Marimaca Copper: Pampa Medina Drilling Confirms Tier-One Scale as Ultra High-Grade Bornite Zone Takes Shape

Marimaca Copper's Pampa Medina hit ultra-high-grade Cu-Ag over 2km²; MOD alone may exceed market cap - making the growing sulfide discovery effectively free for investors.

- Marimaca Copper's Pampa Medina discovery is demonstrating exceptional grade continuity across an area now confirmed by drilling to exceed 2 km², significantly larger than originally anticipated.

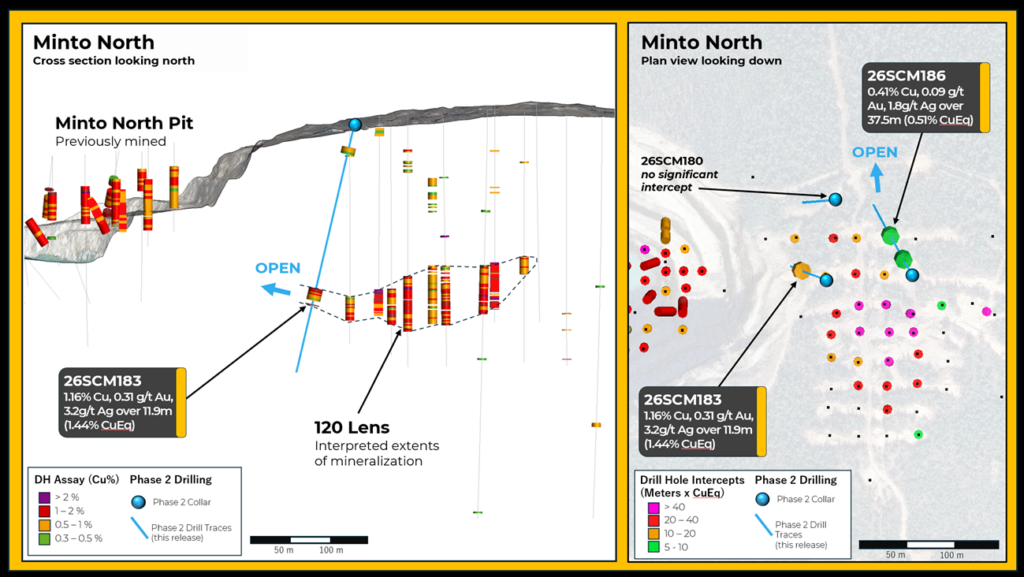

- Three key drill holes - SWRD-13, SPRD-05, and SPRD-04 - have defined an ultra high-grade bornite zone with results including 16 m at 5.7% copper and 62.6 g/t silver, pointing to world-class underground mineralisation.

- Management is reconsidering the mine development model, moving away from a narrow room-and-pillar approach toward a bulk mechanised underground operation, which could dramatically increase captured tonnage and lower the effective cut-off grade.

- The company sees potential for 120–500 million tonnes of contained ore depending on true thickness, with evidence of mineralisation extending deeper and along a northeast–southwest trend not yet fully drilled.

- While the Marimaca Oxide Deposit (MOD) remains the near-term value anchor - described as worth more than the current share price on its own - Pampa Medina is increasingly being positioned as a potential standalone tier-one asset capable of attracting major mining company interest.

Marimaca Copper (TSX:MARI) is advancing two distinct copper assets in Chile's Antofagasta region: its flagship Marimaca Oxide Deposit (MOD), which is already in development-stage planning, and its newer Pampa Medina discovery, which has become the central focus of the company's drill program in 2026. In a June interview, CEO Hayden Locke outlined the latest results from Pampa Medina, where ongoing drilling is revealing a mineralised system of growing scale, exceptional grade, and evolving geological complexity. For investors, the discussion highlights both the near-term de-risking of the MOD and the longer-term potential of what the company believes may become a tier-one copper asset.

Drilling Results Define an Ultra High-Grade Core

The catalyst for investor attention at Pampa Medina has been a series of drill results that have established both grade and spatial continuity across an increasingly large footprint. Of 40-plus holes drilled to date, 36 have returned mineralisation across what management describes as economic widths and grades.

The discovery hole, SWRD-13, intersected 26 metres at approximately 4% copper and 25 g/t silver from 580 metres downhole. Subsequent drilling has extended the mineralised zone materially. SPRD-05 returned 16 metres at 5.7% copper and 62.6 g/t silver approximately 650 metres to the west-northwest of SWRD-13. SPRD-04, drilled roughly 150 metres to the north, intersected 22 metres at 2% copper - lower in grade but carrying similar bornite-dominant mineralisation and high-grade silver patches over 5-10 metre intervals.

These three results in particular have allowed management to define what it is calling an "ultra high-grade bornite zone," a coherent core of exceptional mineralisation that appears to sit within a broader column of lower but still economically relevant grades.

A Broader Column of Rock Changes the Economics

One of the more significant disclosures in the interview relates to how Marimaca is now thinking about the broader mineralised column - not just the high-grade core. Drill logs show that while the ultra high-grade intervals are typically 16 to 26 metres wide, the overall mineralised column can extend to nearly 100 metres at an average grade of approximately 1.2% copper, with only occasional narrow barren intervals attributable to post-mineral dykes.

Locke explained how this broader column changes the development calculus:

"When you start to think about the mining strategy for this, there are mining methods that can allow you to take a much larger proportion of that column if it hangs together, which would materially reduce both your mining cost and therefore your economic cut-off grade, which means you're starting to take a much bigger column of rock."

This observation is shifting management's thinking away from a selective underground mining model - comparable to the room-and-pillar paste-backfill approach used at Kamoa-Kakula - toward a bulk mechanised underground operation. The practical implication is that a greater proportion of the mineralised column could be economically captured, substantially increasing the effective resource tonnage.

Scale Potential: From Millions to Half a Billion Tonnes

Using preliminary geometric assumptions, management has begun sketching the potential scale of the Pampa Medina system. If the mineralised area extends to approximately 2 km by 2 km with a true thickness of 20 metres, the contained ore could reach 120 to 150 million tonnes. Extending the true thickness to 60 metres - which the stacked manto geological model supports - pushes that figure toward 500 million tonnes.

Drilling has already confirmed mineralisation over an area exceeding 2 km², with the northeast–southwest trend being extended further by two active drill rigs. Importantly, recent holes are also intersecting evidence of mineralisation at greater depths than previously drilled, pointing to additional vertical extent that has not yet been quantified.

Locke was direct about the implications:

"Our views are very firmly intact that we believe this has potential to be a tier one asset. The ultra high-grade zone really changes our view about the quality of the asset and the potential for it to deliver exceptional return on investor capital."

Interview with Hayden Locke, President & CEO of Marimaca Copper

The Stacked Mantos Model Remains Intact

Despite the growing complexity of the mineralised system, Marimaca's underlying geological framework - a sediment-hosted copper deposit featuring stacked manto-style ore horizons within the Rancorét sedimentary unit - remains consistent with early interpretations. Mineralisation is hosted across three main units: the upper volcanics, the middle Rancorét sediments, and the basement meta-sediments.

Notably, recent drilling has begun to reveal mineralisation within the basement meta-sediments, a horizon that hosts the nearby historical Cachorro deposit at Antofagasta PLC. This opens an additional layer of geological prospectivity that was not part of the original Pampa Medina model, and one that management believes could further expand the system's endowment. The relationship between high organic matter content in black shales and the concentration of bornite-rich, high-grade mineralisation is becoming clearer, though fully predictive geological modelling is still in progress.

Maiden Resource Estimate and Path to Development

Marimaca intends to publish an initial inferred mineral resource estimate covering a subset of the Pampa Medina area - specifically the portion most densely drilled to date. Drilling is currently at approximately 150 by 150 metre spacing, and the resource will be accompanied by preliminary economics and a mining method study to provide investors with a reference framework.

Critically, management has been explicit that the maiden resource will represent only a fraction of what it believes is the prospective area. Two drill rigs are actively working to extend the mineralised horizon along strike to the northeast and southwest, meaning additional resources will likely be defined after the initial estimate is published.

The current drill program is also aimed at deeper targets, where emerging evidence suggests the system may have meaningful vertical extent beyond what has been drilled to date.

Relationship with the Marimaca Oxide Deposit

The MOD remains the company's near-term development priority. Marimaca is in advanced discussions with a large-scale acid producer to underwrite acid supply across the full life of the oxide operation - a key de-risking step given acid pricing uncertainty. Management states that even at conservative assumptions of $300 per tonne acid price and $5 per pound copper, the MOD alone is worth more than the company's current market capitalisation on a fully diluted basis of approximately C$1.1 billion.

The relationship between the MOD and Pampa Medina is still being evaluated. At relatively modest production scales - 25,000 to 30,000 tonnes of additional copper cathode annually - Pampa Medina could feasibly leverage MOD infrastructure including water, power, logistics, and supply chain. At larger scales, a standalone concentrator and cathode facility would likely be required.

Management is also actively structuring its financing for the MOD in a way that ring-fences that asset, preserving shareholders' unencumbered exposure to Pampa Medina's upside. "We can effectively reduce the amount of dilution to this incredible upside opportunity while still progressing the MOD," Locke noted.

Strategic Optionality and Major Miner Interest

The broader strategic picture for Marimaca is coming into focus. A large-scale deposit in Chile's low-cost copper belt, with access to established infrastructure, proximity to Antofagasta, and growing evidence of tier-one scale, represents a combination of attributes that the major mining companies are actively seeking. Copper supply deficits, driven by underinvestment in new projects and accelerating electrification demand, have intensified competition for quality development-stage assets.

Locke acknowledged the longer-term strategic implications:

"If you start to deliver a project that has 3 to 4 to 5 million tons of contained copper in it in the low coastal belt in Chile with access to infrastructure... that would grab the attention of just about every major mining company in the world because all of them are desperate for copper exposure."

For now, the focus is on drilling, resource definition, and securing the MOD financing structure. But the optionality embedded in the Pampa Medina discovery - whether as a standalone operation, an infrastructure-sharing arrangement with the MOD, or an eventual M&A catalyst - is becoming an increasingly material part of the investment case.

The Investment Thesis for Marimaca Copper

- Near-term value anchor: The Marimaca Oxide Deposit is management's base case for value, with modelling suggesting the asset alone exceeds the current share price at reasonable copper and acid price assumptions, implying Pampa Medina is currently priced near zero.

- Drilling momentum: 36 of 40+ holes have returned economic-grade mineralisation; the current program at 150×150 metre spacing is confirming continuity, with two rigs extending the system along strike and at depth.

- Grade quality: Ultra high-grade bornite intervals (up to 5.7% Cu, 62.6 g/t Ag) within a broader low-grade column present optionality on both selective high-grade and bulk tonnage mining strategies.

- Scale trajectory: Confirmed drilling over 2+ km² with open extensions to the north, south, east, and at depth; preliminary geometric modelling suggests 120–500 million tonnes of contained ore depending on true thickness assumptions.

- Mining method optionality: Evolving from a selective underground to a bulk mechanised model could lower unit costs and expand the effective cut-off grade, capturing substantially more of the mineralised column economically.

- Chile jurisdiction advantage: Located in the Antofagasta region with access to existing infrastructure - water, power, logistics, and acid supply - materially reducing greenfield development costs and timeline risk.

- Financing structure: Management is actively structuring MOD financing to ring-fence that asset and preserve shareholder exposure to Pampa Medina upside without diluting into the discovery.

- M&A optionality: A potential 3–5 million tonne contained copper endowment in a low-cost, infrastructure-rich jurisdiction is precisely the profile that major mining companies are targeting in the current supply-constrained copper market.

- Macro tailwind: Global copper demand, driven by electrification, grid expansion, and EV adoption, is structurally outpacing supply, creating a sustained premium for development-stage assets with demonstrated scale potential.

- Early-stage discovery premium: The stock is currently trading at a valuation that appears to ascribe minimal value to the Pampa Medina sulfide resource, creating asymmetric upside as resource definition milestones are reached.

Macro Thematic Analysis

The global copper market is entering a period of structural undersupply. Decades of declining ore grades at major mines, combined with years of capital underinvestment in new project development and rising demand from electrification - electric vehicles, grid infrastructure, and renewable energy buildout - have created a deficit that is proving difficult to close through existing supply alone.

Chile, the world's largest copper-producing nation, remains the most strategically important address for new copper development. Projects in the Antofagasta region benefit from established mining infrastructure, experienced labour, regulatory familiarity, and proximity to port. Against this backdrop, a discovery of Pampa Medina's apparent scale and grade profile is rare. As Locke put it: "All of them [major mining companies] are desperate for copper exposure." With contained copper endowment potentially reaching 3 to 5 million tonnes and a tier-one jurisdiction, Marimaca is positioned at the intersection of geological merit and macro necessity.

TL;DR - Executive Summary

Marimaca Copper's Pampa Medina discovery has grown well beyond initial expectations, with drilling confirming economic-grade mineralisation across more than 2 km² and ultra high-grade bornite intersections up to 5.7% copper with 62.6 g/t silver. The company's flagship Marimaca Oxide Deposit is advancing toward development and is valued by management as worth more than the current share price on a standalone basis, implying Pampa Medina is effectively unpriced by the market. A maiden inferred resource is expected to cover a subset of the drilled area, with two rigs extending the system along strike and at depth. The combination of a near-term de-risked oxide asset and a growing sulfide discovery in Chile's low-cost copper belt presents a materially asymmetric risk-reward profile for investors.

FAQs (AI Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed