AI Power Demand & Utility Undercontracting Tighten Uranium Supply as Contract Prices Reach $90 per Pound

AI power demand and 13 years of utility under-contracting are driving uranium term prices to a 14-year high of $90/lb, with no new mine supply before 2030.

- Meta committed to 7.8 gigawatts of nuclear power purchase agreements and Microsoft to over 800 megawatts of dedicated reactor capacity in Q1 2026, establishing hyperscalers as a new uranium demand class that prioritizes supply certainty over price and supports term contract prices above spot.

- Utilities have undercontracted annual uranium replacement requirements for 13 consecutive years. In 2025, approximately 116 million pounds U3O8 were placed under long-term contracts, still below annual utility uranium requirements.

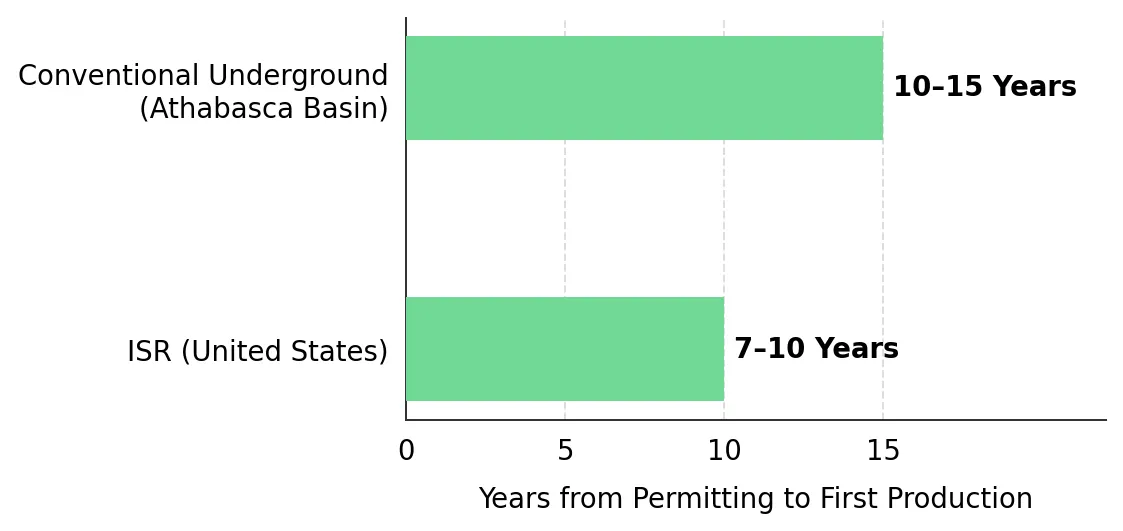

- In-situ recovery uranium projects in the US require 7 to 10 years from permitting to first production, and Athabasca Basin conventional mines require 10 to 15 years from discovery to output, meaning demand contracted in 2026 cannot be served by new primary supply before the early 2030s.

- US Section 232 Proclamation 11001 authorizes minimum import prices for uranium, creating a domestic pricing floor that decouples US producer realized prices from global spot dynamics.

- In-situ recovery producers, development-stage companies, and exploration-stage discoveries each carry a different catalyst timeline against the same uranium supply shortage, with project economics, jurisdiction, and development stage determining which companies re-rate first as utilities secure uranium supply further into the future.

Two Demand Shocks Are Arriving at the Same Time

Kazatomprom's 2026 nominal production target stands at 29,697 tU, down 10% from 32,777 tU under prior subsoil use agreements. Cameco indicated McArthur River production recovery remains below prior restart expectations, limiting the volume available to utilities already facing reduced Kazakh supply. SOMAÏR produced zero output in 2025 under Niger's military junta. These disruptions remove incremental pounds from a market where long-term contracting already exceeds near-term uranium deliveries needed by utilities. None explains why long-term U3O8 contract prices reached $90 per pound by end of Q1 2026, the highest since 2008, per Cameco's monthly price reference data.

In Q1 2026, Meta signed agreements for up to 7.8 gigawatts of nuclear capacity and Microsoft executed arrangements for over 800 megawatts exclusively for data center operations. These buyers are turning to nuclear because it provides large amounts of uninterrupted electricity without the fuel-price volatility of natural gas.

Traditional nuclear utilities, which account for approximately 90% of global uranium demand through multi-year long-term supply contracts, remain undercontracted for the 13th consecutive year. Two distinct demand forces are now competing to secure future uranium supply contracts from existing uranium mines that cannot expand production within the window of those contracts requiring delivery.

AI Nuclear Procurement & the Case for Baseload Power

AI data centers require large amounts of continuous electricity at gigawatt scale. Wind and solar require large battery storage systems to deliver uninterrupted electricity, increasing delivered electricity costs versus continuously operating nuclear generation. Natural gas can provide continuous power generation but carries commodity price exposure: Brent crude exceeded $111 per barrel in early May 2026 following the Iran conflict's restriction of Strait of Hormuz transit. Nuclear eliminates both risks simultaneously.

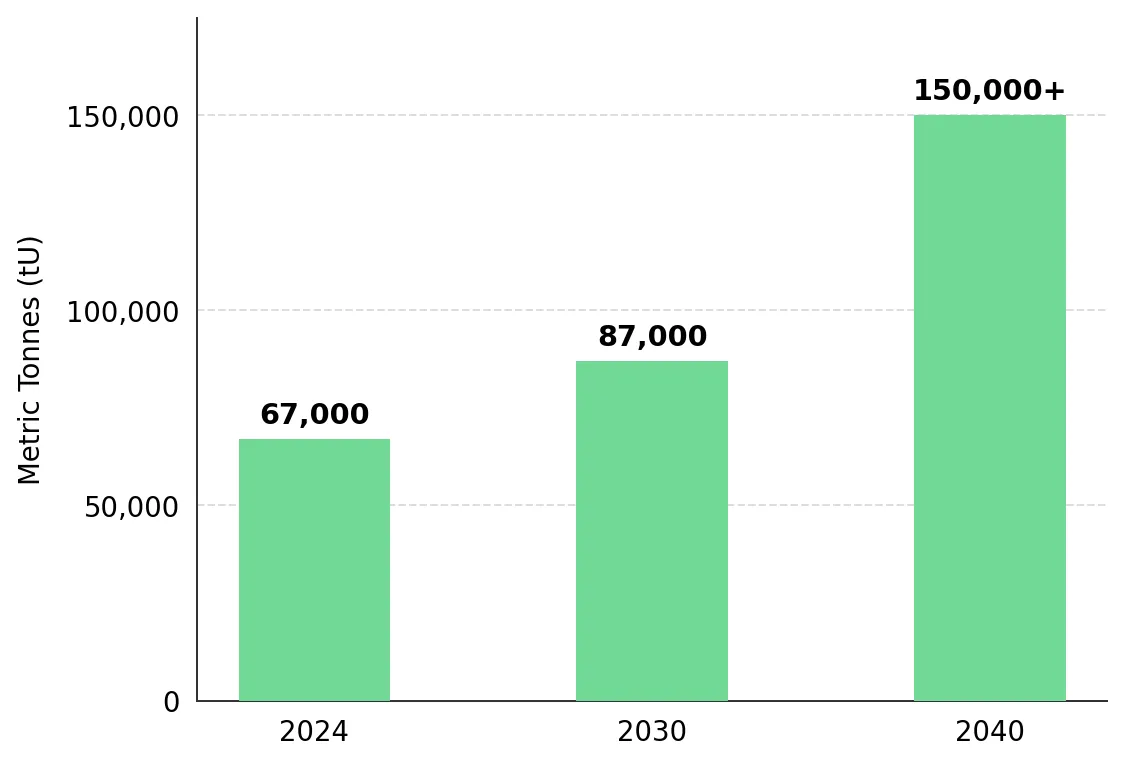

The IEA's World Energy Outlook 2025 projects global data center electricity consumption growing faster than any prior demand category in the agency's forecast set. Under the Announced Pledges Scenario, annual nuclear investment rises from approximately $70 billion today to $210 billion by 2035. The World Nuclear Association's 2025 Nuclear Fuel Report projects uranium demand at 87,000 metric tonnes per year by 2030, a 28% increase from the 2024 baseline of 67,000 metric tonnes. Hyperscalers purchasing supply certainty rather than managing spot price are willing to accept above-spot term pricing, raising the floor that utilities must compete against when they return to the contract market.

Utilities and hyperscalers are increasingly competing for future uranium supply as AI-related nuclear procurement expands beyond traditional reactor demand. Philip Williams, Chief Executive Officer of IsoEnergy Ltd., described how utilities risk falling behind newer entrants securing long-term uranium exposure:

“Think about utilities. Think about tech companies. That’s the next wave. I think the North American utilities and maybe the European utilities are kind of on the back foot here, and they’re going to have to be scrambling to play a game of catch up.”

Thirteen Years of Under-Contracting & the Compounding Procurement Problem

Uranium utilities contract 2 to 5 years ahead of delivery, with uncovered reactor requirements extending 7 to 10 years forward. When a utility undercontracts against its annual replacement requirement, the unfilled uranium requirement grows each year. The 13-year streak of below-replacement-rate contracting has produced a cumulative shortfall that near-term spot purchasing cannot resolve.

Cameco reported approximately 116 million pounds U3O8 placed under long-term contracts in 2025, still below the level needed to replace annual reactor fuel consumption. Secondary supply inventories from the post-Fukushima oversupply period have been drawn down, removing the inventory cushion that allowed utilities to avoid buying directly from uranium producers throughout the 2010s. Long-term U3O8 contract prices reached $90 per pound by end of Q1 2026 while spot prices held between approximately $85 and $87 per pound.

Scale creates measurable commercial advantages for uranium producers negotiating long-term supply agreements with utilities. William Sheriff, Founder and Executive Chairman of enCore Energy Corp., explains how production scale directly affects cost of capital and long-term contracting strength:

"In terms of the ISR business, you're going to have to have some producers that produce more than a million pounds a year or you're going to be essentially running a mom and pop grocery store on the corner. Your credit ratings go up, so your cost of capital goes down."

Primary Supply Cannot Respond Within the Demand Window

In-situ recovery uranium projects in the US require 7 to 10 years from initial permitting to first production. Conventional underground mines in Canada's Athabasca Basin require 10 to 15 years from discovery to commercial output. The mine supply that will serve contracts signed in 2026 either already exists or is in late-stage development today.

Kazakhstan accounted for approximately 43% of global primary uranium production in 2024 and has adopted a "value over volume" production philosophy. Kazatomprom's August 2025 guidance revision reduced its 2026 nominal production target from 32,777 tU to 29,697 tU, a reduction of approximately 8 million pounds representing roughly 5% of annual global supply. The company stated that current market conditions do not justify returning to full production capacity.

ATHA Energy Corp. is advancing the Angilak Uranium Project in Nunavut, where 2025 drilling returned mineralization in every target tested, including a 34.7-meter interval grading up to 8.16% U3O8 at the RIB target. The company believes the scale of mineralization identified across the Angilak basin compares favorably with major Athabasca Basin uranium systems. Troy Boisjoli, Chief Executive Officer of ATHA Energy, contrasted the project’s mineralized strike extent against some of Canada’s largest uranium deposits:

"You look at the strike length of some of the major uranium deposits in the basin. Arrow has a strike length currently of plus or minus 900 meters. Cigar Lake, same thing. You're under a kilometer in strike length. And we have mineralization contiguously in the Rib area over 14 kilometers."

US Policy & the Domestic Pricing Architecture

US Section 232 Proclamation 11001 designates foreign uranium reliance as a national security threat and authorizes the Commerce Secretary to negotiate trade adjustments including tariffs, import quotas, and minimum import prices. Tariffs were not imposed at issuance and negotiations are ongoing. The authorization to impose minimum import prices establishes a policy-supported pricing floor that operates independent of global spot market movements.

This follows uranium's reinstatement to the USGS Critical Minerals List in November 2025, the January 2026 award of $2.7 billion in Department of Energy enrichment contracts to Centrus and two additional operators, and the 2024 Prohibiting Russian Uranium Imports Act, which removed the largest non-Western enriched uranium supplier from the US utility procurement pool. Each measure narrows the competitive field for US producers, cumulatively establishing a policy framework that supports uranium selling prices above global production-cost levels.

Energy Fuels Inc. holds supply contracts with price floors through 2032. Mark Chalmers, former Chief Executive Officer of Energy Fuels Inc., quantifies the company's uranium production position:

"In the meantime, it’s all about uranium revenue. We'll give guidance up to 2.5 million pounds, and that's greater than anybody else in the US. Really good cost structures, and prices are firming. So that is the revenue story right now."

The Development Spectrum & Investment Positioning

Producers, developers, and explorers each benefit differently from the same uranium supply shortage. Producers capture the long-term contract price of $90 per pound through existing supply agreements. Developers become more valuable as higher long-term uranium prices improve project economics and support future construction decisions. Explorers provide exposure to new uranium discoveries in Tier-1 jurisdictions that utilities and hyperscalers are more likely to secure long-term supply from.

IsoEnergy Ltd. completed the Tony M Mine bulk sample in Utah's Henry Mountains in April 2026, extracting approximately 2,100 tonnes with zero lost-time incidents. A Preliminary Economic Assessment incorporating actual bulk sample cost data is targeting completion before year-end 2026, with processing planned through Energy Fuels' White Mesa Mill under a toll milling arrangement. The company holds approximately C$144 million in cash and equivalents funding the Tony M production decision and drilling at the Hurricane deposit in Saskatchewan.

Atomic Eagle Ltd. holds the Muntanga Uranium Project in Zambia, where a Feasibility Study in April 2026 models after-tax NPV at an 8% discount rate of US$243 million, cash operating costs of US$32.20 per pound, and a post-tax payback of 3.5 years at approximately US$86 per pound. Resources stand at 58.8 million pounds U3O8 at 309 parts per million following a 24% increase in March 2026. Phil Hoskins, Chief Executive Officer of Atomic Eagle Ltd., frames the production timeline against the strategic procurement cycle utilities and hyperscalers are now entering:

“If you're operating in a stable and credible jurisdiction like Zambia and can bring new uranium pounds into production by around 2030 - which is a realistic target for us - then you're well positioned within the window that these groups are looking for.”

The Investment Thesis for Uranium

- Long-term U3O8 contract prices at $90 per pound confirm that institutional buyers are already paying higher prices to secure future uranium supply, making long-term contract pricing the key benchmark for evaluating project economics over near-term spot levels.

- In-situ recovery projects require 7 to 10 years from US permitting to production and Athabasca Basin conventional mines require 10 to 15 years from discovery to output, meaning no new primary supply can reach the market before the early 2030s regardless of demand signals confirmed in 2026, which insulates current producers, developers, and Tier-1 explorers from near-term supply competition.

- US Section 232 Proclamation 11001, authorizing minimum import prices for uranium, creates a domestic pricing floor independent of global spot dynamics, reducing cash flow risk for producers and improving risk-adjusted returns for developers advancing in-situ recovery projects under the US permitting framework.

- Utilities and hyperscalers contracting for supply certainty are more likely to award long-term contracts to Tier-1 jurisdictions with permitting stability and transparent regulatory frameworks, distinguishing them from cost-equivalent deposits in higher sovereign-risk environments in long-term contract negotiations.

- Producers capture the long-term contract price at $90 per pound today; developers become more valuable as higher uranium prices improve project economics; and explorers provide exposure to uranium discoveries that may become strategically important as the demand-supply gap peaks in the early 2030s.

The uranium market in May 2026 is being shaped by utilities and hyperscalers securing more future uranium supply than miners can deliver within the current development timeline. Utilities remain undercontracted after 13 consecutive years below replacement-rate procurement, while hyperscalers including Meta and Microsoft are entering nuclear contracting to secure continuous electricity supply for AI infrastructure. At the same time, US in-situ recovery projects require 7 to 10 years to reach production and Athabasca Basin conventional mines require 10 to 15 years, limiting the industry's ability to respond before the early 2030s.

Long-term U3O8 contract prices reaching $90 per pound, the highest since 2008, indicate that institutional buyers are already paying higher prices to secure future uranium supply. For investors, the key question is which producers, developers, and exploration-stage companies control projects in jurisdictions capable of capturing long-term utility and hyperscaler contracting before uranium spot prices catch up to the supply shortage.

TL;DR

Two structural demand forces are converging on a uranium market that cannot respond with new supply before the early 2030s. AI hyperscalers including Meta at 7.8 gigawatts and Microsoft at 800-plus megawatts have entered nuclear fuel procurement prioritizing supply certainty over price. Traditional utilities, undercontracted for 13 consecutive years per Cameco's 2025 analysis, face a compounding shortfall that spot purchasing cannot resolve. Kazatomprom has reduced 2026 output by approximately 5% below licensed capacity. Long-term U3O8 contract prices at $90 per pound, the highest since 2008, already price in forward supply risk. Section 232 Proclamation 11001 adds a domestic pricing floor for US producers. Across producers, developers, and explorers, the uranium investment case is structural and independent of short-term geopolitical triggers.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

Stay Informed