Mining Alpha EP3 | The New Valuation Framework for Junior Gold Assets

Junior mining M&A at $500-600/oz signals sector revaluation opportunity for infrastructure-adjacent assets with production potential vs $50-150/oz typical valuations.

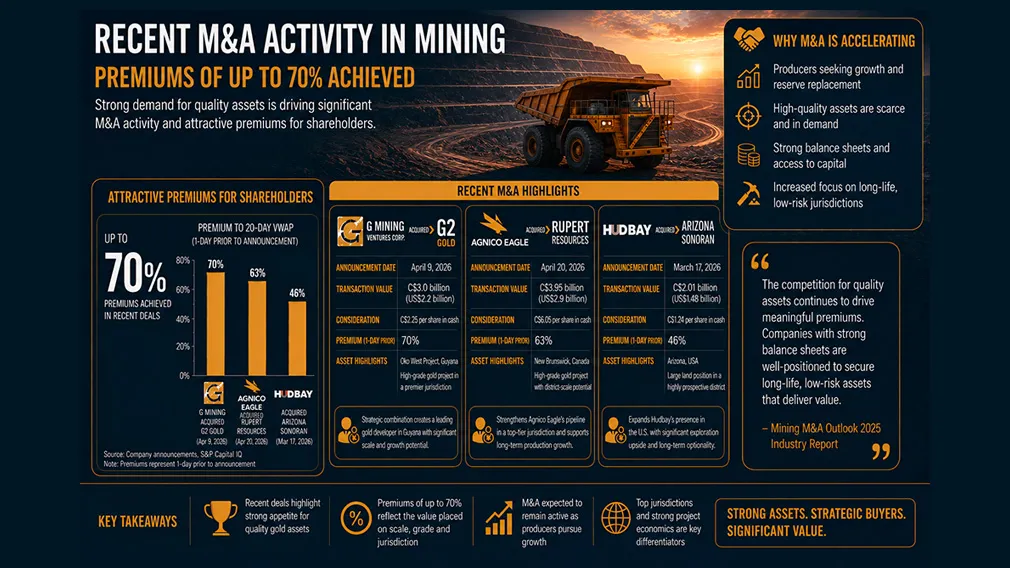

- Recent acquisitions by G Mining Ventures (G2 Goldfields at ~$600/oz) & Agnico Eagle (Rupert Resources at $500-600/oz) signal a fundamental revaluation of junior mining assets from the typical $50-150/oz range, with both deals commanding 70% premiums to market price.

- Assets located near existing mills, roads, power, and producing operations command significant valuation premiums due to reduced capital requirements and higher synergistic value, with some deals showing over $1 billion in potential synergies.

- Gentile's strategy focuses on 5-10 year holding periods, initial 1% portfolio allocations targeting 5-20% ownership stakes, post-discovery stage companies with clear pathways to production, and management teams with significant equity ownership (10-30% of company).

- After 9-years of full-time investing, Gentile has achieved 5-6 takeouts demonstrating the viability of identifying early-stage discoveries ($30M market caps) that mature into acquisition targets over 5-7 years, with current portfolio companies at various development stages.

- Only 5 new investments annually from ~500 meetings reviewed (1% conversion rate), prioritising assets with infrastructure proximity, strong management ownership, favourable jurisdictions, and geological potential for economic ounces rather than pure exploration plays.

The junior mining sector is experiencing a fundamental reassessment of asset valuations, driven by two landmark acquisitions that have established new pricing benchmarks for quality ounces. Michael Gentile, strategic investor and co-founder of Bastion Asset Management, argues in Episode #3 of Mining Alpha that recent deals by G Mining Ventures and Agnico Eagle represent "seminal moments" that could trigger sector-wide revaluation. With gold prices rising from $1,500 to $4,500 while junior resource stocks remained anchored at historical valuation levels, the gap between intrinsic value and market pricing has created what Gentile characterises as a significant opportunity for informed investors.

Landmark Transactions Establish New Valuation Framework

The acquisition of G2 Goldfields by G Mining Ventures at approximately $600 per ounce and Agnico Eagle's purchase of Rupert Resources at $500-600 per ounce mark a departure from the $50-150 per ounce valuations that have persisted throughout the recent gold price rally. Both transactions commanded 70% premiums to prevailing market prices, despite the target companies already trading at elevated levels due to M&A speculation.

These premium valuations reflect specific characteristics that major mining companies now prioritise: proximity to existing infrastructure, near-term production potential, and high synergistic value. In G Mining's case, the target asset sits directly adjacent to their 300,000-ounce-per-year operation currently under construction, potentially creating a combined 500,000-ounce annual production profile while eliminating over $1 billion in duplicate infrastructure costs.

The economic rationale becomes clear when examining the margin structure, as Gentile explains:

"If you don't have to build a mill, don't put any infrastructure in, any roads, any power, and all your primary cost is just a kilometer away and pulling that gold out of the ground at $2,000 an ounce, there's $2,500 of margin. And if those ounces can be produced in the near term, you can easily pay 600 dollars an ounce and you're still left with 1,900 dollars an ounce cash margins on that"

Infrastructure Proximity as Primary Value Driver

The emphasis on infrastructure-adjacent assets represents a strategic shift in how major mining companies approach growth. Rather than pursuing greenfield developments requiring billions in capital and multi-year permitting processes, acquirers are prioritising brownfield expansion opportunities that offer faster payback periods and higher internal rates of return.

Gentile's investment framework explicitly prioritises this dynamic. Current holdings including Radisson Mining (multiple mills surrounding the asset), Galleon Gold (Pan American Silver ownership stake, numerous hungry mills in Timmins camp), Big Ridge Gold (water access for barging ore to nearby mills), and Canterra Minerals (adjacent to Equinox's Valentine Gold operation) all share the common thread of existing infrastructure that dramatically reduces the capital intensity of bringing ounces into production.

This infrastructure focus extends beyond physical assets to include workforce availability, operational expertise, and established supply chains. Agnico Eagle's acquisition of Rupert Resources, while offering less natural synergies than the G Mining transaction, still benefits from existing producing operations in Finland, ensuring 20-30 years of regional production continuity with minimal incremental infrastructure investment.

Investment Process & Portfolio Construction

Gentile's approach combines concentrated conviction with systematic risk management. Operating with 30-35 core positions, he allocates initial capital at 1% of total portfolio value, targeting 5-20% ownership stakes in companies with $30 million market capitalisations or less. This structure allows for significant influence in strategic decision-making while maintaining portfolio diversification appropriate to the junior mining sector's inherent risks.

The investment process emphasises post-discovery opportunities rather than pure exploration plays. By entering after initial discovery holes validate geological potential, Gentile reduces discovery risk while maintaining substantial upside as resources expand and development de-risks. He acknowledges that even with rigorous due diligence, only 20-30% of investments will "go all the way" to production or acquisition - a batting average he considers strong given the sector's mathematical realities.

Position sizing scales with conviction and performance. Successful investments receive up to 5% of book capital across multiple financings over 5-10 year holding periods, while underperforming positions are capped at the initial 1% allocation. This "watering the flowers and pulling the weeds" methodology has produced 5 to 6 exits over 9-years of full-time investing, validating the timeline required for discovery-stage assets to mature into acquisition targets.

Interview with Michael Gentile, Gold Fund Manager & Investor

The Critical Role of Management Ownership

Beyond geological and infrastructure considerations, Gentile emphasises management team quality and alignment as critical investment criteria. Board and management ownership of 10-30% of outstanding shares serves as a primary filter, with particular weight given to market purchases and participation in subsequent financings rather than founder shares issued at nominal cost.

"Board ownership and management ownership is essential in the junior mining space," Gentile notes, explaining that meaningful equity stakes ensure management persistence through challenging periods and alignment with shareholder interests during strategic decisions. The combination of technical expertise (geology, engineering) and business acumen (finance, strategy, capital markets) provides the optimal skill mix for navigating the complex path from discovery to production or exit.

Past success - whether building producing mines or delivering shareholder returns through strategic sales - provides important validation, though Gentile acknowledges the challenge retail investors face in evaluating management quality when "every single one" claims to have a great team.

Improving Capital Access for Quality Projects

The financing environment for quality junior mining companies has improved markedly, with deals increasingly structured at 5-10% discounts to market without warrants, compared to historical norms of 20% discounts with full warrant coverage. This tightening of terms reflects growing investor recognition of the valuation gap between current market prices and potential M&A outcomes.

Gentile prioritises companies with clean capital structures, avoiding situations where previous financings have created warrant overhangs or concentrated positions among short-term oriented investors. The ability to raise capital on favourable terms over multi-year development timelines proves essential, as even well-managed projects consume significant capital before reaching production or exit.

Contrarian Cycle Management

With a 25-30 year history in commodity investing, Gentile emphasises cycle timing as crucial to success. His current deployment of capital reflects conviction in a 5-10 year precious metals bull market, driven by geopolitical instability, monetary policy dynamics, and structural supply constraints. While acknowledging short-term volatility from geopolitical events, he views market dislocations as buying opportunities rather than reasons to reduce exposure.

The contrarian approach extends to long-term portfolio management. Should gold become a consensus overweight allocation with widespread investor enthusiasm, Gentile indicates he would likely shift to 40-50% cash, waiting for more attractive entry points. This willingness to step aside during periods of excess stands in contrast to his current stance as a fully invested participant in what he views as an early-stage upcycle.

The recent M&A transactions have established that major mining companies will pay $500-600 per ounce for quality assets with infrastructure proximity, near-term production potential, and synergistic value - multiples of where most junior resource stocks currently trade. This pricing discovery creates opportunity for investors who can identify assets with these characteristics early in the development cycle. Success requires patience (5-10 year horizons), diversification (minimum 10-15 positions), rigorous evaluation of management quality and equity ownership, and focus on post-discovery assets with clear pathways to economic production. The improving financing environment and major miners' strong balance sheets support continued M&A activity, potentially driving sector-wide revaluation as the inventory of quality near-term assets depletes and attention shifts to earlier-stage development projects with the right characteristics.

TL;DR: Executive Summary

Recent acquisitions at $500-600/oz (G Mining/G2 Goldfields, Agnico Eagle/Rupert Resources) establish new valuation benchmarks for junior mining assets with infrastructure proximity and near-term production potential, representing 3-4x typical trading multiples and signaling potential sector revaluation. Major miners' strong balance sheets, limited inventory of quality near-term assets, and high gold margins ($1,900+/oz after $600 acquisition cost) support continued M&A activity. Investment opportunity exists in post-discovery assets with infrastructure access, strong management ownership, and 5-10 year development timelines, requiring diversified portfolios (10+ positions) and patient capital to capture value as projects mature into acquisition targets.

FAQs (AI Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

Stay Informed