Minera Alamos (MAI) - Classy Gold Team Repeating Previous Success

We catch up with Doug Ramshaw, President and Director of Minera Alamos and disucss their strategy to get Santana and new asset Cerro De Oro into production

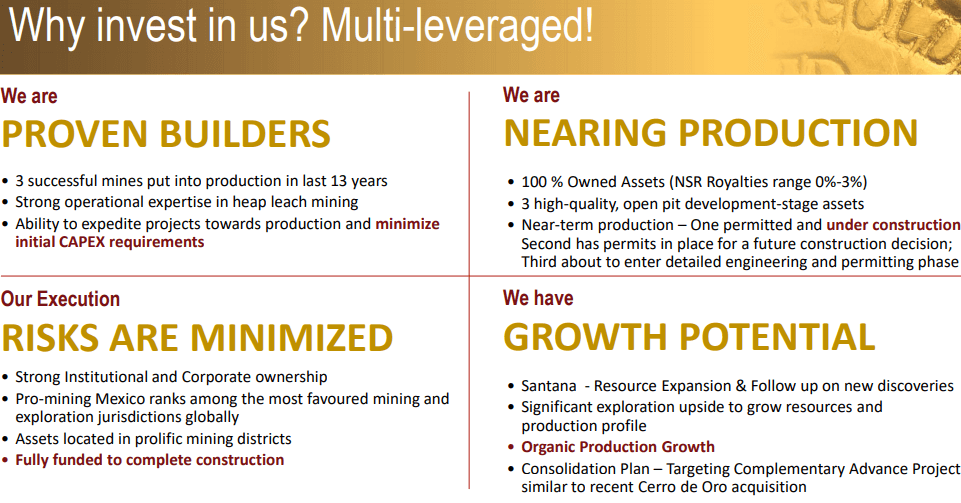

Minera Alamos is a profitable Mexican gold developer using low-cost heap leach on low-grade ore to generate a profit. They've done it before at Castle Gold. There is a smart management team of Doug Ramshaw and Darren Koningen who are focused on getting to the first gold pour in 2021.

We catch up with Doug Ramshaw, President and Director of Minera Alamos and talk through their strategy to get Santana, and new asset, Cerro De Oro into production. Their 3rd asset La Fortuna has a slightly different profile and will be brought into production later. We like the low-cost approach of buying a second hand mill from the US, using heap leach, low G&A and realistic M&A. They have a Resource which they can talk to the market about.

Company Overview

Minera is a mine development team focused on Mexico. They have their first construction due for completion in Q1 of 2021 and first Gold production in Q2 of 2021 and then they have a series of pipeline projects. Their goal is to become a new, bigger gold producer but first are completing the foundations to build the first mine and a solid foundation for growth. They are excited to be on the cusp of their first Gold production in 2021.

A Change of Focus: Data on Santana & Cerro de Oro

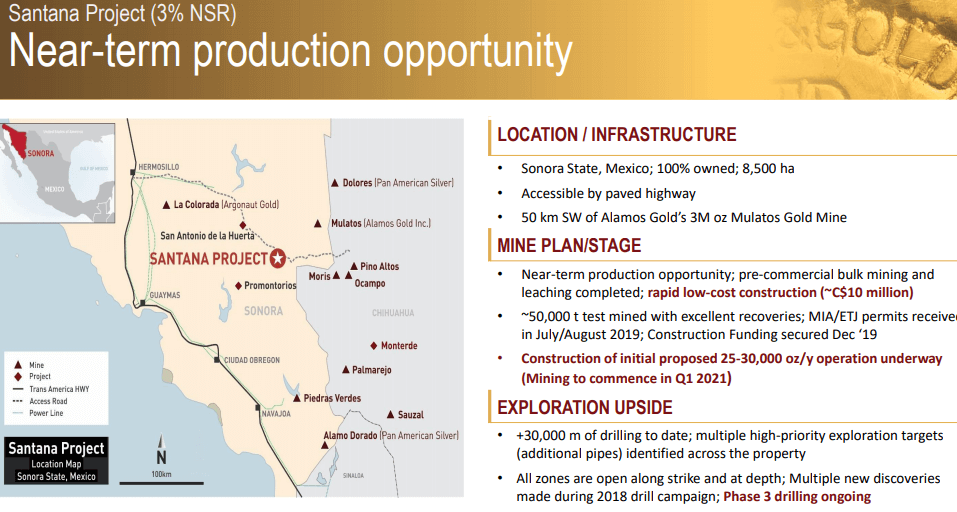

Their first project was Fortuna, but the number 1 project now is Santana, followed very quickly by Cerra de Oro. Cerra de Oro, like Santana, will be a very simple heap leach build; low Capex with a build cost of CAD$10M-12M. La Fortuna has modest Capex for a 50,000oz/year operation at CAD$27M, but it's almost 3.5 x what Santana would cost to build. It also has a slightly longer construction time and it’s more complex than building a heap leach. Fortuna also needs a bit more exploration. They did the PEA off a high-grade, 5-year starter pit but it would be better to have a project that at least is starting with a 7-8-year mine life, as opposed to 5 years.

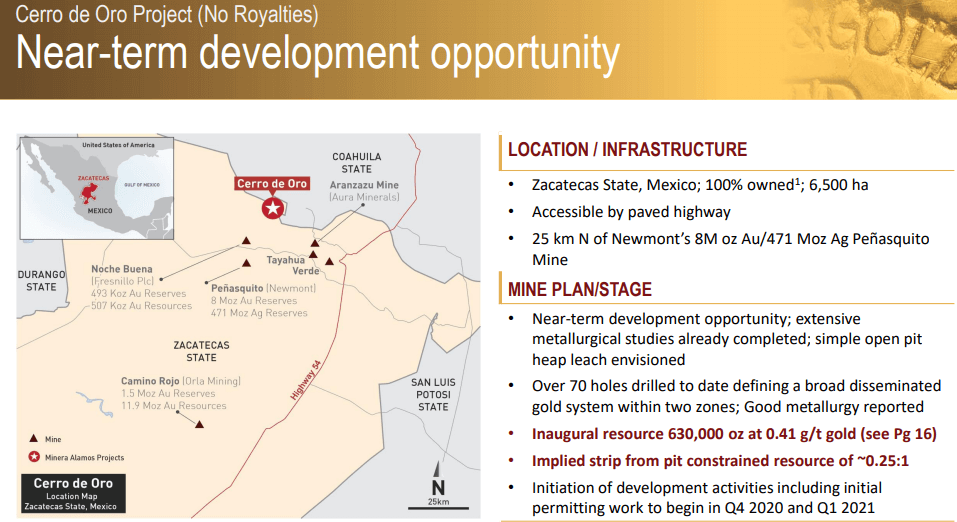

Cerra de Oro, for so many reasons, is higher up the list than Fortuna and when that is built it will be a testimony to the team and the jurisdiction they operate in. There are very few jurisdictions in the world where in August 2020 you can acquire a Gold project with no permits on it and within 2-years be producing Gold from it, which is their goal, by summer of 2022.

The Heap Leach Process

The technical report for Cerro de Oro should be out within a couple of weeks so people can really look into the numbers. They have used conservative figures in low gold prices and high mining costs for the report but it's important to have a conservative base case and then, as you refine the data, work up the numbers from there.

It's a heap-leach project and there is plenty of land around it for building heap leach pads, etc. It will be similar to Santana in producing loaded carbon and not building an ADR there to keep the Capex numbers similar to the final numbers at Santana.

The Santana and Cerro de Oro projects will run very similarly. The crucial thing with heap leach is the metallurgical characteristics of the ore. At Santana they were lucky to have a 50,000t heap leach pad at site which gave them a good understanding of how the ore leaches. At Cerro de Oro, a lot of historical work has been done and they plan to do more met work in the new year.

Buy the Mystery, Sell the History: Understanding the Approach

Santana could be the cornerstone project for Minera at 25,000oz-30,000/year, potentially more with further exploration but there is little information on Santana available to the market. But the resource statement is coming soon. They are completing phase 3 drilling now, which will be incorporated into it.

The 25,000oz-30,000oz/year is the year 1 production target for Santana without any expansion and just with those open pits opening up in Y2, it gets up to a steady state of 45,000-50,000/pa. After that, it will be about exploration upside.

In terms of the market, the reason that Minera Alamos is performing is due to jurisdiction. Cerro de Oro has highlighted that the permitting environment in Mexico and the geological prospectivity there is fantastic for the kinds of projects that they like but there are very few jurisdictions in the world where you could pick up an asset like Cerro de Oro and have it in production within 2-years. Mexico offers an environment where you can get on with the process and like Minera aim to build 3 mines over the next 4-years. In Canada, the process takes a lot longer mainly due to the permitting process.

Expectations & Concerns of Institutional Investors

Minera has Osisko as a partner on the institutional side and they are likely to become more institutional as they build Santana. They also have Donald Smith and Aegis, US generalist investors and going forward, they want to appeal to generalist investors as well as mining investment funds.

Much of the M&A Minera are talking about now are mergers of equals. Corex and Minera was a merger of equals 2.5-years ago, putting together 2x CAD$25M-companies creating value by bringing them together. Similar mergers have happened with Argonauts-Alio and Terangars-Endeavours and it’s a good direction for the industry to be heading in.

Cost: Why is the CapEx so Low?

There are 2 parts of the plant at Santana, and they’re not building a refinery at site. Instead, they are building a simple carbon plant and carbon recovery is the cheaper aspect. Not having the whole absorption-desorption refinery at site is a big cost saving. So, instead of having that Capex, they will have slightly higher op-costs, because the ship and strip are loaded carbon. It costs about CAD$10/oz but they'd rather take a slight hit on their op-cost and not have the upfront capital.

Recovering Gold: Production & Shipment of Loaded Carbon

At both Santana and Cerro de Oro, initially, there will just be a basic carbon plant producing loaded carbon that will get shipped to Metals Research in Idaho who strip the Gold. Once they have a couple of plants up and running, the aim would be to buy or rent some industrial land outside Hermosillo and build an in-country refinery in a very secure location for themselves.

La Fortuna has a very different process where half the Gold is actually recovered by gravity and will create a concentrate to dip. The other 50% of the precious metals has an off-spec 17-18% Copper con, largely valued for its precious metal content. A few years ago, Minera started talks with a concentrate trader who will work with them on marketing the Copper con, to get some value for the Copper. But the value is in the precious metals contained within it. It is slightly different, more complex milling operation to deal with the higher grade at Fortuna which is another reason why the project there will be developed after the simple heap leach builds.

Timeline for Growth: What's Next?

2021 sees Minera pouring their first Gold at Santana, and then in 2022 they plan to get the asset into production at Cerro de Oro. La Fortuna has been pushed back, but it hasn't been discarded. They can bring value to La Fortuna by adding mine life and remodelling it for higher Gold prices capturing a larger initial mine life, which makes more sense for it to come on stream. Like all their other projects, Fortuna has the capacity.

In terms of sequencing, they're looking at Santana to come on next year and will get permit applications submitted early in the new year for Cerro de Oro. With the permitting environment in Mexico, they're hoping to have permits to allow construction to commence at Cerro de Oro in Q4 of next year using the cash produced by Santana.

They aim to start building at Fortuna at the beginning of 2023 so it's coming on stream right at the beginning of 2024 and it's a bigger operation than both Santana and Cerro de Oro.

Cash Position & Burn Rate

Minera raised CAD$50M in September and they have no debt. They have about CAD$22M in cash right now plus a few million dollars-worth of a non-core equity investment. That's enough to get Santana built and with existing treasury, allow them to work on the other projects and still have cash by the time Cerro de Oro is ready. They will put a working capital facility in place but might not need it.

Views for the Market in 2021

Minera knows that it’s about building a project that works at lower Gold prices as well as high prices. They, as a company, realise they need to stress-test projects as this bull Gold markeis not going to last forever.

Renting Mexico's Police Force for Mines

The Mexican government has tried to crackdown on the cartels and has introduced a scheme to rent Mexico’s police force for mine protection. In the south of the country, there is a lot of fuel theft and trucks get stolen by the cartels. Mexico is trying to tackle the problem of cartels and violence which is long overdue.

To find out more, go to the Minera Alamos Website.

Analyst's Notes

Subscribe to Our Channel

Stay Informed