High Energy Costs and Persistent Fed Tightening are Exposing North America's 25-year Supply Deficit in Domestic De-icing Salt Production

Fed tightening and $120 oil expose North America's 25-year salt supply deficit, revealing structural dependence on imports amid rising transport costs.

- The April 29, 2026 Federal Open Market Committee meeting signaled that interest rates may remain restrictive for longer as the Federal Reserve prioritizes inflation control over growth support, despite slowing economic momentum.

- Brent crude approaching $120/barrel materially impacts the economics of the salt industry because de-icing salt is a diesel-intensive, transportation-heavy bulk commodity business.

- Higher energy costs compress margins across trucking, rail, marine freight, underground mining operations, and mobile equipment fleets, creating cost inflation throughout the salt supply chain.

- North America's structural reliance on imported de-icing salt creates strategic opportunities for new domestic supply projects, particularly low-cost, long-life assets located near existing infrastructure.

- Developing companies may benefit from scarcity value and regional supply deficits, but elevated discount rates and financing costs remain critical variables investors must monitor.

Why the April FOMC Meeting Matters to the Salt Market

The Federal Reserve's April 29 meeting was not directly about mining commodities, industrial minerals, or de-icing salt. Yet the policy implications from that meeting may materially reshape the economics of North America's bulk salt market over the next several years.

The Fed's decision to maintain rates at 3.5–3.75%, combined with Chair Jerome Powell's acknowledgment that inflation remains elevated due to energy and tariff shocks, reinforces higher transportation costs, more expensive project financing, persistent inflation in industrial inputs, and elevated municipal budget stress.

Demand remains relatively resilient, and supply economics are deteriorating. This creates potential opportunities for low-cost domestic producers and developers capable of operating profitably under prolonged inflationary conditions.

Atlas Salt Inc. is advancing a development-stage salt project in Newfoundland and Labrador with 95.0 million tonnes of proven and probable reserves grading 95.9% sodium chloride, 868 million tonnes of inferred resources grading 95.2% sodium chloride, and a planned 4 million tonnes per annum production capacity, according to the company's September 2025 Updated Feasibility Study. The project's location approximately 2 kilometers from the deepwater port at Turf Point potentially reduces transportation complexity relative to more remote inland operations.

The company's Chief Executive Officer & Director, Nolan Peterson, frames the context around municipal procurement security:

"The primary customer for our salt is cities and governments and in many cases, they are legally obligated to purchase salt to de-ice roads for liability reasons. This is kind of the best customer anybody could ever ask for."

The Fed's Inflation Fight Is Now an Industrial Commodity Story

The April 29, 2026 FOMC meeting reinforced that the Federal Reserve remains primarily focused on inflation persistence rather than short-term economic stimulus. Two inflationary drivers stand out: the US-Iran energy shock and tariff-related goods inflation.

Oil at $120 & the Repricing of Bulk Commodity Logistics

Salt mining is unusually exposed to transportation inflation because the product itself is low value per tonne, high volume, and freight-intensive. Unlike precious metals, where transport costs represent a negligible share of realized value, salt economics depend heavily on efficient logistics.

As Brent crude approaches $120/barrel, delivered costs increase materially and margin compression accelerates for higher-cost suppliers. This becomes especially important in imported salt markets where overseas freight economics deteriorate rapidly during energy spikes. For North American buyers, the cost differential between imported Chilean or Egyptian salt and domestic supply narrows as ocean freight rates increase, creating potential pricing advantages for regionally proximate producers.

Tariffs & Equipment Inflation Add a Second Cost Layer

For mining projects, tariff impacts affect mobile equipment, ventilation systems, conveyors, crushing infrastructure, and steel-intensive underground development. For developers advancing greenfield projects, higher capital intensity can materially alter net present value calculations, internal rate of return assumptions, payback periods, and debt serviceability.

Why the North American Salt Market Faces Supply Pressure

North America already operates within a structurally tight de-icing salt market. The region remains dependent on imported supply despite substantial seasonal demand variability.

The winter of 2026 exposed vulnerabilities in North American road salt inventories. Eastern Ontario municipalities faced stockpile depletion risks during January and February 2026, highlighting recurring challenges in market structure.

Salt demand spikes suddenly during severe winters, inventories are difficult to replenish quickly, transportation bottlenecks emerge during peak demand periods, and municipal buyers compete simultaneously for supply. Unlike metals markets, substitution options are limited because sodium chloride remains the most cost-effective de-icing material and municipal infrastructure is designed around traditional salt usage.

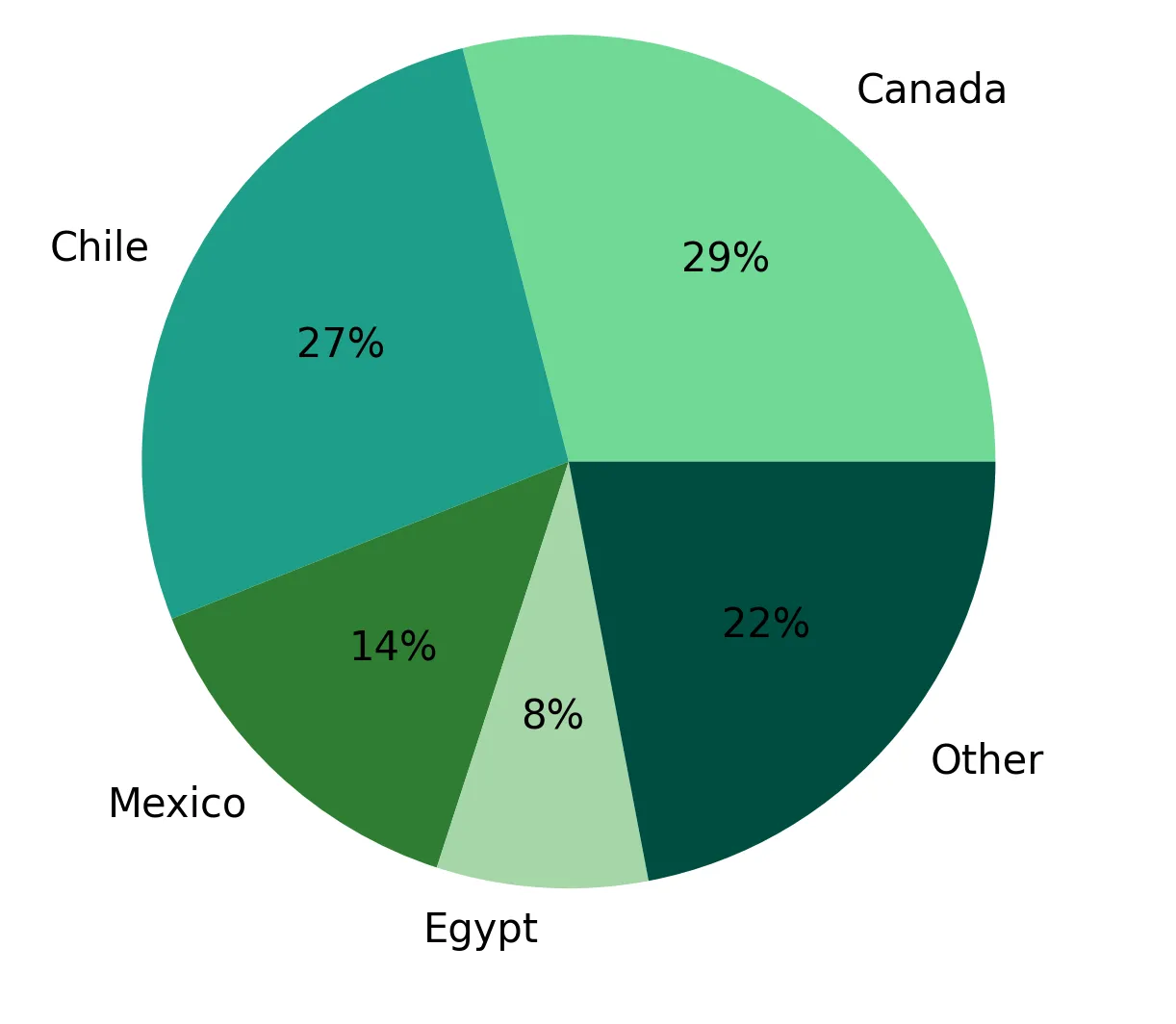

Imported Salt Dependence Is Becoming a Strategic Vulnerability

North America imports approximately 8–10 million tonnes per annum of de-icing salt supply. The United States alone imported 67.5 million tonnes of salt from Egypt, Chile, Mexico, and the Caribbean between 2020 and 2023. This creates exposure to ocean freight inflation, port disruptions, geopolitical shipping risk, currency fluctuations, and energy-linked transportation costs.

This backdrop increasingly favors domestic projects with existing infrastructure access, long reserve lives, low all-in sustaining cost profiles, and proximity to end markets. Atlas Salt's Great Atlantic Salt Project in Newfoundland and Labrador positions within this strategic framework through its proximity to the deepwater port at Turf Point.

Nolan Peterson characterizes the project's positioning within North American supply constraints:

"We aim to supply de-icing road salt to the North American market and we will be the first new salt mine built in North America in 25 years."

The company's September 2025 Updated Feasibility Study outlines an all-in sustaining cost of $34.9/tonne free-on-board Turf Point, a base selling price assumption of $81.67/tonne, an average margin of $74.5/tonne, an after-tax net present value at 8% discount rate of $920 million, and an after-tax internal rate of return of 21.3%. The last new salt mine to open in North America was the American Rock Salt mine in New York, which commenced operations in 2001.

Higher-for-Longer Rates Are Changing Mining Project Economics

Chair Powell's April 29, 2026 statement that his term as Fed Chair ends May 15, 2026, combined with the prospective leadership transition to Kevin Warsh following Senate Banking Committee advancement on April 29, 2026, reinforces that monetary policy continuity remains the Fed's priority.

Discount Rates Matter More in Bulk Commodity Valuations

For institutional investors, the most immediate implication is the persistence of elevated discount rates in project valuation models. When rates remain higher, cost of debt increases, equity financing becomes more dilutive, project hurdle rates rise, and net present value sensitivity worsens.

Bulk industrial mineral projects are particularly sensitive because margins are lower than precious metals, revenue per tonne is smaller, logistics costs are higher, and payback periods are longer. The distinction between high-cost and low-cost operators becomes increasingly important during prolonged inflationary cycles.

Low-Cost Assets Gain Relative Strategic Value

Atlas Salt's September 2025 Updated Feasibility Study outlines metrics that may provide relative insulation against discount rate expansion. The project's all-in sustaining cost of $34.9/tonne positions it favorably within the North American production landscape. The project's shallow geometry and decline access method rather than vertical shaft infrastructure may also reduce capital intensity relative to conventional shaft-based underground mines.

The company signed a Memorandum of Understanding establishing Hatch as the Lead Engineering Partner and Integrated Project Delivery Partner. The company received release from the provincial environmental assessment process in April 2024, with the Newfoundland and Labrador Environmental Minister releasing the project with conditions. Newfoundland and Labrador was rated the 9th best mining jurisdiction globally by the Fraser Institute in 2025.

Nolan Peterson characterizes the permitting and technical risk profile:

"We don't have those bottom three risks: metallurgical, block model, geology, and stakeholder in permitting. We have no metallurgy on our project; salt deposits are very easy to define. Permitting is advanced on this project as we have an approved environmental assessment. "

The company has engaged Endeavour Financial for project finance structuring but has not yet secured a financing package. Investors should remain cautious regarding execution risk during the construction phase, as inflationary pressures on labor, materials, and equipment could materially impact capital expenditure forecasts and project returns if not adequately hedged or contractually protected.

The Investment Thesis for Salt

- North American salt markets face structural supply tightness driven by import dependence and seasonal inventory volatility, creating potential opportunities for domestic producers capable of ensuring reliable winter delivery schedules.

- Elevated oil prices materially improve the strategic value of regional supply chains and infrastructure-linked domestic production, as ocean freight economics deteriorate rapidly when Brent crude approaches $120/barrel.

- Low-cost projects with shallow deposits, existing infrastructure access, and long reserve life become increasingly differentiated under inflationary conditions, as margin durability separates resilient operators from high-cost producers facing compression.

- Higher-for-longer rates favor developers with lower capital intensity, advanced permitting, experienced engineering support, and potential access to debt-weighted financing structures that leverage predictable municipal procurement patterns.

- Investors should remain cautious regarding financing risk, construction inflation, sustained diesel cost escalation, municipal procurement pressure, and execution risk during development, as any of these variables could materially impact project returns.

The FOMC meeting reinforced that inflation, energy costs, and financing conditions are likely to remain central market variables for longer than many investors anticipated earlier in the year.

For the salt market, this matters disproportionately because the industry sits at the intersection of energy-intensive logistics, public infrastructure spending, bulk commodity transportation, and long-duration project financing. What was once viewed as a relatively stable industrial mineral market is increasingly becoming sensitive to macroeconomic volatility and supply-chain security concerns.

The key differentiator may no longer simply be resource size or production scale. Instead, competitive advantage may increasingly depend on resilience in cost structures, infrastructure positioning, financing flexibility, and domestic supply security. In that environment, low-cost North American development projects with strong logistics access may command increasing strategic relevance within institutional commodity portfolios.

TL;DR

The Federal Reserve's April 2026 decision to maintain restrictive rates at 3.5–3.75%, combined with Brent crude approaching $120/barrel, is fundamentally altering North American salt market economics. De-icing salt is a diesel-intensive, freight-heavy bulk commodity business where elevated energy costs compress margins across the entire supply chain. North America imports 8–10 million tonnes annually, creating exposure to ocean freight inflation and geopolitical shipping risk. This structural vulnerability favors domestic projects with existing infrastructure access, long reserve lives, and low all-in sustaining costs. Atlas Salt's Great Atlantic Salt Project in Newfoundland positions as the first new North American salt mine in 25 years, with $34.9/tonne all-in sustaining costs and proximity to deepwater port infrastructure, potentially capturing scarcity value as higher-for-longer rates and persistent energy inflation separate low-cost operators from marginal producers.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed