Memory Chips Trade at 7x Earnings While Hyperscalers Lock Nuclear Capacity for the Same AI Load

Memory chip makers trade at 7x earnings while hyperscalers lock DRAM supply and nuclear power for the same AI load - chips’ August earnings may resolve gap.

- All three major memory makers exceeded $1 trillion in market capitalization, yet trade at 6–10x forward earnings, against the PHLX Semiconductor Index 30-stock average of 26x.

- Hyperscalers have locked approximately two-thirds of global server DRAM production through multiyear supply agreements, removing the demand uncertainty that historically drove memory cycle collapses (WSJ).

- The nuclear contracts are a direct uranium fuel demand signal: reactor construction, enriched fuel supply, and grid interconnection must mobilize ahead of the 2030–2035 delivery window.

- The condition that closes the 7x-to-26x valuation gap: Micron Q3 FY26 earnings confirming five-year contract expansion beyond the March 2026 first deal.

- If FY26 EPS guidance falls below $50 against the $60 consensus, or the Korean names decline to confirm contract progress on their next calls, they compress below 6x forward earnings.

Enterprise Token Rationing Is a Software Invoice Decision: Server DRAM Demand Grew 7x Year-Over-Year

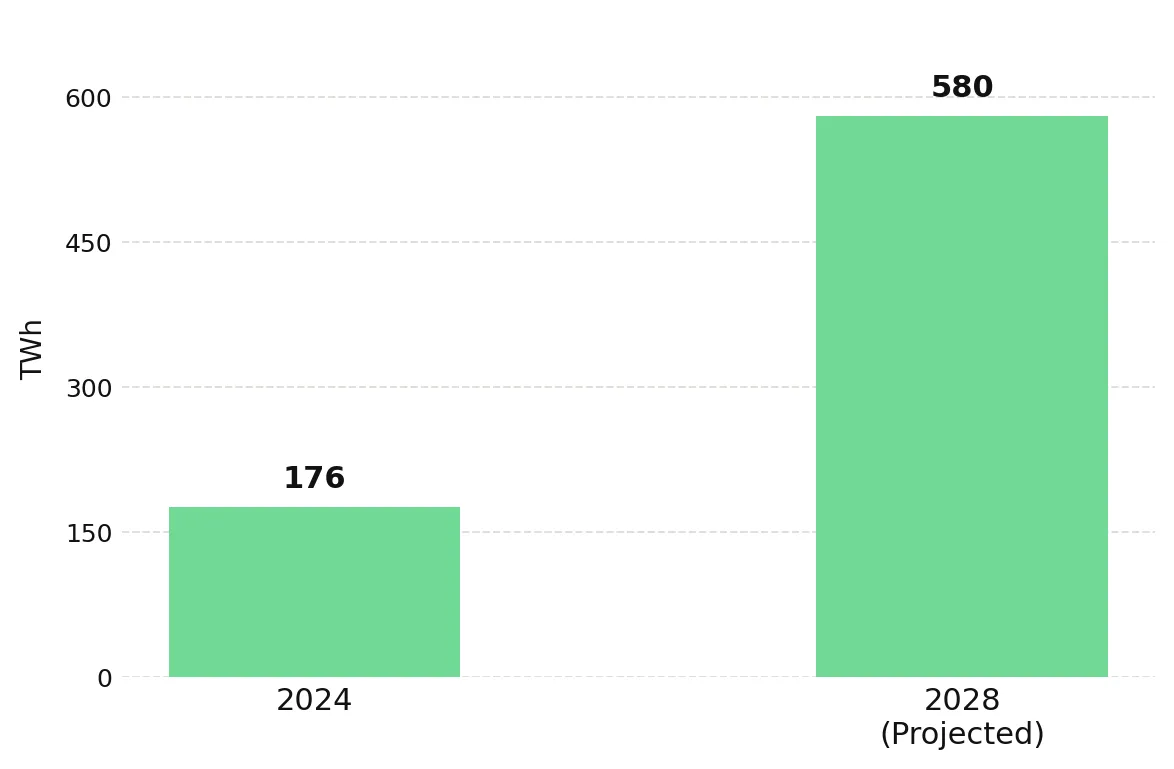

Enterprise AI cost rationing is being misread as infrastructure demand destruction. Uber exhausted its full-year AI budget by March; Meta CTO Andrew Bosworth instructed employees to stop using AI tokens; Microsoft restricted internal access to Anthropic's Claude Code. Google processed 3.2 quadrillion tokens per month in May - seven times the volume from a year earlier (WSJ). Enterprise rationing redirects which model tier handles a query; it does not remove the DRAM requirement at the hyperscaler layer processing those queries. Enterprise AI budget cuts are the wrong data layer - hyperscaler infrastructure procurement is the signal that moves memory chip valuations.

Hyperscalers Are Locking Both Chip Supply and Power Supply: Two Markets Pricing the Same Demand Differently

AI demand has exceeded manufacturing capacity at all three major memory producers, enabling multiyear supply agreements that partially replace spot revenue with contracted forward cash flows. Micron signed its first five-year deal at its March 2026 earnings report and confirmed "meaningful progress" on additional agreements the week of May 22 (WSJ). Sandisk disclosed five customers had signed long-term agreements covering more than one-third of its production capacity for the next fiscal year.

The contractual logic runs simultaneously in the power grid: Meta signed 20-year nuclear power agreements in January, targeting up to 6.6 GW of capacity by 2035 - the same 7x annual token volume growth validating the three-year DRAM demand shortfall is the electricity load growth requiring those nuclear gigawatts.

DRAM makers at 7x earnings and power equities at full infrastructure multiples are pricing the same AI demand story at opposite ends of the valuation spectrum, and the fuel supply chain behind those gigawatts is tightening at the commodity layer.

Base case: Micron Q3 FY26 earnings confirm five-year contract expansion past one-third capacity coverage and the Visible Alpha FY27 EPS consensus of $106 holds - re-rating from under 10x toward sector norms begins within two quarters. Bear case: Samsung and SK Hynix decline to confirm contract progress on their next calls and Micron FY26 EPS guidance falls below $50 - Korean names compress below 6x forward earnings.

Contract Coverage Ratios Are Unconfirmed: August Is the Disclosure Event That Resolves the Gap

Samsung (005930) and SK Hynix (000660) have not disclosed contract-to-capacity ratios comparable to Sandisk's one-third threshold - coverage depth cannot be independently verified before the next earnings cycle. Sizing a position ahead of August means carrying unquantified coverage risk that spot DRAM price screens and enterprise token headlines cannot resolve.

The specific number to watch at Micron Q3 FY26 earnings: five-year agreements signed beyond the March 2026 first deal - for the nuclear supply chain, the monitoring signal is not another hyperscaler announcement but the first quarterly earnings from a nuclear operator confirming that contracted gigawatts are converting into revenue, establishing that multi-decade power agreements are funding construction ahead of the 2030–2035 delivery window.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed