nickel and cobalt is the second major risk to the financing thesis. Lithium iron phosphate and sodium-ion batteries reduce demand for those metals, weakening the cash-flow assumptions that support project financing. The nickel-manganese-cobalt share of Chinese battery production has already fallen to about 18% from 25% a year earlier, illustrating that this transition is already underway. A higher-for-longer Fed and a stronger US dollar can also limit gains in dollar-denominated metal prices, reducing project cash flows and making new financing more difficult to secure.

Execution risk remains a key constraint on project financing and should be assessed explicitly. Pre-construction valuations rely on modeled economics rather than operating cash flow, inferred resources carry greater geological uncertainty than indicated or measured resources, permits can be delayed, and financing commitments may not close. The financing thesis depends on verifiable milestones, including government quotas, financing mandates and loan commitments, while assuming that the security premium for non-Chinese supply and lender appetite remain in place.

Government Policy & Financing Are Reshaping Battery Metals Supply

Rebuilding refining and processing capacity outside China requires years of investment and substantial capital, which is why governments are subsidizing new projects instead of relying on higher prices to attract private investment. Financing, rather than geology, now determines how quickly alternative critical-minerals supply chains can reach construction. As governments continue to provide loans, tax credits and other financial support, access to capital has become the primary constraint on expanding non-Chinese refining and processing capacity.

The Investment Thesis for Battery & Critical Metals

- Export controls and resource nationalism increase the value of low-cost projects in secure jurisdictions, improving financing terms and valuations.

- Financing access now matters more than resource size, making balance-sheet strength and funding progress the key differentiators among developers.

- Government loans, tax credits and offtake agreements reduce equity needs, limiting dilution and preserving shareholder value.

- Vertical integration into processing and manufacturing diversifies cash flow, improving credit quality and financing capacity.

- Low-cost projects are better able to withstand price declines, making them more attractive to lenders.

- A hawkish Fed and stronger US dollar raise financing costs, favoring funded projects over equity-dependent developers.

- Long-term demand from power grids, electric vehicles and defense supports projects that secure permits and financing on time.

Battery and critical minerals are no longer driven by electric-vehicle demand alone. Government policy and tighter financing conditions increasingly determine which projects secure funding and advance toward construction, giving an advantage to developers that can permit and finance projects within non-Chinese supply chains before policy priorities change. Modeled economics create value only when projects reach production, making financing capacity, permitting progress and execution the primary factors separating successful developers from those that remain stalled.

TL;DR

Government policy, rather than geology alone, is increasingly determining which battery metals projects reach construction. Loans, tax credits and other state-backed financing reduce equity dilution while higher interest rates and a stronger US dollar make private capital more expensive. China's dominance of critical minerals refining has increased the strategic value of secure non-Chinese supply chains, directing financing toward low-cost, well-funded developers with strong execution capabilities. Investors should prioritize companies that have secured financing, permits and competitive operating costs, while monitoring risks including changing battery chemistries, easing supply restrictions and project execution delays.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed