Meridian Mining (MNO) - High-Grade Starter Pit Could Fund Project

Interview with Gilbert Clark, Executive Chairman of Meridian Mining (TSX: MNO)

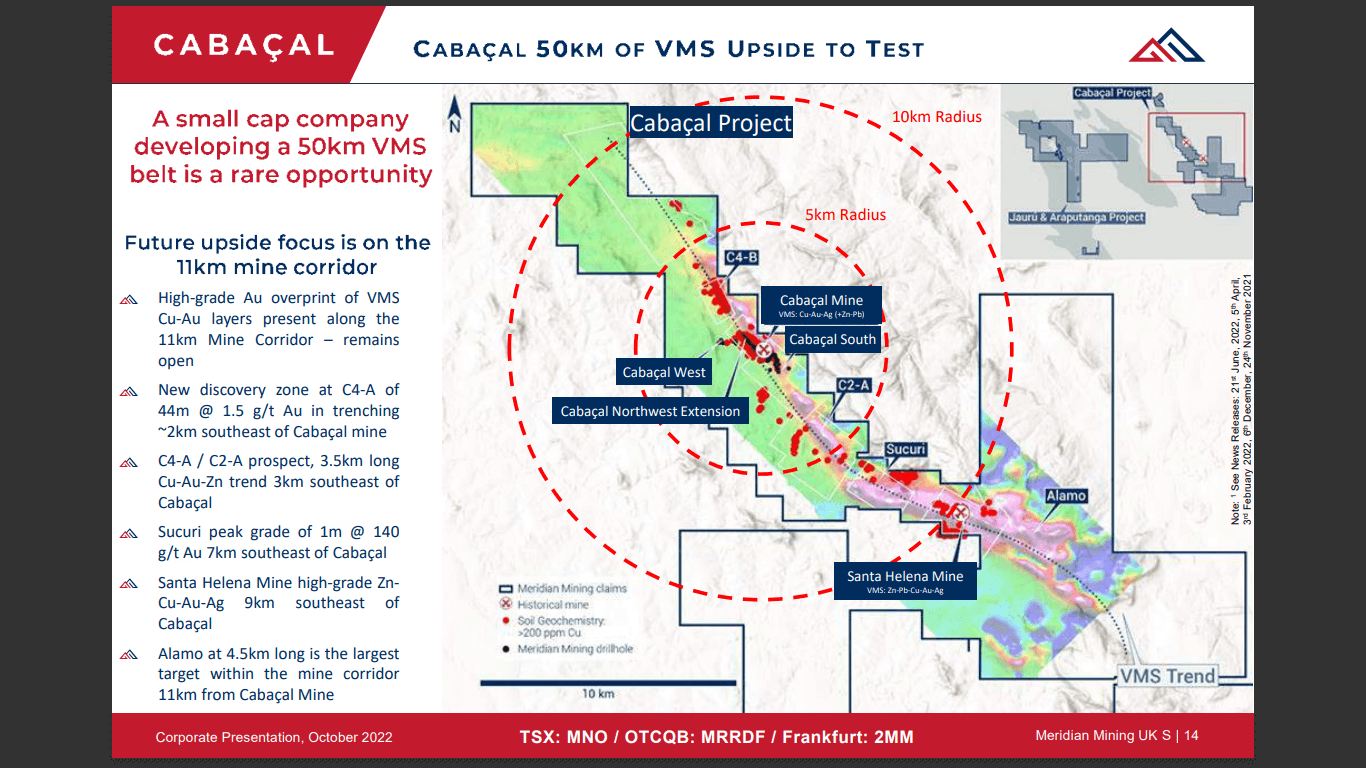

Meridian Mining UK S aims to become the next mid-tier copper, silver and gold developer and producer in Brazil with its focus on the development of its Cabaçal copper-gold-silver project in the state of Mato Grosso. The Cabaçal project is an advanced-stage district-scale VMS deposit, which was discovered in 1983 by BP Minerals. The deposit contains broad zones of coalescing Cu-Au mineralization which starts close to the surface and is open at a depth of 175 m whilst extending 2,000 m along strike.

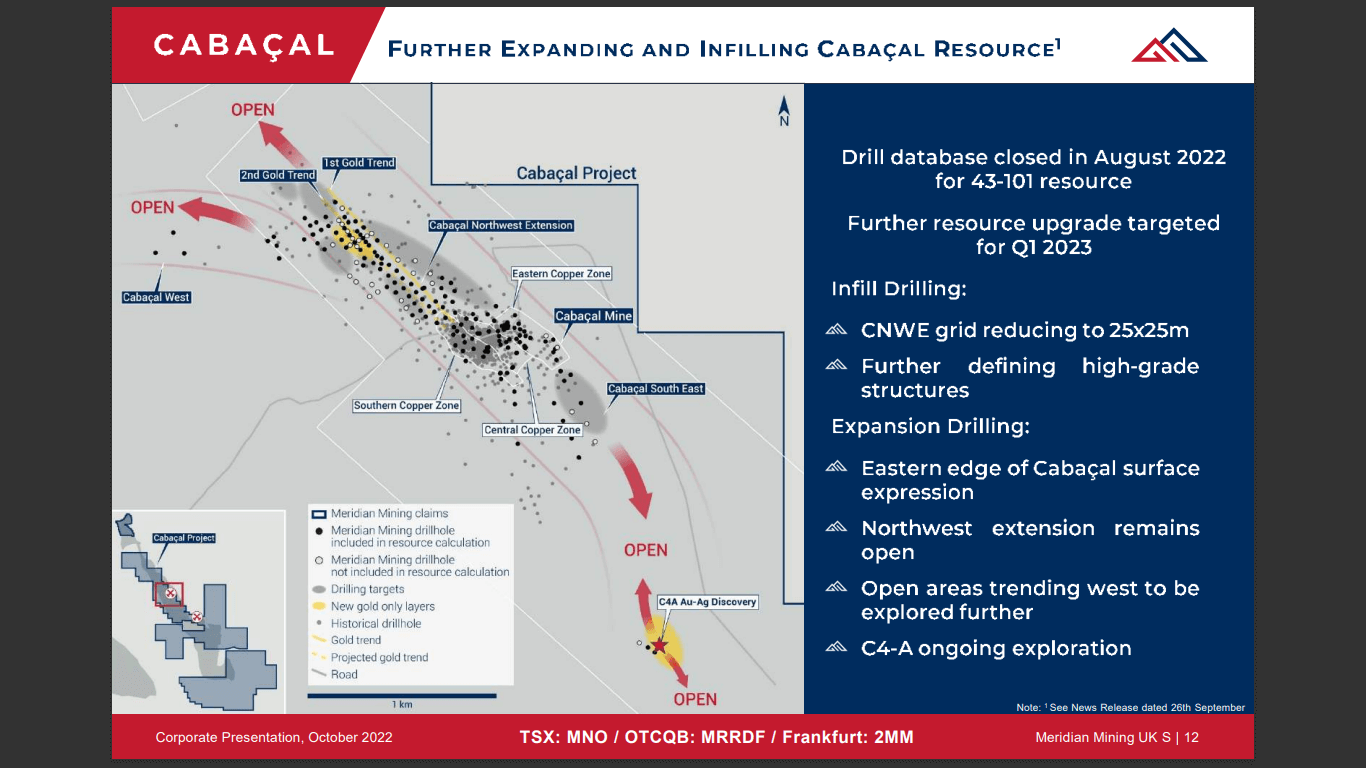

The company on the 6th of September 2022 released an update to its Cabaçal mine corridor exploration program. The exploration program was able to successfully link the C4-A gold/silver discovery with the Cabaçal deposit through the implementation of an IP survey, which has also been able to identify multiple targets for follow-up evaluation and future drill programs.

