Mining Companies Recast Long-Life Deposits as Infrastructure Assets, Not Cyclical Bets

Atlas Salt frames Great Atlantic Salt as an infrastructure asset, not a cyclical mining bet, citing 24-year mine life & steady cash flow.

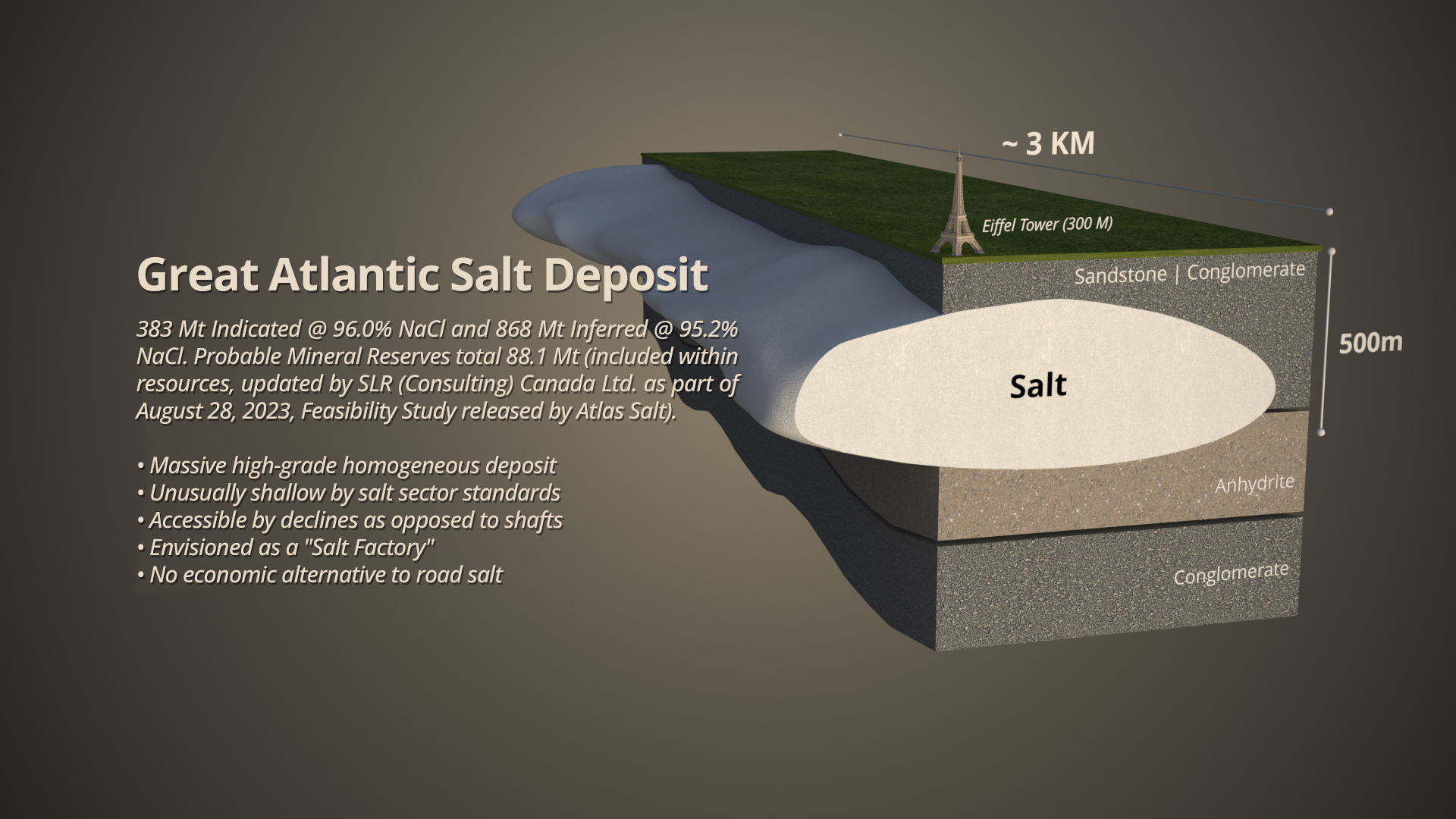

- Atlas Salt Inc. frames its Great Atlantic Salt Project using infrastructure-style language, citing a mine life exceeding 24 years, government-driven demand, and a staged capital return plan rather than a traditional commodity-cycle pitch.

- The company's presentation targets average annual unlevered free cash flow of approximately CA$161 million in years 1 through 8 of production and approximately CA$203 million in years 9 through 24, with shareholder return allocations rising from 50% to more than 90% over that period.

- Comparable transaction data shows established salt producers Compass Minerals, K+S Americas Salt, and US Salt trading at EV/EBITDA multiples of 8.8 times, 12.5 times, and 16.5 times respectively, while Atlas Salt's USD-converted enterprise value of US$104.0 million to US$146.0 million reflects its pre-production status.

- No new salt mine has opened in North America since 2001, and Cargill's 2021 closure of its Avery Island, Louisiana operation removed approximately 2.5 million tons per year of domestic supply from the market.

- Newfoundland and Labrador ranked 9th among global mining jurisdictions in the Fraser Institute's 2025 investment attractiveness survey, and the Great Atlantic Salt Project cleared provincial environmental review in April 2024 after approximately 2 months.

For decades, the pitch to mining investors followed a familiar script: find a deposit, model the commodity price cycle, and promise leveraged upside when prices turn. A parallel narrative has since taken hold among developers of long-life, steady-demand deposits, which increasingly describe their projects using the vocabulary of infrastructure investing: predictable government customers, structurally stable demand, low reinvestment requirements, and eventual capital return through dividends or buybacks.

The distinction matters because it changes who the natural buyer of the equity is. A cyclical mining stock is priced on where a fund manager believes the commodity cycle sits, while an infrastructure-style asset competes against utilities and other long-duration cash flow vehicles, priced on the durability of that cash flow rather than a price forecast.

Atlas Salt Inc. (TSXV: SALT | OTCQX: SALQF | FRA: 9D00), developer of the Great Atlantic Salt Project in Newfoundland and Labrador, Canada, has built its 2026 investor presentation almost entirely around this framing, describing the project as a strategic infrastructure-like asset with a mine life exceeding 24 years and a capital allocation plan that shifts from debt repayment toward dividends and buybacks as the project matures. The positioning offers a useful lens into why mining developers are borrowing the language of capital allocation rather than commodity speculation, and where the limits of that comparison sit.

Industry Context

The case for treating some mining assets as infrastructure rests on structural features that differ from a typical base or precious metals project. According to FactSet data referenced in Atlas Salt's investor materials, the median life of mine for silver operations globally is 7 years, gold is 9 years, and copper is 18 years, based on sample sizes of 52, 352, and 124 operations respectively. Long-duration assets reduce the frequency with which a company must find, permit, and finance a replacement project, shifting the investment question toward capital discipline over that horizon.

Demand stability is the second pillar. Road salt used for winter de-icing is purchased primarily by government and municipal customers, and consumption is tied to weather rather than industrial cycles. United States Geological Survey data show the average price of rock salt in the United States rising at a compound annual growth rate of approximately 4.2% since 2000, a trend Atlas Salt's presentation characterizes as evidence of a recession-resilient commodity, though this depends on continued weather-driven demand.

Emerging Practices & Industry Progress

Companies pursuing the infrastructure framing are structuring financing and capital return plans differently from a typical development-stage miner. Atlas Salt's presentation lays out a two-phase plan tied to its 2025 Updated Feasibility Study: in years 1 through 8, the company targets average annual unlevered free cash flow of approximately CA$161 million, with 50% directed to debt repayment and 50% to shareholder returns. From year 9 through year 24, average annual unlevered free cash flow is targeted at approximately CA$203 million, with more than 90% earmarked for shareholder returns once debt obligations are satisfied.

This kind of explicit, multi-decade capital return schedule is more commonly associated with regulated utilities than a pre-production mining developer. Atlas Salt has structured its financing plan to be debt-weighted, citing cash flow predictability as the basis for that structure, and has engaged Endeavour Financial to lead project financing. The company has also secured a memorandum of understanding with Scotwood Industries LLC, described as the largest distributor of packaged retail de-icing salt in the United States, targeting offtake volumes of 1.25 to 1.5 million tonnes per annum, along with equipment financing and engineering agreements with Sandvik and Hatch Ltd.

Remaining Challenges

The infrastructure comparison has real limits. Unlike a regulated utility, a mining project has no guaranteed rate of return, no captive customer base locked in perpetuity, and no regulator setting allowed revenue. The company's after-tax net present value figures, ranging from CA$0.5 billion (16.9% IRR) at a CA$73.50 per tonne salt price to CA$1.5 billion (25.0% IRR) at CA$89.84 per tonne, show that project economics remain sensitive to commodity pricing even for a supposedly recession-resilient input.

Financing risk is also unresolved. As of June 19, 2026, Atlas Salt's Canadian-dollar enterprise value stood at approximately CA$197.8 million against a pre-production capital expenditure requirement of CA$589 million, meaning most of the project's construction capital has yet to be secured. The company's own Lassonde Curve framing places the project in the trough of pre-project financing, with illustrative price-to-net-asset-value ranges of 0.2 to 0.4 times, below the approximately 1.0 times multiple typically associated with companies that have reached production.

How the Market Prices Comparable Salt Assets

One way analysts compare mining companies is by looking at enterprise value, meaning what the whole company would cost to buy including its debt, and dividing that by EBITDA, short for earnings before interest, taxes, depreciation, and amortization, a rough measure of how much cash the business generates each year. The result, called an EV/EBITDA multiple, shows how many years of that cash flow investors are effectively paying for. A higher multiple usually means the market has more confidence that the cash flow will keep coming.

Using this measure, established salt producers already in production trade at noticeably higher multiples than Atlas Salt, which has not yet built its mine. Compass Minerals, a publicly traded company, has an enterprise value of US$1,952 million and EBITDA of US$222 million, an EV/EBITDA multiple of 8.8 times. K+S Americas Salt was sold to Stone Canyon Industries Holding for US$3,200 million, equal to 12.5 times its 2019 EBITDA. US Salt was valued in a December 2025 ContextLogic investor presentation at US$907.5 million, or 16.5 times its EBITDA of US$55 million. By comparison, Atlas Salt's enterprise value, converted to US dollars at a 1.40x exchange rate, is only US$104.0 million to US$146.0 million. That much lower figure is not a sign the company is cheap in the traditional sense, it reflects the fact that Great Atlantic Salt has not started producing or generating cash flow yet, so there is no current EBITDA to compare it against.

Part of the opportunity for Atlas Salt comes from how little new supply has entered the market. No new salt mine has opened in North America since American Rock Salt's mine in New York began production in 2001. Meanwhile, existing supply has shrunk: Cargill closed its Avery Island, Louisiana salt mine in 2021, removing approximately 2.5 million tons per year from the US east coast de-icing market, and the company has been unable to sell its remaining New York and Cleveland salt operations since starting that process in 2023, reportedly because of environmental concerns tied to those older sites. Great Atlantic Salt is also comparatively shallow and easier to access than many existing mines, sitting approximately 180 meters below surface, compared with other North American salt mines that range from about 250 meters deep, at the Ojibway Mine in Windsor, Ontario, to roughly 1,000 meters deep, at the Picadilly Mine in Sussex, New Brunswick. A shallower deposit is generally faster and less costly to develop.

Jurisdictional Perspective

Newfoundland and Labrador was ranked 9th among global mining jurisdictions by the Fraser Institute in its 2025 investment attractiveness survey, based on mineral content and government policy alignment. The province released the Great Atlantic Salt Project from further provincial environmental review in April 2024 after approximately 2 months, and Atlas Salt's presentation notes the region's existing mining history, including an operating limestone mine and a gypsum mining area active since the 1950s, along with proximity to the Trans-Canada Highway and the Turf Point deep water port approximately 2 kilometers from the site.

That jurisdictional advantage connects to the demand side of the thesis. Media coverage referenced in the presentation described road salt shortages affecting Eastern Ontario municipalities in February 2026 and Canadian road salt being redirected to United States buyers in January 2026, alongside wholesale price increases in Ontario from roughly $65 to $70 per ton to nearly $190 per ton. United States Geological Survey data show 67.5 million tonnes of salt imported into the United States between 2020 and 2023, with Canada, Chile, Mexico, and Egypt as the leading source countries, underscoring the import dependence new domestic supply could address.

Industry Outlook

Whether the infrastructure framing sticks will depend less on messaging and more on execution through the phases the industry itself uses to price development risk. Atlas Salt's presentation frames its path using the Lassonde Curve, a widely used model in mining finance describing how valuation multiples move through discovery, feasibility, financing, construction, and production. The company has completed its feasibility study and environmental assessment and describes itself as shovel ready, with production estimated by 2030, but its remaining milestones, securing a financing package, finalizing strategic partnerships, and completing construction, are the same de-risking steps any development-stage mining company must clear regardless of how its cash flow profile is described to investors.

For the broader industry, the Atlas Salt case suggests a template other long-life, steady-demand developers may increasingly adopt: multi-decade reserve life, demand tied to non-discretionary end uses, and a staged capital return plan aimed at investors who might otherwise avoid mining equities. The approach does not eliminate commodity price, permitting, or financing risk, but it offers a different entry point for capital that prioritizes cash flow visibility over cyclical upside.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed