Higher Real Yields & 70% Fed Hike Odds Raise Gold's Cost of Capital & Favor Self-Funding Producers

Higher real yields and 70% Fed hike odds are raising gold's cost of capital, favoring self-funding producers despite continued support from central-bank demand.

- May CPI inflation of 4.2% and Kevin Warsh's first Fed meeting pushed year-end rate-hike odds to roughly 70%, increasing real yields and pressuring gold prices.

- Higher-for-longer policy pressures gold equities more than bullion because higher discount rates reduce the value of future mine cash flows.

- Realized prices near $4,900 per ounce are widening operating margins despite rising costs, allowing producers to fund growth from cash flow rather than capital markets.

- Higher financing costs favor companies that can fund growth from cash flow over those that must raise external capital.

- Investors should assess balance-sheet strength and funding capacity alongside resource size because higher real yields can reduce gold-equity valuations.

Fed Policy Signals Shift Gold's Valuation Framework

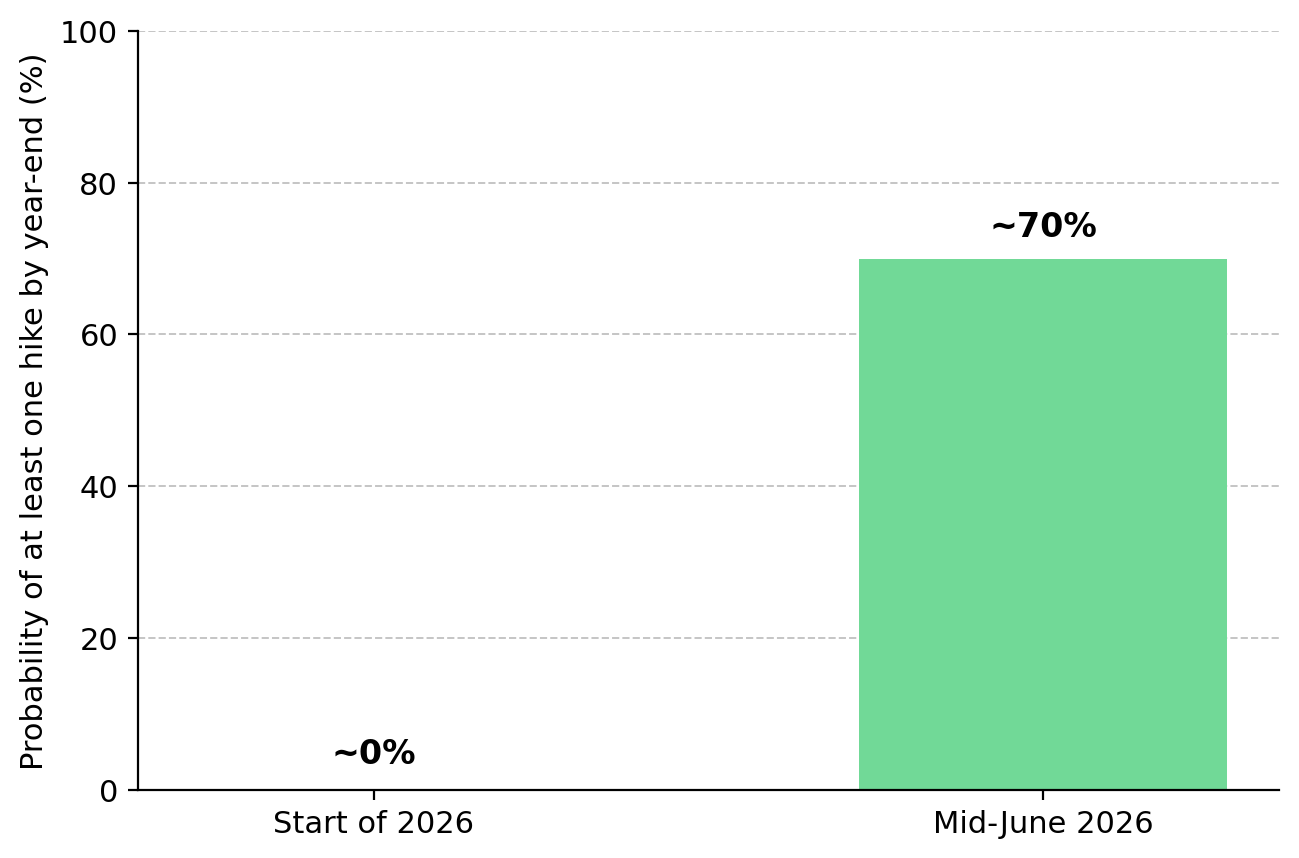

Kevin Warsh chaired his first Federal Open Market Committee meeting on June 16-17, and while the Fed held rates at 3.50% to 3.75%, markets focused on the Summary of Economic Projections and its implications for future rates. CME Group's FedWatch tool showed roughly 70% odds of at least one year-end rate hike, up from near zero at the start of the year.

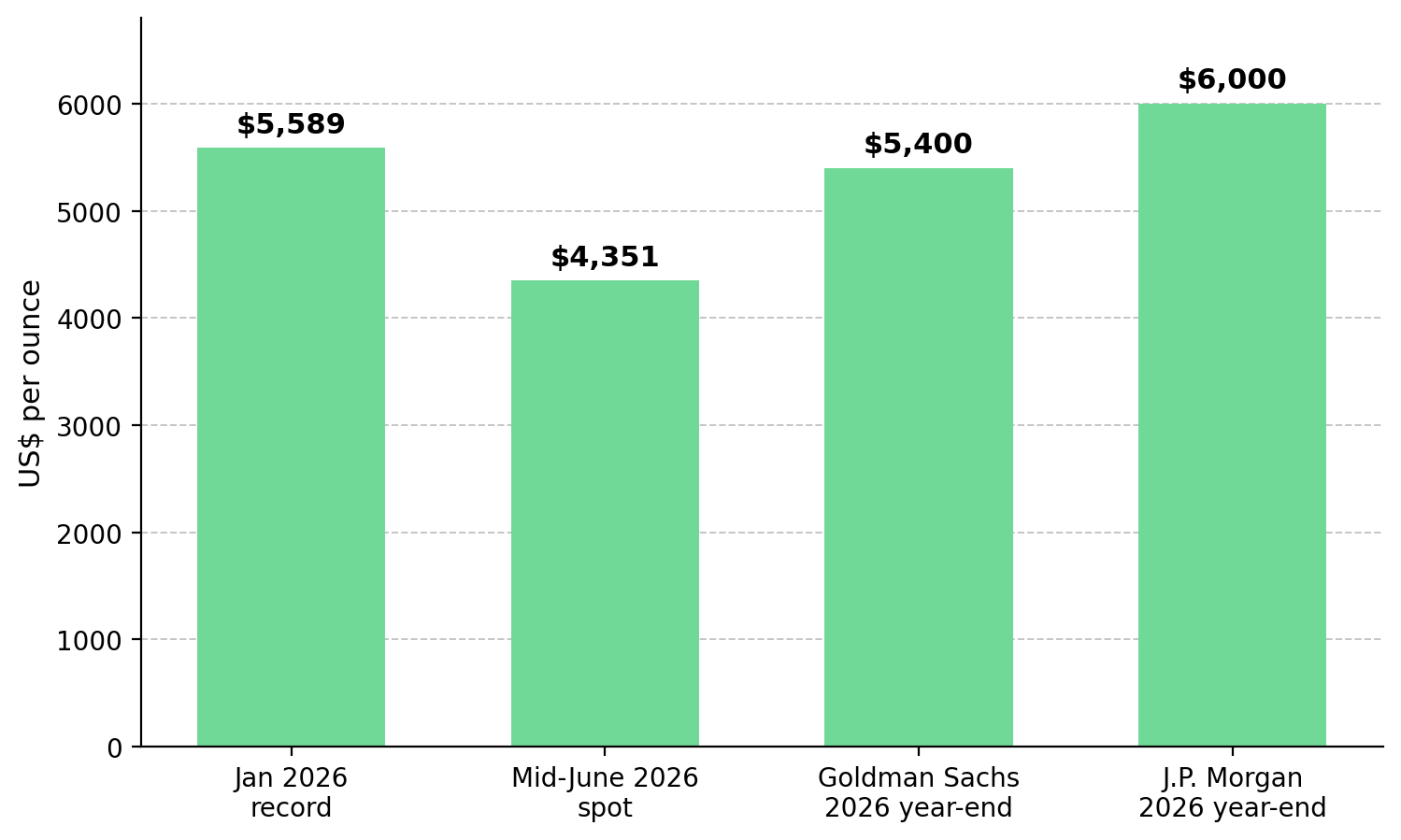

The Bureau of Labor Statistics reported May CPI inflation of 4.2% year over year, the third consecutive monthly acceleration, with energy the largest contributor and core inflation near 2.9%. Gold pays no income, so higher real yields increase the opportunity cost of holding it and often pressure prices. Gold traded near $4,351 per ounce in mid-June, down roughly 25% from its January record of $5,589.

The unwinding of the Middle East risk premium and lower oil prices contributed to gold's decline from its January peak, but neither directly affects gold-equity valuations. Higher real yields matter more than geopolitical risk because they reduce gold-equity valuations even when gold prices remain elevated.

Strong Labor Data Reinforces Higher-for-Longer Rates

Strong labor-market data reduced the likelihood of near-term rate cuts. The Bureau of Labor Statistics reported 172,000 nonfarm jobs added in May, more than double economists' expectations of roughly 80,000, with unemployment near 4.3%. Strong employment growth reinforced expectations that rates will remain elevated while inflation remains above target.

Traders lifted year-end rate expectations to roughly 3.87%, while Goldman Sachs removed all remaining 2026 rate cuts from its forecast and pushed expected easing into 2027. The probability of at least one hike by year-end climbed to about 70% on the CME FedWatch tool, from near zero at the start of the year. For gold, expectations that rates will remain elevated matter more than the rate level on any single day because they increase the opportunity cost of holding a non-yielding asset.

Higher rate expectations increase returns on cash and short-dated Treasuries, which compete directly with gold for defensive allocations. Gold closed below its 200-day moving average in June for the first time since October 2023, reflecting weaker price support as rate expectations moved higher.

A Stronger Dollar & Higher Real Yields Pressure Gold Demand

Gold is priced in dollars, and the same factors pushing yields higher have also strengthened the currency. A stronger dollar makes gold more expensive for non-US buyers, reducing demand and adding to pressure from higher real yields. Policy divergence also supported the dollar, as the Bank of Japan raised rates by 25 basis points while the Reserve Bank of Australia signaled further tightening, reinforcing pressure on gold demand outside the US.

Real yields determine the opportunity cost of holding gold, while the dollar affects its price for non-US buyers, and both often strengthen when the Fed turns hawkish. When both strengthen at the same time, they can pressure gold prices even without a broader increase in market risk.

Recent de-escalation in the Middle East reduced safe-haven demand for gold, but it has had less influence on prices than changes in interest-rate expectations. As the conflict premium fades, real yields and the dollar are likely to play a larger role in gold-price direction during the second half of the year.

Why Higher-for-Longer Pressures Gold Equities More Than Bullion

A gold producer derives much of its value from cash flows expected years into the future. When real yields rise, higher discount rates reduce the value of those future cash flows. Physical gold is less sensitive to discount-rate changes because it does not generate future cash flows. As a result, higher-for-longer rates can reduce gold-equity valuations even when gold prices remain stable.

Companies whose future production depends on projects that will not generate cash flow for years are more sensitive to higher discount rates. Heap-leach projects typically require less upfront capital and reach payback faster than more complex processing routes. Projects that require autoclaves need more capital and longer development timelines, making them more sensitive to higher discount rates. Higher financing costs favor companies that can fund growth from cash flow over those that require external capital.

Slow Supply Growth Helps Sustain High Gold Prices

The World Gold Council reported that total gold supply rose about 1% in 2025 despite record prices, while mine production reached a record 3,672 tonnes. New mines take years to permit and build, while higher energy and labor costs raise development costs, limiting near-term supply growth.

When gold prices rise, previously uneconomic ounces and idled operations can return to production faster than new mines can be built. Because new mine supply responds slowly, higher prices can support producer margins for longer. The World Gold Council recorded a record 1,313 tonnes of gold demand in the third quarter of 2025, worth about $146 billion. When supply responds slowly, high gold prices can persist long enough to fund growth from cash flow. That favors self-funding producers over companies that must raise external capital.

Record Realized Prices Expand Margins Despite Rising Costs

Realized prices near $4,800 to $4,900 per ounce are widening margins even as unit costs rise, making cost performance more important than a simple "low-cost producer" label. The key question is how much of that margin converts into cash flow that can fund future growth.

Strong Margins Fund Future Production Growth

In Q1 2026, Integra Resources reported a 40% operating margin at a record realized gold price of $4,854 per ounce, despite cash costs of $2,422 per ounce and Mine-site AISC of $3,310 per ounce rising above guidance on higher royalties, excise taxes, and diesel costs. DeLamar is not yet contributing production, and current spending is intended to increase future output. George Salamis, President and Chief Executive Officer of Integra Resources, explains how today's investment supports future production:

"Essentially 2026 is about building capacity today at Florida Canyon to deliver more ounces, stronger cash flow, lower costs tomorrow."

Higher Gold Prices Bring Uneconomic Ounces Back Into Production

Serabi Gold reported record first-quarter post-tax profit of $21.0 million and an 83% increase in revenue, while cash costs rose to $1,863 per ounce and AISC reached $2,293 per ounce during the Coringa ramp-up. Mike Hodgson, Chief Executive Officer of Serabi Gold, highlights how higher gold prices can bring more supply to market:

"We are enjoying phenomenal gold prices and we mustn't forget our old mine, Sao Chico. It was marginal really at the time with the gold price we had of the day. But at these gold prices, Sao Chico is very, very much a viable business again."

Higher Financing Costs Reward Self-Funding Producers

Higher financing costs favor companies that can fund growth internally over those that must raise external capital. The sector spans debt-free operators funding growth from cash flow and companies relying on equity financing or larger capital-market packages to advance future production.

Capital-Efficient Growth Extends Production Potential

West Red Lake Gold Mines, a gold producer whose Madsen mine in the Red Lake district of Ontario reached commercial production in early 2026. Its Rowan deposit saw indicated resources rise 70% to 334,825 ounces at 13.03 grams of gold per tonne, with the lower-confidence inferred category up 52%. The company achieved that growth for roughly 17.60 Canadian dollars per ounce of discovery cost, a measure of capital discipline that matters more when capital is expensive. Shane Williams, President and Chief Executive Officer of West Red Lake Gold Mines, outlines a low-cost path to production growth:

"We can see a pathway to 150,000 ounces a year in Red Lake. Our mill can be ramped up and effectively doubled with very little capital, and we can grow to that 150,000-ounce level through steady expansion around the Madsen operation."

