OPEC+ Output Hikes Fail to Lift Supply as US Crude Stocks Stay 7% Below Average

OPEC+ output hikes failed to lift physical supply as Gulf exports lagged and US crude inventories stayed 7% below average, supporting Brent prices.

- OPEC+ approved a third consecutive monthly output increase of 188,000 bpd from August, but the Strait of Hormuz closure continued to cap output from Saudi Arabia, Kuwait, and Iraq, limiting the increase in physical supply.

- Gulf oil exports exceeded 10 million bpd in June, up more than 3 million bpd from May, but remained 40% below pre-war levels, limiting the recovery in global oil supply.

- Brent crude fell to $71.78 per barrel, near a four-month low, while WTI traded at $68.49, reflecting continued pressure from expectations of higher OPEC+ supply and recovering Gulf exports.

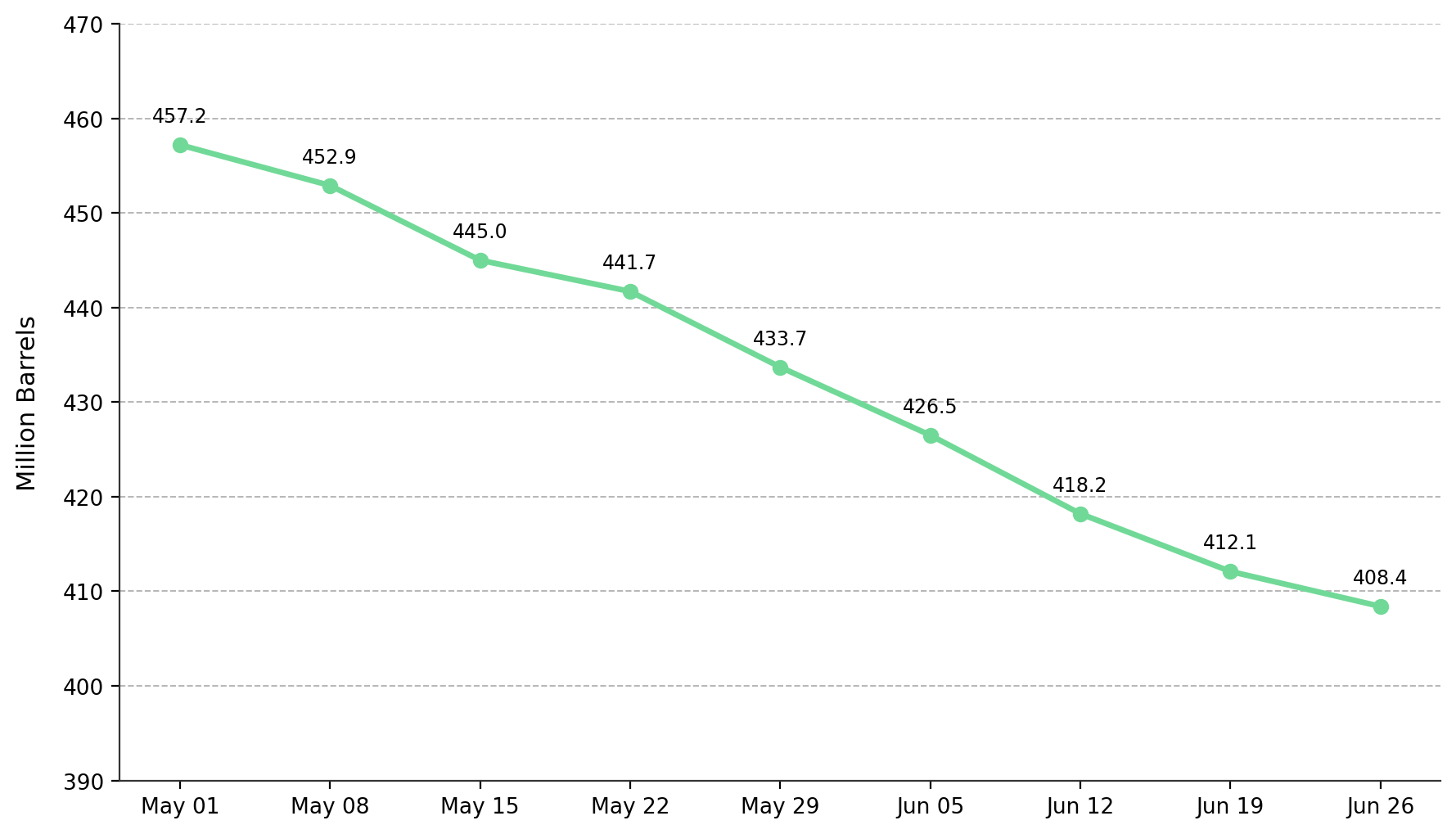

- US commercial crude oil inventories fell 3.8 million barrels to 408.4 million barrels, leaving stocks about 7% below the five-year seasonal average and supporting crude prices despite higher OPEC+ output targets.

- Four-week average US crude imports averaged 5.5 million bpd, down 10.9% from a year earlier, limiting inventory replenishment despite recovering Gulf exports.

Gulf Export Recovery & Crude Market Repricing

Brent crude fell 34 cents, or 0.47%, to $71.78 per barrel after OPEC+ approved a third consecutive monthly output increase of 188,000 bpd from August, adding to planned increases for June and July. WTI crude traded at $68.49, down 20 cents, as the market priced in additional planned OPEC+ supply. Both contracts weakened in recent weeks as markets weighed US-Iran peace talks against recovering Gulf oil exports through the Strait of Hormuz.

OPEC output rose 3.3 million bpd in June to 19.43 million bpd, rebounding from its lowest level in more than two decades, while Gulf exports from Saudi Arabia, Kuwait, Iraq, and neighboring producers increased by more than 3 million bpd to exceed 10 million bpd. Gulf exports still remained 40% below pre-war levels, limiting the effect of three consecutive OPEC+ quota increases on global oil supply.

Strait of Hormuz Disruptions & Production Constraints

The August output increase of 188,000 bpd has not translated into higher production because the US-Israeli war with Iran closed the Strait of Hormuz to tanker traffic, capping output from Saudi Arabia, Kuwait, and Iraq. IG market analyst Tony Sycamore said quotas are "probably still not being met due to production still ramping up after the conflict," indicating official targets remain above current output.

Four-week average US crude imports averaged 5.5 million bpd, down 10.9% from a year earlier. US refineries operated at 96.6% of capacity and processed 17.2 million bpd of crude, keeping demand for feedstock high while imports remained below last year's level. US commercial crude inventories fell 3.8 million barrels to 408.4 million barrels, leaving stocks 7% below the five-year seasonal average despite recovering Gulf exports.

US-Iran Peace Talks & Oil Market Outlook

KCM Trade chief market analyst Tim Waterer said markets were waiting to see whether US-Iran relations would stabilize or deteriorate. No new progress emerged in US-Iran peace talks, while 160 vessels transited the Strait of Hormuz during the previous week. Shipping activity recovered, but Gulf oil exports remained about 40% below pre-war levels.

Current export flows and US crude inventories point to two likely market outcomes. In the base case, Gulf exports recover gradually but remain well below pre-war levels, US crude inventories stay 5% to 8% below the five-year average, Brent trades between $68 and $78 per barrel, and producers with breakeven costs below $55 per barrel maintain healthy operating margins. In the bear case, a US-Iran ceasefire allows Gulf exports to recover more quickly, US crude inventories rise above the five-year average, Brent falls below $68 per barrel, and producers with breakeven costs of $60 to $65 per barrel face margin pressure.

Elevated Diesel Costs & Mining Margin Resilience

The national average on-highway diesel price was $4.668 per gallon, up $0.941 from a year earlier. Crude prices remained below last year's conflict-driven levels, but diesel prices stayed nearly $0.94 per gallon higher than a year earlier, indicating downstream fuel costs have not fallen in line with crude prices. Mining, heavy haulage, and agriculture operators with fuel hedges rolling off in Q3 2026 could continue to face elevated diesel costs even if crude prices remain lower.

WTI Cushing spot prices were $70.30, while WTI later traded at $68.49 per barrel. Mining projects with diesel-equivalent breakeven costs below $50 per barrel remain profitable at current fuel prices. Operators without fuel hedges remain exposed to diesel prices of about $4.67 per gallon, which can increase operating costs even if crude prices remain near current levels.

Inventory Trends & Energy Market Signals

US commercial crude inventories remained 7% below the five-year seasonal average while Brent traded near $71.78 per barrel. Commercial crude inventories stood at 408.4 million barrels as four-week average imports remained 10.9% below a year earlier at 5.5 million bpd. Refinery utilization of 96.6% and below-average crude inventories continue to support crude prices by limiting the pace of inventory rebuilding as Gulf exports recover.

A faster recovery in Gulf exports and a sustained increase in US crude inventories toward the five-year seasonal average would indicate improving supply conditions and could increase downward pressure on crude prices. The next EIA Weekly Petroleum Status Report and the FOMC minutes will provide fresh signals on supply and macro conditions. Key indicators include whether US crude inventories continue to rebuild and whether four-week average crude imports recover toward recent historical levels.

Analyst's Notes

Subscribe to Our Channel

Stay Informed