Grade, Infrastructure & Partnership Underpin Selkirk Copper Growth

.webp)

High-grade Yukon copper restart w/ 6-10% grades, $330M+ infrastructure, 20% First Nation equity, cleared streams. targets mid-2028 production.

- Selkirk Copper Mines is advancing a high-grade copper restart in Yukon with production targeted for mid-2028, featuring exceptional grades of 6-10% copper across 85+ lenses and 91% recovery rates, positioning it among the world's highest-grade concentrate producers

- The company benefits from $330M+ in existing infrastructure including processing plant, roads, and power, reducing estimated restart capital to ~25% of greenfield equivalent, with the bankruptcy clearing financial incumbrances including a legacy gold-silver stream

- Selkirk First Nation holds ~20% equity in the company - the first time a First Nation has held largest equity interest in a publicly traded mining company - creating strong alignment and exploration opportunities in a district that hasn't seen modern exploration for 50 years

- The project produces premium 39-40% copper concentrate (top 5% globally vs 26-28% industry average) from a co-product mine generating 65% revenue from copper and 35% from gold/silver, with minimal deleterious elements making it highly attractive to smelters for non-dilutive financing

- Recent Phase 1 drilling achieved 87% success rate across 175 holes, with results in the top 98-99th percentile of 60+ years of historical data, demonstrating improved geological understanding and vectoring capabilities that support a 12-15 year mine life targeting 30,000 tons/year copper equivalent

In a mining sector increasingly focused on near-term production and lower-risk development opportunities, Selkirk Copper Mines presents a compelling restart story built on exceptional geology, substantial existing infrastructure, and an unprecedented partnership with the Selkirk First Nation. President and CEO Colin Joudrie, a geoscientist with decades of experience spanning global copper development projects, outlined the company's path to mid-2028 production in a detailed discussion covering technical advantages, capital efficiency, and the strategic approach guiding this Yukon copper-gold-silver project.

The Grade Advantage

The Selkirk project stands out for its geology. The deposit comprises a series of lenses consisting almost exclusively of chalcopyrite and bornite, with minimal other sulfides - a rare configuration that translates directly into exceptional grades and metallurgical performance. Joudrie emphasised this fundamental advantage:

"When you're getting decameters like 10-15 meter intervals of 6 to 10% copper, that by definition is not just rare, it's almost unique."

The deposit contains over 85 identified lenses, each exhibiting similar characteristics despite structural disruption. These lenses typically measure approximately 150 meters wide, 50 meters thick, and up to 400 meters long, with a recognisable periodicity that aids targeting. The geological team has identified structural controls that keep the lenses coherent, with edge effects that are increasingly predictable. This understanding has enabled the company to vector toward high-grade zones with unprecedented precision.

The ore bodies feature a distinctive zonation pattern. An outer shell contains moderate grades of 0.7-2% copper with slight structural deformation, followed by a high-grade core where structural fabric intensifies and sulfides behave plastically. The highest-grade zones - including intervals exceeding 20% copper - occur where sulfides have mobilised "like toothpaste" within the most deformed sections. This predictable architecture provides multiple advantages for mine planning and selective mining strategies.

Built-in Capital Efficiency

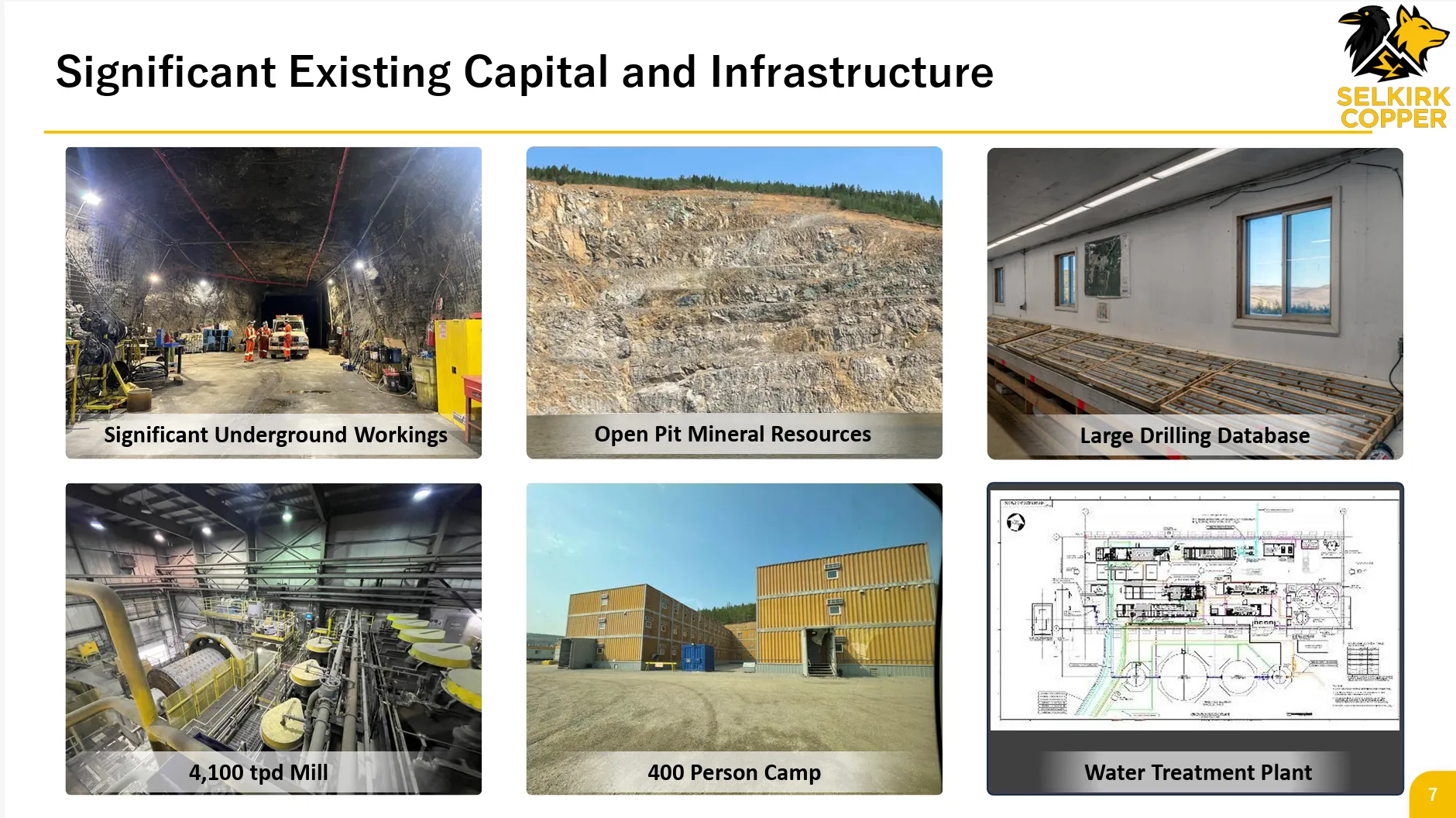

Perhaps the most significant financial advantage stems from existing infrastructure. Over $330 million has been invested in above-ground facilities, including a 4,100-ton-per-day processing plant featuring SAG-ball mill configuration, roads, and power infrastructure. Joudrie explained the strategic implications:

"Most major mining operations or potential major mining operations today are not actually mines. They're massive infrastructure undertakings where people are building ports, roads, power lines, power plants. We don't have to do that."

The company estimates restart capital at approximately 25% of what an equivalent greenfield project would require - roughly $225 million versus $800-900 million for a comparable new development. This capital efficiency derives not only from existing facilities but also from the company's measured approach to refurbishment and enhancement rather than wholesale replacement.

Planned capital investments focus on three main areas: mill upgrades including a permanent three-stage crushing circuit and updated tailings filtration equipment; mine development including pre-strip for the Ridgetop open pit and a new adit to the Minto Northwest zone; and waste, water, and tailings management infrastructure. Additional investments in energy efficiency, such as variable speed drives on the mills, are justified by the projected 12-15 year mine life with extension potential.

Unprecedented Indigenous Partnership

The Selkirk First Nation's ~20% equity position represents a groundbreaking structure in the mining industry - the first time a First Nation holds majority equity interest in a publicly traded mining company globally. This partnership emerged from the bankruptcy process and fundamentally differentiates Selkirk Copper's operating environment and exploration potential.

Joudrie recounted a pivotal conversation with First Nation leadership:

"I said, 'What would be success for you folks?' And they said, 'If the work is done well.' That's all they basically said. They just said, 'We really just want the work to be done well.'"

This alignment on operational excellence rather than purely financial metrics creates a foundation for long-term value creation.

The partnership unlocks exploration potential that previous operators could not access. The district hasn't seen modern exploration for nearly 50 years, presenting a significant opportunity for resource expansion beyond the current 12-15 year mine plan.

Interview with Chief Executive Officer, Colin Joudrie

Proving the Geological Model

Selkirk's Phase 1 drill program delivered an 87% success rate across 175 holes, with recent results ranking in the top 98-99th percentile of the project's 60+ year drilling history. This performance reflects both improved geological understanding and disciplined targeting methodology.

The team's approach prioritised geological description over model-fitting. By asking geologists to describe what they observed rather than confirm a predetermined model, the company identified structural controls and periodicity patterns that enhance predictive capability. For the first time at the project, oriented drill core is being collected, adding further geological insight.

The program balanced extension drilling on known lenses with exploration targeting of high-grade intercepts that previous operators hadn't followed up, including notable intersections like 5 meters of 11% copper. The extensive historical database - 390,000 meters of drilling - was fully digitised and made available in 3D space, enabling the team to identify opportunities that weren't obvious in legacy formats.

Premium Product Positioning

The project's metallurgical characteristics create significant commercial advantages. The operation achieves 91% copper recovery over the mine life - and as Joudrie noted, "they really didn't even try very hard" - suggesting potential for further optimisation. The simple mineralogy of chalcopyrite and bornite with minimal other sulfides enables coarse grinding to approximately 200 microns, with the company exploring even coarser grinds to reduce energy consumption while maintaining recovery.

The concentrate grade of 39-40% copper places Selkirk in the top 5% globally, compared to an industry average of 26-28% that continues declining as ore grades decrease worldwide. This premium product with minimal deleterious elements is well-known in smelter markets, where it commanded interest historically and represents a scarce supply option.

The concentrate quality creates financing optionality. The company can potentially monetise offtake agreements as a source of non-dilutive capital for the restart. Previous offtake arrangements with Wheaton and Sumitomo were eliminated through the bankruptcy, giving Selkirk full control of its production for the first time. Discussions are already underway with smelters, traders, traditional project financiers, private equity groups, and Canadian critical minerals funds.

Emerging from Bankruptcy Unencumbered

The project operates as a co-product mine generating approximately 65% of revenue from copper and 35% from gold and silver (predominantly gold at 31-32%). Critically, the bankruptcy process eliminated a gold-silver stream dating to 2007 that had encumbered the asset through multiple ownership changes. Joudrie characterised this as transformative: "Removal of that stream is just a game-changer for the asset from a financial and operating perspective."

Combined with metal price appreciation of 150-200% across copper, gold, and silver since the May 2023 bankruptcy, the economic fundamentals have shifted dramatically. The company now owns 100% of the ore with no legacy streaming obligations, positioning it to capture the full value of a favourable pricing environment while maintaining operational flexibility.

The Path to Production

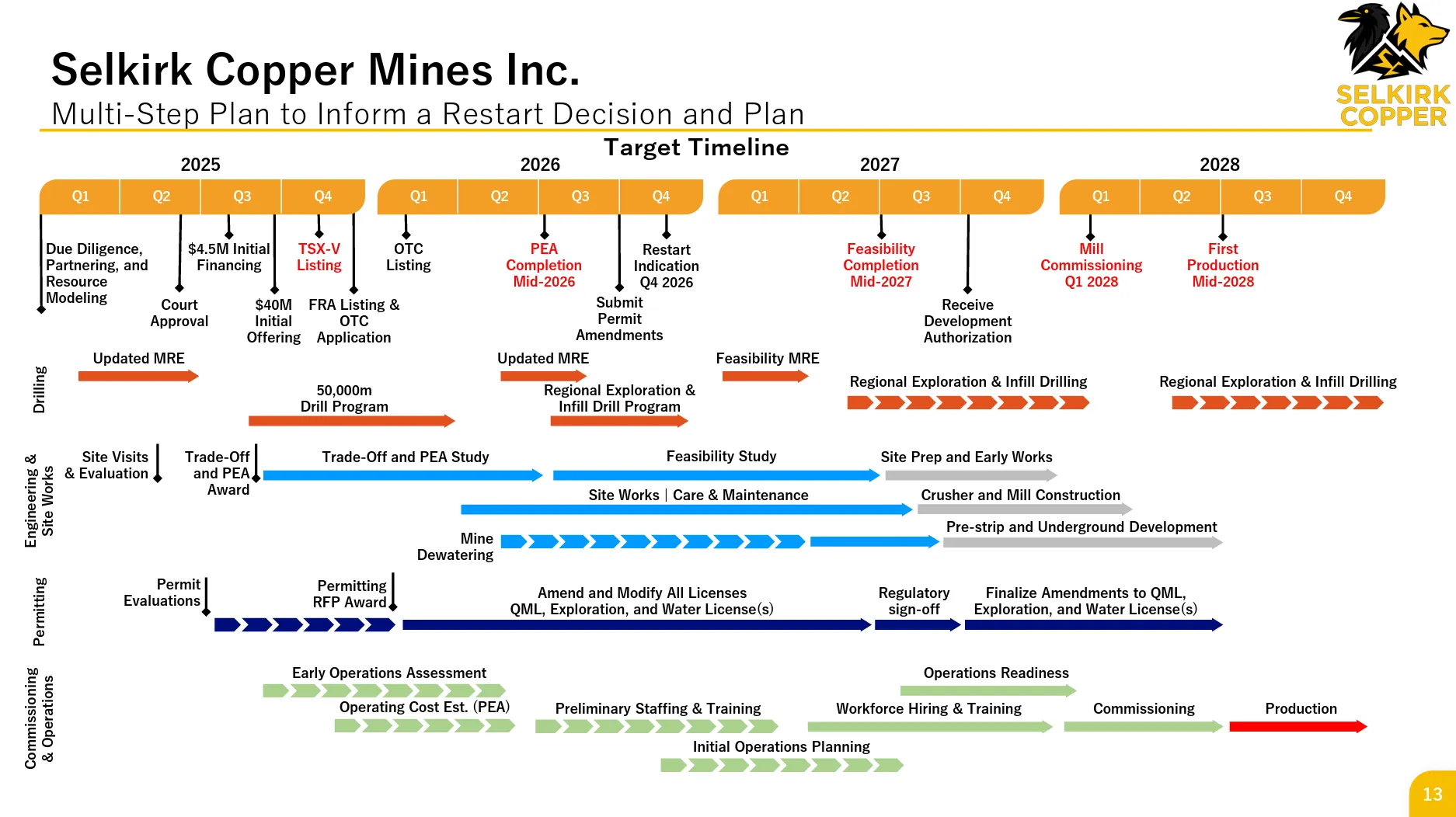

Selkirk targets a preliminary economic assessment (PEA) in mid-2026, followed by a feasibility study in 2027 and a restart decision by mid-2027, with production commencing in mid-2028. This timeline reflects Joudrie's philosophy of "measure twice, cut once" rather than rushing into production.

The approach balances competing stakeholder pressures - some advocating for aggressive drilling, others pushing for immediate restart - by maintaining focus on comprehensive planning. The company is taking time to understand water management, permitting, community interaction, and technical details that previous operators may have assumed rather than verified. With $35 million raised in the most recent financing, the company has sufficient capital to reach mid-2027 milestones, with the main uncertainty being the pace of assuming care and maintenance responsibilities from government and receivers.

The target production profile envisions 30,000 tons per year copper equivalent over a 12-15 year mine life, with extension potential supported by ongoing exploration. The company has already identified 12-13 years of mine life from resources integrated into current mine plans, with 85+ lenses providing substantial optionality for sequencing and optimisation.

The Investment Thesis for Selkirk Copper

- High-Grade Copper Leverage: Exceptional grades of 6-10% copper across 85+ lenses with 91% recovery rates and 39-40% concentrate quality (top 5% globally) in a market where average concentrate grades continue declining

- Cleared Financial Incumbrances: Bankruptcy eliminated legacy gold-silver stream from 2007, giving company 100% ore ownership in favorable pricing environment (150-200% metal price appreciation since May 2023)

- Indigenous Partnership Advantage: Selkirk First Nation's ~20% equity position (first in global publicly traded mining) provides social license, operational alignment on excellence, and exploration access to district untouched by modern exploration for 50 years

- Near-Term Production: Mid-2028 production target with PEA mid-2026, feasibility 2027, and restart decision mid-2027 - rapid timeline for sector while maintaining disciplined approach

- Premium Product for Non-Dilutive Financing: High-grade concentrate with minimal deleterious elements known to smelters creates optionality for offtake-based financing, reducing equity dilution

- Resource Growth Potential: 87% Phase 1 drill success rate with results in top 98-99th percentile historically, improved geological understanding supporting 12-15 year mine life with extension opportunities

- Experienced Leadership: CEO Colin Joudrie brings decades of global copper development experience including six years managing Tech's copper development portfolio across six large Americas assets

- Proven Deposit: 390,000m historical drilling, previous production demonstrates extractability, with enhanced understanding of structural controls and zonation enabling better mine planning than historical operators

- Strategic Timing: Copper supply constraints, energy transition demand, and critical minerals focus align with project's production timeline and premium product characteristics

Selkirk Copper exemplifies the mining industry's pivot toward low-risk, near-term copper production amid intensifying supply constraints and energy transition demand. The project addresses a critical market need: high-grade copper concentrate production in stable jurisdictions with existing infrastructure and established social license. As global average ore grades decline - reflected in the industry's 26-28% concentrate grades versus Selkirk's 39-40% - projects delivering premium products with minimal capital intensity command significant strategic value. The Yukon jurisdiction, combined with First Nation partnership, positions Selkirk within Canada's critical minerals strategy while sidestepping permitting and infrastructure challenges plaguing greenfield development. As Joudrie noted:

"The best way to [make money] is not to have to spend money on the stuff that doesn't make money."

This capital efficiency, combined with favourable commodity pricing and cleared legacy obligations, creates a compelling value proposition for investors seeking leveraged copper exposure without typical development risks.

TL;DR

Selkirk Copper is restarting a high-grade Yukon copper-gold-silver mine with exceptional geology (6-10% copper grades, 91% recovery, 39-40% concentrate quality in top 5% globally), $330M+ existing infrastructure reducing restart capital to ~25% of greenfield equivalent (800-900M), and an unprecedented 20% equity partnership with Selkirk First Nation providing social license and exploration upside. The bankruptcy cleared legacy streams, giving the company 100% ore ownership in a favorable pricing environment, with mid-2028 production targeted following PEA (mid-2026), feasibility (2027), and restart decision (mid-2027).

FAQs (AI Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

%20(1).jpg)

Stay Informed