Investment Demand & Trade Barriers Redirect Commodity Supply, Favoring Producers Over Manufacturers

Gold demand and trade barriers are redirecting commodity supply, benefiting producers and raising manufacturing costs.

- Physical gold investment demand is forecast to rise 15% to 1,615 metric tons in 2026, overtaking jewelry demand for the first time and making investment buying the primary driver of the gold market.

- US crude inventories fell by 8 million barrels to 433.7 million barrels in the week ending May 29, exceeding forecasts for a 4 million barrel draw and indicating stronger crude demand or lower supply than the market expected.

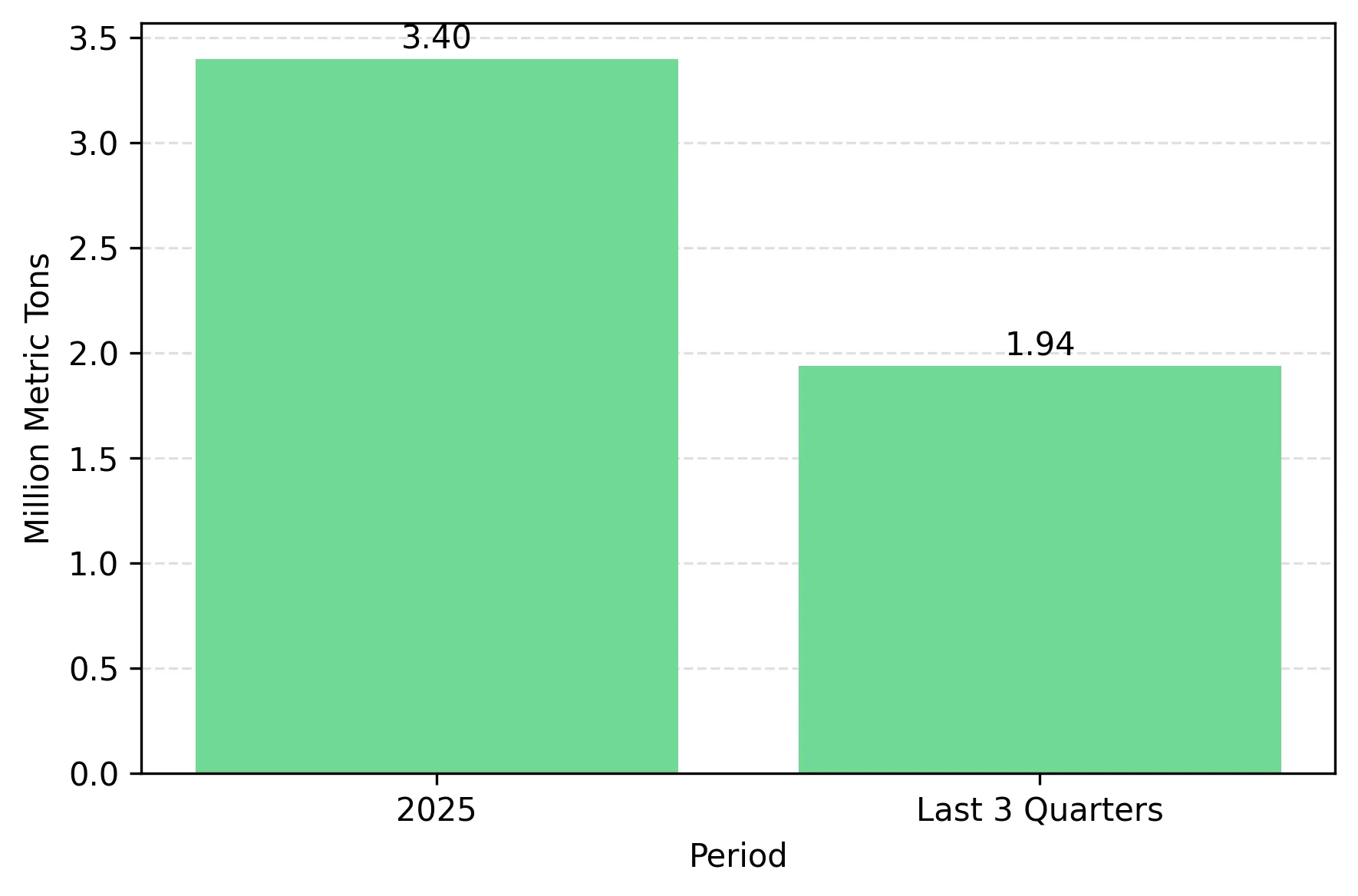

- European steel exports to the US fell 34% to 1.94 million metric tons over the past three quarters after Washington increased steel and derivative-product tariffs, reducing material available to US buyers and redirecting shipments to other markets.

- Metals Focus projects average gold prices will reach a record $4,920 per ounce in 2026 if investor purchases continue diverting gold from jewelry demand into bars and coins, according to its June 4, 2026 outlook.

- Current supply constraints favor commodity producers, while US manufacturers that rely on imported metal face higher input costs; a reduction in US derivative metal tariffs to 15% would lower those costs and improve access to imported steel.

Gold Buyers & Tariffs Are Redirecting Commodity Supply

Gold investment demand is forecast to rise 15% to 1,615 metric tons in 2026, while US crude inventories fell by 8 million barrels and European steel exports to the United States dropped 34%, highlighting tighter physical supply across multiple commodity markets, according to Metals Focus, the EIA and Eurofer on June 4, 2026.

European steel exports to the United States fell 43% to 1.94 million metric tons from 3.4 million metric tons in 2025 after US tariffs increased, reducing material available to American buyers, according to Eurofer on June 4, 2026. Fewer imports leave US manufacturers competing for a smaller steel supply, while displaced volumes are redirected to other markets.

Inventories & Supply Chains Adjust More Slowly Than Policy

Higher gold prices reduced jewelry purchases and changed how buyers use physical gold. Metals Focus reported jewelry demand fell 19% in 2025, while investors increased purchases of bars and coins, shifting gold demand from jewelry to investment products, according to Metals Focus on June 4, 2026. Gold refining and fabrication capacity is limited, so changes in demand affect how available metal is allocated. As investors absorb more physical gold, less metal is available for jewelry manufacturers, increasing competition for available supply.

