US Salt Import Reliance Reaches 31% as Domestic Supply Constraints Lift the Value of New Capacity

US salt import reliance reached 31% as aging mines, financing constraints, and limited new supply increase the strategic value of domestic salt projects.

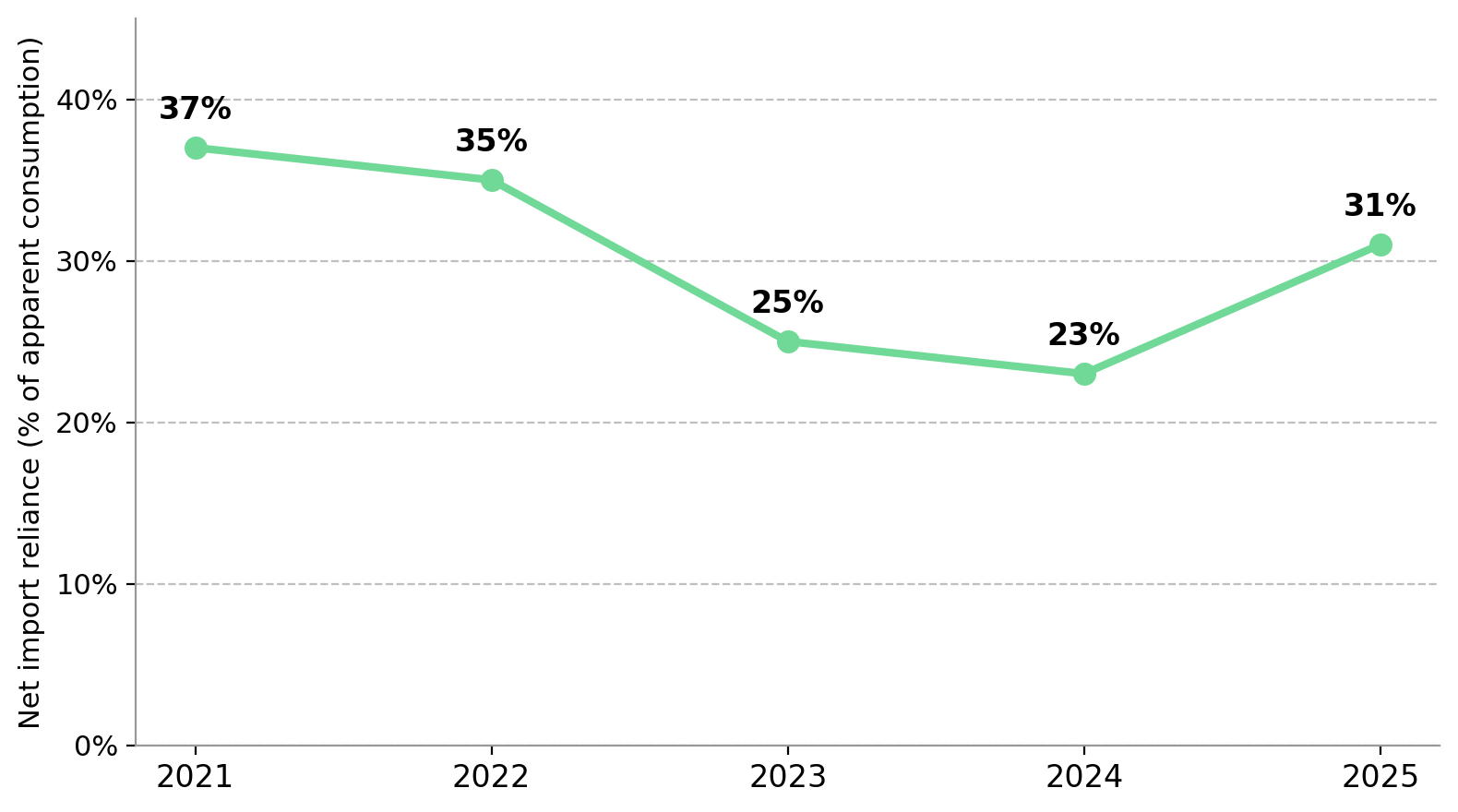

- US net import reliance for salt rose to 31% in 2025 from 23% in 2024, according to the US Geological Survey, indicating that imports supplied a larger share of apparent consumption as domestic production failed to keep pace with demand.

- North America has not opened a new underground salt mine in nearly 25 years, while several existing operations are expected to reach the end of their mine lives within the next five to ten years, limiting replacement capacity and increasing reliance on imported supply.

- The 2026 Strait of Hormuz crisis affects the US salt market primarily through the chlor-alkali value chain, which accounts for roughly 42% of US salt consumption, rather than through demand for road de-icing.

- Salt prices remain relatively stable because demand is anchored by budget-backed road de-icing programs and the chemical industry, both of which continue purchasing salt regardless of broader commodity cycles..

- The opportunity lies with development-stage projects that can add new domestic salt capacity, as rising import reliance and a 25-year gap in new mine construction make replacement supply increasingly valuable without requiring a sharp increase in salt prices.

Rising US Salt Import Reliance & North America's Supply Gap

Salt is rarely viewed as a strategic commodity because it lacks the price volatility and global trading profile of most mined resources. It has no liquid futures market, commands far lower prices than base or precious metals, and is priced primarily through regional supply and transportation costs rather than global commodity benchmarks. The latest US Geological Survey data show that reliance on imports increased sharply in 2025, pointing to a growing gap between domestic supply and consumption. US net import reliance for salt climbed to 31% in 2025 from 23% in 2024, according to the US Geological Survey, meaning imports accounted for a larger share of apparent consumption. An eight-percentage-point increase in a single year indicates that domestic production is not keeping pace with demand, increasing dependence on imported supply.

US salt demand remains stable because road de-icing and chemical manufacturing account for nearly four-fifths of domestic consumption. Highway de-icing accounts for roughly 37% of US salt consumption, while the chemical industry accounts for about 42%, with salt-in-brine supplying nearly 90% of the feedstock used in chlor-alkali production. Domestic production totaled approximately 40 million tons in 2025, but much of that output came from mines that are approaching the end of their operating lives. No new underground salt mine has been built in North America in nearly 25 years, increasing reliance on imported salt from Mexico, Chile, Canada, and Egypt to meet domestic demand.

Because demand for road salt is supported by municipal and state budgets and remains largely inelastic, the key question is whether new domestic supply can replace aging production capacity and reduce reliance on imports. As a result, project execution and new mine development are more important to the thesis than incremental demand growth.

31% Import Reliance Signals Growing Supply Risk

The 31% net import reliance figure comes directly from the US Geological Survey. The data alone cannot determine whether the increase reflects declining domestic production capacity or temporary effects from winter severity and import timing. Regardless of the cause, the data shows that the US relies more heavily on imported salt from a limited number of supplier countries, increasing exposure to supply disruptions if those trade flows are interrupted.

Nolan Peterson, Chief Executive Officer of Atlas Salt, explains how import reliance can affect pricing during winter supply disruptions:

"There's really only upside potential in cold winters, when there are fuel shortages, like we're seeing now, that put pressure on the price and drive the price up, because a lot of our salt is imported."

Strait of Hormuz Risk Shapes Industrial Salt Demand Through Chlor-Alkali

Industrial chemicals, rather than road de-icing, account for the largest source of salt demand in the US. Salt-in-brine is the primary feedstock for the chlor-alkali process, where electrolysis separates brine into chlorine and caustic soda (sodium hydroxide). Caustic soda is used across industries including alumina refining, pulp and paper, polyvinyl chloride production, and water treatment, linking salt demand to a broad industrial customer base. Because chlorine and caustic soda are produced together, changes in demand or pricing for either product affect chlor-alkali production rates and, in turn, demand for salt feedstock.

A Middle East shipping disruption affects the US salt market through the chlor-alkali supply chain rather than through direct salt shipments. The Gulf supplies significant volumes of naphtha, liquefied petroleum gas, and natural-gas derivatives used by the global petrochemical industry. The 2026 Strait of Hormuz crisis, which disrupted shipping from late February through the June diplomatic negotiations, increased risks to the energy and petrochemical inputs used in chlor-alkali production rather than to road-salt supply. A prolonged disruption could increase energy and feedstock costs for chlor-alkali producers, making industrial salt demand more sensitive to production decisions than to road-deicing activity.

The Strait of Hormuz disruption has had little effect on the chlor-alkali supply chain. Crude prices changed little after the latest escalation, and electricity, which represents 40% to 60% of the cash cost of producing caustic soda, has remained broadly stable. At the same time, oversupply in the soda-ash market continues to weigh on chemical pricing. China produces roughly half of the world's soda ash, and continued oversupply has pushed benchmark prices down by double digits year over year, while European producers such as Solvay have reduced capacity in response to weaker market conditions. As a result, chemical-market conditions are currently limiting upside for industrial salt demand despite ongoing geopolitical risks.

Municipal Budgets Drive Road Salt Demand

A developer focused on the road-deicing market is less exposed to chlor-alkali market conditions than producers serving industrial chemical demand. Its cash flow depends primarily on winter weather and municipal road-maintenance budgets rather than polyvinyl chloride demand or Chinese soda-ash inventories. As a result, demand for road salt can remain stable even when weaker chlor-alkali markets reduce industrial salt consumption. The distinction matters because development-stage road-salt projects are primarily exposed to municipal demand rather than industrial chemical cycles.

High Capital Costs & Interest Rates Delay New Salt Supply

Despite favorable economics for new domestic salt capacity, supply has not expanded for nearly two decades because new mine development requires substantial upfront capital. Building a new underground salt mine requires infrastructure-scale investment and multi-year construction rather than the shorter development timelines typical of many mining projects. Atlas Salt's Great Atlantic Salt Project has an estimated construction cost of approximately C$590 million, including about C$150 million for two parallel underground access drifts, each extending roughly 1.5 kilometers. Unlike many metal mines, the project has no by-product revenue to offset development costs before production begins.

The project's feasibility study provides an estimate of its potential economics, but those figures depend on the project securing financing and reaching production. An independent feasibility study completed in September 2025 estimated an after-tax net present value of approximately C$920 million, representing the discounted value of future after-tax cash flows. The study also projected average after-tax cash flow of roughly C$188 million per year over the life of mine and a payback period of about 4.2 years from the start of production. These are feasibility-stage projections that depend on securing financing and successfully constructing the project. These projections are not operating results, and Atlas will remain a development-stage company until construction is funded and commercial production begins.

Higher interest rates increase the cost of financing new salt mines, adding to the capital barrier for new supply. With the Fed holding its policy rate at 3.50% to 3.75% and signaling that rates could remain elevated, developers face higher borrowing costs while investors apply higher discount rates to long-dated infrastructure projects. Higher financing costs also slow new mine development, limiting the industry's ability to add capacity even as import reliance increases.

Salt Reflects a Broader Shift Toward Domestic Supply Security

Beyond any single development project, the key question is whether the US salt market reflects a broader shift toward securing domestic industrial supply. The salt market reflects a broader shift toward securing domestic industrial supply as rising import dependence exposes the risks of relying on low-cost foreign production. Rising net import reliance, nearly 25 years without a new underground salt mine in North America, and industrial demand linked to geopolitically sensitive supply chains together indicate that domestic salt supply is becoming more vulnerable to disruption despite historically stable market conditions.

The US salt market combines stable demand with increasingly constrained domestic supply. Demand is supported by municipal road-maintenance budgets and industrial chemical production, while domestic supply depends on aging mines and new projects that require substantial capital and multi-year development timelines. These conditions are more likely to influence long-term supply availability than short-term price movements. Projects that can add new, low-cost domestic production may become more valuable if import reliance continues to increase and replacement capacity remains limited. The increase in net import reliance to 31% suggests that changes in supply security can emerge gradually before they become visible in commodity prices.

The Investment Thesis for Salt

- The investment case rests on domestic supply security as US net import reliance reached 31% in 2025 and North America has gone nearly 25 years without building a new underground salt mine.

- Demand remains resilient because road de-icing is funded through public-safety budgets and chemical feedstock supports essential industrial production.

- Low-cost developers with regulated power and port access are better positioned to secure financing and reach production.

- Higher interest rates slow new mine development by increasing borrowing costs and discount rates, making it harder to finance new supply and favoring developers with credible funding.

- The base case depends on securing financing and completing construction, while a prolonged Strait of Hormuz disruption could provide additional upside through stronger chlor-alkali demand.

- Evaluation should match project stage, with producers judged on operating performance, developers on financing and permitting, and explorers on resource definition.

The 31% net import reliance figure indicates that domestic salt supply is increasingly dependent on imports despite historically stable market conditions. North America's domestic salt supply is becoming more constrained as aging mines limit replacement capacity while higher interest rates and uncertainty in the chlor-alkali supply chain discourage new project development. Projects with credible financing and competitive operating costs are best positioned to add replacement capacity if import reliance continues to increase. A prolonged Strait of Hormuz disruption could provide additional upside through the chlor-alkali market, but that remains a secondary scenario rather than the base case. The long-term outlook depends more on financing, permitting, and project execution than on short-term commodity price movements.

TL;DR

US net import reliance for salt increased to 31% in 2025 as domestic production failed to keep pace with demand and North America went nearly 25 years without opening a new underground salt mine. Stable demand from road de-icing and the chlor-alkali industry contrasts with an aging supply base, high capital costs, and elevated interest rates that slow new mine development. While the Strait of Hormuz creates indirect risks through the chemical supply chain, the primary investment thesis centers on domestic supply security, financing execution, and the ability of well-funded, low-cost development projects to add replacement capacity.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed