Undervalued Junior Miner: Strong Cash Flow, Big Growth Plans: Mineros Realising Growth

Mineros CEO discusses Q1 record results, 0.49x P/NAV valuation discount, Nicaragua expansion, Porvenir development, and path to 500k oz production by 2030 with strong cash returns.

- Mineros delivered 61,000 oz gold equivalent production with $154M EBITDA in Q1, exceeding upper guidance range while costs came in below lower guidance range

- Trading at 0.49x P/NAV compared to peer group average, with $220M in cash and gold assets against $1.2B market cap and minimal debt

- Processing capacity increasing 50% from 1,750 to 2,500 tons per day to eliminate bottleneck, with 11,000 oz inventory awaiting processing

- Executing $30M dividend program and $80M buyback while funding 100km exploration program and advancing Porvenir project ($200M capex, 70k oz target)

- Targeting 300,000 oz production near-term and 500,000 oz by 2030 through operational improvements, Porvenir development, and strategic acquisitions

Mineros S.A., a 50-year-old gold producer with operations in Colombia and Nicaragua, presents a noteworthy case study in market mispricing according to CEO Daniel Henao. Despite recently achieving record operational and financial performance, the company trades at a significant discount to peers while simultaneously returning capital to shareholders and funding multiple growth initiatives. The company's public listing on the TSX during the pandemic period means many North American and European investors are encountering the Mineros story for the first time, creating what management views as a unique investment opportunity.

Operational Performance and Financial Results

Mineros reported substantial improvements in its first quarter results, demonstrating operational momentum across multiple metrics. The company produced 61,000 ounces of gold equivalent, tracking toward or exceeding the upper end of full-year guidance of 233,000 ounces. Revenue reached $292 million for the quarter, generating EBITDA $154 million. Gross profits increased 122% to $143 million, while net profit totaled $88 million. These results reflect not merely the benefit of higher gold prices but fundamental operational improvements being implemented across the asset base.

Silver production emerged as a particularly notable success story, increasing 109% year-over-year with revenues jumping 450% due to improved recovery rates. Management attributes this to focused technical efforts on metallurgical optimisation. Similarly, gold recovery rates have improved from 87% to beyond 90%, contributing to enhanced economics independent of commodity price movements. In Nicaragua specifically, gold production increased 22% in the first quarter as the company began executing on its operational improvement initiatives.

The company maintains a strong balance sheet with approximately $220 million in liquid assets comprising both cash and gold bullion. Management has adopted an updated treasury policy to build gold exposure, accumulating physical bullion in vaults in Switzerland and the United States. This financial position supports multiple simultaneous initiatives including capital returns, exploration, and project development.

Valuation Analysis

Management emphasises a significant disconnect between operational performance and market valuation. The company trades at 0.49 times price-to-net asset value, well below peer group averages, despite growing its NAV through operational improvements and project advancement. From a cash flow perspective, Mineros generated approximately $500 million of EBITDA over the trailing twelve months, supporting management's view that the valuation fails to reflect current earnings power.

Henao stressed the company's present-tense execution rather than forward-looking promises:

"We are delivering value right now. This is our reality. This is not a plan."

With a market capitalisation around $1.2 billion, minimal debt, and over $200 million in cash and gold assets, the company's enterprise value metrics appear compressed relative to both asset base and earnings.

The valuation discount persists despite the company's recognition as a TSX 30 honoree, indicating it outperformed 98% of all TSX-listed companies across sectors. Management attributes the current market pricing partially to the company's recent entry into North American public markets and ongoing profit-taking by early investors who achieved substantial returns.

Nicaragua Operations and Expansion

The Nicaragua operation represents the company's primary growth engine, currently producing 140,000 to 150,000 ounces annually with significant near-term expansion potential. The operation features a unique business model incorporating the Bonanza Mining Partnership, where artisanal miners operate within Mineros' concessions under a three-party agreement involving the company, miners, and local government. Mineros purchases ore from these miners at approximately 40-50% of spot prices, creating favorable economics while supporting community employment.

The critical operational constraint in Nicaragua has been processing capacity, which management is addressing through a 50% expansion from 1,750 to 2,500 tons per day. Previous management had responded to this bottleneck by curtailing mine production, which the current team reversed immediately upon taking control. The company's owned mines, Pioneer and Panama, saw cash costs decline from approximately $3,000 per ounce to $1,200 per ounce by running at full capacity, with excess ore building inventory for future processing. As of quarter-end, approximately 11,000 ounces worth of ore sat in stockpiles awaiting the expanded processing capacity.

Additional improvement initiatives in Nicaragua focus on grade control, mine planning optimisation, and dilution reduction. Management describes these as "quick ounces" programs already showing results in current production figures.

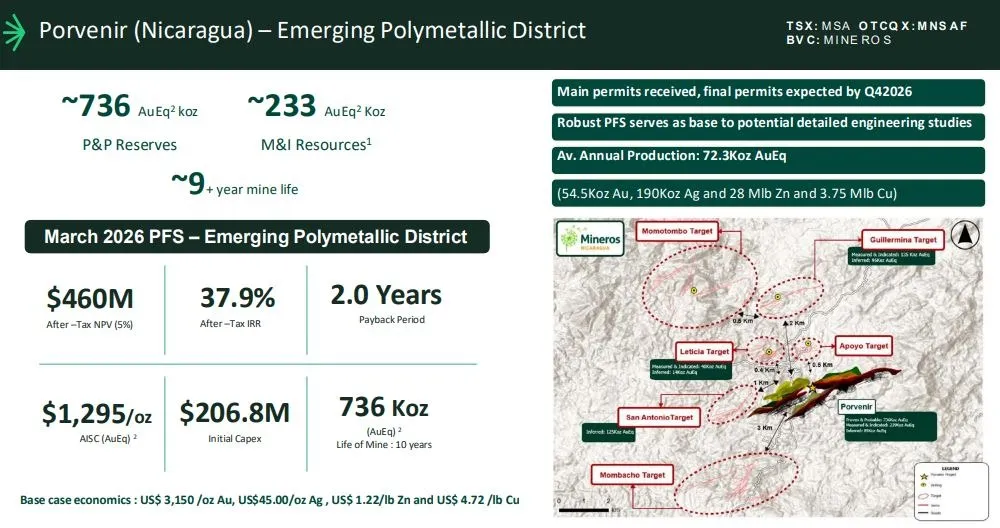

Porvenir Development Project

The Porvenir project in Nicaragua represents the company's clearest path to near-term production growth. The pre-feasibility study envisions a $200 million capital investment producing approximately 70,000 ounces of gold equivalent annually with a 38% internal rate of return at $3,150 gold. Current gold prices substantially above this assumption improve project economics materially.

Development momentum has accelerated under current management. The project recently received major environmental permits for the tailings facility several months ahead of initial guidance, which management credits to productive engagement with regulatory authorities regarding project benefits. With the mine itself already permitted, remaining approvals are progressing while detailed engineering work advances in parallel.

The project's location immediately southwest of existing producing mines provides infrastructure advantages and operational synergies. Management has designed the initial 2,000 tons-per-day processing facility with explicit expansion capacity to double throughput, reflecting confidence in the district's resource potential. Exploration around Porvenir continues with encouraging results suggesting the asset may evolve into a district-scale opportunity exceeding initial project parameters.

Colombian Operations and Strategic Stability

The Colombian operation provides production stability and cash flow consistency, having operated continuously for over a century. Current production approximates 90,000 ounces annually using gravity recovery methods without chemical processing, powered by the company's own hydroelectric generation. This low-risk operational profile generates strong margins despite representing a smaller portion of company-wide output.

The asset holds a 12-year reserve life with an additional one million ounces in measured and indicated resources beyond current reserves. Management views Colombia as the next phase of operational improvement after addressing more immediate opportunities in Nicaragua, with recovery rates already improving from 84% to 87% under current initiatives.

Interview with Daniel Henao, CEO, Mineros S.A.

Capital Allocation Strategy

Mineros demonstrates the ability to simultaneously fund multiple priorities from operating cash flow. The board approved a $30 million dividend program for the current year alongside an $80 million share buyback authorisation, with the first phase of buyback activity announced concurrent with first quarter results. Management frames the buyback as both value return and tactical response to selling pressure from early investors realising profits, describing the company's own shares as its best current investment opportunity.

Simultaneously, the company launched what management characterises as its most aggressive exploration program historically, planning 100 kilometers of drilling across its three jurisdictions. Ownership of drilling rigs enables all-in drilling costs below $100 per meter, providing cost-efficient exploration relative to contractors. This exploration program encompasses existing operations, Porvenir expansion potential, and newer acquisitions including assets in Chile's Maricunga district and a large Colombian project with 24 million ounces of resources.

Growth Trajectory and Strategic Vision

Management has established clear production targets: achieving 300,000 ounces in the near term, then reaching 500,000 ounces annually by 2030. The near-term target builds on current production of approximately 230,000 to 240,000 ounces through Nicaragua expansion and Porvenir commissioning. Henao emphasised:

"We're not selling a dream. We're selling a reality."

The longer-term 500,000-ounce objective incorporates Colombian expansion, continued exploration success, and development of recently acquired assets. Management believes achieving this scale will fundamentally shift market perception and valuation, making the company impossible to ignore within the mid-tier gold producer segment.

Mineros S.A. presents a case study in operational execution potentially mispriced by public markets. The company combines immediate cash flow generation and capital returns with funded growth initiatives across multiple time horizons. Record recent performance stems from operational improvements rather than solely commodity price benefits, with management implementing systematic programs targeting recovery rates, processing capacity, and cost reduction. The balance sheet supports simultaneous dividends, buybacks, exploration, and project development without requiring external capital.

Primary risks include execution on capacity expansion, permitting and construction timelines for Porvenir, and exploration success in proving up district-scale resources. The valuation discount to peers appears substantial if the company achieves stated production targets while maintaining current cost performance, though investors must weigh jurisdiction risk in Nicaragua and Colombia against the operational track record and growth potential management describes.

TL;DR: Executive Summary

Mineros S.A. trades at 0.49x P/NAV despite generating $154M EBITDA in Q1 alone and holding $220M cash/gold with minimal debt. The company is executing simultaneous capital returns ($30M dividends, $80M buyback) while funding Nicaragua processing expansion (+50% capacity), advancing the Porvenir project (70k oz, $200M capex), and running 100km exploration program. Management targets 300k oz near-term and 500k oz by 2030, with Q1 results already exceeding guidance on production while beating cost targets.

FAQ's (AI Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

%20(1).jpg)

Stay Informed