Oil markets show a similar pattern, with inventories falling faster than expected. US crude inventories fell by 8 million barrels in the week ending May 29, double forecasts for a 4 million barrel draw, according to the Energy Information Administration on June 4, 2026. Steel trade flows are being limited by tariffs rather than a shortage of steel production. Eurofer reported that US tariffs expanded from primary steel products to derivative goods such as rail components and industrial equipment, according to Eurofer on June 4, 2026.

Each tariff expansion increased import costs for more manufacturers and narrowed their choice of suppliers.

Tariff Negotiations Move Faster Than Supply Chains

Trade flows are unlikely to recover immediately because tariff negotiations do not automatically restore inventories, supplier relationships or procurement contracts.

Inventories, procurement contracts and production schedules typically adjust over quarters rather than days.

Weekly EIA crude inventory reports and Metals Focus gold investment demand data; falling inventories and rising physical gold purchases would support the higher-price scenarios outlined above.

Commodity Producers Gain While Manufacturers Face Higher Costs

Manufacturers of appliances, transport equipment and industrial products face higher input costs because derivative metal products remain subject to elevated US tariffs. These costs reduce profit margins unless companies can raise prices enough to offset the tariff burden.

Commodity producers can benefit from supply shortages because they sell the resource becoming harder to obtain. Manufacturers that buy those commodities face higher input costs and lower margins. Giovanni Staunovo of UBS said on June 4, 2026 that oil prices are more likely to rise while supply flows remain constrained. Investors should assess whether a company sells scarce commodities or depends on them as inputs.

EIA crude inventories, Metals Focus gold investment demand data, and US tariff announcements should be monitored. Rising inventories or lower tariffs would indicate improving supply conditions and could weaken the case for commodity-focused positions.

Analyst's Notes

Subscribe to Our Channel

Stay Informed