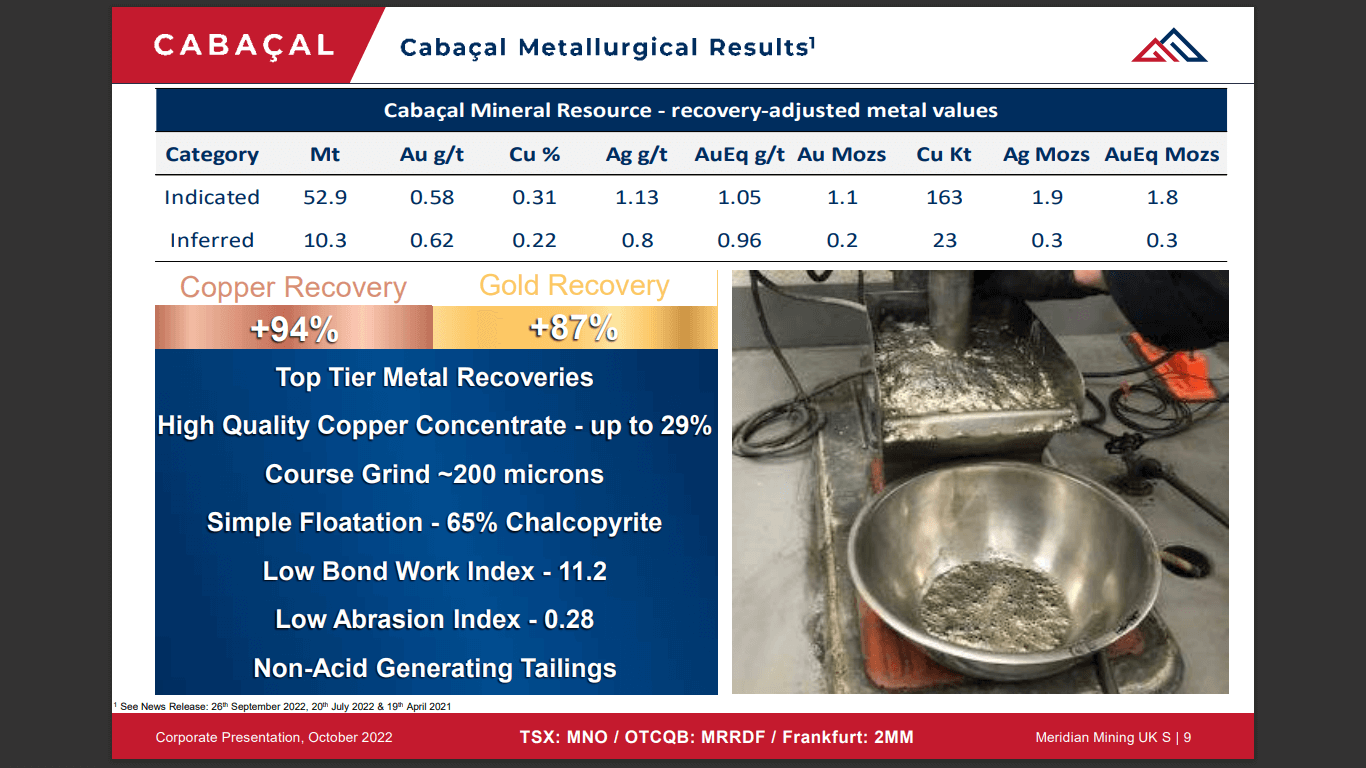

Meridian Mining UK S on the 26th of September 2022, released the maiden mineral resource estimate for its Cabaçal copper-gold-silver project VMS deposit. The mineral resource estimate was conducted by H&S Consultants Pty Ltd. and consists of 1.1 million ounces of gold, 168 kilotons of copper and 2.4 million ounces of silver in the indicated category with a further 0.2 million ounces of gold, 24.5 kilotons of copper and 0.4 million ounces of silver in the inferred category.

The resource is located close to the surface and extends for more than 1.9 km in length remaining open, with the ongoing expansion drilling initiatives continuing to intercept mineralisation at the resource’s boundary. Meridian Mining UK S believes that the mineral resource estimate shows the potential to be a long-life, stand-alone and open-pit operation within the larger Cabaçal VMS belt.

Cabaçal Copper-Gold VMS deposit

Meridian Mining UK S on the 26th of September 2022, released the maiden mineral resource estimate for its Cabaçal copper-gold-silver project VMS deposit. The mineral resource estimate was conducted by H&S Consultants Pty Ltd. and consists of 1.1 million ounces of gold, 168 kilotons of copper and 2.4 million ounces of silver in the indicated category with a further 0.2 million ounces of gold, 24.5 kilotons of copper and 0.4 million ounces of silver in the inferred category.

The Maiden mineral resource estimate was not met with support from the market, with the company’s shares trading sideways on the day of and days following its publishing. Gilbert Clarke, the Executive Director of Meridian Mining UK S, explains what he believes may have been the challenge:

“Inside that resource, which is I think the part we should have communicated better; I should have communicated that better was there’s actually a very high-grade 40 million tons at nearly 1% Copper equivalent. And that's what we're going to be mining for the first 15 years of the mine. And then, on top of that, we've identified an area in the Northwest extension to start our mining to focus our mining schedule on and that's 3.5 million tons at about 2.5 g/t Gold or 1.6% Copper equivalent. So, it's a very economical deposit. But I think people just looked at the resource statement and I guess that's looking at the leaves on the tree and didn't see the solid hardwood trunk that's underneath it.”

The mineral resource estimate shows a high-grade mineralisation zone which hosts 1.8 million ounces of gold equivalent in the indicated category and 0.8 million ounces of gold in the inferred category. The high-grade mineralisation lies close to the surface, with the company believing that it is the ideal deposit for low-cost open-pit mining. The metallurgy of the deposit adds to its allure, with recoveries ranging from 91% for copper and 90% for gold.

“I think if it was published 3 years ago, it would have been a unicorn mining junior would have been over a billion-dollar market cap because it's great to have these answers these high-grade but if you can't get it out of the ground, it's worthless. So, what Cabaçal has is like this high-grade, starting at 40 million tons 1% Copper, 1.4% Gold equivalent, but our recoveries on that Copper is above 92%, 91%. Gold is sort of approaching 90% recovery. So, we get all of that metal out and that's what drives the economics.”

The company plans to first mine the high-grade Northwest extension of the project upon initiating production at the project, with its economics proving to be very attractive.

“What we're saying is, of course, we're going to focus on the high-grade Northwest extension first. We can pay off all that, well, I think we can remodel it. We have internally modelled it. We can pay off the debt component, say at 210 to 220 million in say 12 months. “

Envisioned operation and ongoing exploration

Meridian Mining UK S plans to initiate its operations at the Cabaçal project by first focusing on the high-grade northwest extension. The rationale behind first initiating production at the northwest extension is that the company will be able to generate cash flow through the gold production, which will enable the company to be in a position where it may more easily raise funds to advance the rest of the project.

“You could say and pay off your debt component for the very high-grade, still mine the high-grade pit, build up your cash. Then the banks will come to you, this is pretty much the norm and say, let's refinance. Let's increase throughput to say 3, 3.5, 4 million tons, drop and push it through. And this is 101 mining, 101 equity growth. So, this is what we're really focused on. We've got that big high-grade pit because it's so high-grade and so easy and so cheap to mine, we don't need super high commodity prices to make positive cash flow.”

The initial economic studies of the company show that it will be able to produce gold at USD$ 1650, copper at approximately USD$ 359 and silver at USD$ 21, which shows the low operational costs associated with the high-grade deposit.

“We did our long-term, we did a 5-year banking consensus at USD$ 1650 for gold and USD$ 359 for copper, USD$ 21 for silver. And even if we were to drop that you'll still be making money. We're looking at our OPEX, it is projected to be sort of USD$ 1,650 a ton. So, it's really interesting that low CAPEX, because we compare us to say one of these porphyries or a big underground mine, it's billions.”

The company also on the 6th of September 2022 released an update to its Cabaçal mine corridor exploration program. The exploration program was able to successfully link the C4-A gold/silver discovery with the Cabaçal deposit through the implementation of an IP survey, which has also been able to identify multiple targets for follow-up evaluation and future drill programs.

Current finances and future plans

Meridian Mining UK S sits with a current cash balance of approximately CAD$ 5 million, with the company expecting to add to its treasury another CAD$ 1.8 million in the near future. The additional funds are due to the expiry of various warrants issued in previous capital raises.

“Cash on hand, just under CAD$ 5 million. We actually just had more warrants over CAD$ 0.30 warrants converted. There's not going to be this if you got 5 million warrants out there. They will all be converted in the coming weeks and months, it gives us another CAD$ 1.8 million, so we're not sort of, oh, we're going to have to raise money straight away and we're worried about it.”

The company does not foresee the need to raise any funds in the near future but does believe that it is undervalued.

“The equity markets are what they are. It provides, in my view, the market is really given a discount, a very great discount at the entry point for people. Now when you look at our share price, I think it's circa CAD$ 0.49, CAD$ 0.50 a share… I mean, it's a fantastic investment opportunity. I can't give a comparison.”

The need to raise funds may arise in the future for Meridian Mining UK S, but should that day come, the company will be cognisant regarding how it raises its funds. Clark explains that aside from the company not wanting to dilute its shares, it also wants to create an environment where investors may become long-term shareholders in the company.

“It's always easy to raise money, it's not always easy to raise the correct money for the existing shareholders and the incoming shareholders. That's the key. We don't want to destroy the equity value of the existing shareholders. Normally, when you have people, investors come in. Again, we don't want people to come in and just dump the stock when they've got 20% up. We want to see those long-term retail, high net worth institutional investors. And they're the ones I keep communicating to. It's very easy to raise a speculative 25% discount and all this stuff and nonsense, but what you want is partners going forward.”

Clark explains that various analysts have speculated that the company’s share price may rise from its current CAD$ 0.50 per share price to anywhere between CAD$ 1.50 to CAD$ 2.60.

The company plans to further continue to create value for its shareholders through various exploration initiatives in the near future, including its ongoing expansion drilling campaign. The expansion drilling campaign is aimed at defining the utmost economic limits of the project as well as converting the project’s inferred mineral resources to the indicated category.

“We've got three bank analysts now following us, mining analysts and their price range from CAD$ 1.50, CAD$ 1.60 to CAD$ 2.50. So none of them say it's a CAD$ 0.20 or CAD$ 0.30 of CAD$ 0.550 of this, this is CAD$ 1.50, CAD$ 1.60, CAD$ 2.60 stock. So this is the opportunity, you come in now you're looking at that three times multiple and this is what all the mining people say or mining investors. Where do I find the company that has got the opportunity to do a three or four or 10 times multiple, I think this is the asset that's going to drive it.”

To find out more, go to the Meridian Mining website

Analyst's Notes

Subscribe to Our Channel

Stay Informed