Geopolitical Risk Pushes Bulk Mineral Deals to 7x EBITDA & Signals Higher Salt Project Valuations

Geopolitical risk, trade uncertainty, and a 7x EBITDA salt acquisition highlight stronger valuations for essential-use bulk minerals and salt projects.

- Capital is rotating toward defensive, essential-use industrial minerals as geopolitical risk premiums and trade policy uncertainty continue through 2026, supporting higher acquisition valuations.

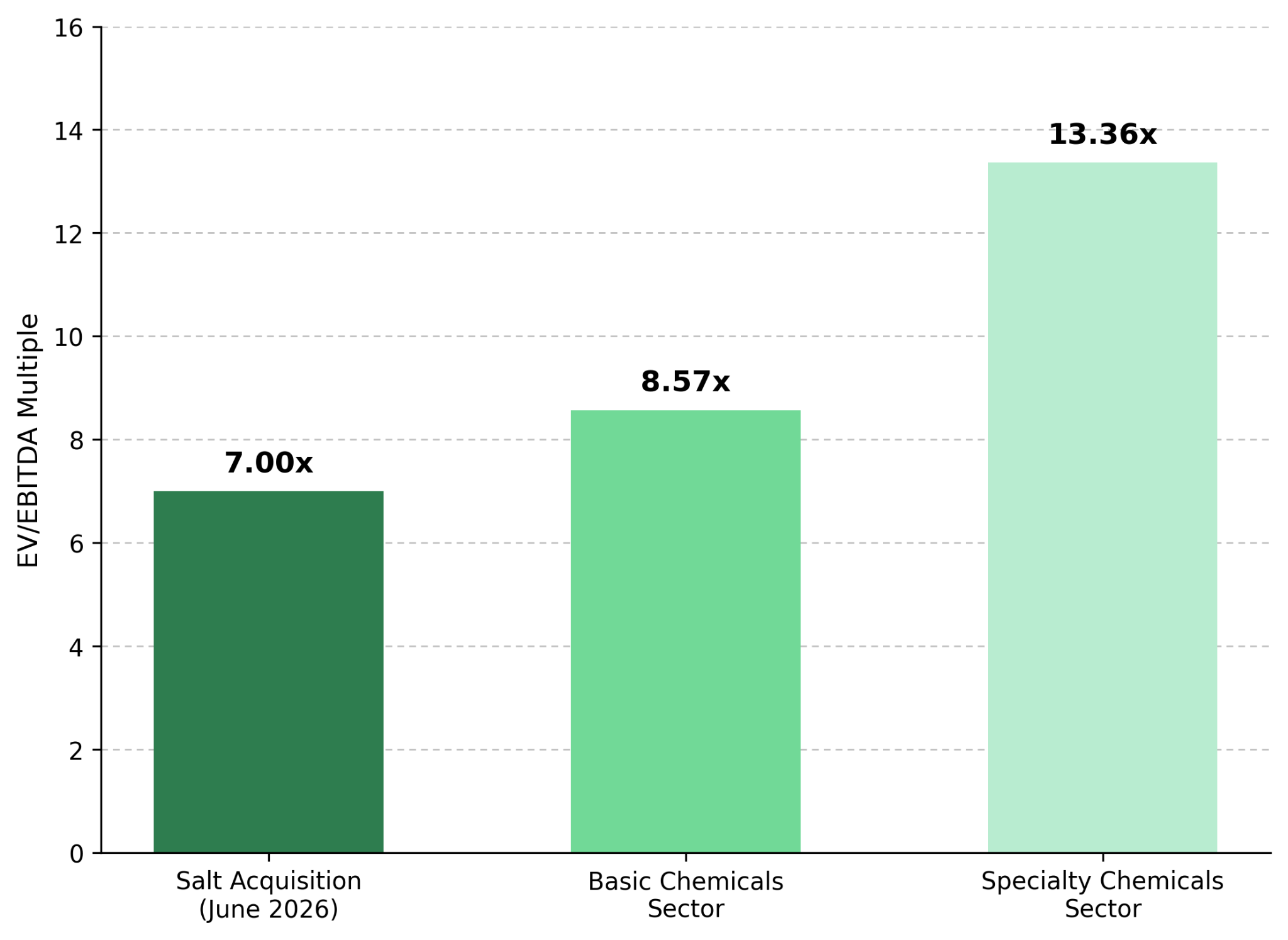

- A recent acquisition of a European evaporated salt business at roughly 7x EBITDA aligns with broader basic chemicals sector trading multiples, indicating buyers value salt in line with the sector.

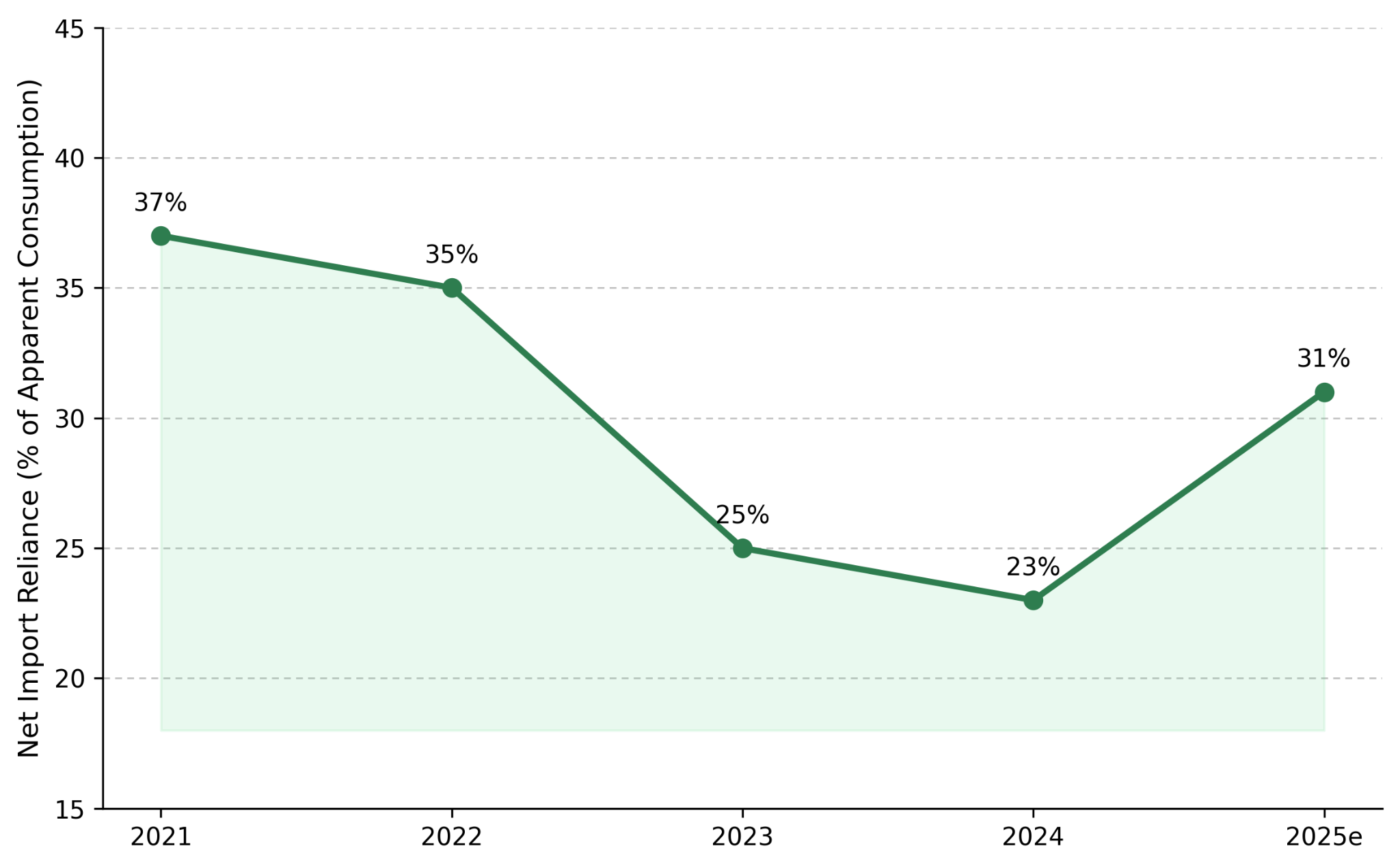

- United States Geological Survey data shows salt in brine and chemical feedstock account for roughly 42% of domestic salt sales, with highway deicing at 37%, while net import reliance rose from 23% of apparent consumption in 2024 to an estimated 31% in 2025.

- The re-rating supports feasibility-backed, permitted greenfield projects in stable jurisdictions by improving financing and acquisition prospects before first production.

- Merger and acquisition multiples, government production data, and price trends are more important indicators than spot prices for tracking capital allocation to bulk minerals.

Trade Uncertainty & Capital Allocation Favor Essential-Use Minerals

Institutional capital allocation in 2026 reflects elevated geopolitical risk premiums, trade policy uncertainty, and commodity market volatility. Geopolitical risk premiums remain elevated, new tariffs on Chinese goods take effect in late July, and cyclical commodities have remained volatile, increasing demand for defensive assets. Allocators managing multi-decade mandates, including pension funds and infrastructure-focused capital pools, are favoring assets tied to essential, non-discretionary demand over those exposed to industrial capital expenditure and construction cycles.

Capital is shifting toward cash-generative bulk minerals supported by stable, non-discretionary demand. Municipal spending on infrastructure maintenance, water treatment, and food security typically continues during slower economic growth, supporting stable demand and cash flow. Salt illustrates this shift because buyers are valuing it in line with the broader chemicals sector.

Acquisition Multiples & Development Projects Improve Financing Prospects

In June, a major European fertilizer and salt producer agreed to acquire two evaporated salt production sites from a Polish chemicals group for €350 million to €380 million. Against 2025 revenue of approximately €125 million and EBITDA of just under €50 million, the deal implies a roughly 7x EBITDA multiple.

The 7x multiple is best assessed against broader chemicals sector valuations. Enterprise value-to-EBITDA data published by New York University Stern School of Business in January 2026 shows the broad chemicals sector trading at 8.57x, with specialty chemicals at 13.36x. A 7x multiple places salt in line with the broader chemicals sector instead of the discount typically applied to bulk commodities. The transaction indicates buyers valued salt in line with the broader chemicals value chain rather than as a discounted bulk commodity. Valuations for producing salt assets in line with the broader chemicals sector may improve financing and acquisition prospects for permitted, feasibility-backed projects before first production.

Diversified Demand & Stronger Pricing Support Acquisition Multiples

According to the United States Geological Survey's (USGS) 2026 Mineral Commodity Summaries, the chemical industry accounted for approximately 42% of US salt sales in 2025, with salt in brine supplying about 90% of chemical feedstock demand for chlorine and caustic soda production. Highway deicing accounted for roughly 37% of total domestic salt consumption, with the remainder split across agricultural use, food processing, general industrial applications, and primary water treatment.

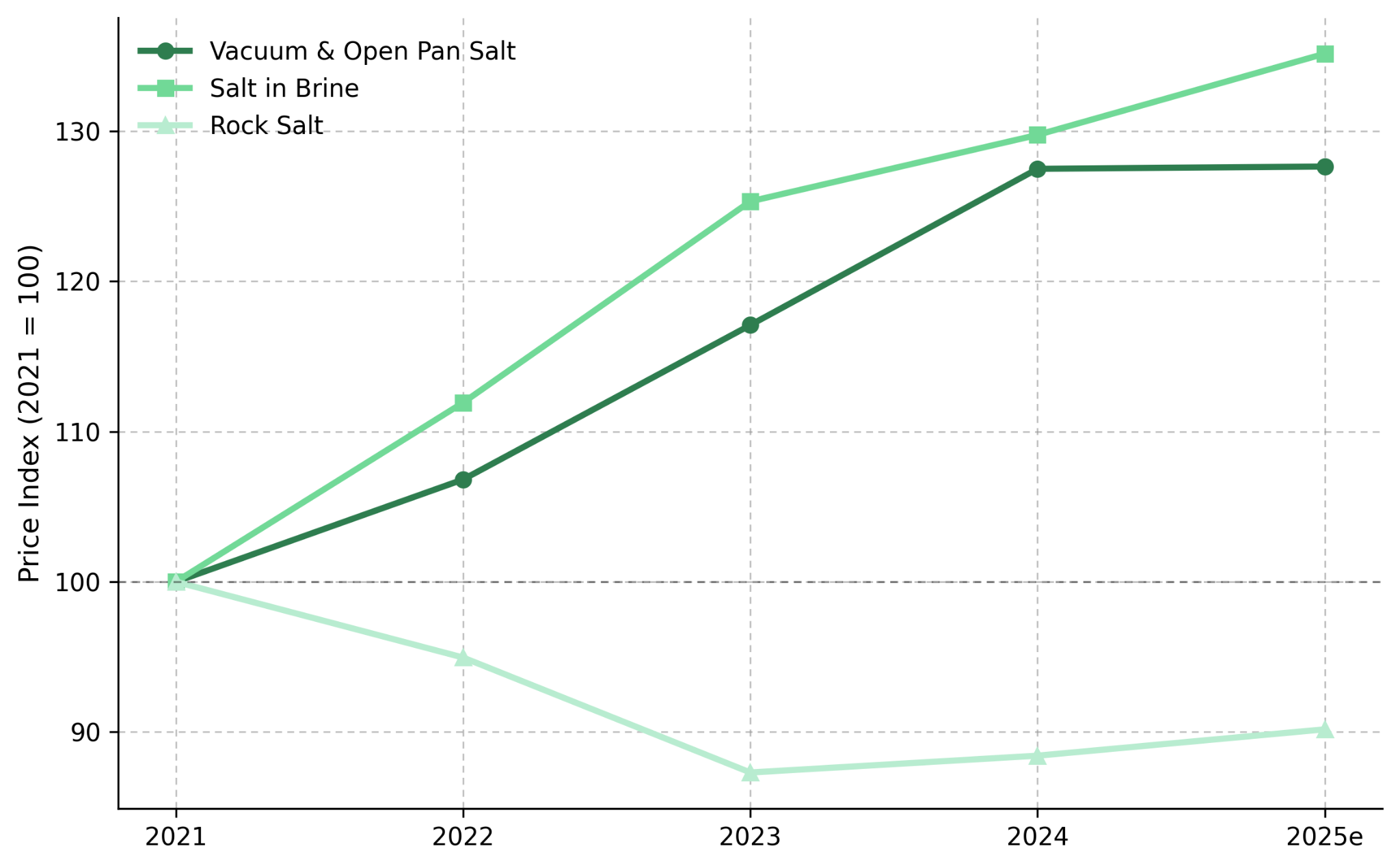

The average free-on-board mine and plant value of vacuum and open pan salt rose from $203.72 per metric ton in 2021 to an estimated $260 in 2025, a gain of approximately 28%. Salt in brine, the chemical feedstock grade tied most directly to chlor-alkali demand, rose from $8.14 per metric ton in 2021 to an estimated $11 in 2025, a gain of roughly 35%, the steepest increase of any salt category the USGS tracks. Rock salt declined from $59.88 per metric ton in 2021 to an estimated $54 in 2025. Chemical feedstock salt recorded the strongest unit-price growth despite China's construction PMI remaining in contraction at 49.0 in June, supporting higher salt valuations.

The USGS reports that most salt applications have no economic substitutes. Calcium chloride, calcium magnesium acetate, hydrochloric acid, and potassium chloride can substitute in deicing, certain chemical processes, and food flavoring, but only at a higher cost. The USGS' 2026 outlook projects chlor-alkali demand growth in Asia, supporting demand for salt in brine used in caustic soda and polyvinyl chloride production. US salt demand remains largely flat, while European demand declines because high energy costs have reduced chlor-alkali capacity. Australia and India have increased salt exports to meet stronger Asian demand, reinforcing Asia as the primary source of demand growth.

Supply Constraints & Project Economics Strengthen Financing Prospects

Atlas Salt's Great Atlantic Salt Project September 2025 feasibility study reported an after-tax net present value, discounted at 8%, of $920 million, an internal rate of return of 21.3%, a 4.2-year payback period, annual production of 4.0 million tons, and approximately $188 million in annual after-tax free cash flow over a 25-year mine life. The project is in Early Works, with site earthworks, road grading, and drainage installation underway under a Town Development Permit issued in April. Mine and plant construction remains contingent on securing a senior secured debt package of approximately $350 million to $400 million, which has not yet been finalized.

Nolan Peterson, President and Chief Executive Officer of Atlas Salt, highlights North America's supply-constrained salt market fundamentals today:

"We're the only project development company looking to put a salt mine into operation, so our market is driven less by demand than by a lack of supply. Even when we come online, we won't disrupt the market. We're the lowest-cost producer, so we don't need to compete on price with our nearest competitor, only with the highest-cost producers."

Import Reliance & Domestic Supply Improve Competitive Position

The US is becoming more reliant on imported salt, increasing the value of domestic supply. USGS data shows net import reliance rose from 23% of apparent domestic consumption in 2024 to an estimated 31% in 2025, while imports increased from roughly 13.9 million tons to an estimated 19 million tons. Mexico supplied 26% of US salt imports over 2021 through 2024, followed by Chile at 23%, Canada at 21%, Egypt at 6%, and other countries at 24%. Canadian mine production rose from an estimated 10.6 million tons in 2024 to 13.0 million tons in 2025, a gain of roughly 23%, reinforcing Canada's role as a key supplier to the North American market.

The USGS reports that a regional rock salt shortage affected New York in early 2025 because of higher weather-related demand and limited supply. Rock salt imports also increased as state and local transportation departments raised consumption relative to 2024. The National Oceanic and Atmospheric Administration forecasts a weak La Niña pattern for the 2025-26 winter. The forecast could support modestly higher rock salt demand in parts of the US. Higher freight and marine fuel costs, ongoing Gulf shipping disruption, and new tariffs increase the cost of imported salt, supporting regionally anchored producers with existing rail, port, and grid infrastructure. US salt production totaled an estimated 40 million tons worth approximately $2.6 billion in 2025. Twenty-five companies operated 60 plants, with seven states accounting for roughly 95% of output, leaving regional supply chains exposed to localized shortages like those seen in New York.

Capital Allocation & Bulk Minerals Shift Valuation Signals

Markets are assigning higher valuations to essential-use bulk minerals such as potash and soda ash because of their stable, non-discretionary demand. Asian chlor-alkali demand growth, European capacity closures, and US net import reliance moving from 37% in 2021 to 23% in 2024 before rising to 31% in 2025 show how regional supply and demand conditions can influence valuations across bulk minerals exposed to energy costs and weather-driven demand.

Merger and acquisition multiples, benchmarked against sector trading multiples and read alongside USGSproduction and price data, provide an early indicator of capital allocation across bulk minerals. Changes in merger and acquisition multiples are more likely to develop over multiple quarters than through near-term commodity price movements.

The Investment Thesis for Salt

- USGS data shows highway deicing accounts for 37% of US salt demand and chemical feedstock for 42%, reducing reliance on any single end market compared with more concentrated industrial minerals.

- Acquisition multiples in line with broader basic chemicals sector benchmarks suggest lenders and strategic buyers may assign higher valuations to development-stage projects serving similar end markets.

- Feasibility-backed, permitted development projects may attract stronger financing and acquisition interest if basic chemicals sector valuations extend to greenfield assets.

- Rising import reliance, concentrated import sources, higher freight costs, and new tariffs increase the relative competitiveness of regionally anchored supply chains over import-dependent competitors.

- Municipal and infrastructure-linked demand provides a demand floor that is less correlated to broader industrial capital expenditure cycles than chlorine and caustic soda-driven consumption, which government data shows is currently diverging sharply by region.

- Key risks include non-binding development financing, weather-driven fluctuations in deicing demand, and continued weakness in Chinese construction, which remains the main driver of chlor-alkali demand.

The June salt acquisition was small by global mining standards, but its 7x EBITDA multiple aligned with broader basic chemicals sector valuations. Combined with five years of production and pricing data, the transaction supports higher valuations for essential-use bulk minerals during elevated geopolitical and trade policy uncertainty. Merger and acquisition multiples, compared with sector trading multiples and USGS supply and pricing data, provide a more useful indicator than spot prices for assessing capital allocation across bulk minerals. These metrics provide the earliest indication of how capital is being allocated across essential-use bulk minerals.

TL;DR

Geopolitical risk, trade policy uncertainty, and commodity market volatility are directing capital toward essential-use bulk minerals with stable demand. A recent European salt acquisition at roughly 7x EBITDA, in line with broader basic chemicals sector valuations, suggests buyers are assigning higher values to salt assets than typically expected for bulk commodities. Data show diversified demand, stronger pricing for chemical feedstock salt, rising US import reliance, and limited substitution, supporting the long-term case for domestic supply. Together, these trends indicate merger and acquisition activity, sector valuation benchmarks, and government supply and pricing data provide better signals of capital allocation than spot prices for development-stage salt and other bulk mineral projects.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed