Magna Mining Targets Improved Grades and Lower Costs in H2 2025

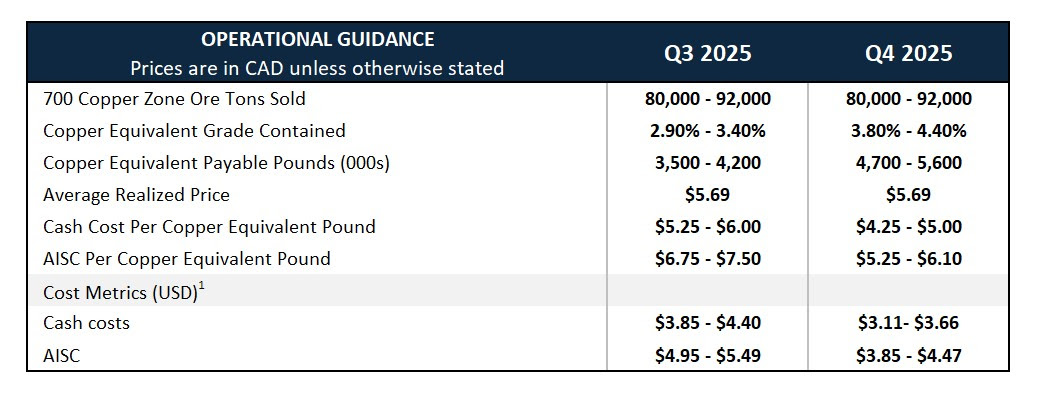

Magna Mining projects quarterly ore sales of 80,000-92,000 tonnes with rising copper equivalent grades and decreasing all-in sustaining costs through Q4 2025.

- Copper equivalent grades expected to improve from 2.9-3.4% in Q3 2025 to 3.8-4.4% in Q4 2025

- All-in sustaining costs projected to decrease from $4.95-$5.49 per pound in Q3 to $3.85-$4.47 in Q4 2025

- Daily development rates targeting 28 feet per day in H2 2025, with 5,100 feet of total underground development planned

- Capital development programme accessing western side of 700 Copper Zone to exploit known resources and explore untested areas

- Cost structure expected to improve further in 2026 as accelerated capital development programme concludes

Magna Mining (TSXV: NICU) is a mining company with copper, nickel and platinum group metals projects in Ontario's Sudbury Region. The company's primary asset is the McCreedy West copper mine, complemented by past-producing assets including Levack, Podolsky, Shakespeare and Crean Hill mines.

Chief Executive Officer Jason Jessup leads the transformation of McCreedy West operations through targeted capital investments and operational improvements. Chief Operating Officer Jeff Huffman focuses on development activities and production optimisation. The management team has transitioned from the inherited mine plan to a company-designed strategy emphasising higher-grade mining areas and operational flexibility.

McCreedy West Mine Development Update

The McCreedy West Mine has undergone significant operational improvements, with the company implementing 24-hour operations and hiring additional personnel to support expanded production capacity. These investments are materialising into improved metrics, with quarterly ore sales targeted at 80,000 to 92,000 tonnes for H2 2025.

Copper equivalent grades show progressive improvement, rising from 2.9% to 3.4% in Q3 2025 to 3.8% to 4.4% in Q4 2025. This enhancement reflects strategic focus on developing higher-quality mining areas within the 700 Copper Zone. Daily development rates are expected to reach 28 feet per day in H2 2025, supported by a contract mining company engaged to accelerate capital development.

The development strategy involves accessing the western side of the 700 Copper Zone across multiple levels. COO Jeff Huffman noted that "the planned capital development on the western side of the 700 Copper Zone should allow us to exploit the existing known resources as well as facilitate access to areas from which we can launch an exploration program in previously untested western areas."

Total underground development planned for H2 2025 reaches approximately 5,100 feet, including both operating and capital development components. Operating development is expected to provide increased stope development inventory and enhanced production flexibility, supporting more robust operations moving into 2026.

Sustaining Capital Costs and Financial Outlook

Magna's cost structure demonstrates a clear pathway towards improved profitability. Cash costs per copper equivalent pound are expected to decrease from $3.85 to $4.40 in Q3 2025 to $3.11 to $3.66 in Q4 2025. All-in sustaining costs follow a similar trajectory, declining from $4.95 to $5.49 in Q3 to $3.85 to $4.47 in Q4 2025.

Figure 1. Operational guidance shows improving copper equivalent grades and declining all-in sustaining costs throughout H2 2025.

The cost reduction strategy extends beyond 2025, with management expecting further decreases in 2026. This improvement is anticipated as the company concludes its accelerated capital development programme and achieves optimisation goals. The contract mining company is not planned to be retained for capital development in 2026, contributing to expected cost reductions.

CEO Jason Jessup emphasised the long-term vision, stating,

"We expect all-in sustaining costs to decrease in 2026 as we conclude our accelerated capital development program and achieve our optimization goals. I am proud of our team at the mine, and the dedicated executive management team that are helping to build McCreedy West into what we believe will be a long life, cash flow generating copper, nickel and PGE mine."

Financial projections are based on copper equivalent calculations using metal prices of $4.17 per pound for copper and $6.90 per pound for nickel, providing a framework for investors to evaluate performance against current market conditions.

Conclusion and Future Outlook

Magna Mining's H2 2025 guidance reflects a company transitioning from acquisition integration to operational optimisation. The combination of rising grades, decreasing costs, and expanded development activities positions the company for improved financial performance. Key milestones include achieving targeted development rates, accessing higher-grade areas, and demonstrating operational flexibility through increased stope inventory.

The company's focus shifts to exploration programmes in previously untested western areas, with the first underground diamond drill scheduled for mobilisation in coming weeks. The strategic development programme supports a more robust operating plan moving into 2026, when sustaining capital costs are expected to decrease significantly, supporting management's vision of building McCreedy West into a long-life, cash-generating operation.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed