Koryx Copper Positions for Pre-Feasibility Milestone as Haib Project Gains Institutional Backing

Koryx Copper advances Namibia's Haib copper project toward pre-feasibility study completion, backed by $100M+ raised and strong share price momentum.

Koryx Copper is entering 2026 with considerable momentum behind its flagship Haib copper project in southern Namibia, as CEO Heye Daun outlined during an investor interview at PDAC. The company has raised over $100 million since assuming management control in early 2024, completed a preliminary economic assessment demonstrating robust economics at conservative copper pricing, and is now drilling aggressively ahead of a pre-feasibility study targeted for year-end.

The market has taken notice. Koryx's share price has risen more than 128% over the past twelve months, supported by a January 2026 financing round that brought in $51 million from institutional investors and strategic capital, including participation from Middle Eastern and Chinese financial groups. The company closed the raise at C$2.45 per share - a significant premium to where it traded when Daun's team took the helm roughly two years ago.

"When we started off two years ago, we were a nothing company, $10 million market cap, and we raised small rounds of $5-10 million. Since then, we're becoming more institutionalised. We've just done a $50 million raise and that was big institutional money. We had some real strategic money that came in."

Daun is no stranger to building value in Namibia. A Namibian citizen and mining engineer by training, he co-founded Osino Resources and sold the company to Chinese producer Shanjin Gold for $368 million in 2024. Before that, he co-founded Auryx Gold and sold it to B2 Gold for $180 million in 2011; the Otjikoto mine Auryx developed is now one of B2's top-performing assets globally. The pattern Daun is attempting to repeat at Koryx is straightforward: acquire an undervalued or mismanaged project, bring in a credible technical team, advance it methodically through permitting and studies, and surface it for a strategic transaction once it reaches investment readiness.

Technical Repositioning and the Path to Credibility

When Daun's team assumed control of what was then Deep South Resources, the project had fallen into disrepair - not geologically, but commercially. The previous management had proposed heap-leach bio-oxidation, a processing route that works in laboratory settings but has not been proven at commercial scale for sulfide copper deposits. Combined with licensing problems, the approach had eroded investor confidence.

"The project has an excellent pedigree. It was drilled by Rio Tinto in the 1970s. Then they sold it to Teck. Teck had a strategy, but didn't really have a strategy for this project. It just sat there and then it fell into the hands of this junior."

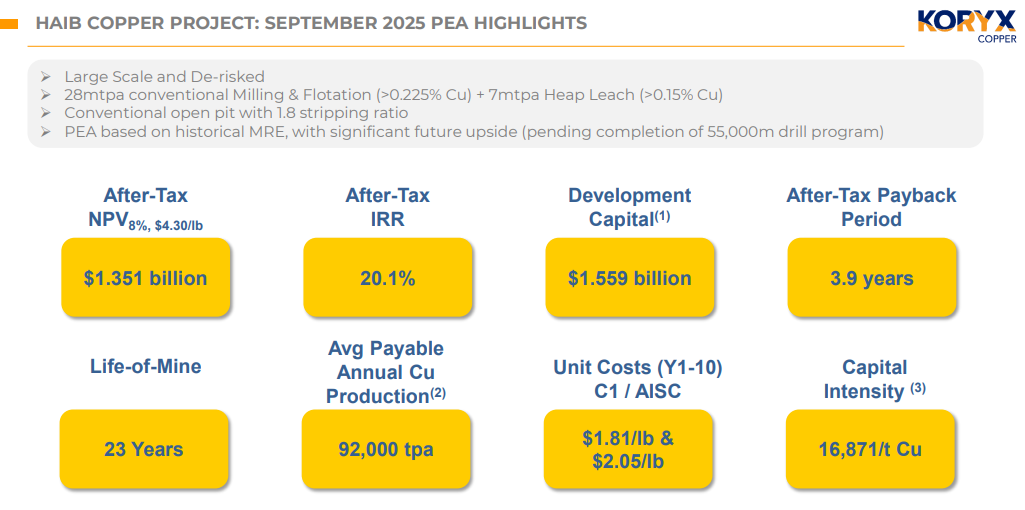

The fix was conceptually simple but capital-intensive: revert to conventional milling and flotation, the proven processing route for sulfide porphyry deposits. The company published a PEA in late 2025 modelling a $1.5 billion capital cost, production of just under 100,000 tonnes of copper per year, and all-in sustaining costs in the middle of the global cost curve. The study was conducted at a conservative copper price of $4.30 per pound - roughly 30% below spot pricing at the time of the interview - and returned an after-tax NPV of $1.35 billion and a 20% IRR.

"Our PEAs are credible documents," Daun said, contrasting Koryx's approach with the frequently promotional tone of junior mining studies. "What backs that up is that in all the projects I've been involved in, the step from PEA to PFS, the scope of the project generally stays the same or gets a little bit better."

The company is now midway through a 55,000-meter infill and expansion drill program designed to feed an updated mineral resource estimate, expected in or around the first quarter of 2026, and a pre-feasibility study due in the fourth quarter. Recent drill results have been encouraging: hole HM112 returned 602 meters grading 0.32% copper-equivalent, including 272 meters at 0.44%, while HM117 intersected 184 meters at 0.51%. The deposit remains open at depth and along strike.

Namibia as an Operating Advantage

One of Koryx's underappreciated strengths is jurisdiction. Namibia is not a typical African mining story. The country has been a stable democracy since independence in 1990, has hosted operations from Rio Tinto, AngloGold Ashanti, and several large Chinese groups, and benefits from currency weakness that structurally lowers operating costs. Daun noted that drilling costs in Namibia are roughly half those in West Africa, a meaningful advantage for a project that will require substantial ongoing geological work.

Infrastructure is similarly favourable. The Haib project sits within 20 kilometers of grid power, sealed roads, water supply infrastructure, and serviced towns. The company is advancing trade-off studies on power (grid connection versus renewables) and water sourcing (Orange River versus the Neckartal Dam), but the baseline access is already in place. Offshore oil discoveries in Namibia - the country is being touted as the next Guyana - are driving further investment in ports, power, and desalination capacity, all of which will benefit the broader mining sector.

"Namibia has these massive offshore oil discoveries. It's being touted as the next Guyana. Ultimately it's good for the country - deepening harbors, infrastructure investment, power investment, gas to power. That's all great."

Interview with Heye Daun, President & CEO of Koryx Copper Inc.

Strategic Endgame: Partner or Exit

Koryx's stated strategy is to advance Haib to an investment decision on a standalone basis, at which point a joint venture, acquisition, or other strategic structure becomes the most logical path forward. Daun was direct: the project's likely $1.5 to $2 billion capital requirement is too large for a junior to finance and construct independently.

"I fundamentally believe that juniors are not the right companies to build mega projects. This will be a mega project."

Daun emphasised that his role as a Namibian citizen adds a layer of accountability. The Haib project, if built, would be a GDP-moving asset for the country, and custodianship matters. Chinese groups are already in dialogue about offtake - the project will produce a clean copper concentrate, commercially attractive because it avoids smelting penalties - and broader strategic interest is building as the project de-risks.

The company's financing position is strong. With roughly $66 million in cash as of late January and no debt, Koryx has sufficient capital to complete the PFS and advance permitting without requiring additional dilutive raises in the near term. The presence of institutional investors, strategic capital, and high-net-worth Namibian backers provides both financial flexibility and in-country credibility.

Investor Positioning

Koryx sits at a relatively early stage in the development curve, but the pieces are aligning. The PEA established technical and economic feasibility. The drill program is expanding the resource ahead of the PFS. Permitting is progressing. Strategic interest is building. And the management team has a demonstrated track record of executing this exact playbook in this exact jurisdiction.

The key near-term catalysts are clear: the updated mineral resource estimate in the first quarter of 2026 and the PFS at year-end. A credible PFS - particularly one that maintains or improves the project economics outlined in the PEA - would represent a material de-risking event and likely trigger further re-rating. Daun's emphasis on conservative assumptions and realistic study parameters suggests the company is positioning for delivery rather than promotion.

For investors looking for leveraged exposure to copper in a low-risk jurisdiction with proven management, Koryx presents a relatively straightforward thesis: a large-scale, long-life, low-cost project advancing methodically toward the point where a major mining company or financial institution steps in to fund construction. The share price performance over the past year suggests the market is beginning to recognise that story. The next twelve months will determine whether the technical work supports it.

Analyst's Notes

Subscribe to Our Channel

Stay Informed