Indonesia's RKAB Revision & Nickel Price Outlook Keep High-Cost Producers Below Cost

Indonesia's RKAB quota review could shift nickel to $14,000-19,000/mt as higher ore supply, sulfur costs, and inventories reshape H2 prices.

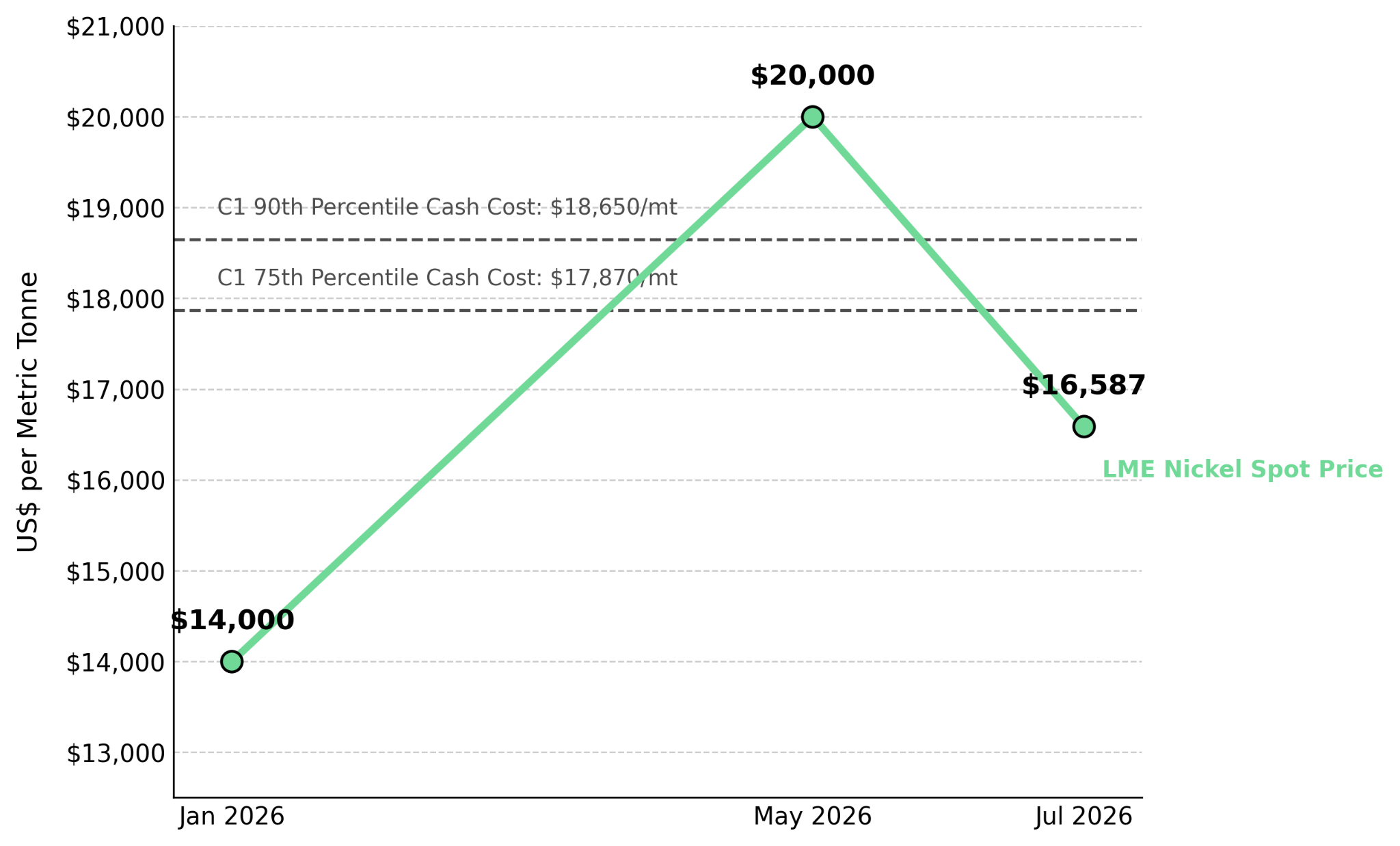

- LME nickel closed at $16,587/mt, up 1.52%, while LME opening stocks totaled 274,584 metric tons, including 16,650 cancelled warrants.

- Indonesia's RKAB mid-year revision could raise the 2026 quota to 300-350 million wet metric tons from the initial 260-270 million, increasing ore supply and pressuring nickel prices.

- Sulfur prices CIF Indonesia surged from below $600/mt to $1,300/mt after Hormuz disruptions disrupted imports, triggering HPAL production cuts, including at Huayou Cobalt's Huafei Nickel-Cobalt.

- C1 cash costs at the 75th and 90th percentiles rose to $17,870/mt and $18,650/mt in 2026, above spot nickel at $16,587/mt and up from $14,650/mt and $15,300/mt in 2025.

- SMM outlines three H2 nickel price scenarios: bearish at $14,000-16,000/mt if quotas rise by at least 30% and sulfur prices fall, neutral at $15,500-17,500/mt, and bullish at $17,000-19,000/mt if quotas remain tight and sulfur costs rise.

Ore Supply Cuts & Sulfur Shortages Drive Nickel's Five-Month Rally

LME nickel closed at $16,587/mt, up 1.52%, with opening stocks of 274,584 metric tons, including 16,650 cancelled warrants. LME nickel rose from $14,000/mt in January to nearly $20,000/mt in May before pulling back to $16,000-17,000/mt by July. Three factors drove the move: Indonesia's 2026 RKAB quota cut from 379 million to 270 million wet metric tons, a Hormuz-driven sulfur supply shock that raised Indonesian HPAL production costs, and the Fed's hawkish June pivot, which drove the price pullback.

HPAL production consumes about 10 metric tons of sulfur for every metric ton of MHP nickel produced, making sulfur costs a key driver of the May price spike. Hormuz disruptions disrupted Indonesia's sulfur imports, lifting sulfur prices from below $600/mt to about $1,000/mt before peaking at $1,300/mt CIF Indonesia. Huayou Cobalt's Huafei Nickel-Cobalt cut HPAL production after higher sulfur costs flowed through the MHP-to-nickel sulfate supply chain, helping lift nickel prices toward $20,000/mt.

Indonesia's Ore Supply Review & Nickel Prices Test the May Rally

Indonesia's July 1-31 application period for supplementary RKAB quotas will determine nickel ore supply in H2 2026. Reports that the 2026 RKAB quota could increase to 300-350 million WMT from the initial 260-270 million likely contributed to the June pullback by signaling higher ore supply. A larger quota increase would ease ore shortages that forced WBN to halt production after exhausting its 2026 quota.

Sulfur costs depend on geopolitical developments rather than Indonesia's quota decision and could fall if a peace agreement restores sulfuric acid supply. Indonesia's Finance Minister Regulation No. 32, introduced in July 2026, requires export licenses for ferronickel products containing at least 4% nickel, adding another supply constraint alongside tighter quotas and higher HPM pricing.

Ore Supply Outcomes & Nickel Price Ranges Guide H2 Positioning

Indonesia's long-term nickel price target of $19,000-20,000/mt limits how much it can raise RKAB quotas because higher ore supply would make that price harder to sustain. The bearish scenario assumes a quota increase of at least 30%, lower sulfur prices, and high inventories, putting LME nickel at $14,000-16,000/mt. The neutral scenario assumes a modest quota increase and sustained high sulfur costs, putting LME nickel at $15,500-17,500/mt. The bullish scenario assumes tighter quotas, stricter export controls, and higher sulfur costs from geopolitical disruptions, putting LME nickel at $17,000-19,000/mt.

Spot nickel at $16,587/mt is at the midpoint of the neutral range, indicating the market is pricing a modest RKAB quota increase. Bernstein raised its 2026 nickel price target to $17,357/mt, aligning with the upper end of the neutral scenario. The RKAB decision, due by July 31, will determine the price outlook: a quota increase to 300-350 million WMT points to the bearish scenario, while a quota below 300 million WMT supports the neutral or bullish range.

High Inventories & Processing Costs Cap Nickel Price Gains

Combined LME and SHFE nickel stocks reached 375,000 metric tons, equal to about 9% of 2025 mine production. Global nickel inventory totaled 497,000 metric tons, including 274,584 metric tons held in LME warehouses. High visible inventories capped nickel prices, sending LME nickel back to about $16,100/mt as weak demand outweighed earlier supply concerns.

C1 cash costs at the 75th and 90th percentiles reached $17,870/mt and $18,650/mt, above the LME spot at $16,587/mt, leaving many producers below their cost of production. RKEF-based high-grade nickel matte operations have a cost advantage over sulfur-dependent HPAL facilities when sulfur prices are high. Indonesia's high-grade nickel matte production rose 123% year over year to 185,000 metric tons of contained nickel in H1 as producers shifted away from sulfur-dependent HPAL operations, while HPAL producers remained under margin pressure at current spot prices.

Supply Policy & Nickel Prices Determine the Next Market Catalyst

C1 cash costs at the 75th percentile rose from $14,650/mt in 2025 to $17,870/mt in 2026, supporting current nickel prices only if Indonesia keeps quotas tight and sulfur costs remain high. LME nickel at $16,587/mt depends on Indonesia maintaining its 270 million WMT quota and high sulfur costs across the MHP-to-nickel supply chain.

Indonesia's RKAB decision, due by July 31, will determine the price outlook: a quota increase to 300-350 million WMT points to $14,000-16,000/mt, while a quota below 300 million WMT supports $15,500-17,500/mt or $17,000-19,000/mt, depending on sulfur supply. The RKAB decision will set the market's supply outlook and determine how traders interpret the Fed's policy path, sulfur supply, stainless steel and NEV demand, and inventory levels. A quota above 300 million WMT would point to the bearish scenario of $14,000-16,000/mt in H2 2026.

Analyst's Notes

Subscribe to Our Channel

Stay Informed