Large Financings Reduce Funding Risk but Raise Return Requirements

i-80 Gold, a Nevada gold producer scaling through a phased development plan, completed a $787.5 million recapitalization across a Franco-Nevada net smelter return royalty, retiring $165 million of debt and resolving the going-concern doubt flagged in its 2025 accounts. The financing de-risks execution, yet it also shows how a higher cost of capital raises the stakes for development-stage scale-ups that must access markets to build new supply, and its Phase 1 to Phase 3 targets remain pipeline rather than current output. Richard Young, President and Chief Executive Officer of i-80 Gold, explains how new funding can accelerate future supply growth:

"What this facility with Franco has allowed us to do is to actually accelerate our technical work and our prefeasibility work for Mineral Point. For 2026, we actually have $50 million in the budget for a resource expansion and infill drill program as part of prefeasibility engineering work as well as initial permitting."

Higher Real Yields Pressure Gold While Central Banks Support Demand

Gold prices are being shaped by both monetary policy and long-term demand. In the near term, roughly 70% year-end hike odds and elevated real yields continue to pressure gold prices. Longer-term demand remains supported by central-bank buying. The World Gold Council's June survey found central banks have averaged about 1,000 tonnes of annual purchases over the past four years, while central banks bought a net 244 tonnes in the first quarter of 2026 and 89% of respondents expect global reserves to keep rising.

Interest-rate expectations remain the main driver of short-term gold-price movements. Financing costs help determine which gold equities outperform. Central banks bought a net 244 tonnes of gold in Q1 2026, supporting long-term demand. Sell-side year-end targets remain above spot prices, with J.P. Morgan near $6,000 and Goldman Sachs at $5,400, while the $4,200 to $4,400 range has continued to act as support. Higher real yields continue to pressure gold prices, but the 25% decline from January has not eliminated support from central-bank demand.

The Fed's projected rate path remains the key variable for gold. If the 2026 median still shows a rate cut, the Fed would be signaling a willingness to ease despite inflation remaining above target. If the cut is removed, it would reinforce expectations of higher financing costs and increase pressure on gold-equity valuations. In either scenario, interest-rate expectations are likely to have a greater influence on gold equities than geopolitical developments.

The Investment Thesis for Gold

- Gold equities are more sensitive to higher real yields than bullion because rising discount rates reduce the value of future mine cash flows.

- Near-record realized prices are widening producer margins despite rising all-in sustaining costs, turning a strong gold price into a source of growth funding.

- Higher financing costs favor capital-efficient producers that can fund growth from cash flow over those reliant on dilutive equity or higher-cost debt.

- Large financings can fund project development and strengthen the balance sheet, but they also increase the return required to create value for shareholders.

- Gold output rose only about 1% in 2025, helping sustain high realized prices long enough for disciplined producers to fund growth from cash flow.

- Sustained central-bank buying supports gold demand and can help cushion gold equities when higher real yields pressure prices.

- Gold equities are more sensitive to interest-rate expectations than bullion, and a hawkish policy surprise could pressure valuations across the sector.

The fading Middle East premium affected short-term sentiment, but interest-rate expectations remain the main driver of gold-equity valuations. In a higher-for-longer environment, financing costs play a larger role in determining equity valuations. Higher financing costs reduce valuations, favor self-funding companies, and weigh most heavily on projects that will not generate cash flow for years. Near-record realized prices support producer cash flow, slow supply growth helps sustain high prices, and continued central-bank buying supports demand during periods of volatility. Investors should assess the Fed's projected rate path alongside balance-sheet strength, distinguishing companies that can fund growth internally from those that depend on external capital. This is analysis rather than a recommendation, and gold equities carry a real risk of loss.

TL;DR

May inflation of 4.2% and rising expectations for a Fed rate hike have increased real yields, putting pressure on gold prices and gold-equity valuations. Higher financing costs favor producers that can fund growth from cash flow rather than relying on external capital, while near-record realized gold prices continue to support margins despite rising costs. Gold supply remains slow to respond, with output rising only about 1% in 2025, helping sustain elevated prices. Although higher real yields remain a near-term challenge, continued central-bank buying and constrained supply provide longer-term support for gold and select gold equities.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed