Kazatomprom’s Supply Cut Forces Uranium Market Repricing, Elevating Valuation Premiums for Tier-One Producers

Kazatomprom's 20% uranium production cut exposes global supply fragility. North American producers gain as utilities pay 23% premiums for secure supply.

- Kazatomprom cut 2025 production guidance by approximately 20%, reducing midpoint output to 14 million pounds U3O8

- This compounds global supply fragility amid Niger political risks and chronic underinvestment following Fukushima

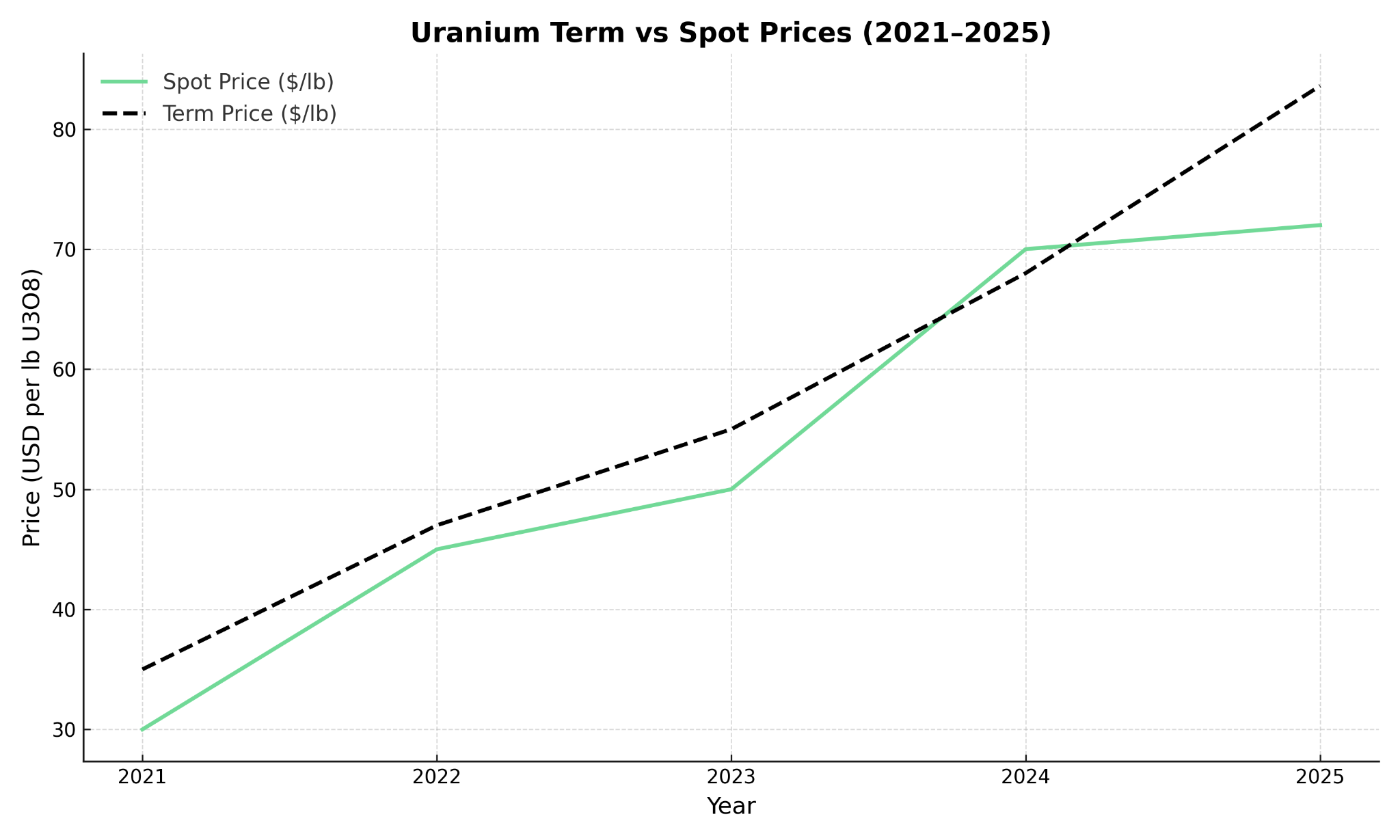

- Spot prices hold above $70 per pound while term prices surged 23%, showing utilities are paying premiums for long-term supply

- Investors are prioritizing stable jurisdictions, U.S. and Canadian producers see valuation premiums over international peers

- Energy Fuels, IsoEnergy, and Global Atomic offer differentiated exposure to secure supply, near-term catalysts, and ESG alignment

Uranium Markets Face Structural Supply Shock

Kazatomprom's revised production guidance represents more than operational adjustments, it signals a fundamental shift in global uranium supply dynamics. The state-owned Kazakhstani producer, which controls approximately 25% of global uranium output, reduced its 2025 production target by roughly 20%, bringing the midpoint to 14 million pounds U3O8. This reduction stems from operational constraints, infrastructure bottlenecks, and broader geopolitical instability affecting the Central Asian mining complex.

The significance extends beyond Kazakhstan's borders. Kazatomprom's supply reduction arrives amid a uranium market already strained by geographic concentration risk, thin liquidity, and a decade-long investment drought following the Fukushima disaster. The company's dominant market position means production cuts carry systemic implications, forcing utilities and investors to reassess supply security assumptions that have underpinned uranium pricing for years.

This development exposes the vulnerability of a market where a handful of producers in politically volatile regions control the majority of global output. The combination of Kazakhstan's operational challenges and Niger's political instability has effectively removed nearly 30% of global supply from reliable production status, creating conditions for sustained price appreciation and structural market repricing.

Fragility Across the Global Supply Chain

The uranium supply chain's vulnerability extends beyond individual country risks to encompass broader structural weaknesses that have accumulated over more than a decade of underinvestment and market consolidation.

Niger & Orano's SOMAIR Mine Risk

Political upheaval in Niger presents another critical stress point for global uranium supply. The military coup that displaced the democratically elected government has created uncertainty around Orano's SOMAIR mine operations, which contribute approximately 8% of global uranium production. France's colonial legacy and military presence in the region have become flashpoints, with the new military leadership signaling intentions to diversify mining partnerships away from traditional European operators.

This instability compounds the risks already emerging from Kazakhstan, effectively concentrating supply disruption risk across two major producing regions. The geographic concentration of uranium production in politically unstable jurisdictions has become a structural liability for utilities seeking reliable fuel supply, driving increased interest in producers operating within stable regulatory frameworks.

Chronic Underinvestment Post-Fukushima

The uranium sector's chronic underinvestment following the 2011 Fukushima disaster continues to constrain new supply development. Exploration and development activities fell dramatically during the prolonged bear market, creating a pipeline deficit that cannot be quickly remedied. New uranium projects typically require 7-10 years from discovery to production, with permitting cycles extending timelines further in many jurisdictions.

The lack of new greenfield projects amplifies supply fragility precisely when demand growth is accelerating. Recent nuclear capacity additions in China, India, and emerging markets, combined with renewed Western interest in nuclear baseload power, have tightened supply-demand fundamentals. However, the investment required to develop new production capacity remains constrained by uncertain long-term pricing and regulatory complexity in key mining jurisdictions.

Market Signals, Prices, Inventories & Term Contracts

Uranium spot prices have demonstrated remarkable resilience, holding above $70 per pound despite broader commodity market weakness and macroeconomic uncertainty. The price stability reflects tight physical supply conditions and growing recognition among market participants that structural supply constraints are emerging across the uranium value chain.

More significantly, term contract pricing has surged 23% while inventory levels have grown only 6%, indicating utilities are prioritizing supply security over cost optimization. This shift represents a fundamental change in utility procurement behavior, moving away from just-in-time purchasing strategies toward longer-term contract arrangements that provide greater supply certainty.

Institutional buying activity provides additional evidence of market tightening. Sprott Physical Uranium Trust's $200 million allocation demonstrates how physical uranium purchases can impact spot pricing in a market characterized by limited liquidity and concentrated supply. The trust's buying activity has effectively removed material quantities of uranium from available spot supply, contributing to price support and highlighting the market's sensitivity to incremental demand.

The bifurcation between short-term price volatility and long-term structural bullishness creates opportunities for investors willing to navigate near-term uncertainty while positioning for sustained uranium price appreciation driven by supply constraints and growing nuclear demand.

Policy Realignment & Security of Supply

Government policy initiatives across major nuclear markets are reshaping uranium supply chains and creating competitive advantages for domestic producers. U.S. initiatives include uranium enrichment capacity expansion, accelerated licensing procedures for new nuclear facilities, and trade restrictions targeting imports from Russia and allied countries. These policies reflect growing recognition that nuclear fuel supply security represents a critical national security consideration.

European and Japanese policy pivots toward nuclear baseload power for decarbonization objectives are driving similar supply security initiatives. The European Union's taxonomy classification of nuclear power as a sustainable energy source, combined with life extensions for existing nuclear facilities and new construction programs, supports long-term uranium demand growth. Japan's renewed embrace of nuclear power following years of post-Fukushima caution adds incremental demand while highlighting the importance of diversified supply sources.

The emerging small modular reactor market represents another policy-driven demand catalyst. Government support for SMR development and deployment, combined with growing corporate interest in nuclear-powered data centers and industrial applications, creates new uranium demand categories that did not exist during previous market cycles.

These policy developments favor uranium producers operating in stable jurisdictions with established regulatory frameworks. Capital flows are increasingly directed toward domestic and allied-nation producers capable of meeting long-term supply requirements while aligning with energy security objectives and ESG mandates.

Strategic Positioning of Producers in Tier-One Jurisdictions

The uranium market's evolution toward supply security premiums has created distinct advantages for producers operating in stable jurisdictions with established infrastructure and regulatory frameworks.

Energy Fuels: Leveraging White Mesa Mill & Rare Earth Diversification

Energy Fuels operates the only conventional uranium mill in the United States, providing strategic control over domestic uranium processing capacity. The White Mesa Mill's 8 million pound annual capacity positions the company as an essential component of domestic uranium supply chains, particularly as utilities seek alternatives to foreign processing services.

The company's active mining operations at Pinyon Plain have exceeded initial grade expectations, with recent drilling results confirming the deposit's status as one of the highest-grade breccia pipe deposits in the Arizona Strip region. Higher grades provide natural inflation hedging and cost advantages that become more valuable as operating expenses increase across the industry.

President and Chief Executive Officer Mark Chalmers articulates the company's strategic positioning:

"Energy Fuels is a unique company where we are a critical mineral company building a critical mineral hub that is built around the uranium industry as the largest producer of uranium in the United States and recently over the last few years expanding into producing and mining rare earth elements."

The company's diversification into rare earth elements and critical minerals provides strategic hedging against Chinese supply dominance while leveraging existing infrastructure and expertise. With $210 million in cash and zero debt, Energy Fuels maintains the financial flexibility to execute growth initiatives while navigating market volatility.

IsoEnergy: High-Grade Athabasca & Near-Term U.S. Restart Potential

IsoEnergy's Hurricane Deposit in Saskatchewan's Athabasca Basin represents one of the world's highest-grade uranium resources, with 48.6 million pounds U3O8 at 34.5% grade at relatively shallow depths. The deposit's exceptional grade and favorable geology position it for low-cost production when market conditions support development.

The company's acquisition of the Tony M Mine in Utah, along with a toll milling agreement with Energy Fuels, provides near-term production optionality in the U.S. market. The fully permitted Utah asset contains 6.6 million pounds of resources and requires minimal capital for restart operations.

Chief Operating Officer Marty Tunney explains the strategic importance of domestic processing access:

"If you don't have access to the White Mesa Mill and you're a conventional hard rock miner in the USA you don't have anywhere in the next 5 to 7 years to process your ore."

IsoEnergy maintains strong financial backing with C$84.7 million in cash plus C$42 million in equity investments, providing the resources necessary to advance development while maintaining operational flexibility. The company's dual-jurisdiction strategy offers exposure to both Canadian resource quality and U.S. market premiums.

Global Atomic: Near-Term Production in Niger Amid Geopolitical Risk

Global Atomic's Dasa Project in Niger represents advanced-stage development with 68.1 million pounds of reserves and a 57% internal rate of return based on current feasibility studies. Construction progress has reached 75% completion, with first production targeted for Q2 2026 despite regional political challenges.

President and Chief Executive Officer Stephen Roman provides insight into the project's timeline and government support:

"We are on schedule to start producing in Q2 of 2026. We received a letter from the president and he copied all of his ministers and he said this is a strategic project it's of national importance and we're 100% behind it."

The project's lowest-quartile cost positioning and existing off-take agreements with U.S. utilities provide revenue visibility while the company navigates geopolitical complexity. Global Atomic's ESG leadership and community engagement initiatives have helped maintain local support despite broader regional instability.

The Investment Thesis for Uranium

The uranium investment landscape has been fundamentally altered by supply constraints, policy realignment, and growing recognition of nuclear power's role in decarbonization and energy security. Several key factors support sustained investor interest in the sector:

- Supply tightness driven by Kazatomprom production cuts reinforces global supply fragility while utilities accelerate term contracting to secure long-term fuel requirements

- Geopolitical risk premiums favor non-Kazakhstani, North American producers who offer greater supply security and alignment with Western energy security objectives

- Policy tailwinds across major nuclear markets, including U.S. and European Union initiatives, underpin long-term demand growth while supporting domestic uranium production

- Company-specific leverage opportunities include Energy Fuels' combination of low-cost U.S. production and rare earth diversification, IsoEnergy's high-grade Athabasca deposits and U.S. restart potential, and Global Atomic's construction-ready, low-cost, high-IRR development project

- Structural demand growth from small modular reactors, nuclear capacity expansion, and energy security considerations creates durable demand drivers independent of traditional nuclear markets

- Financial positioning among leading producers provides operational flexibility and growth capital while maintaining defensive characteristics during market volatility

A Market Redefined by Supply Fragility

Kazatomprom's production reduction represents more than an isolated operational adjustment, it exposes structural vulnerabilities that have been building across global uranium supply chains for over a decade. The combination of geographic concentration, political instability, and chronic underinvestment has created conditions for sustained price appreciation and fundamental market repricing.

Investors must now differentiate between speculative exploration companies and near-term, de-risked producers with operational visibility and jurisdictional stability. The market's evolution toward supply security premiums and policy-driven demand support creates favorable conditions for companies that can deliver reliable uranium production from stable jurisdictions.

Capital allocation will increasingly favor producers with secure processing access, strong balance sheets, and alignment with government energy security initiatives. The uranium market's structural transformation from commodity trading to strategic resource management represents a fundamental shift that will define investment returns for the remainder of this decade.

Analyst's Notes

Subscribe to Our Channel

Stay Informed